Commercial Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.56 Trillion |

| Market Size (2031) | USD 2.07 Trillion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

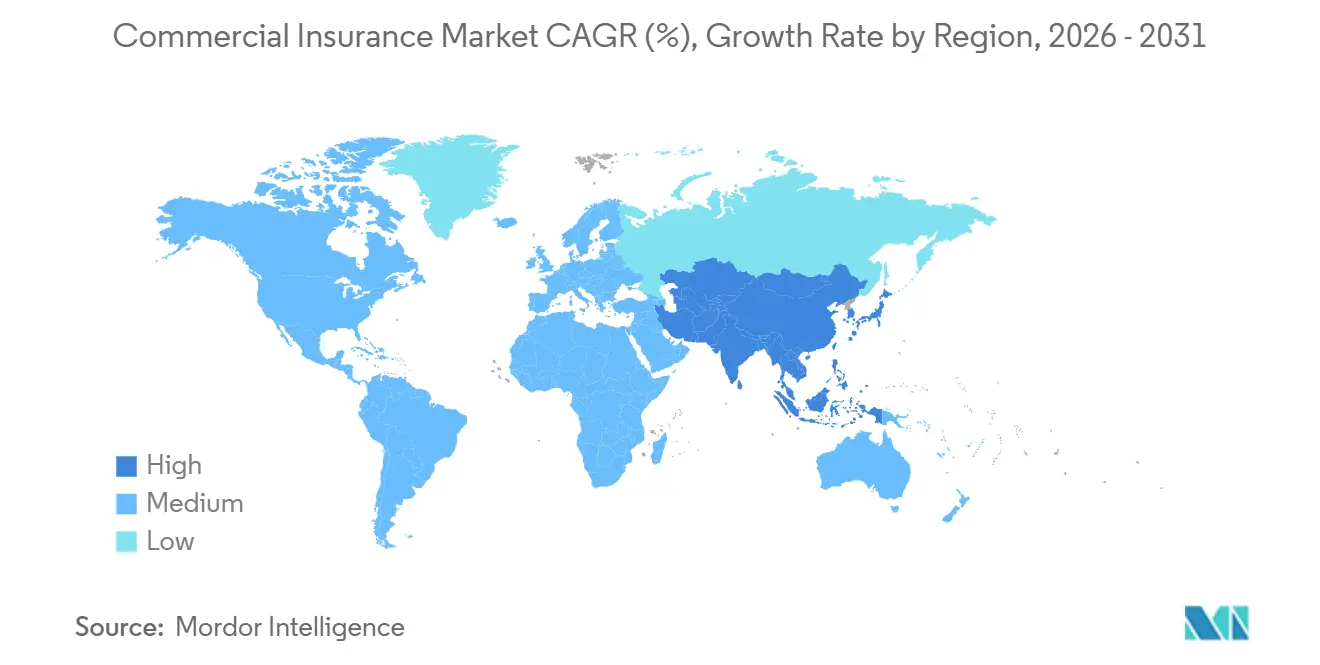

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Insurance Market Analysis by Mordor Intelligence

The Commercial Insurance Market size is expected to grow from USD 1.47 trillion in 2025 to USD 1.56 trillion in 2026 and is forecast to reach USD 2.07 trillion by 2031 at 5.86% CAGR over 2026-2031.

Growth is being supported by a broader set of enterprise risks, especially cyber, climate, and liability exposures, which now affect smaller firms as much as large accounts. The commercial insurance market is also being boosted by proof-of-coverage requirements, stronger demand for specialty protection, and better digital access for smaller buyers who were harder to reach through traditional channels. Competition remains moderate because global carriers still lead large-account and specialty lines, while regional and niche insurers are gaining ground where underwriting capacity is available and pricing has eased. Carriers are also using AI-led underwriting and embedded distribution to improve access to underserved buyers, helping the commercial insurance market move beyond its historical reliance on rate hardening alone. The main constraint remains casualty loss severity, as buyer resistance has become more pronounced amid high pricing across general liability and commercial auto lines.

Key Report Takeaways

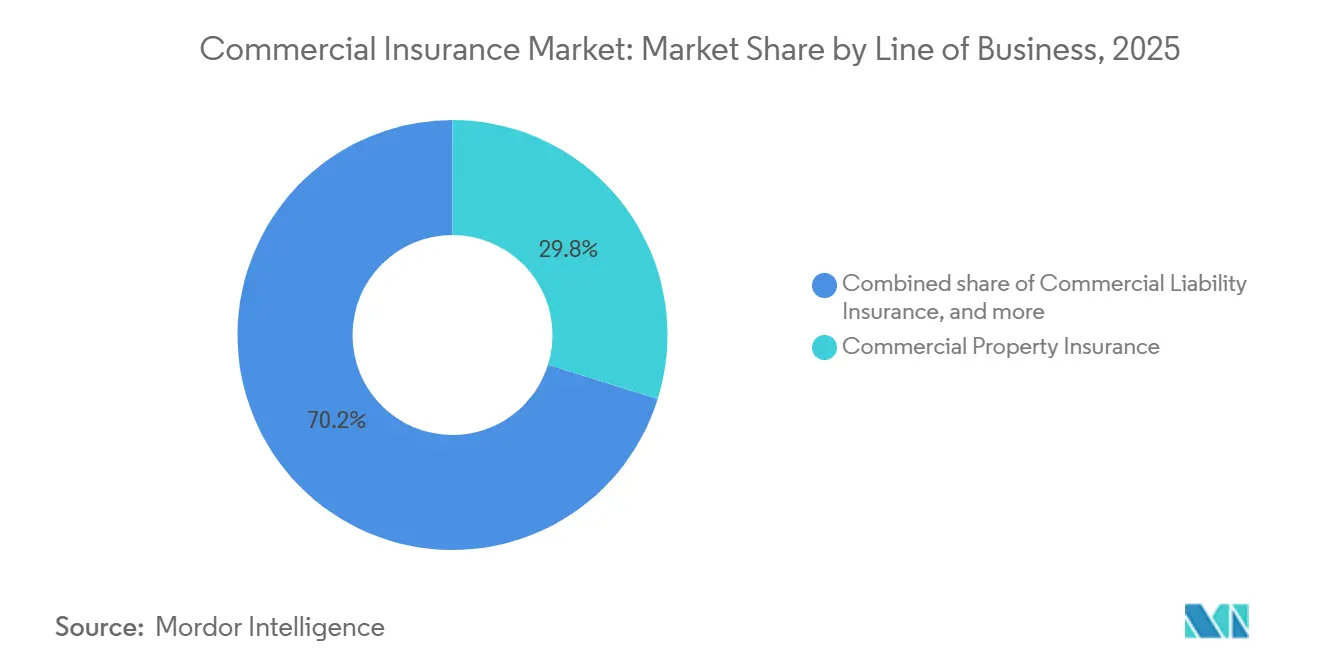

- By line of business, commercial property insurance captured 29.8% of the commercial insurance market share in 2025, while professional and financial lines are projected to grow at 8.8% CAGR through 2031.

- By enterprise size, large enterprises held 67.1% of the commercial insurance market share in 2025, while SMEs are projected to grow at 7.5% CAGR through 2031.

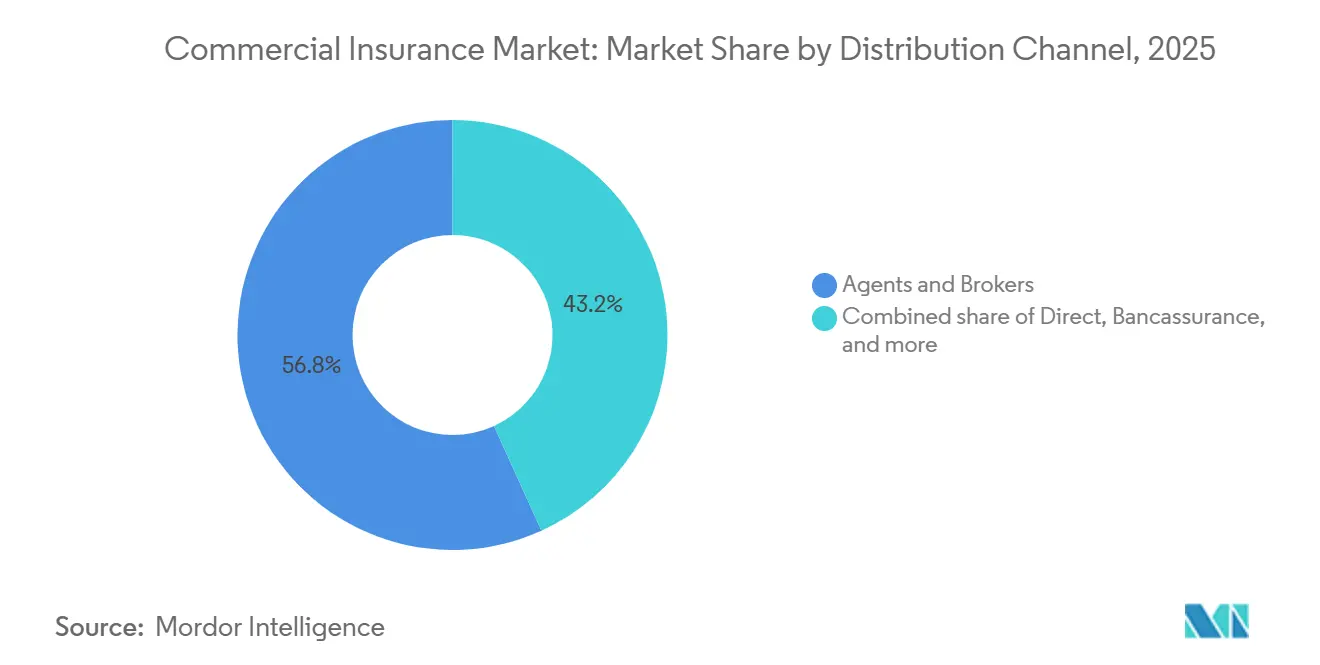

- By distribution channel, agents and brokers held 56.8% of the commercial insurance market share in 2025, while digital platforms are projected to grow at 10.2% CAGR through 2031.

- By industry vertical, manufacturing accounted for 22.3% of the commercial insurance market share in 2025, while information technology and telecommunications are projected to grow at 9.2% CAGR through 2031.

- By geography, North America captured 41.6% of the commercial insurance market share in 2025, while Asia-Pacific is projected to grow at 7.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cyber Liability Buying Across SMEs and Mid-Market Firms | +1.2% | North America & EU, Asia-Pacific core | Medium term (2-4 years) |

| Climate Volatility Repricing Property and Business Interruption Risk | +0.9% | North America, Asia-Pacific, spill-over to MEA | Short term (≤ 2 years) |

| Embedded Insurance and Digital Distribution Expanding Access for Small Businesses | +0.8% | Global, early gains in Asia-Pacific and EU | Medium term (2-4 years) |

| Regulatory Proof-Of-Coverage Requirements Increasing Policy Penetration | +0.7% | Global | Short term (≤ 2 years) |

| Parametric and Event-Triggered Covers Unlocking Uninsured Catastrophe Gaps | +0.4% | Asia-Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| AI-Driven Underwriting Improving Appetite for Thin-File Commercial Risks | +0.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber Liability Buying Across SMEs and Mid-Market Firms

Munich Re’s 2026 survey showed that nearly 9 out of 10 C-level respondents believed their companies were not adequately protected against cyberattacks, which points to a durable demand base for the commercial insurance market[1]Munich Re, “Cyber Insurance Risks and Trends 2026,” Munich Re, munichre.com. Global cyber gross written premiums reached USD 14 billion in 2025, with much of the increase coming from SMEs and mid-market firms. The Geneva Association reported that only 10% of SMEs globally carry cyber insurance, indicating the commercial insurance market still has a large protection gap to close, even though awareness has increased. Small business cyber adoption rose sharply through 2025, and completed policy purchases rose even faster, indicating that conversion is improving as products become easier to understand and buy. Cyber coverage is also being bundled with general and professional liability policies, which increases average premium per account and helps the commercial insurance market deepen relationships with smaller business customers.

Climate Volatility is Repricing Commercial Property and Business Interruption Risk

Munich Re reported USD 108 billion in insured natural hazard losses in 2025 against USD 224 billion in total economic losses, leaving a USD 116 billion protection gap that continues to reshape property underwriting in the commercial insurance market. Premium pressure is no longer confined to coastal catastrophe zones, because inland hail, flood, and wind exposures are also drawing more scrutiny from carriers and reinsurers. This change is widening the premium base for commercial property insurance even as insurers reduce limits or narrow appetite in the highest-risk locations. The result is a commercial insurance market that is still growing through property repricing, but with more selective capital deployment across exposed books. That pattern is altering carrier positioning, because firms with stronger catastrophe analytics and reinsurance support are better placed to keep writing business where others are stepping back.

Embedded Insurance and Digital Distribution are Expanding SME Access

Embedded distribution is changing how smaller firms enter the commercial insurance market, because coverage can now be offered within the platforms where those firms already sell, bank, or process payments. In 2026, TikTok Shop and ERGO NEXT Insurance embedded general liability, professional liability, workers’ compensation, and cyber coverage into the merchant onboarding flow, bringing commercial insurance into social commerce at a visible scale[2]ERGO NEXT Insurance and TikTok Shop, “Insurance Distribution Moves into the Social Commerce Ecosystem,” Insurance Business Magazine, insurancebusinessmag.com. Munich Re completed its USD 2.6 billion acquisition of NEXT Insurance in July 2025, signaling that digital-native small-business distribution is now viewed as a strategic route to growth rather than a side initiative. Willis launched Zest Insurance in Australia in June 2025 to target the AUD 9 billion SME segment through a fully digital model, which shows that distribution redesign is spreading across markets with different broker traditions. In Spain, BBVA Allianz reported 40% growth in SME premiums to EUR 57 million in 2025, demonstrating that digital bancassurance can unlock commercial insurance demand that standard broker channels have not captured as effectively.

AI-Driven Underwriting is Improving Carrier Appetite for Thin-File Commercial Risks

AI-led underwriting is becoming more important in the commercial insurance market because smaller accounts and specialty risks often arrive with incomplete or uneven data. AIG said it had processed more than 370,000 submissions through its agentic AI ecosystem, using Palantir’s Foundry platform and Anthropic’s Claude models with access to more than 4 million industry data points. Verisk launched its Commercial GenAI Underwriting Assistant in September 2025 to automate submission intake, data enrichment, and risk scoring in commercial property workflows[3]Verisk, “Verisk Launches Generative AI Commercial Underwriting Assistant,” Verisk, verisk.com. Zurich North America also expanded its use of Convr AI in December 2025, enabling underwriters to spend less time extracting data and more time on selection and broker relationships. This matters because the commercial insurance market can grow faster when carriers can quote and accept thin-file commercial risks that manual models once priced too slowly or declined too often.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Claims Severity Keeping Premiums Elevated for Price-Sensitive Buyers | -1.1% | North America, EU | Short term (≤ 2 years) |

| Policy Complexity Continuing to Slow SME Conversion | -0.6% | Global | Medium term (2-4 years) |

| Aggregation Risk Reducing Carrier Appetite for Catastrophe-Exposed Sectors | -0.4% | Asia-Pacific core, North America | Medium term (2-4 years) |

| Legacy Data and Integration Gaps Delaying Straight-Through Underwriting | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Claims Severity is Keeping Premiums Elevated for Price-Sensitive Buyers

The United States property and casualty industry posted a 92.9% combined ratio in 2025, but that improvement was helped by a mild hurricane season rather than a broad easing of casualty pressure. General liability and commercial auto are both expected to post combined ratios above 100 in 2026, with general liability set to rank among the weakest results in more than 10 years because of social inflation, litigation funding, and nuclear verdicts. That pressure is important for the commercial insurance market because mid-market buyers are less able to retain risk through captives or self-insurance, so that higher pricing can lead to lower limits or delayed purchases. State rate-filing rules in markets such as California, Florida, and Texas also limit how quickly insurers can adjust to loss trends, potentially pushing adverse selection into admitted books. Verisk reported that the United States net written premium growth slowed to 2.9% in Q1 2026 from 6.8% in Q1 2025, indicating that elevated pricing is now meeting greater buyer resistance.

Policy Complexity Continues to Slow SME Conversion

Policy complexity still slows the expansion of the commercial insurance market for SMEs because many owner-operators lack the time or technical background to compare multiple cover types, exclusions, and limits during a standard advisory process. The problem is especially evident in cyber insurance, where Geneva Association data still shows very low SME penetration, even though the risk profile is now much better understood. This leaves a large conversion gap in the commercial insurance market, particularly in products that require more explanation at the point of sale than property or basic liability coverage. The broker-led model remains important for complex accounts, but it has also preserved friction in the segment with the strongest growth potential. Simply Business integrated its pricing engine with OpenAI’s ChatGPT App Directory in 2026, demonstrating how conversational discovery tools can reduce that friction and bring more small buyers into the purchase funnel[4]Simply Business, “Simply Business Brings ChatGPT into SME Insurance Funnel,” Insurance Business Magazine, insurancebusinessmag.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Line of Business: Professional Lines Outpace a Diversifying Premium Base

Commercial property insurance accounted for 29.8% of the commercial insurance market in 2025, making it the largest line, as most enterprises still begin their risk transfer with protection for buildings, equipment, inventory, and business interruption. Property has also stayed prominent because climate-linked repricing has pushed premiums higher across many exposed locations even as rate momentum softened in 2026. The commercial insurance market is still using property as a core anchor line, but the strongest growth within the mix is moving toward more specialized liability products. Professional and financial lines are expected to expand at an 8.8% CAGR through 2031, supported by rising exposure tied to AI governance, digital services, board liability, and shareholder action. United States D&O direct written premiums reached USD 10.8 billion in 2024, and reserve concerns around the 2023 and 2024 accident years suggest pricing conditions may stabilize or firm from 2026 as loss development becomes clearer.

Commercial liability and commercial motor insurance remain important middle-tier lines in the commercial insurance market, but both continue to face pressure from claims severity and litigation costs. Workers’ compensation stands out as a healthier line, with the combined ratio expected to stay in the high 80s to low 90s through 2027 under disciplined reserving and favorable frequency trends. Marine, aviation, and transport insurance is also seeing repricing as geopolitical disruption raises cargo, war-risk, and corridor-specific exposures. Other specialty covers, including trade credit, environmental liability, and parametric structures, are attracting more attention as companies try to close catastrophe protection gaps and diversify sources of risk transfer. Catastrophe bond issuance reached USD 25.6 billion in 2025, indicating that capital market support is becoming increasingly relevant to how the commercial insurance industry manages peak property and specialty exposures.

By Enterprise Size: SME Growth Outpaces the Market as Coverage Gaps Narrow

Large enterprises held 67.1% of premiums in 2025, reflecting their greater risk complexity, lender-driven coverage requirements, and greater use of multi-line structured programs. That position remains firm because large accounts are transferring cyber, climate, supply chain, and liability risks into increasingly tailored placements that still depend on heavy advisory support. The commercial insurance market remains anchored by these large insureds, but the faster-growth opportunity lies with businesses that have historically been too costly to underwrite manually. SMEs are projected to grow at a 7.5% CAGR through 2031, which is well above the overall pace of the commercial insurance market. That faster expansion is coming from both sides, with stronger buyer awareness on one side and better underwriting economics on the other.

The SME portion of the commercial insurance market is benefiting from digital acquisition, embedded offers, and lower-friction quoting tools that can turn latent demand into completed policy purchases. In April 2026, Paydibs and Great Eastern General Insurance introduced embedded business protection via digital payment terminals for Malaysian MSMEs, demonstrating how fintech infrastructure can serve as a commercial insurance entry point. In Spain, BBVA Allianz grew SME premiums by 40% in 2025, which supports the view that digitally enabled bancassurance can reach smaller firms more efficiently than legacy distribution alone. AI-assisted underwriting also matters here, as carriers can quote thin-file SME accounts faster and at lower servicing costs than before. As these tools scale, the commercial insurance market should continue to narrow the gap between risk awareness and actual policy purchase among smaller firms.

By Distribution Channel: Digital Platforms Disrupt a Broker-Dominated Market

Agents and brokers captured 56.8% of the commercial insurance market share in 2025, which shows that advisory intermediation still matters in a product set that often involves customization, layered structures, and carrier negotiation. This channel remains especially strong in large corporate placements, excess and surplus lines, and other specialty risks where placement expertise and market relationships are still difficult to automate. Bancassurance also retains a meaningful role in parts of Europe and Southeast Asia, where lending and insurance relationships are closely linked. Direct distribution remains present, but it is not yet reshaping the core of complex commercial placement. The commercial insurance market, therefore, still depends heavily on brokers for large-account execution even as newer channels build share at the smaller end.

Digital platforms are forecast to grow at a 10.2% CAGR through 2031, making them the fastest-growing distribution route in the commercial insurance market. Growth is being driven by embedded insurance, AI-based quoting, and a buyer preference for self-service purchase journeys with smaller firms. Aon launched Broker Copilot in June 2025 to modernize placement work with AI and predictive analytics, while First Connect exceeded USD 500 million in gross written premium in 2025 through its digital marketplace model. European IDD rules and Australian financial services reforms are also shaping how digital and bancassurance channels document suitability, raising operating requirements but also creating standard processes that can scale. The commercial insurance industry is therefore not moving toward broker elimination, but toward a model where digital tools improve speed, access, and economics across the distribution chain.

By Industry Vertical: Technology Sector Drives Specialty Demand Beyond Manufacturing Base

Manufacturing held a 22.3% share in 2025, making it the largest vertical, as it combines property concentration, product liability, workers’ compensation, supply chain dependency, and trade credit exposure into a single risk base. At the same time, information technology and telecommunications are expected to grow at a 9.2% CAGR through 2031, making it the fastest-growing vertical in the commercial insurance market. The sector is bringing new demand for cyber, professional liability, directors and officers coverage, and business interruption protection tied to digital operations. Munich Re reported that manufacturing accounted for 33% of commercial cyber insurance claims in 2025, which shows that traditional sectors are also becoming heavy buyers of technology-linked protection. Tariff shifts and nearshoring are adding another layer, because new manufacturing facilities in destinations such as Mexico, Vietnam, and Eastern Europe require fresh property, liability, and trade credit cover that carriers did not previously write in those portfolios.

Construction and real estate are also becoming more important to the commercial insurance market because infrastructure and data center investment are expanding values at risk across building, equipment, liability, and operational delay coverages. Healthcare and life sciences continue to face heightened medical device and regulatory liability exposure, keeping specialty protection relevant even as broader pricing softens. Energy and utilities face both physical asset risk and transition-related uncertainty, making this vertical a continuing source of specialized underwriting demand. Transportation and logistics are facing rising motor and liability exposures, while retail and wholesale trade are moving from a property-heavy risk profile toward greater reliance on cyber and supply chain coverage. Taken together, this means the commercial insurance market is growing not only through sector size, but through a steady increase in the number of risks each vertical now needs to insure.

Geography Analysis

North America accounted for 41.6% of the commercial insurance market in 2025, making it the largest regional base. The region benefits from mandatory coverage requirements, high litigation intensity in casualty lines, and deep capital market support for specialty, excess, and surplus risks. Verisk and APCIA reported a USD 63 billion net underwriting gain for the United States property and casualty industry in 2025, while policyholders’ surplus rose to USD 1.2 trillion. Canada is also seeing repricing tied to updated hail, wildfire, and flood modeling, while Mexico is gaining from nearshoring-led demand for property, liability, and trade credit coverage. The main near-term challenge is casualty severity, as general liability remains under pressure and United States premium growth slowed to 2.9% in Q1 2026 amid buyer pushback against elevated pricing.

Europe remained the second-largest region in the commercial insurance market, supported by a mature carrier base and strong specialty capability across large industrial accounts. MAPFRE Economics reported that the 20 largest European insurance groups recorded premiums of EUR 922.8 billion (USD 150 billion) in 2025, up 4.6%. Zurich reported 8% like-for-like growth in its EMEA commercial insurance operations in Q1 2026, indicating that underwriting momentum continued even as pricing became more competitive. Central and Eastern Europe still offers room for expansion, as insurance penetration remains well below Western European levels, leaving meaningful headroom as business risk sophistication improves. Solvency II and IDD rules continue to shape capital discipline and distribution standards, which support incumbents that already operate at scale across the region.

Asia-Pacific is forecast to expand at a 7.9% CAGR through 2031, making it the fastest-growing geography in the commercial insurance market. Regional premiums grew 14% to USD 1.4 trillion in 2026, with Asia-Pacific accounting for 28% of global insurance premium growth, indicating the region is adding volume faster than North America and Europe. Commercial insurance rates in Asia fell 5% in Q1 2026, but demand remained firm because cyber regulation, industrial expansion, and climate claims kept businesses focused on structured protection. India is expected to be one of the strongest incremental demand contributors through 2031, as manufacturing expansion, infrastructure investment, and data regulation are expanding the insurable base. The Middle East and Africa remain smaller within the commercial insurance market. Still, Dubai is strengthening its role in regional placement, while South America is seeing better momentum in construction, energy, and trade credit lines tied to infrastructure spending and commodity flows.

Competitive Landscape

The commercial insurance market remains moderately concentrated, with large global carriers holding strong positions in specialty and large-account business while regional insurers and focused challengers compete more selectively. Allianz, AXA, Chubb, Zurich, and AIG continue to shape pricing, capacity, and underwriting standards across many of the highest-value commercial segments. The current competitive pattern in the commercial insurance market is centered on specialty scale, AI-enabled underwriting, and digital distribution partnerships. That combination matters because growth is coming from both complex risk categories and smaller firms that need faster, simpler access to coverage. The result is a market where scale still matters, but execution quality in technology and distribution is becoming a more visible source of differentiation.

Zurich moved to strengthen its specialty position by filing in June 2026 with the European Commission for approval to acquire Beazley for USD 8.1 billion, which would create a combined specialty platform with around USD 15 billion in gross written premiums and targeted annual cost savings of USD 150 million by 2029. Allianz chose a different route in May 2026 by expanding its global cyber relationship with Coalition, giving the MGA lead responsibility for pricing, product development, risk mitigation, and claims management in standalone commercial cyber. Those two moves show that commercial insurance market leaders are not following a single model, because some are buying specialty scale while others are delegating specialist execution to technology-led partners. Chubb’s Q1 2026 results also showed the value of geographic diversification, with consolidated net premiums written rising to USD 14 billion and growth outside North America remaining particularly strong. This reinforces the point that leading carriers are balancing specialization with geographic spread as pricing conditions normalize.

Another major battleground in the commercial insurance market is underwriting efficiency, especially in SME cyber, parametric structures, and technology-sector liability. AIG’s agentic AI program has already processed more than 370,000 submissions, which suggests that underwriting speed and data enrichment are becoming important competitive assets rather than back-office improvements. Munich Re’s acquisition of NEXT Insurance sends a similar message from the distribution side, as the largest reinsurer moved directly into a digital-native small-business carrier to improve access to a fragmented buyer base. Newer players, including API-first MGAs and embedded insurance providers, are unlikely to displace incumbents in large accounts anytime soon. Still, they are steadily improving conversion economics where legacy models were weakest. Established carriers, therefore, lead the commercial insurance market, while the edges of competition are shifting toward firms that can combine capital strength with faster product delivery and lower acquisition cost.

Commercial Insurance Industry Leaders

Allianz SE

AXA SA

Chubb Limited

Zurich Insurance Group Ltd.

The Travelers Companies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zurich Insurance Group filed with the European Commission for regulatory approval to acquire specialty insurer Beazley for approximately USD 8.1 billion, funded by approximately USD 3 billion in existing cash, USD 2.9 billion in new debt facilities, and a USD 5 billion capital raise completed in March 2026. The combined entity is expected to generate approximately USD 15 billion in specialty gross written premiums annually, targeting USD 150 million in annual cost savings by 2029 and over USD 1 billion in incremental revenue opportunities in the medium term.

- May 2026: Allianz Commercial and Coalition signed a strategic global agreement establishing Coalition as Allianz's exclusive partner for standalone commercial cyber insurance across all commercial segments. The coalition assumes primary responsibility for pricing, product development, risk mitigation, and claims management, with an initial rollout in the United States, United Kingdom, Australia, Germany, Denmark, and Sweden.

- April 2026: Paydibs and Great Eastern General Insurance Malaysia launched an embedded commercial insurance solution bundled with digital payment terminals for micro, small, and medium enterprises in Malaysia, representing one of the first Southeast Asian deployments of embedded commercial insurance through fintech payment infrastructure.

- December 2025: American International Group formed Lloyd's Syndicate 2479 in partnership with Amwins and Blackstone, with an initial underwriting capacity of USD 300 million in premium managed by Talbot Underwriting. The syndicate uses Palantir's Foundry platform and large language models with access to over 4 million industry data points for AI-assisted portfolio underwriting, representing a direct application of agentic AI to commercial insurance risk selection at Lloyd's.

Global Commercial Insurance Market Report Scope

| Commercial Property Insurance |

| Commercial Liability Insurance |

| Commercial Motor Insurance |

| Professional and Financial Lines (D&O, E&O, etc.) |

| Marine, Aviation and Transport (MAT) Insurance |

| Workers’ Compensation and Employers’ Liability Insurance |

| Other Specialty and Niche Lines (Trade Credit, Political Risk, Environmental Liability, Legal Expenses, Parametric, etc.) |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Agents and Brokers |

| Direct |

| Bancassurance |

| Digital Platforms |

| Manufacturing |

| Construction and Real Estate |

| Information Technology and Telecommunications |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Transportation and Logistics |

| Retail and Wholesale Trade |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Line of Business | Commercial Property Insurance | |

| Commercial Liability Insurance | ||

| Commercial Motor Insurance | ||

| Professional and Financial Lines (D&O, E&O, etc.) | ||

| Marine, Aviation and Transport (MAT) Insurance | ||

| Workers’ Compensation and Employers’ Liability Insurance | ||

| Other Specialty and Niche Lines (Trade Credit, Political Risk, Environmental Liability, Legal Expenses, Parametric, etc.) | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Distribution Channel | Agents and Brokers | |

| Direct | ||

| Bancassurance | ||

| Digital Platforms | ||

| By Industry Vertical | Manufacturing | |

| Construction and Real Estate | ||

| Information Technology and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Energy and Utilities | ||

| Transportation and Logistics | ||

| Retail and Wholesale Trade | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value outlook for commercial insurance worldwide?

The commercial insurance market is expected to reach USD 2.1 trillion by 2031, rising from USD 1.6 trillion in 2026 at a 5.9% CAGR.

Which geography leads global premium volume today?

North America held 41.6% share in 2025, supported by mandatory coverage, deep specialty capacity, and high litigation-driven demand.

Which region is expanding the fastest through 2031?

Asia-Pacific is forecast to grow at 7.9% CAGR through 2031 as industrialization, infrastructure spending, and regulatory change broaden the insurable base.

Which line of business is the largest and which is growing fastest?

Commercial property was the largest line with 29.8% share in 2025, while professional and financial lines are expected to grow fastest at 8.8% CAGR through 2031.

Why are SMEs becoming more important for carriers?

SMEs are projected to grow at 7.5% CAGR through 2031 because embedded insurance, AI underwriting, and digital platforms are lowering acquisition and servicing costs.

How is technology changing underwriting and distribution?

Carriers are using AI to process submissions faster and improve thin-file risk selection, while digital and embedded channels are making it easier for smaller firms to discover and buy coverage.

Page last updated on: