Term Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.52 Trillion |

| Market Size (2031) | USD 2.32 Trillion |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Term Insurance Market Analysis by Mordor Intelligence

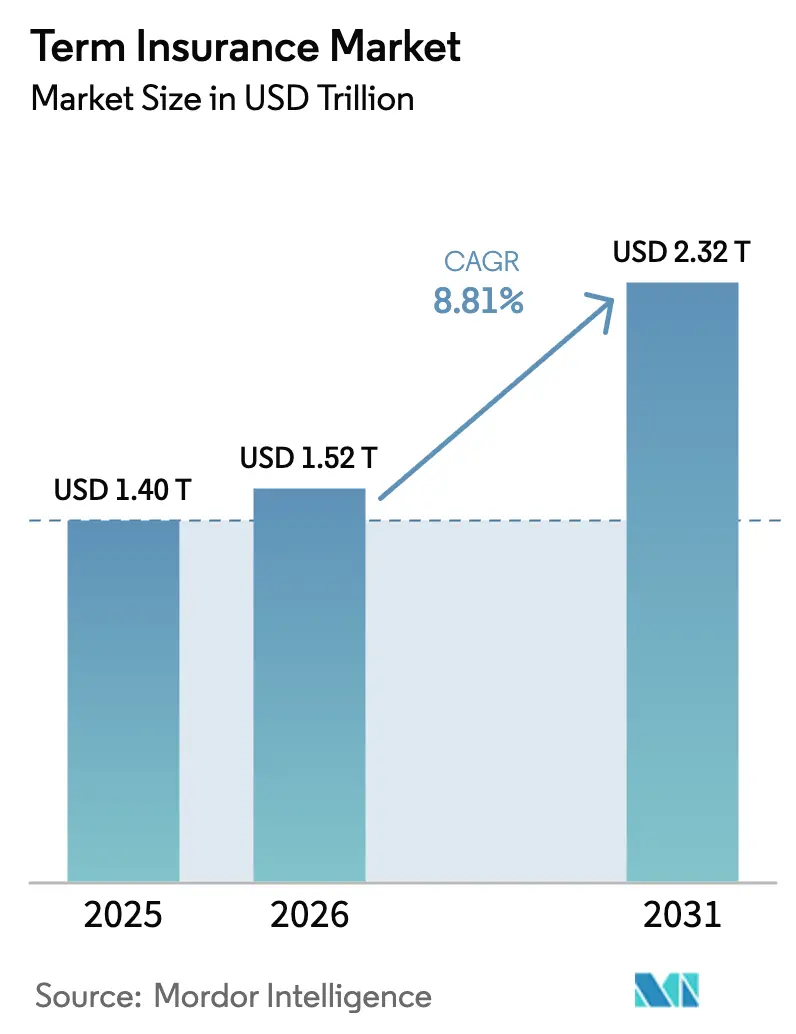

The term insurance market size was valued at USD 1.40 trillion in 2025 and estimated to grow from USD 1.52 trillion in 2026 to reach USD 2.32 trillion by 2031, at a CAGR of 8.81% during the forecast period (2026-2031). Continuous digitalisation, rising middle-class prosperity in Asia-Pacific and Africa, and supportive tax rules in North America and Europe underpin this trajectory. Direct-to-consumer portals are expanding at 16.20% CAGR as self-service buying habits spread from retail banking into life protection. Wearable-enabled underwriting and embedded micro-covers widen addressable demand while lowering acquisition costs. Meanwhile, insurers respond to low-yield pressures by re-tooling capital management, partnering with reinsurers, and focusing on protection-only products that carry limited investment guarantees.

Key Report Takeaways

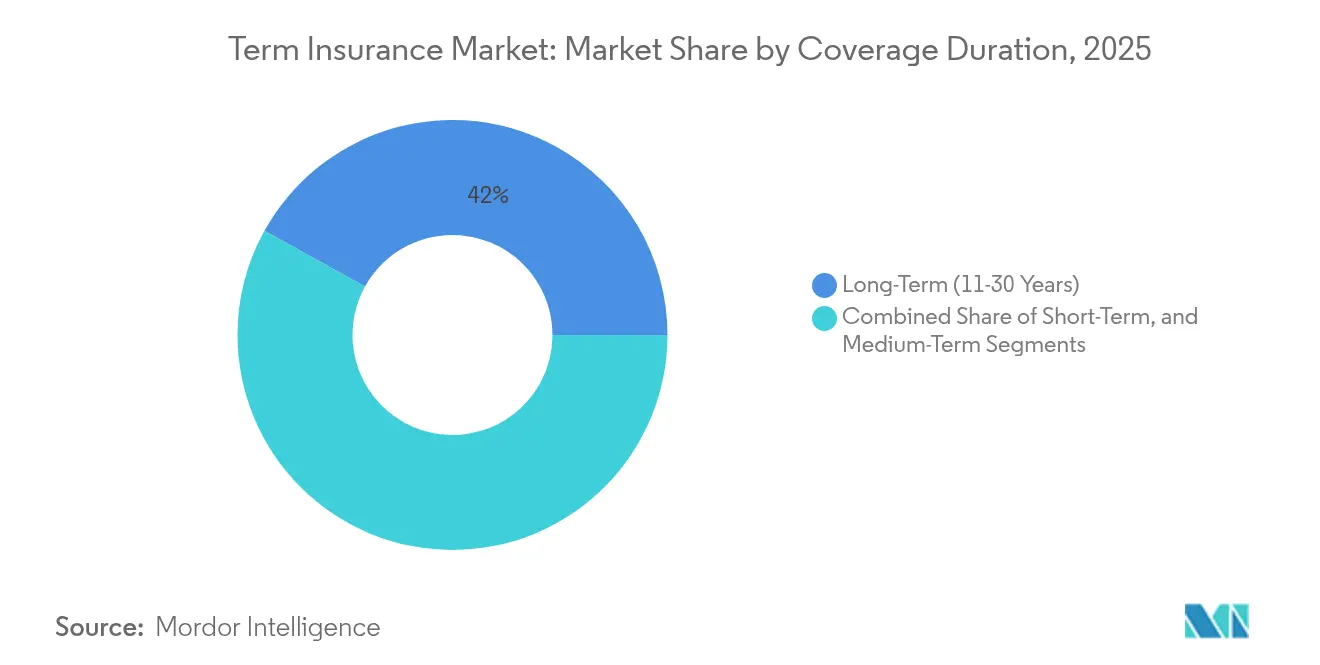

- By coverage duration, long-term policies (11–30 years) held a 41.95% term insurance market share in 2025, whereas short-term covers (≤5 years) are growing at 8.28% CAGR to 2031.

- By age group, the 31–45 cohort accounted for 37.15% of the term insurance market size in 2025; the 18–30 segment registers the fastest growth at 9.62% CAGR.

- By distribution, independent agents retained 52.95% of the term insurance market share in 2025, yet direct-to-consumer channels deliver a 15.85% CAGR.

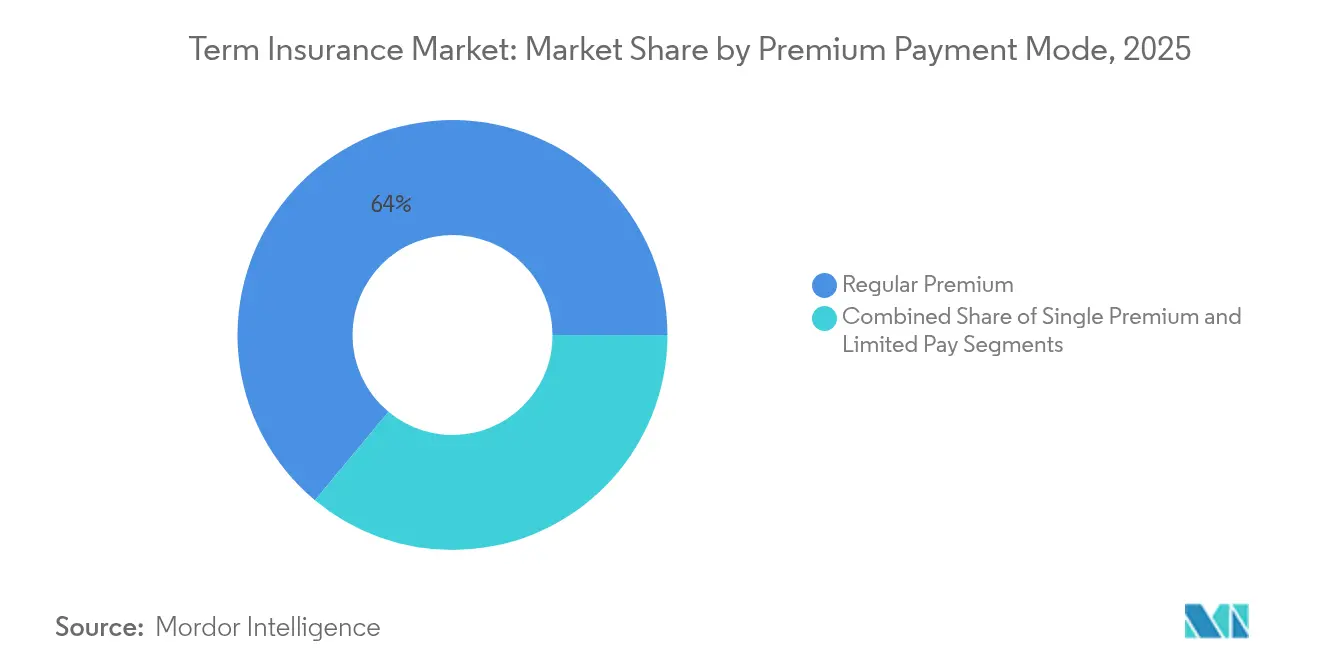

- By payment mode, regular-premium plans dominated with 63.95% share of the term insurance market size in 2025; single-premium products lead growth momentum.

- By end user, individual cover represented 71.85% of the term insurance market size in 2025 and is rising at 8.74% CAGR through 2031.

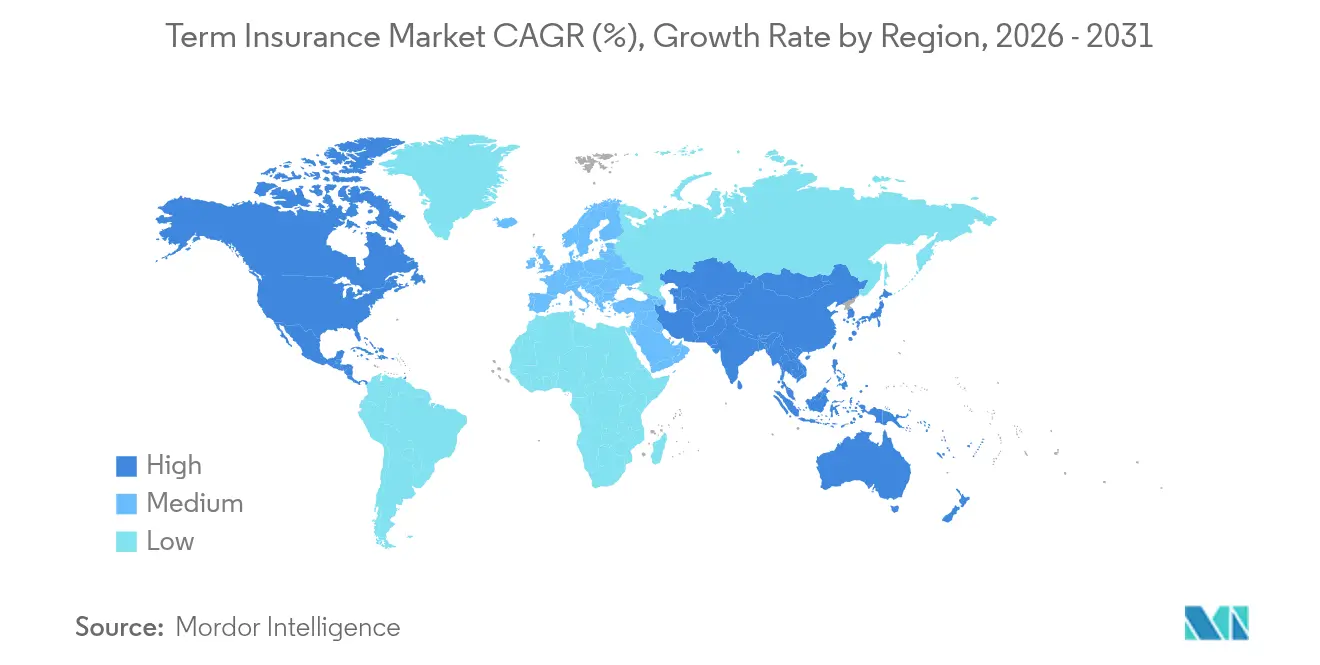

- By geography, North America led with 33.72% revenue share in 2025, while Asia-Pacific posts the highest 9.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Term Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic surge in digital purchasing of low-ticket term policies | +1.8% | Global with North America and Asia-Pacific clusters | Short term (≤ 2 years) |

| Rising middle-class income and protection gap in emerging APAC and Africa | +2.1% | Asia-Pacific core; spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Embedded-insurance launches by fintech and super-apps | +1.5% | Global; early adoption in Asia-Pacific and North America | Medium term (2–4 years) |

| Accelerated underwriting via real-time health and wearables data | +1.2% | North America and EU; expanding to Asia-Pacific | Medium term (2–4 years) |

| Tax-efficient retirement and legacy-planning regulations | +0.9% | EU and North America; selected Asia-Pacific markets | Long term (≥ 4 years) |

| Wider availability of micro-term covers through insurtech MGAs | +1.3% | Global with focus on emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic surge in digital purchasing of low-ticket term policies

Direct-to-consumer storefronts accelerated once in-person sales channels shut during lockdowns. The experience convinced both carriers and customers that simple life covers can be quoted, underwritten, and bound entirely online within minutes. HealthGuard Insurance Solutions’ January 2025 platform launch illustrates the one-stop approach that compares multiple carrier rates and binds coverage in real time[1]HealthGuard Insurance Solutions, “One-stop online life insurance marketplace launches,” healthguard.com. Younger buyers appreciate transparency and the absence of pressure, so online conversion rates remain high. Insurers that combine friction-free interfaces with robust data analytics now acquire policyholders at lower cost than agent networks. The challenge is avoiding price-led commoditisation by wrapping covers with wellness perks or loyalty programmes.

Rising middle-class income and protection gap in emerging APAC and Africa

A fast-growing middle class across Asia-Pacific and parts of Africa is translating higher disposable income into first-time life cover purchases. Life insurance penetration in many Latin American markets remained below 15% in 2024, highlighting the latent runway for basic risk protection. China Pacific Insurance recorded RMB 228.842 billion (USD 31.8 billion) in life premiums during the first 11 months of 2024, supported by wage growth and urbanisation. Insurers must balance affordability with sound risk margins because standard Western pricing tables often over-price emerging-market risks. Simplified-issue micro-covers and mobile payments are bridging this gap. Long-term upside remains highest where regulators champion inclusive insurance and grant tax relief on minimal-ticket covers.

Embedded-insurance launches by fintech and super-apps

Embedding term cover within digital payments or e-commerce journeys offers instant protection at the point of need. PayPal Ventures’ USD 13 million investment in Olé Life underlines fintech interest in bundling protection with financial transactions. Super-apps in Southeast Asia offer click-through life covers when users book rides or transfer money, leveraging rich behavioural data to pre-fill applications. The embedded model slashes distribution costs, allowing unit premiums as low as USD 5 annually for accidental death. Regulatory complexity is its main hurdle, demanding joint licences or authorised intermediaries in each jurisdiction. Success hinges on transparent disclosures that secure user trust while keeping user journeys frictionless.

Accelerated underwriting via real-time health and wearables data

Artificial intelligence and wearable sensors shorten underwriting from weeks to minutes. A newly patented pre-qualification engine by Insurance Software Automation cut placement times by 15% and boosted issue rates by 25% in pilot tests. Continuous data feeds enable dynamic risk scoring that rewards healthy lifestyles with premium discounts. Younger policyholders accept data sharing in exchange for personalised pricing, though regulators enforce strict consent and storage protocols. Insurers gain improved selection and lower claims ratios, yet must articulate clear boundaries on data usage. Widespread adoption could eventually realign actuarial tables to real-time biometric trends rather than historic averages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commoditised pricing pressure and rate-shopping platforms | -1.4% | Global, especially mature markets | Short term (≤ 2 years) |

| Prolonged low-yield environment squeezing insurer capital buffers | -1.1% | Global, strongest in EU and Japan | Medium term (2–4 years) |

| Persistent “too-expensive” perception among Gen Z and low-income groups | -0.8% | Global, concentrated in developed regions | Long term (≥ 4 years) |

| Data-privacy rules limiting behavioural-data underwriting | -0.6% | EU and North America; spreading worldwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Commoditised pricing pressure and rate-shopping platforms

Online aggregators have turned life cover into a transparent commodity where premiums are displayed side by side. Consumers benefit from competition but continuous repricing narrows underwriting margins within standard risk classes. Fierce price rivalry encourages some carriers to relax underwriting thresholds to maintain volume, raising potential adverse-selection losses. As a counter-measure, firms add wellness coaching, accelerated claims or flexible riders to differentiate on value rather than cost alone. Long-run profitability depends on creating service ecosystems that make switching inconvenient despite marginal price gaps.

Prolonged low-yield environment squeezing insurer capital buffers

Sustained low interest rates depress the investment returns that historically subsidised mortality risks. With bond yields lagging, insurers boost reliance on underwriting surplus, pressuring risk selection tightening and premium increases. Swiss Re estimated supply-chain disruptions cost corporates USD 184 million annually, underscoring external shocks that further squeeze solvency[2]Insurance Business, “China Pacific Insurance posts steady 2024 premium growth,” insurancebusinessmag.com. Reserve strengthening for legacy guarantees ties up capital that could fund new policy growth. Some carriers offload closed books to consolidators to unlock capital, yet persistently thin spreads keep pricing discipline tight. Rate upticks would relieve strain, but strategic planning assumes muted yields through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Duration: Short-term Products Drive Innovation

Long-term policies captured 41.95% of the term insurance market in 2025, reflecting demand for predictable cover that aligns with mortgage and childcare commitments. Short-term products are advancing at 8.28% CAGR to 2031 as consumers favour flexible protection aligned with gig-working cycles. Medium-term tenures function as transition solutions when life stages shift faster than once-traditional career paths.

Short-term growth stems from insurtech MGAs that wrap parametric triggers into mobile apps, offering instant pay-outs after defined events. Guardian Life’s SafeGuard360 bundles life, disability, and long-term care into one policy, signalling how hybrid designs blur segment boundaries. The evolution suggests that fixed duration buckets may fade as modular riders enable policyholders to re-scale cover without lengthy re-underwriting. Insurers that master data-driven pricing of micro-terms now influence wider market standards.

By Age Group: Youth Adoption Accelerates Digital Transformation

The 31–45 cohort retained 37.15% share of the term insurance market in 2025, mirroring peak household formation and debt obligations. The 18–30 group is expanding at 9.62% CAGR, powered by embedded offers within super-apps and buy-now-pay-later ecosystems. Older demographics continue steady uptake for estate planning but seldom drive volume spikes.

Digital-native buyers expect instant quotes, transparent pricing, and chat-first service. A survey revealed 96% of Gen Z research life cover online while 84% prefer embedded offers at the point of car purchase. Winning carriers blend gamified wellness with flexible sum-assured top-ups that adapt as incomes rise. This cohort’s loyalty will shape lifetime customer value, making early acquisition critical. Carriers slow to redesign journeys risk ceding market relevance for decades.

By Distribution Channel: Digital Disruption Reshapes Sales Models

Independent agents still delivered 52.95% of term insurance market revenue in 2025 thanks to trusted advice for complex needs. Yet direct-to-consumer portals post 15.85% CAGR as self-directed buying normalises across demographics. Bancassurance expands steadily by cross-selling through existing banking relationships while affinity programmes ride employer benefits modernisation.

Canada Life’s partnership with CapIntel showcases how incumbents digitise comparative tools for both advisers and retail clients. A multichannel equilibrium is emerging where human guidance coexists with algorithmic steering. Carriers allocate marketing budgets dynamically, steering high-sum policies toward agents and simpler covers online. The dividing line is no longer product type alone but buyer confidence, ticket size, and required personalisation.

By Premium Payment Mode: Single-premium Growth Signals Wealth Accumulation

Regular-premium contracts dominated 63.95% of term insurance market payments in 2025, suiting predictable household budgeting. Single-premium uptake grows swiftly among affluent customers who prefer immediate cover activation and reduced administrative tasks. Limited-pay designs appeal to planners aiming to finish premium obligations before retirement.

Wealth accumulation in emerging middle classes and higher net-worth tiers fuels lump-sum affordability. Voya’s Lifetime Life Insurance lets employees convert group term into individual cover with optional living benefits, marrying payment flexibility with protection continuity. Insurers refine actuarial engines to capture one-time premiums while ensuring risk alignment across policy tenure.

By End User: Individual Coverage Maintains Dominance

Individual policies held 71.85% of the term insurance market in 2025, reflecting personalisation needs that group schemes rarely address fully. Group plans grow through HR modernisation as employers widen wellness and protection packages.

LIMRA projects cautious optimism for workplace life cover in 2025, noting that tailored rider options can boost employee uptake. Carriers designing modular group offers that employees can upscale at personal cost enjoy higher penetration. Nonetheless, individual decision-making remains core, especially in regions where gig work limits access to corporate benefits.

Geography Analysis

North America registered 33.72% share of the term insurance market in 2025, underpinned by mature distribution networks, well-capitalised carriers, and favourable tax treatments for death-benefit proceeds. Growth leans on product upgrades like living-benefit riders and accelerated underwriting rather than new-to-market demand. Legal & General’s USD 2.3 billion divestiture of its US term platform to Meiji Yasuda in February 2025 underscores consolidation that refocuses portfolios while signalling ongoing attractiveness to foreign entrants.

Asia-Pacific delivers the highest 9.63% CAGR, driven by urbanisation, wage inflation, and regulatory encouragement of risk protection. China Life topped regional carriers with 9% market-cap growth to USD 99.50 billion in Q2 2024. Bancassurance remains a pivotal channel as shown by AIA Vietnam’s alliance with HSBC, granting immediate branch access. Localisation of product language and digital KYC tools are prerequisites for multi-jurisdiction growth given divergent regulatory frameworks.

Europe, the Middle East, and Africa display uneven trajectories. EU markets benefit from Solvency II frameworks and cross-border passporting that enable scale efficiencies, yet subdued GDP growth tempers premium expansion. The Middle East shows only 0.2% life-insurance penetration despite projected 2.1% GDP growth for 2024, revealing structural headroom. Africa’s USD 60.19 billion life and non-life premiums in 2020, of which South Africa commanded 67.5%, highlight concentration yet point to latent continental potential. Carriers that invest early in digital onboarding for thin-file customers can leapfrog legacy branch constraints.

Competitive Landscape

The term insurance market is moderately concentrated as global incumbents defend share while specialised insurtechs carve niches. Allianz, AXA, and Prudential combine decades of mortality data with omni-channel reach to retain pricing power. At the same time, digital natives like Lemonade or Ethos employ AI underwriting and mobile-only journeys that resonate with millennial buyers.

Strategic priorities converge on technology integration, partnership expansion, and capital optimisation. Allstate’s patented machine-learning engine that tailors driving-linked life guidance illustrates how incumbents harness data science to refresh propositions. Reinsurer alliances, such as Protective Life’s USD 9.7 billion deal with Resolution Life in March 2025, free surplus for growth while reducing long-duration risk. In emerging markets, cooperative models with telcos or wallets unlock hard-to-reach segments where pure-play insurers lack embedded distribution.

White-space opportunities remain in micro-term covers for gig workers, hybrid protection-investment products for affluent millennials, and wellness-linked riders that monetise behavioural data. Market entry barriers stay meaningful due to solvency capital requirements and brand trust, yet agile digital entrants can still command customer loyalty in underserved niches. Success rests on orchestrating seamless digital journeys without sacrificing actuarial rigour or regulatory compliance.

Term Insurance Industry Leaders

New York Life Insurance Company

Northwestern Mutual Life Insurance Company

MetLife Inc.

Prudential Financial Inc.

Massachusetts Mutual Life Insurance Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allianz, BlackRock, and T&D Holdings agreed to acquire Viridium Group for EUR 3.5 billion (USD 3.8 billion), boosting closed-book consolidation capabilities.

- February 2025: Legal & General sold its US term life businesses Banner Life and William Penn to Meiji Yasuda for USD 2.3 billion, forming a strategic US-Japan partnership.

- February 2025: Securian Financial introduced Eclipse Accumulator II indexed universal life, adding new indices while keeping low expense charges.

- January 2025: AmeriLife acquired Crump Life Insurance Services, gaining access to 31,000 financial professionals and USD 13 billion in annual placed premiums.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the term insurance market as all stand-alone, fixed-period life policies whose premiums purchase only pure mortality protection. Any contract embedding investments, savings, or return-of-premium features is excluded. Coverage spans individual and group contracts sold through digital direct, intermediated, bancassurance, and workplace channels across six regions.

Scope exclusion: mortgage-linked decreasing term riders and credit-life covers bundled with loans lie outside this assessment.

Segmentation Overview

- By Coverage Duration

- Short-Term (Less Than 5 Years)

- Medium-Term (6-10 Years)

- Long-Term (11-30 Years)

- By Age Group

- 18-30 Years

- 31-45 Years

- 46-60 Years

- 60+ Years

- By Distribution Channel

- Direct-to-Consumer / Online

- Independent Agents and Brokers

- Bancassurance

- Affinity / Workplace

- By Premium Payment Mode

- Single Premium

- Regular Premium

- Limited-Pay

- By End User

- Individual

- Group

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with underwriting heads, reinsurer actuaries, insurtech founders, and broker principals across North America, Europe, and Asia-Pacific. These conversations clarified digital ticket sizes, emerging health-data underwriting thresholds, and real-world lapse patterns, filling gaps that documents alone could not bridge.

Desk Research

We began by mining regulator solvency returns, OECD Insurance Statistics, Swiss Re sigma premium books, and reinsurer disclosures that split premiums by product line. Annual reports, 10-Ks, and investor decks from the top twenty carriers supplied average sums assured, lapse ratios, and channel splits, while trade bodies such as the Global Federation of Insurance Associations contributed granular distribution data. Subscription tools, including D&B Hoovers for financials and Dow Jones Factiva for news signals, helped verify pricing shifts and M&A moves. The sources listed are illustrative; many additional open datasets informed baseline figures and narrative checks.

Market-Sizing & Forecasting

The model starts with reported first-year and renewal term premiums by country (top-down). We then reconcile them against sampled average premium rates multiplied by in-force policy counts gathered through carrier roll-ups and channel checks (bottom-up) to validate totals. Key variables include household penetration rates, per-capita disposable income, median face value, digital share of new sales, and mortality-linked reinsurance pricing. Forecasts blend multivariate regression with scenario analysis so income growth and digital adoption drive premium elasticity, while expert-validated mortality and lapse trends temper upside. Where carrier data were incomplete, three-year moving averages of regulator prints bridged shortfalls.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review, anomaly flags trigger re-contact with respondents, and models refresh annually. Interim updates are issued when regulatory or macro events move premiums by more than three percent.

Why Mordor's Term Insurance Baseline Stands Unmatched in Reliability

Published estimates often diverge because providers select unequal product baskets, currency bases, and refresh cadences, causing totals to vary before any forecasting begins.

Key gap drivers include the inclusion of credit-life and rider revenues by some publishers, earlier base years that remain unadjusted for inflation, and limited validation of direct-to-consumer volumes outside the United States.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.40 Tn (2025) | Mordor Intelligence | |

| USD 2.05 Tn (2025) | Global Consultancy A | Combines credit-life and mortgage riders; relies on single-source regulator data |

| USD 1.14 Tn (2024) | Industry Journal B | Earlier base year without FX or inflation normalization; omits Asia digital channels |

| USD 1.26 Tn (2025) | Market Think Tank C | Counts only 25 countries, leaving emerging markets unmodeled |

In sum, Mordor's disciplined scope selection, dual-track modeling, and annual refresh deliver a balanced, transparent baseline that ties every dollar back to observable premiums and repeatable steps, giving decision-makers confidence in our numbers.

Key Questions Answered in the Report

What is the current size of the term insurance market?

The term insurance market is valued at USD 1.52 trillion in 2026 and is projected to climb to USD 2.32 trillion by 2031.

Which region is growing fastest in term life protection?

Asia-Pacific is pacing the field with a 9.63% CAGR through 2031, driven by rising household incomes and supportive regulation.

How are digital channels affecting term insurance sales?

Direct-to-consumer platforms are expanding at 15.85% CAGR, reducing acquisition costs and meeting buyer demand for self-service options.

Which age group is showing the highest growth in adoption?

Consumers aged 18–30 are buying at a 9.62% CAGR as embedded insurance within fintech and super-apps simplifies purchasing.

What are the biggest restraints on market growth?

Pricing commoditisation on comparison sites and the prolonged low-yield environment that squeezes insurer capital limits near-term expansion.

Are single-premium policies becoming more popular?

Yes. Growth in wealth accumulation and demand for immediate cover are driving faster adoption of single-premium term plans, especially among affluent customers.

Page last updated on: