Europe Medium And Heavy Duty Truck Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

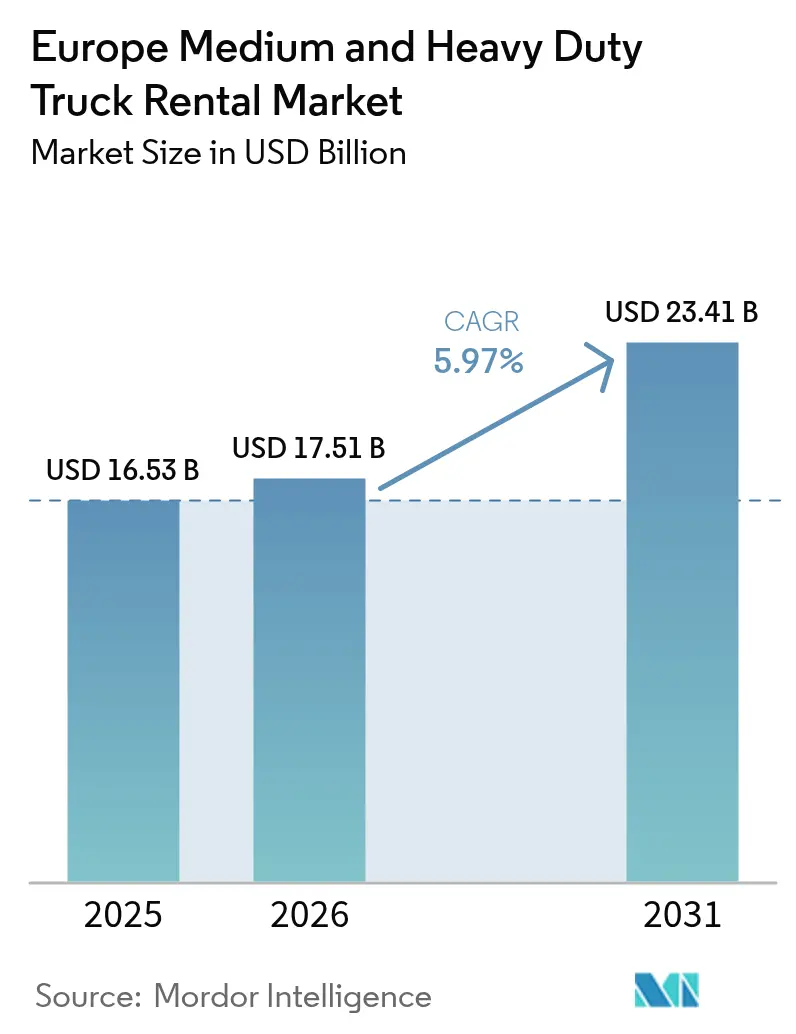

| Base Year Market Size (2025) | USD 16.53 Billion |

| Market Size (2026) | USD 17.51 Billion |

| Market Size (2031) | USD 23.41 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

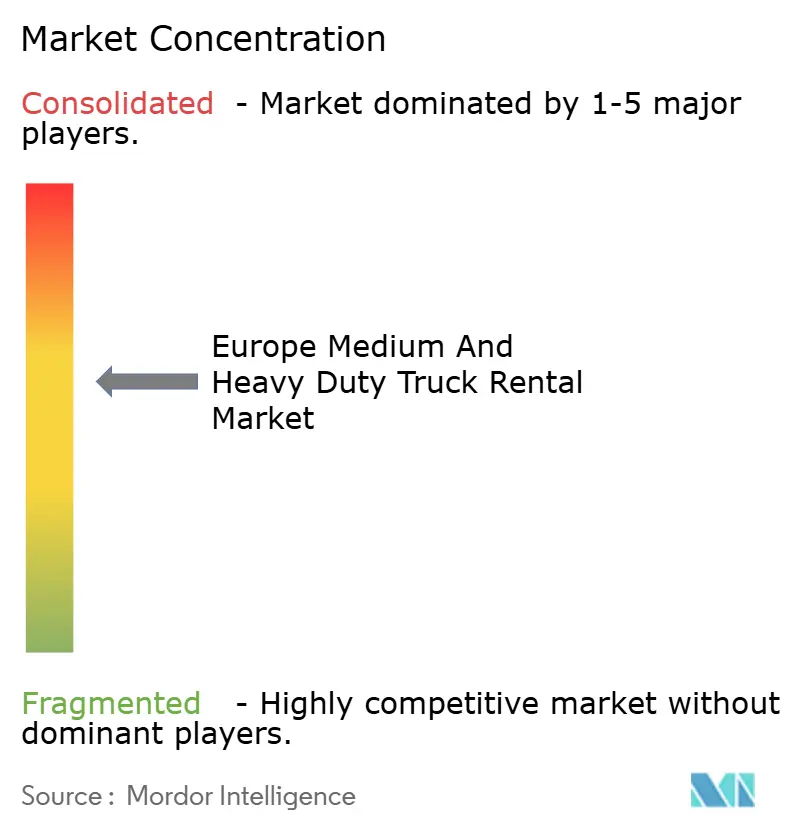

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medium And Heavy Duty Truck Rental Market Analysis by Mordor Intelligence

The Europe Medium and Heavy Duty Truck Rental Market size is projected to be USD 16.53 billion in 2025, USD 17.51 billion in 2026, and reach USD 23.41 billion by 2031, growing at a CAGR of 5.97% from 2026 to 2031. Fleet operators are increasingly turning to rental models. This shift comes as Euro 7 compliance significantly raises per-vehicle costs, increasing ownership expenses amidst volatile freight volumes. E-commerce retail sales in the five largest European economies are expected to grow substantially over the coming years. This growth creates seasonal peaks that rental fleets can manage more effectively than owned assets. Adoption of battery-electric trucks is gaining momentum, especially with the EU extending zero-emission heavy-duty toll exemptions for a longer period. This move skews the total cost of ownership in favor of electric rentals, particularly on high-toll routes. At the same time, with elevated interest rates, the weighted average cost of capital for direct purchases rises, making off-balance-sheet leasing more attractive.

Key Report Takeaways

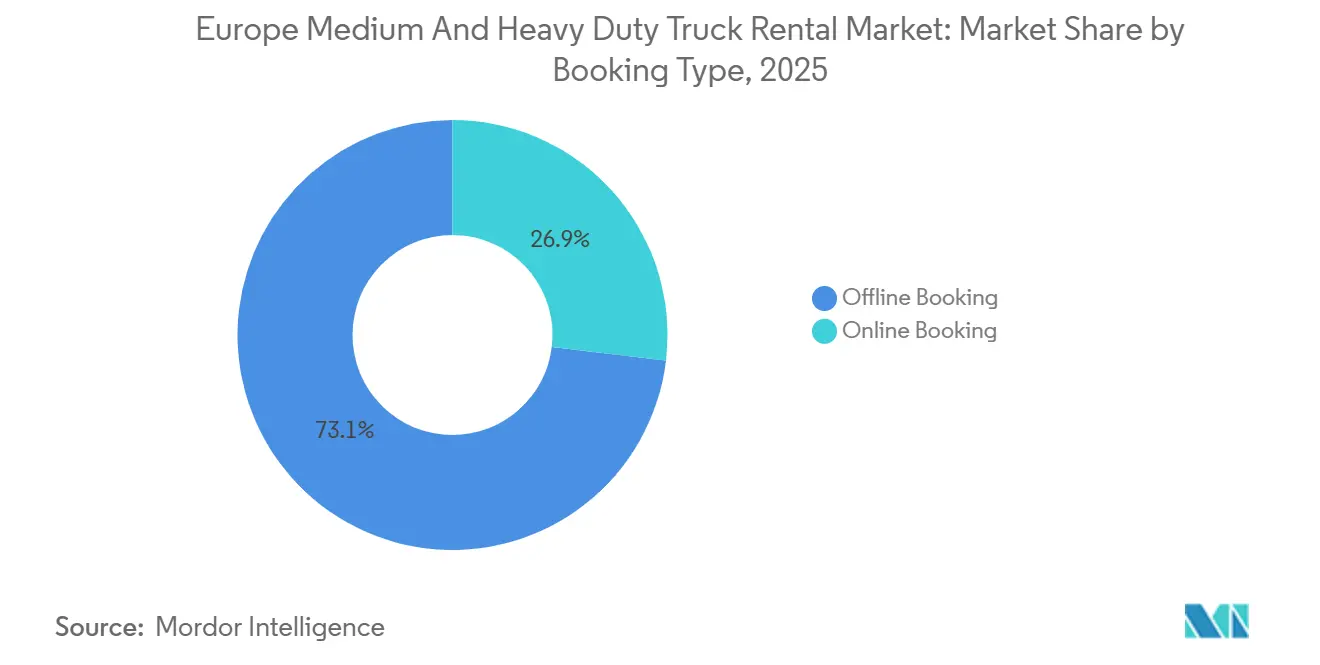

- By booking type, offline bookings held 73.14% of revenue in 2025, while online channels are projected to expand at a 5.99% CAGR through 2031.

- By rental type, long-term leasing accounted for 63.27% of 2025 revenue, while short-term contracts recorded the highest CAGR of 6.03% through 2031.

- By truck class, heavy-duty models above 16 tons accounted for 57.61% of the European medium- and heavy-duty truck rental market in 2025 and are advancing at a 6.16% CAGR through 2031.

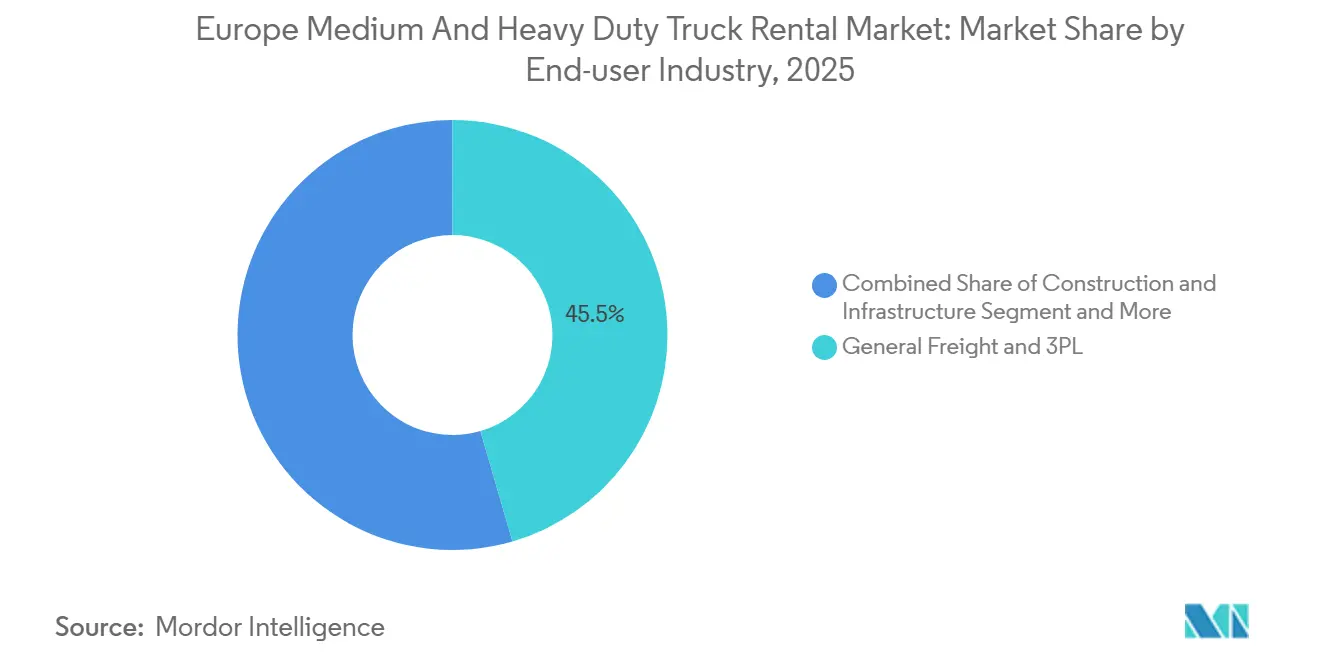

- By end-user, 3PLs account for 45.54% share in 2025, whereas postal, parcel, and E-commerce operators are expanding at a 6.07% CAGR.

- By propulsion, diesel’s 87.73% share in 2025 begins to erode as battery-electric trucks are growing at a 6.13% CAGR.

- By geography, Germany led the European medium- and heavy-duty truck rental market with 28.83% share in 2025; the Netherlands is forecast to post the fastest 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Medium And Heavy Duty Truck Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce-Led Surge | +1.2% | Germany, Netherlands, France, UK, with spillover to Poland and Spain | Short term (≤ 2 years) |

| Stricter Euro 7 Norms Favoring Rental Over Ownership | +1.1% | EU-27, with early compliance pressure in Germany, Netherlands, France | Medium term (2-4 years) |

| Cost-Avoidance Focus Amid High Interest-Rate Cycle | +0.9% | Pan-European, strongest in Germany, France, Italy | Medium term (2-4 years) |

| Subsidized E-Truck Pilots De-Risking Rental Adoption | +0.8% | Germany, France, Netherlands, Spain; pilot corridors in Scandinavia | Long term (≥ 4 years) |

| OEM "Truck-as-a-Service" Roll-Outs | +0.6% | Germany, France, Netherlands, UK; expanding to Italy and Spain | Medium term (2-4 years) |

| Cross-Border Carbon Tolls Amplifying Seasonal Demand Swings | +0.5% | EU-27, particularly high-toll corridors linking Germany, France, Benelux | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Led Surge in Flexible Freight Capacity

Online retail is expected to grow exponentially across Europe’s five largest economies by 2029, creating Black Friday, Cyber Monday, and pre-Christmas peaks that overwhelm owned fleets[1]“Weekly Retail Trade Indicators,” European Commission, ec. europa.eu . Short-term rentals are becoming the go-to solution for third-party logistics providers grappling with demand spikes. This shift is underscored by steady growth in the postal, parcel, and e-commerce segments, projected over the coming years. As cross-border orders surge within the single market, demand for heavy-duty rentals is rising, particularly on routes linking Germany, Poland, and the Netherlands. Digital platforms like Saloodo! are revolutionizing the game, enabling carriers to effortlessly book trucks for short durations. This innovation sidesteps traditional phone negotiations and allows operators to promptly return assets after delivery. Such flexibility diminishes the economic justification for ownership, a sentiment that is especially resonant among small and midsize carriers who struggle to justify year-round buffer capacity.

Stricter Euro 7 Norms Favoring Rental Over Ownership

Euro 7 regulations will significantly reduce permissible nitrogen oxide emissions compared to Euro 6d. These regulations also introduce real-world testing, resulting in a notable increase in compliance costs per vehicle. For fleets with older trucks, retrofitting expenses can become substantial. In contrast, rental contracts transfer this financial burden to major lessors, who can distribute the cost of upgrades across a large number of vehicles. Enforcement of these regulations is already intensifying in Germany and the Netherlands. In these countries, low-emission zones prohibit older truck models, further driving the trend towards rentals. OEM-affiliated lessors, like PACCAR Leasing, are capitalizing on their direct access to DAF's CF Electric and XF Electric models. This strategic advantage allows their customers to comply with the new standards without the hassle of subsidy documentation.

Cost-Avoidance Focus Amid High Interest-Rate Cycle

In early 2025, the European Central Bank's deposit rate is set at a high level, pushing financing costs higher. As a result, a diesel tractor priced at a significant amount now incurs substantial annual interest [2]“Monetary Policy Decisions,” European Central Bank, ecb. europa.eu . In Germany and France, where rising fuel and labor costs are tightening margins, long-term leases offer a lifeline. These leases not only cover maintenance, insurance, and telematics but also provide predictable monthly payments, safeguarding working capital. Moreover, leasing transfers the residual-value risk to the lessors. For instance, diesel trucks from the 2024 model year are projected to experience a significant decline in value within a few years, especially with the introduction of Euro 7 standards and the expansion of urban zero-emission zones. As a result, long-term contracts accounted for a significant portion of 2024's revenue. However, there's a notable uptick in short-term agreements as carriers seek to navigate macroeconomic uncertainties.

Subsidized E-Truck Pilots De-Risking Rental Adoption

Germany's KsNI program subsidizes a significant portion of electric truck prices, covering a large percentage of the cost up to a specified limit per unit [3]“KsNI Funding Guidelines,” Federal Ministry for Digital and Transport, bmdv.bund.de . Meanwhile, France has allocated substantial funding, allowing grants of up to a considerable amount per battery-electric truck. The Netherlands, through its DKTI scheme, provides notable financial incentives for electric trucks. Such financial backing significantly reduces the cost disparity between electric and diesel options. This has led to notable orders, including TIP Group's acquisition of a large number of electric trucks and Fraikin's ambition to secure a significant fleet of zero-emission vehicles by 2025. Additionally, with zero-emission toll exemptions valid for an extended period, the financial landscape increasingly favors electric rentals, especially on high-toll routes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residual-Value Volatility of Diesel Assets | -0.7% | Germany, France, UK, Netherlands; urban centers with zero-emission zone plans | Medium term (2-4 years) |

| Grid-Connection Delays for Depot Chargers | -0.6% | Germany, UK, Poland, Spain; infrastructure bottlenecks in Eastern Europe | Short term (≤ 2 years) |

| Driver Shortages Limiting Utilization | -0.5% | Pan-European, acute in Germany, Poland, UK | Short term (≤ 2 years) |

| Digital Freight Platforms' Asset-Light Competition | -0.4% | Germany, Netherlands, France, UK; urban logistics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Residual-Value Volatility of Diesel Assets

By the late 2020s, cities like Munich, Paris, and Amsterdam will ban Euro 6 diesel trucks from their downtown areas. This move is expected to significantly accelerate depreciation on conventional assets. As Eastern Europe and North Africa establish their own emission standards, export channels that previously absorbed aging rigs from Western Europe are shrinking. This shift leaves lessors grappling with stranded inventory. While Shell's extensive network of LNG stations provides a transitional outlet, uncertainty looms large amid a deceleration in demand amid tightening greenhouse gas targets. The Green Finance Institute's working group on residual values is crafting standardized valuation methods, but their adoption remains inconsistent. Consequently, lessors lacking access to OEM electric pipelines are squeezed, facing both declining resale prices and escalating upgrade costs.

Driver Shortages Limiting Utilization

The International Road Transport Union highlights a significant number of unfilled driver vacancies expected in the near future, with a substantial portion likely to persist further. Germany, Poland, and the UK are experiencing the most severe labor shortages, a situation worsened in the UK due to Brexit's impact on cross-border recruitment. Carriers facing understaffing challenges struggle to operate rented vehicles during peak seasons, which hampers utilization and limits demand growth. To address this issue, lessors are integrating driver-training modules and telematics-driven fuel-saving incentives into their lease packages. While these efforts provide some relief, they do not completely resolve the problem. Looking ahead, autonomous truck pilots by Scania and Einride offer a potential long-term solution. However, regulatory approval for driverless heavy-duty operations is still expected to take several years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Channels Erode Offline Dominance

Offline booking accounted for 73.14% of rental volume in 2025, a dominance rooted in direct relationship selling for complex multi-year contracts. Online portals are expanding at a 5.99% CAGR as platforms such as Saloodo! and Uber Freight automate pricing and reservation workflows. Germany and the Netherlands lead adoption because high e-commerce penetration forces logistics managers to secure trucks within hours rather than days. Dynamic price discovery on digital channels lets lessors fine-tune rates in line with regional utilization, a flexibility unattainable through phone-based negotiations.

Carriers without dedicated procurement teams gain particular value from 24/7 access and transparent tariffs, prompting small and midsize firms to shift incremental capacity online. Offline channels still dominate contracts that bundle bespoke maintenance, insurance riders, and telematics integrations, but configurators and chatbots are narrowing that service gap. The European medium and heavy-duty truck rental market benefits as digital self-service lowers transaction costs and improves fleet utilization, reinforcing the structural pivot toward data-driven asset allocation.

By Rental Type: Short-Term Flexibility Gains Ground

Long-term leasing captured 63.27% of 2025 spending because it spreads costs and embeds services, yet short-term contracts are growing at a 6.03% CAGR through 2031. Postal and e-commerce operators regularly rent trucks for one- to three-month windows to cover fourth-quarter peaks, then return assets in January. Construction firms display similar seasonality, ramping volumes in warm months and scaling back in winter. Mercedes-Benz CharterWay’s 2025 rollout of more than 100 eActros 600 tractors includes 90-day trial packages that let customers test charging logistics before committing to multiyear agreements.

Interest-rate pressure further tilts economics toward rental over ownership, with the European medium and heavy-duty truck rental market capturing operators reluctant to lock in multi-year capital commitments. Long-term leases remain indispensable for general freight carriers seeking predictable cost structures, but incremental growth leans toward flexible tenures aligned with volatile demand cycles.

By Truck Class: Heavy-Duty Assets Drive Volume and Growth

Heavy-duty vehicles above 16 tonnes accounted for 57.61% of 2025 rentals and are advancing at a 6.16% CAGR, as cross-border freight favors high payload and range. TCO parity for battery-electric tractors in 2025-2026 accelerates the segment’s electrification, aided by toll exemptions that last through 2031. Medium-duty trucks between 7.5 and 16 tonnes serve municipal and last-mile routes, but growth trails that of heavy-duty trucks because frequent stops exacerbate driver shortages and limit daily kilometers.

Rental companies prioritize heavy-duty electrics to maximize KsNI and DKTI subsidies, making them the most cost-effective compliance pathway. Medium-duty electrics such as the eEconic are gaining traction in refuse collection mandates, yet their lower annual mileage extends payoff periods. Overall, the European medium- and heavy-duty truck rental market channels capital to classes with the strongest utilization outlook and the greatest subsidy leverage.

By End-User Industry: E-Commerce Outpaces General Freight

General freight and 3PLs accounted for 45.54% of 2025 demand, underscoring their role in intra-European trade, while postal, parcel, and e-commerce operators are expanding at a 6.07% CAGR as online retail surges. DHL and UPS already lease incremental tractors each November, returning units after the holiday rush. Construction shows similar cyclical patterns tied to building-season weather, whereas FMCG fleets maintain steadier flows tied to grocery replenishment.

Zero-emission mandates are opening a niche for municipal and waste services that rent electric trucks rather than purchase assets with uncertain residual values. Volvo’s electric refuse chassis and Mercedes-Benz’s eEconic meet Paris and Amsterdam collection mandates for 2028. Seasonality creates revenue volatility for lessors, but dynamic pricing engines and predictive analytics help smooth fleet utilization, preserving margins while supporting the European medium and heavy-duty truck rental market’s diversification.

By Propulsion Type: Diesel Dominance Erodes as Electric TCO Reaches Parity

Diesel retained a 87.73% share in 2025 because fueling infrastructure is ubiquitous and upfront costs are lower. Battery-electric trucks, however, are growing at a 6.13% CAGR as KsNI, DKTI, and French subsidies compress capital outlays and the EU extends zero-emission toll relief. LNG/CNG remains a transitional niche supported by Shell’s station network but faces uncertain post-2030 emission rules. Hybrid trucks struggle to justify the complexity compared with diesel’s ever-tightening NOx controls.

Grid connection delays hamper charger rollout, with German permitting taking 18–24 months despite EUR 1.6 billion earmarked for depot infrastructure. Large lessors with balance-sheet capacity and OEM pipelines absorb the electrification risk, while smaller independents confront potential consolidation. As electric range improves and megawatt charging pilots emerge, the European medium and heavy-duty truck rental market is poised for a structural propulsion shift toward zero-emission fleets.

Geography Analysis

Germany captured 28.83% of 2025 revenue due to its central location for freight and federal charger investment. The Netherlands, however, is forecast to record a 6.11% CAGR. As the Port of Rotterdam sees its throughput expand, the DKTI subsidy now offers substantial financial support for each electric truck. France is reaping the rewards of a significant grant pool, hastening the electrification of its postal and parcel services. Meanwhile, the UK faces challenges: Brexit-induced driver shortages are limiting potential utilization gains.

While Spain and Italy experience slower growth due to fragmented logistics and a shallower e-commerce penetration, TIP Group's strategic eastward expansion is spotlighting Poland. Once merely a transit point, Poland is now emerging as a pivotal bridge to Ukraine and the Baltics, poised for above-average growth, bolstered by EU cohesion funds. In Scandinavia, autonomous electric trucks are being piloted on less-trafficked corridors. In contrast, Eastern Europe remains tethered to diesel, hampered by sparse charging networks.

Carbon pricing introduces another layer of complexity. Starting in the near future, the ETS extension will increase diesel operating costs. This shift makes battery-electric rentals increasingly appealing, especially on toll-heavy routes connecting Germany, France, and Benelux. In urban centers like Munich, Paris, and Amsterdam, zero-emission zones are tightening the resale windows for diesel assets. This pressure is pushing lessors to accelerate their electrification efforts to safeguard their balance sheet values. Furthermore, Germany's automated license-plate recognition system is ensuring compliance, setting a precedent that other EU member states are beginning to follow.

Competitive Landscape

In the European medium- and heavy-duty truck rental market, TIP Group stands out with its extensive fleet, claiming the largest independent share but accounting for only a relatively small portion of the market's revenue. Meanwhile, OEMs are innovating: Mercedes-Benz CharterWay bundles a significant number of eActros 600 tractors into its Truck-as-a-Service, complete with maintenance, insurance, and telematics, sidestepping traditional lessors. On another front, PACCAR Leasing taps directly into DAF CF Electric units, offering fleets compliant with Euro 7 standards, all without the hassle of customer subsidy paperwork.

Digital freight platforms are shaking up the scene by introducing asset-light competition through the aggregation of third-party capacity. Notably, DKV Mobility’s Saloodo! and Uber Freight’s European division harness real-time matching algorithms, boosting fleet utilization but tightening rental margins. In response, lessors are turning to predictive analytics, cutting downtime significantly, and employing dynamic pricing engines to navigate demand fluctuations.

Strategic moves in the market are increasingly centered on scaling electric fleets. TIP Group has placed a substantial order for electric trucks, while Fraikin aims to secure a notable number of zero-emission units in the near future. Smaller players are eyeing mergers or partnerships with OEMs to mitigate the costs of Euro 7 compliance. Additionally, ACEA’s suggested open telematics standard, if embraced, could democratize data integration, leveling the competitive playing field.

Europe Medium And Heavy Duty Truck Rental Industry Leaders

TIP Group

Fraikin SAS

Ryder System Inc.

Penske Truck Leasing

PACCAR Leasing Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Daimler Truck Financial Services Germany launched eService Leasing, a comprehensive package that combines financing, service contracts, and optional add-ons. This offering is designed to simplify the adoption of electric trucks by addressing key operational and financial challenges businesses face when transitioning to electric mobility.

- June 2025: Through Hylane's Transport-as-a-Service framework, DHL Group has signed a deal for 30 Mercedes-Benz eActros 600 units. This agreement aligns with DHL's commitment to sustainable logistics and reducing carbon emissions in its operations. Deliveries of these electric trucks are scheduled to commence by Q2 2026, marking a significant step toward the adoption of eco-friendly transportation solutions.

Europe Medium And Heavy Duty Truck Rental Market Report Scope

The scope of the report includes Booking Type (Offline and Online), Rental Type (Short-term and Long-term), Truck Class (Medium-Duty and Heavy-Duty), End-user (Freight/3PL and More), Propulsion (Diesel and More), and Geography.

| Offline Booking |

| Online Booking |

| Short-term Leasing |

| Long-term Leasing |

| Medium-Duty (7.5-16 t) |

| Heavy-Duty (Above 16 t) |

| General Freight and 3PL |

| Construction and Infrastructure |

| Retail and FMCG |

| Postal, Parcel and E-commerce |

| Waste and Municipal Services |

| Diesel |

| Battery-Electric |

| LNG / CNG |

| Hybrid |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Poland |

| Rest of Europe |

| By Booking Type | Offline Booking |

| Online Booking | |

| By Rental Type | Short-term Leasing |

| Long-term Leasing | |

| By Truck Class | Medium-Duty (7.5-16 t) |

| Heavy-Duty (Above 16 t) | |

| By End-user Industry | General Freight and 3PL |

| Construction and Infrastructure | |

| Retail and FMCG | |

| Postal, Parcel and E-commerce | |

| Waste and Municipal Services | |

| By Propulsion Type | Diesel |

| Battery-Electric | |

| LNG / CNG | |

| Hybrid | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the European medium and heavy-duty truck rental market in 2031?

It is forecast to reach USD 23.41 billion by 2031.

Which truck class is growing fastest in Europe’s rental segment?

Heavy-duty vehicles above 16 tonnes are expanding at a 6.16% CAGR through 2031.

Why are battery-electric rentals gaining traction among European carriers?

Subsidies in Germany, France, and the Netherlands compress upfront costs, while zero-emission toll exemptions through 2031 lower operating expenses.

How are rising interest rates influencing rental demand?

Policy rate elevates financing costs for purchases, making off-balance-sheet leasing more attractive.

Which European country shows the fastest rental market growth?

The Netherlands is projected to record a 6.11% CAGR from 2026 to 2031 due to port expansion and generous DKTI subsidies.

What major challenge limits rental fleet utilization in the near term?

Shortage of commercial drivers across Europe constrains how many rented trucks can be staffed and operated.

Page last updated on: