Tempeh Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

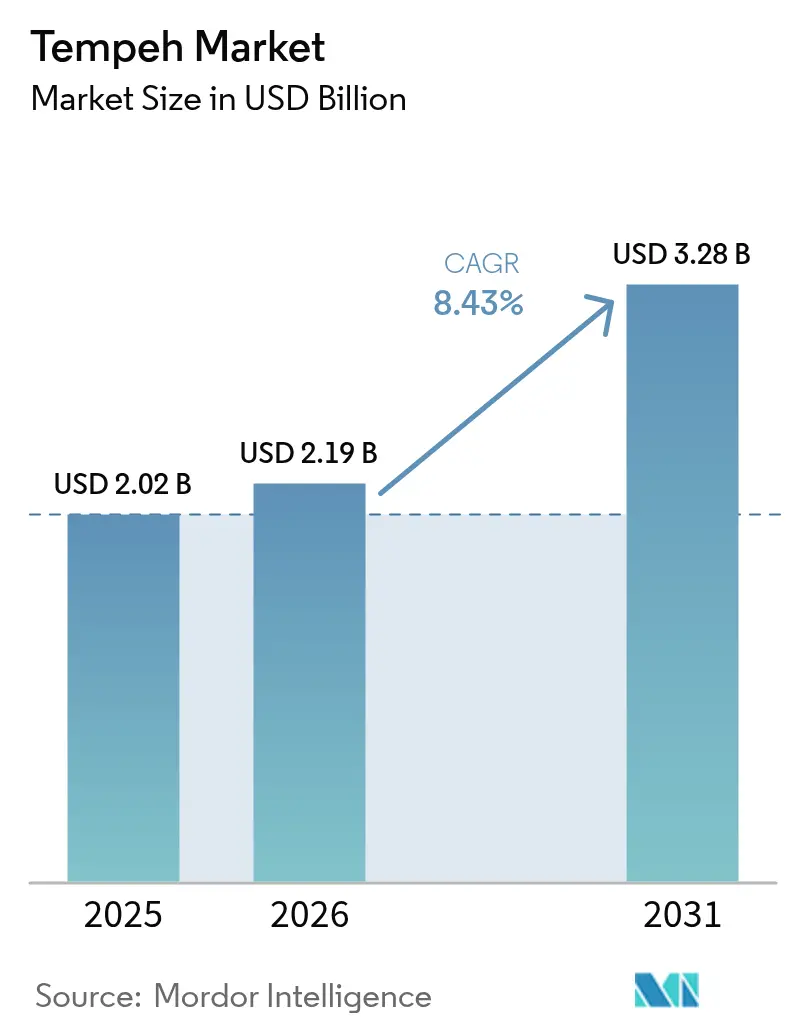

| Market Size (2026) | USD 2.19 Billion |

| Market Size (2031) | USD 3.28 Billion |

| Growth Rate (2026 - 2031) | 8.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tempeh Market Analysis by Mordor Intelligence

The tempeh market size is expected to grow from USD 2.02 billion in 2025 to USD 2.19 billion in 2026 and is forecast to reach USD 3.28 billion by 2031 at 8.43% CAGR over 2026-2031. Driven by health, environmental, and lifestyle considerations, global demand for tempeh is on the rise. The uptick in plant-based diets, coupled with heightened health awareness, underscores a consumer shift towards foods that bolster gut health, muscle development, and overall wellness. This shift also aims to mitigate meat-related health concerns, like obesity and high cholesterol. Furthermore, global demand for tempeh is surging, fueled by government initiatives championing alternative proteins (APs). In 2023, global multilateral organizations made significant commitments and expressed strong support for alternative proteins, underscoring their potential as solutions for climate and food security. This backing not only highlights the environmental advantages of alternative proteins but also fuels innovation, scales up production, and boosts consumer adoption. As a result, the global demand for tempeh is witnessing a notable surge [1]Source: The Good Food Institute, “Governments Around the World Remain Invested in Alternative Proteins,” gfi.org.

Key Report Takeaways

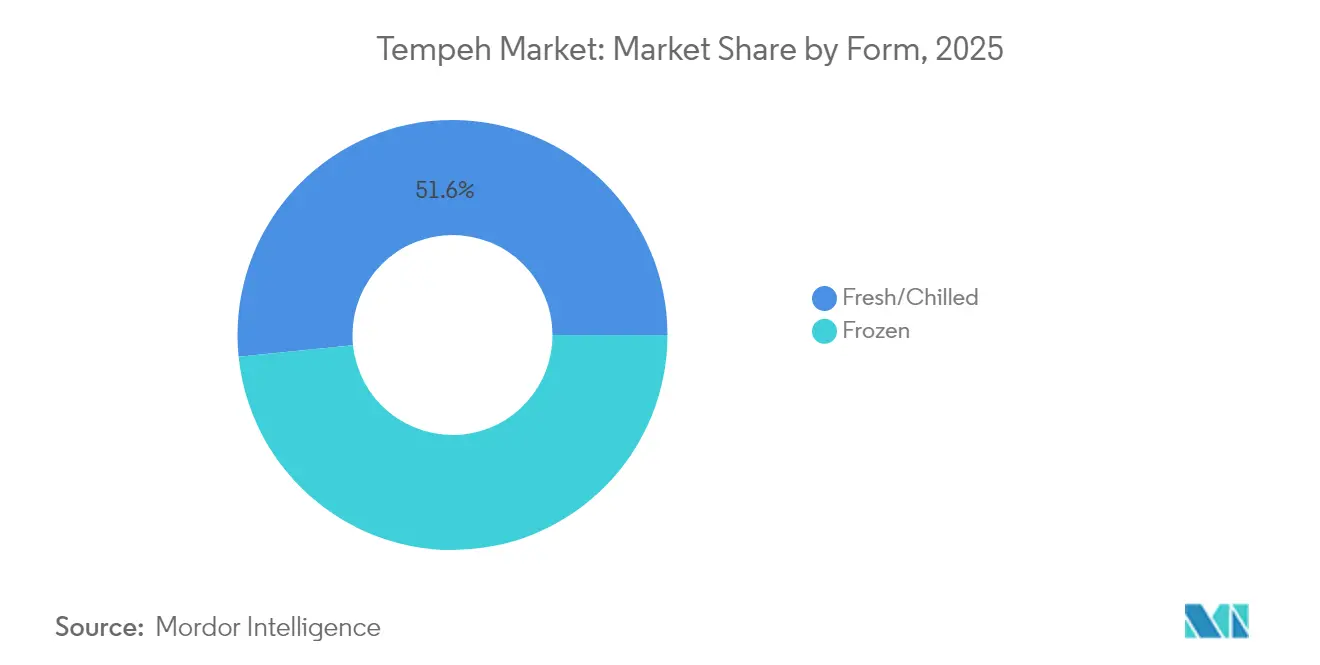

- By form, fresh/chilled products led with 51.62% of tempeh market share in 2025, whereas frozen variants are set to record the fastest 5.55% CAGR to 2031.

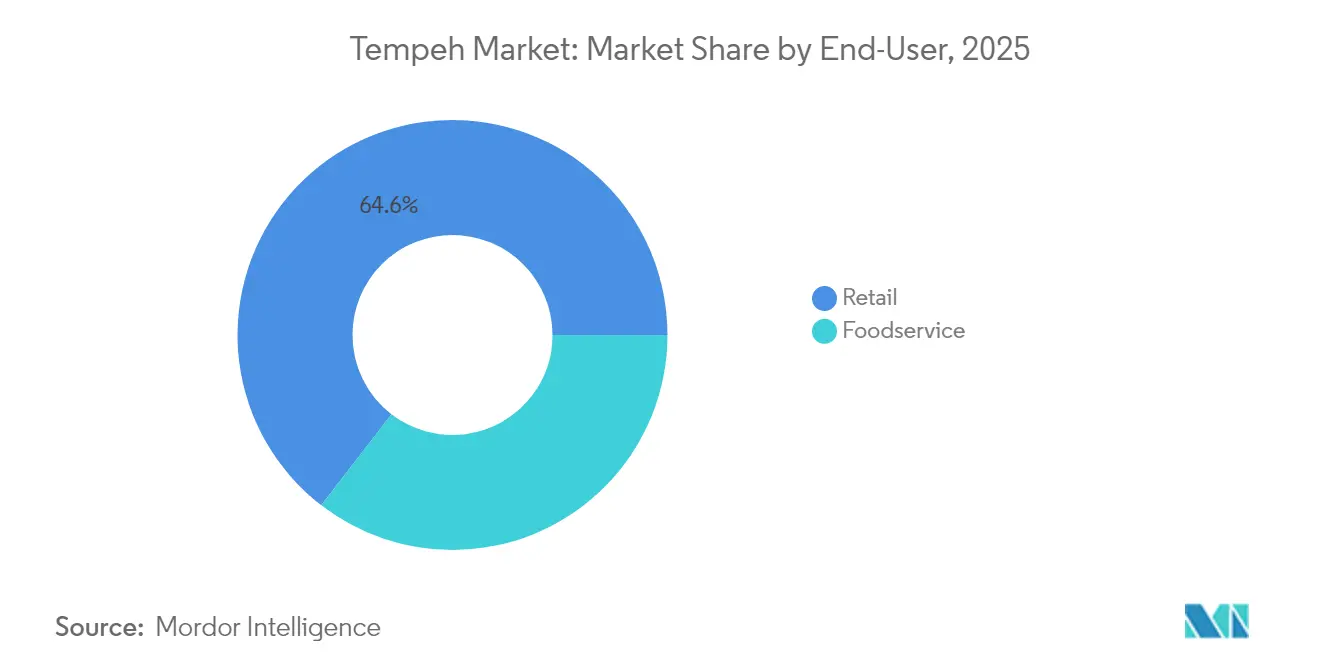

- By end-use, retail formats accounted for 64.55% of the tempeh market size in 2025, while foodservice is forecast to post a 6.02% CAGR from 2026-2031.

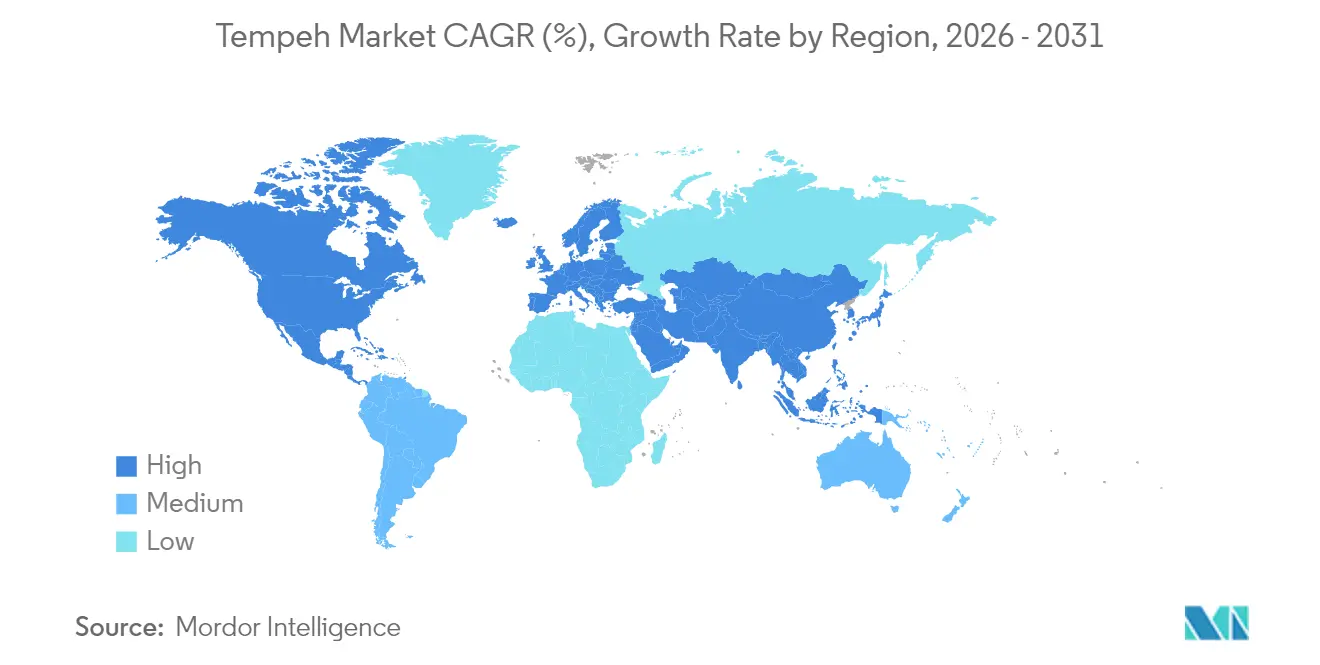

- By geography, North America dominated with 39.75% revenue share in 2025, and Asia-Pacific is expected to outpace all regions with a 12.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tempeh Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Plant-Based Diets Boosts Demand for Tempeh as a Protein-Rich Alternative | +2.1% | Global, with concentrated impact in North America and Europe | Medium term (2-4 years) |

| Rising Health Consciousness Among Consumers Favors Tempeh for Its Nutritional Benefits | +1.8% | Global, particularly strong in developed markets | Long term (≥ 4 years) |

| Innovations In Tempeh Products, Such As Flavored and Ready-To-Eat Options, Attract New Consumers | +1.5% | North America and Europe, expanding to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Increased Availability of Tempeh in Supermarkets and Online Platforms Enhances Accessibility | +1.3% | Global, with rapid Expansion in Asia-Pacific e-commerce | Medium term (2-4 years) |

| Government Initiatives Supporting Plant-Based Food Industries Promote Tempeh Production | +1.0% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Culinary Versatility of Tempeh Encourages Its Use in Various Cuisines And Recipes | +0.9% | Global, with cultural adaptation in non-traditional markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Plant-Based Diets Boosts Demand for Tempeh as a Protein-Rich Alternative

The global growth in tempeh consumption is being driven by a major shift toward plant-based eating, with flexitarian diets where consumers occasionally choose plant-based meals leading to adoption beyond traditional vegetarian groups. This shift is bolstered by mounting evidence linking plant proteins to lower chronic disease risks and better environmental outcomes. Institutional backing further solidifies this trend. The USDA’s Dietary Guidelines Advisory Committee has underscored the importance of legumes like beans, peas, and lentils, while advocating for a decrease in red meat consumption [2]Source: “2025 Dietary Guidelines Advisory Committee,” The Vegetarian Resource Group, vrg.org. Such recommendations bolster tempeh's position as a prominent protein alternative in public nutrition initiatives. Additionally, innovations in food technology have refined tempeh’s taste, texture, and convenience, broadening its appeal. As health consciousness, environmental stewardship, and evolving dietary preferences converge, tempeh is cementing its status as a staple in the global protein arena.

Rising Health Consciousness Among Consumers Favors Tempeh for Its Nutritional Benefits

Health-conscious consumers are increasingly drawn to tempeh due to its fermentation process that boosts nutritional benefits. This fermentation not only enhances the bioavailability of nutrients but also diminishes antinutrients found in raw soy, making tempeh a more digestible and nutrient-rich protein source. Unlike many ultra-processed plant-based alternatives, tempeh stands out for its whole-food integrity, aligning perfectly with the rising demand for clean-label products. This trend is further bolstered as regulatory bodies, including the FDA, redefine healthy foods to emphasize nutrient density and minimal processing. Brands like Lightlife and Tofurky, two frontrunners in the tempeh market, have adeptly tapped into this movement, promoting their products as minimally processed and abundant in natural probiotics. This strategy has resonated with consumers seeking wholesome, gut-friendly protein sources. Consequently, tempeh's presence is on the rise, gracing the shelves of both health food stores and mainstream grocery chains, underscoring its acceptance as a premium plant-based protein in the burgeoning global market.

Innovations in Tempeh Products Attract New Consumers

Product innovation is effectively addressing one of the primary barriers to tempeh adoption and consumer unfamiliarity with preparation methods by introducing convenient, user-friendly formats that enhance accessibility. Lightlife’s Tempeh Protein Crumbles, which offers tempeh in Original and Smoked Chipotle flavors, caters to consumers seeking simple, time-saving meal solutions. Similarly, Tiba Tempeh’s Smoky Block, a ready-to-eat product offering 19 grams of protein per 100 grams and infused with a smoky marinade, eliminates preparation steps while retaining organic and gluten-free certifications. These innovations reflect a broader industry shift toward prioritizing convenience and taste, which are increasingly recognized as key drivers of repeat purchase behavior, often outweighing nutritional messaging. Additionally, companies are expanding product lines to include pre-seasoned, frozen, and snackable tempeh options, further lowering the entry barrier for new consumers. This focus on ease of use and flavor variety not only broadens tempeh’s appeal across different demographics but also supports its integration into mainstream diets, accelerating market growth globally.

Increased Availability of Tempeh in Supermarkets and Online Platforms Enhances Accessibility

Cold-chain logistics are expanding, significantly enhancing the retail accessibility of tempeh. Grocers in secondary and mid-tier cities are now stocking fresh tempeh alongside tofu and seitan, making it a staple in the plant-based protein lineup. Frozen tempeh SKUs are penetrating remote or lower-density markets, areas where the slower inventory turnover once rendered fresh options impractical. This wider distribution is transitioning tempeh from niche urban health stores to mainstream retail outlets. The surge in online grocery shopping, particularly in the organic sector, has opened doors for small-scale tempeh producers. By adopting a direct-to-consumer model, these manufacturers can broaden their distribution reach, offering consumers a wider array of choices and fueling the tempeh market's growth. Furthermore, advancements in cold-chain infrastructure are curbing spoilage and prolonging shelf life. This boosts retailer confidence, encouraging them to introduce tempeh in new markets. Enhanced logistics also pave the way for partnerships between tempeh producers and major retail chains, amplifying product visibility and encouraging consumer trials across varied regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Consumer Awareness in Non-Traditional Markets Hinders Tempeh Adoption | -1.4% | Europe, North America's non-urban areas, emerging Asia-Pacific markets | Medium term (2-4 years) |

| Short Shelf Life of Tempeh Poses Distribution and Storage Challenges | -1.1% | Global, particularly affecting long-distance distribution | Short term (≤ 2 years) |

| Competition From Other Plant-Based Protein Sources Like Tofu and Seitan Affects Market Share | -0.8% | Global, with intense competition in developed markets | Long term (≥ 4 years) |

| Higher Cost Compared to Other Plant-Based Proteins May Deter Price-Sensitive Consumers | -0.7% | Price-sensitive markets globally, particularly emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Consumer Awareness in Non-Traditional Markets Hinders Tempeh Adoption

Consumer unfamiliarity with tempeh preparation and consumption methods poses a significant barrier to its market adoption, especially outside Southeast Asia. Research shows that younger demographics and those actively reducing meat consumption, who are traditionally more open to plant-based alternatives, exhibit a higher acceptance of tempeh. This trend underscores the importance for manufacturers and retailers to roll out educational initiatives and strategically position their products. This is particularly crucial for mainstream consumers who might not yet see tempeh as a viable protein alternative. Cooking demonstrations, recipe development, and clear labeling can simplify tempeh's use and showcase its versatility across various cuisines. Furthermore, collaborations with influencers and chefs can help normalize tempeh consumption, hastening its acceptance in daily diets.

Short Shelf Life of Tempeh Poses Distribution and Storage Challenges

Tempeh's refrigerated shelf life of just 7-10 days poses significant distribution and supply chain challenges, especially when juxtaposed with tofu's longer shelf life. These cold chain requirements not only elevate logistics costs but also limit market expansion, a challenge that's particularly pronounced for small-scale producers. Although technological advancements, like Plant Power's innovative packaging, have successfully extended tempeh's frozen shelf life to an impressive 210 days, there's a pressing need for consumer education and marketing to reshape perceptions regarding the quality of frozen products. Furthermore, adhering to regulatory pH standards adds another layer of operational complexity. To navigate these challenges, there's a clear imperative for investments in cutting-edge cold storage infrastructure and more efficient supply chain management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Fresh Dominance Drives Innovation

In 2025, fresh/chilled tempeh accounted for 51.62% of the market, driven by consumer preference for refrigerated fermented products. While the frozen segment represents a smaller share, it is projected to grow at a CAGR of 5.55%, supported by extended shelf life and the expansion of cold-chain infrastructure in emerging markets. As consumers increasingly view frozen foods as both convenient and nutritious, demand for frozen tempeh is surging, particularly in areas with limited access to fresh tempeh. Moreover, advancements in packaging and freezing technologies are not only boosting product quality but also preserving taste, positioning frozen tempeh as a preferred choice for retailers and consumers alike.

Fresh formats maintain a strong foothold in local and farmers-market-style distribution, where branding emphasizes minimal processing and short, transparent supply chains. Conversely, frozen variants are better suited for e-commerce and large-scale retail, where shelf stability and inventory efficiency are critical. Both segments are increasingly adopting predictive microbiology modeling, utilizing real-time sensor data to control fermentation variables and ensure flavor integrity at industrial scales exceeding 10 metric tons.

By End-Use: Retail Leadership Faces Foodservice Surge

In 2025, retail outlets captured 64.55% of the tempeh market share, driven by strategic planogram realignments in supermarkets that repositioned plant-based proteins from isolated organic sections to high-visibility primary refrigeration areas. This shift significantly boosted product exposure and shopper engagement. The retail segment is anticipated to maintain consistent growth as product lines expand to include flavored sausages, burger patties, and deli-style slices, catering to evolving consumer preferences. Moreover, retailers are teaming up with tempeh manufacturers to boost in-store sampling and promotional campaigns, leading to heightened consumer trials and repeat purchases.

Driven by a surge in consumer preference for plant-based and sustainable protein options, the foodservice segment is projected to grow at a 6.02% CAGR through 2031. As diners increasingly prioritize healthier, ethical, and environmentally friendly meals, foodservice providers are weaving tempeh into their menus. This includes a range of offerings, from vegan and vegetarian dishes to bowls, sandwiches, and protein-rich salads. In a notable move, Greenleaf Foods, the parent company of Lightlife, unveiled its “Tempeh Protein Crumbles” in 2024. Aimed squarely at foodservice operators, these crumbles serve as a versatile ingredient, seamlessly fitting into recipes from tacos to pasta sauces. This innovation not only simplifies preparation for chefs but also broadens tempeh's appeal in the culinary world.

Geography Analysis

North America dominated the global tempeh market in 2025, accounting for 39.75% of total revenue. Robust consumer adoption of plant-based proteins, coupled with advanced cold-chain infrastructure, continues to reinforce the dominance of fresh tempeh while enabling frozen SKUs to penetrate rural and lower-density regions. Governmental backing further strengthens market momentum, such as the USDA’s allocation of USD 387,000 to the University of Massachusetts Amherst for chickpea-based tempeh research, underscoring strategic investment in raw material diversification.

The Asia-Pacific region is expected to register the fastest growth, with a projected CAGR of 12.41%. Indonesia, with its rich cultural ties to soy foods, is ramping up investments in decentralized fermentation units, aiming to uplift rural livelihoods. At the same time, both China and India are showcasing a significant, untapped demand. Health-conscious urbanites in these nations are turning to e-commerce, purchasing tempeh bundles that come with localized recipe cards, making it easier for them to try and adopt the product. Furthermore, the region's tight-knit relationship with U.S. soybean export supply chains bolsters the scalability of production. Due to its deep-rooted consumption of traditional soy foods like tempeh, Indonesia has emerged as the region's top importer of food-use soybeans. In 2023 alone, Indonesia brought in 2.7 million metric tons (MMT) of soybeans for food, with over 85% sourced from the U.S .

The European tempeh market is experiencing steady growth, supported by regulatory frameworks and consumer demand for sustainable products. German retailers have increased tempeh product placement, building on an established consumer base that prefers organic and fermented foods. The French Ministry of Agriculture's inclusion of legume-based proteins in its circular economy strategy has created a favorable regulatory environment. In the United Kingdom, a Bristol-based tempeh manufacturer received funding from a GBP 1.1 million alternative protein investment initiative, indicating increased venture capital activity. The combination of government support, retail expansion, and product innovation positions the European tempeh market for double-digit growth during the forecast period.

Regulatory Landscape

Tempeh producers operate under core food safety and hygiene frameworks that shape fermentation controls, labeling, and contaminant management. Codex Alimentarius anchors this with the General Principles of Food Hygiene (CXC 1-1969) and contaminant guidance (CXS 193-1995), alongside the 2023 Codex Regional Standard for soybean products fermented with Bacillus spp. (CXS 354R-2023), which supports alignment on safety and quality expectations for fermented soybean categories in trade.

Regionally, requirements layer onto these baselines. In China, the China National Food Industry Association standard T/CNFIA 164-2022 provides tempeh-specific definitions, processing requirements, and contaminant limits that influence manufacturing and import compliance. In the EU, firms commercializing novel substrates or processes for fermented proteins work within Regulation (EU) 2015/2283, supported by EFSA scientific guidance updated in 2024 that details data expectations for novel food applications. Labeling claims for plant-based foods are also being shaped by ISO 8700:2025 (published July 16, 2025), which provides definitions and technical criteria relevant to plant-based labeling and claims.

Competitive Landscape

The global tempeh market structure is fragmented. This fragmentation creates opportunities for new market entrants to establish distinct positions through regional ingredient sourcing and product development. Maple Leaf Foods' Lightlife brand demonstrates this through its vertically integrated Indianapolis facility, which manages soybean sourcing, fermentation, and packaging operations, resulting in production efficiency and consistent product quality.

Key players in the global tempeh market, such as Nutrisoy Pty Ltd., House Foods Group Inc., and Tempeh Meades Ltd., are actively shaping the industry's landscape. Other notable names include Noble Bean Inc., Maple Leaf Foods Inc., Tootie's Tempeh, Mun Alimentos, Wiwas Tempeh LLC, and Rhapsody Natural Foods. These companies are leveraging diverse strategies to bolster their market presence. A significant emphasis on product innovation is evident, with many companies introducing flavored, seasoned, and ready-to-cook tempeh offerings. This move aims to broaden their consumer appeal and align with shifting taste preferences.

Marketing strategies are increasingly centered on ingredient provenance and sustainable production. Brands are highlighting practices such as single-origin soy sourcing and the use of regenerative agriculture, while also expanding into alternative protein bases like chickpea and lupin to cater to allergen-sensitive consumers. Rising consumer demand has drawn the attention of major food manufacturers, who are well-positioned to scale tempeh offerings through their established cold-chain logistics and plant-based portfolios.

Tempeh Industry Leaders

Tempeh Meades Ltd

Maple Leaf Foods Inc.

Nutrisoy Pty Ltd

Noble Bean Inc

House Foods Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Convenience-led formats and chilled-to-frozen portfolio expansion create whitespace for tempeh brands to move beyond traditional blocks into snackable and foodservice-friendly SKUs. As evidence, Better Nature expanded organic tempeh across hundreds of REWE stores in Germany in April 2025, illustrating mainstream distribution growth; UK-based Tiba Tempeh received GBP 1 million funding from NPIF II Maven Equity Finance in March 2025 to scale fermentation capabilities and regional supply.

Operational opportunities center on improving consistency, shelf life, and compliance as production scales. The EU Deforestation Regulation (EUDR) requires geolocation and third-party certification to verify origin, reinforcing the role of verified sourcing in tempeh positioning and market access.

Recent Industry Developments

- May 2026: Maple Leaf Foods announced plans to revive its plant-based Yves Veggie Cuisine brand, with products slated for stores in summer 2026. This signals renewed portfolio attention and retail shelf competition within plant-based proteins, where tempeh brands cross-shop with broader meat-alternative sets.

- April 2025: Better Nature expands organic tempeh across hundreds of REWE stores in Germany, underscoring rapid mainstream distribution expansion in Europe and raising tempehs profile in standard grocery channels.

- March 2024: Maple Leaf Foods Lightlife launched Tempeh Protein Crumbles in Original and Smoked Chipotle flavors, enabling easier adoption in foodservice and home cooking by reducing preparation steps and broadening tempehs use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the tempeh market is defined as the retail and foodservice sales value generated from tempeh products (fresh or chilled and frozen) across major consuming regions, measured in USD.

Scope exclusions: We exclude adjacent fermented soy foods and non-tempeh meat substitute products that are not sold as tempeh.

Segmentation Overview

- By Form

- Fresh/Chilled

- Frozen

- By End-Use

- Retail

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

- Foodservice

- Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pinning down the demand context for tempeh as a food category, and then aligning it with how products are listed and sold in trade. We review public sources such as USDA and other national agriculture agencies, FAOSTAT for crops and protein inputs, UN Comtrade for trade direction signals, and consumer price series published by statistical agencies.

To keep assumptions grounded, we also use sources such as Codex Alimentarius and food labeling regulations for category definitions, peer reviewed nutrition and food science journals for production and storage patterns (fresh or chilled versus frozen), plus company filings and investor presentations for portfolio mix and channel priorities. In selective cases, we cross-check company financials and intelligence databases, plus an import and export shipment level database, mainly to sanity check regional activity and product movement. These desk sources are illustrative only, and many other public and paid references are used for data collection, validation, and clarification throughout the research.

Primary Interviews and Surveys

Primary discussions are used to pressure test the desk assumptions that matter most, especially price positioning, channel mix (retail versus foodservice), and how often buyers switch between fresh or chilled and frozen formats. We speak with producers, distributors, ingredient and packaging participants, as well as retail and foodservice buyers across APAC, EMEA, and the Americas, so the final model reflects stated purchasing behavior rather than only published headlines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 43% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 16% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool reconstruction, where food category spending and channel level consumption signals are translated into tempeh value by region, and then reconciled back to the defined scope. In parallel, we run selective bottom-up approximations using sampled brand and private label price points, typical pack sizes, and observed assortment counts across key channels, which helps us adjust totals when the first pass looks too high or too low.

A few inputs that repeatedly shape the model include tempeh penetration within plant-based protein assortments, retail versus foodservice split, fresh or chilled versus frozen mix, average selling price progression by format, and region level consumption trends tied to plant-forward diets. When gaps show up (for example, limited visibility into smaller local brands), we fill them using informed ranges from interviews and then cap the impact using channel checks so the estimate does not drift.

For forecasting, scenario analysis is applied and then anchored to a regression-style view of drivers like price inflation, category expansion in modern retail, and menu adoption in quick service and casual dining. Growth rates are reviewed with experts so short-term spikes are not carried forward without support, and the final trajectory stays consistent with distribution and supply expansion plans.

Data Validation & Update Cycle

Validation is done through repeated triangulation across independent signals, so a single data point does not steer the total market. Analysts compare outputs against trade movement, category pricing ranges, and reported channel momentum, and then investigate anomalies such as sudden share shifts between fresh or chilled and frozen.

Before sign-off, the model goes through multi-step internal review, where assumptions are checked for consistency across regions and years, and clarifying calls are triggered if a key variable falls outside expected bounds. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity changes or significant pricing swings. Right before delivery, a final pass is completed so clients receive the latest updated view we can support.

Mordor Intelligence's Tempeh Market Sizing Compared With Other Published Estimates

Published tempeh market values often look far apart because each publisher draws the line differently around what counts as tempeh revenue, and they also vary on the year used as the anchor. Differences in channel coverage, price build-up logic, and currency timing can further widen the gap even when the story on growth looks similar.

Some estimates broaden scope by blending tempeh with a wider plant-based or fermented foods set, or by including ready-to-eat protein items that are not sold as tempeh. In Mordor Intelligence, the value is counted only for tempeh sold in fresh or chilled and frozen formats across retail and foodservice, and adjacent soy foods are kept out even if they sit in the same shelf set.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.19 B (2026) | |

| Global Consultancy A | USD 5.54 B (2025) | Uses a different base year and appears to apply a broader category treatment, which can pull in adjacent plant-based or prepared protein products and lifts the implied value versus a tempeh-only view. |

| Industry Publisher B | USD 5.17 B (2023) | Anchors the model on an earlier year and includes wider format groupings such as ready-to-eat, which can raise totals if the tempeh definition is not limited to the retail and foodservice tempeh items tracked in this study. |

The spread in the table mainly comes from how narrowly tempeh is defined, and which year and pricing structure is used to scale current value. By keeping the steps tied to observable channel activity, format mix, and price ranges that can be rechecked, our approach stays easier to replicate and explain when clients need to plan distribution or capacity.

Key Questions Answered in the Report

How big is the tempeh market today?

The tempeh market reached USD 2.19 billion in 2026 and is projected to rise to USD 3.28 billion by 2031 on an 8.43% CAGR.

Which region will grow the fastest between 2026 and 2031?

Asia-Pacific is forecast to record a 12.41% CAGR, the strongest regional growth, led by Indonesia, China, India, and Southeast Asia.

What product form is gaining momentum?

Frozen tempeh is the fastest-growing form segment, expected to post a 5.55% CAGR due to extended shelf life and e-commerce compatibility.

How is government policy supporting tempeh adoption?

USDA now credits 1 ounce of tempeh as a meat alternate in federal nutrition programs, and the United States has earmarked USD 125 million for precision-fermentation R&D.

Page last updated on: