Marine Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 40.89 Billion |

| Market Size (2031) | USD 48.07 Billion |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

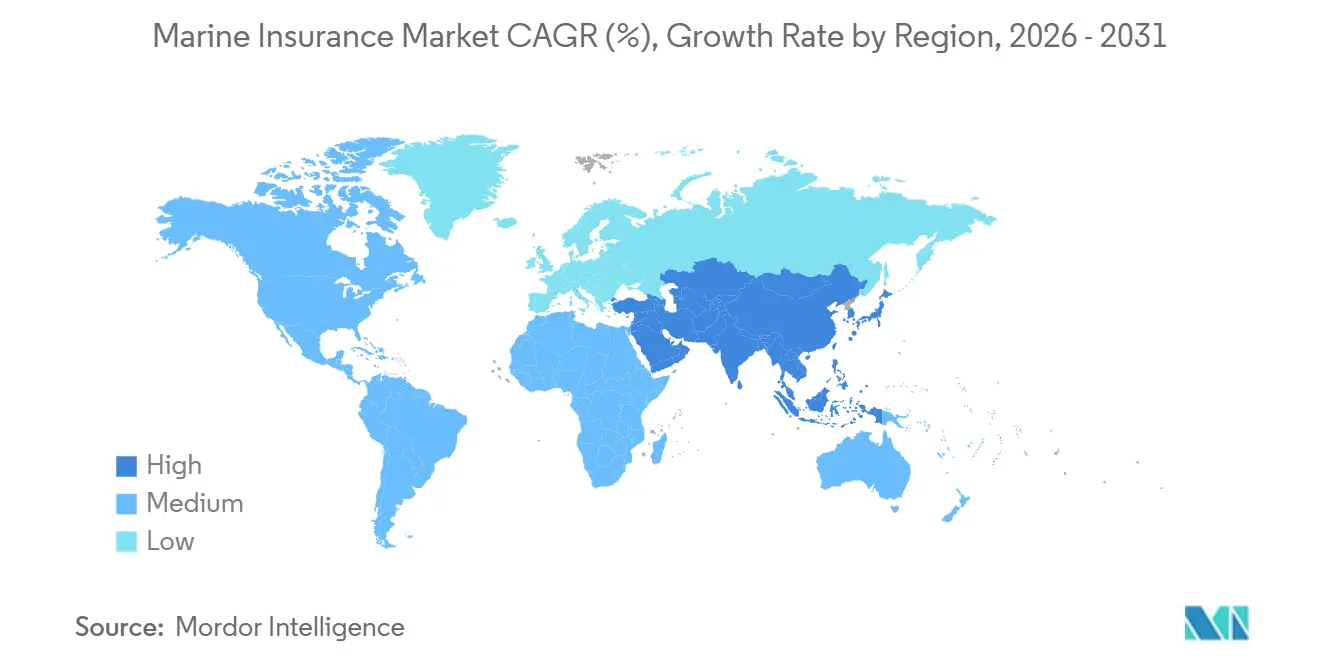

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Insurance Market Analysis by Mordor Intelligence

The Marine Insurance Market size is projected to be USD 39.74 billion in 2025, USD 40.89 billion in 2026, and reach USD 48.07 billion by 2031, growing at a CAGR of 3.29% from 2026 to 2031.

The marine insurance market is advancing on a stable demand base, as global seaborne trade continues to support cargo volumes and insured exposure, even as broader trade conditions remain uneven. The marine insurance market is also dealing with higher claims severity as vessel fleets age, fire incidents remain elevated, and the insured value of vessels continues to rise across key shipping classes. Demand is shifting toward specialized covers as conflict-exposed routes, alternative-fuel liabilities, and more complex machinery risks are changing how underwriters assess exposure in the marine insurance market. At the same time, soft conditions in standard cargo and hull placements are keeping pricing discipline under pressure, even as risk intensity rises across several major trade corridors. This combination of stable demand, rising technical complexity, and a gradual move toward digital and specialty underwriting is shaping how capacity is being deployed across the marine insurance market.

Key Report Takeaways

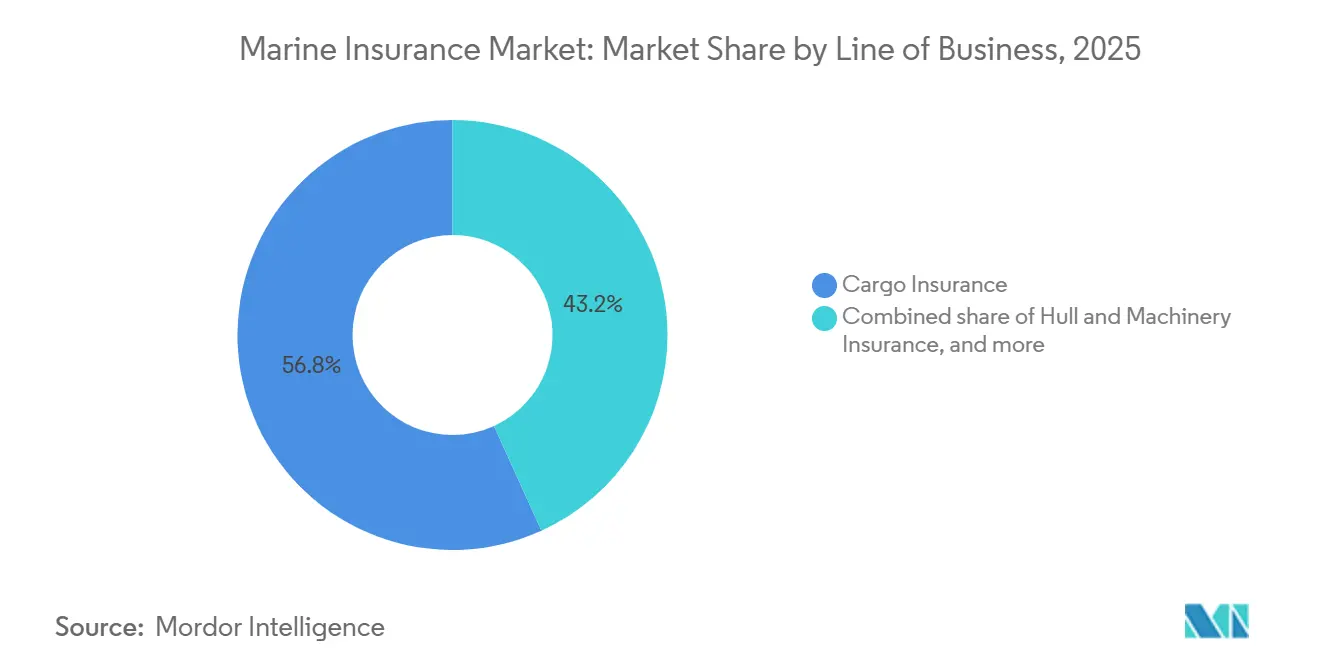

- By line of business, cargo insurance captured 56.8% of the marine insurance market share in 2025, while war risks and political risks insurance are projected to grow at 6.7% CAGR through 2031.

- By distribution channel, brokers accounted for 81.2% of the marine insurance market share in 2025, while online and digital platforms are projected to grow at 7.3% CAGR through 2031.

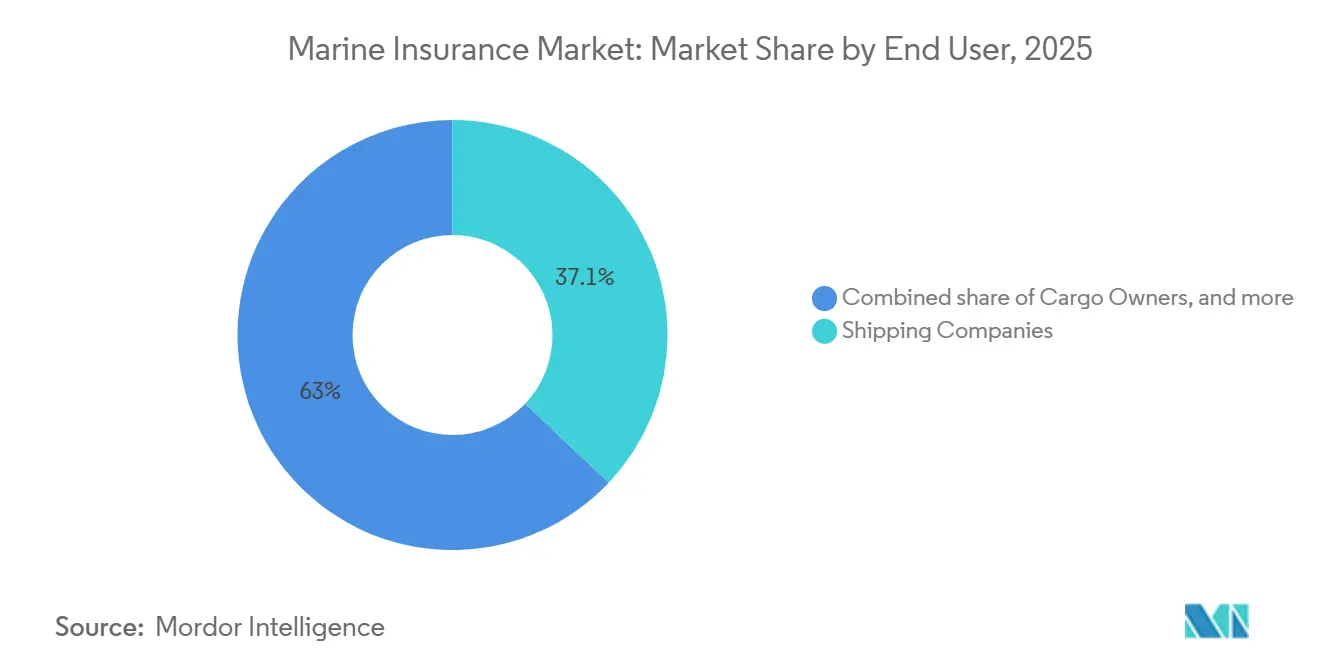

- By end user, shipping companies held 37.1% of the marine insurance market share in 2025, while freight forwarders are projected to grow at 4.8% CAGR through 2031.

- By geography, Europe captured 44.0% of the marine insurance market share in 2025, while Asia-Pacific is projected to grow at 4.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Seaborne Trade Volumes and Cargo Values | +0.8% | Global | Medium term (2-4 years) |

| Fleet Value Inflation from Higher Replacement and Repair Costs | +0.6% | Global, Particularly Europe and Asia | Short term (≤ 2 years) |

| Stronger Demand for Specialty War Risk Cover Along High-Risk Routes | +0.7% | Middle East, Red Sea, Black Sea Corridors | Short term (≤ 2 years) |

| Growth In Cargo Digitization, Real-Time Tracking, and Parametric Trigger Use | +0.4% | Global, With Asia-Pacific and Europe Leading Adoption | Medium term (2-4 years) |

| Aging Fleet, Larger Vessel Fire Exposure, and Higher Loss Severity | +0.5% | Global | Short term (≤ 2 years) |

| Decarbonization-Linked Liability and Machinery Risk Shifts | +0.3% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Seaborne Trade Volumes and Cargo Values

Global seaborne trade reached 12.9 billion metric tons in 2025, and dry bulk flows hit a record 5.7 billion metric tons, providing the marine insurance market with a broad cargo exposure base across commodity and container movements[1]AXSMarine, “Another Record Year for Dry Bulk Flows in 2025,” AXSMarine, axsmarine.com. The marine insurance market also benefited from longer voyage patterns, as trade rerouting increased the time insured goods spent at sea. UNCTAD data showed that average haul distances rose from 4,831 miles in 2018 to 5,245 miles in 2024, thereby increasing exposure per shipment even as volume growth was moderate. Higher declared cargo values are expanding the premium base for manufactured goods, energy cargoes, and other traded products that require more comprehensive cover in the marine insurance market. UNCTAD expects seaborne trade volumes to grow at a 2% annual average from 2026 to 2030, while containerized trade is set to rise at 2.3% a year, which gives cargo underwriters a durable demand backdrop through the forecast period.

Stronger Demand for Specialty War Risk Cover Along High-Risk Routes

The marine insurance market has seen war risk cover move from a cyclical add-on to a more structural underwriting priority for operators using conflict-exposed routes. This shift reflects the fact that disruptions in the Red Sea, Gulf waters, and nearby transit zones now affect routing choices, voyage timing, and the level of specialist protection that shipowners and cargo interests require. The Joint War Committee expanded high-risk designations in 2025 to include additional waters around Bahrain, Djibouti, Kuwait, Oman, and Qatar, thereby changing how the marine insurance market priced Gulf-related voyages. Lloyd’s also supported a Chubb-led marine war risk consortium for Strait of Hormuz transits, which showed that new capacity in this part of the marine insurance market is being built through coordinated structures rather than broad-based open competition. As a result, specialty war cover is becoming a more persistent premium line, and its growth is likely to remain stronger than that of standard cargo and hull business during the forecast period.

Aging Fleet, Larger Vessel Fire Exposure, and Higher Loss Severity

The marine insurance market is facing heavier claims pressure because older vessels, larger asset values, and more severe fire events are combining in the same underwriting cycle. The average commercial vessel age rose to 23 years in 2025, and ships aged 20 years and above made up nearly one-quarter of the global container fleet, which is changing how the marine insurance market evaluates maintenance risk and machinery exposure. More than 200 fires on large vessels were reported in 2025, while vessel fire incidents across major ship classes had already reached a decade-high in 2024, keeping loss prevention at the center of underwriting discussions[2]Allianz Commercial, “Safety and Shipping Review 2025,” Allianz Commercial, commercial.allianz.com. The global fleet also reached an estimated USD 1.5 trillion in insured value in 2024, up 4% year on year, so each major incident now carries greater absolute financial weight for the marine insurance market. With repair costs still elevated and older vessels accounting for a greater share of incidents, the marine insurance market is likely to keep tightening risk selection in hull, machinery, and related liability placements.

Decarbonization-Linked Liability and Machinery Risk Shifts

The marine insurance market is entering a period in which fuel transition risks are evolving faster than the legal and insurance frameworks meant to address them. A 2026 submission to the IMO Legal Committee concluded that no international civil liability regime currently exists for incidents involving alternative fuels used for marine propulsion, leaving important gaps across several established conventions[3]International Chamber of Shipping, “Report of the Informal Correspondence Group, Suitability of IMO Liability and Compensation Regimes With Respect to Alternative Fuels,” IMO Legal Committee LEG 113, ics-shipping.org . That means the marine insurance market must price toxicity, machinery compatibility, and incident response risk before a mature claims history is available for ammonia, methanol, and hydrogen-based operations. BIMCO’s 2026 Biofuel Clause created a standard contract framework for fuel quality, storage, and liability allocation, which helps the marine insurance market on the contractual side, even though the broader compulsory insurance gap remains unresolved. As alternative fuels move from pilot use to wider commercial deployment, underwriting standards in the marine insurance market will need to evolve faster across P&I, hull, and machinery lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soft Pricing And Capacity Abundance In Commodity Cargo And Hull Lines | -0.7% | Global, Most Acute in London and Nordic Markets | Short term (≤ 2 years) |

| Regulatory Complexity Across Jurisdictions And Claims Handling Delays | -0.4% | Global | Long term (≥ 4 years) |

| Data Gaps In Specialty Risks Such As Autonomous Vessels And Cyber Losses | -0.3% | Global | Medium term (2-4 years) |

| Reinsurance Concentration In Key Placement Hubs Increases Cost Volatility | -0.3% | London, Zurich, Bermuda | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soft Pricing and Capacity Abundance in Commodity Cargo and Hull Lines

The marine insurance market continues to face a difficult pricing environment in commodity cargo and hull business, where available capacity is still outpacing disciplined demand. This is limiting premium growth in the marine insurance market, even as underlying loss costs move in the opposite direction. Standard placements remain highly competitive, and buyers with clean claims records still benefit from broad market interest in routine hull and cargo accounts. That situation creates a clear mismatch because repair inflation, machinery losses, and route-specific stress have not eased at the same pace as pricing pressure. Unless capacity tightens or a major loss event changes sentiment, the marine insurance market is likely to remain soft in these commoditized lines over the near term.

Regulatory Complexity Across Jurisdictions and Claims Handling Delays

The marine insurance market is also constrained by cross-border compliance rules that are becoming more complex and more uneven across jurisdictions. In April 2025, the EU amended reporting requirements under Directive 2002/59/EC so that vessels transiting member state territorial waters must notify insurance certificate details, even when they do not call at a port, thereby widening operational obligations for carriers and insurers[4]Council of the European Union, “Delegated Directive Amending Annex I to Directive 2002/59/EC, Mandatory Ship Reporting and Insurance Certificates,” Council of the European Union, consilium.europa.eu. The marine insurance market also has to prepare for updates to the Maritime Labor Convention adopted in June 2025, with entry into force expected in December 2027 and implementation left to multiple flag states, which creates procedural inconsistencies across claims and compliance processes. Digital claims workflows are still not harmonized across all registries and ports, so multi-party claims remain document-heavy and slow in the marine insurance market. These frictions do not stop demand, but they do raise administrative costs and extend settlement timelines across the marine insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Line of Business: Cargo Insurance Anchors Revenue Amid Specialty Line Growth

Cargo insurance held 56.8% of the marine insurance market share in 2025, and global cargo premiums reached USD 22.6 billion in 2024, which kept this class at the center of premium generation in the marine insurance market. Asia-Pacific led cargo premium growth in 2024 at 8.8%, and China alone recorded 9.7% growth, offsetting softer trends in several other Asian markets. Cargo also remained technically attractive because IUMI reported a sixth straight year of improving loss ratios in 2024, and European ultimate loss ratios fell from above 65% to below 45% over that six-year period. At the same time, ocean voyage claims rose from a long-run average of 25% of loss location to 37% in 2024, which showed that the marine insurance market was still absorbing more loss activity during transit itself. ISM Code compliance, SOLAS declaration obligations, and mis-declared cargo risk are keeping underwriting scrutiny high, especially as lithium-ion battery shipments increase and fire severity remains an active concern.

Hull and machinery insurance accounted for 23.5% share in 2025, while the marine insurance market size for war risks and political risks insurance is projected to expand at 6.7% CAGR between 2026 and 2031. Global hull premiums reached USD 9.7 billion in 2024, up 3.5% year on year, which reflected the support coming from higher vessel values even as standard pricing conditions stayed competitive. Marine liability represented 7.6% of premiums, and this line is gaining relevance as crew, environmental, and fuel-transition exposures create more specialized product demand across the marine insurance industry. Offshore and energy insurance saw a premium decline of nearly 8% in 2024 because underwriting capacity remained abundant, yet expected offshore capital spending by 2026 should help rebuild premium depth in this part of the marine insurance market. Other and ancillary covers, including builders’ risk, yacht, and port liability, continue to provide a smaller but stable contribution that broadens the product mix of the marine insurance market.

By Distribution Channel: Brokers Defend Scale While Digital Platforms Emerge

Brokers held an 81.2% share in 2025, indicating that complex marine placements still depend heavily on expert intermediation across the marine insurance market. Large fleet programs, war risk structures, offshore energy placements, and manuscript liability covers still require market access, wording expertise, and reinsurance relationships that digital-only channels cannot fully replace. Large brokerage groups such as Marsh McLennan and Aon, along with marine specialists such as Miller and BMS, continue to defend their position through scale and specialty execution within the marine insurance market. The Lloyd’s ecosystem also supports this structure because specialist underwriting remains concentrated in a broker-led environment, and its 2025 combined ratio of 87.6% reflected continued operating strength across key specialty lines. This model remains sticky because policy wording for war risk, hull, and P&I cover often requires difficult-to-standardize negotiations across the marine insurance market.

Online and digital platforms are projected to grow at 7.3% CAGR between 2026 and 2031, and the marine insurance market size for this channel is expanding faster than any other distribution route in the forecast period. These platforms are gaining traction in SME cargo, embedded logistics cover, and parametric delay products, where users place a higher value on speed, transparency, and direct workflow integration. Parsyl’s launch of Chauncey for Brokers in March 2026 showed that digital change in the marine insurance market is not limited to direct clients, because brokers themselves are using chat-based submission tools to shorten the route from document upload to indicative quote. IUMI’s work with UN/CEFACT on international digital standardization of cargo insurance documents is also helping build the back-end structure needed for wider digital issuance across the marine insurance industry. Direct sales remain a smaller but steady route, mainly serving captives, large state-linked operators, and clients with established internal risk functions.

By End User: Shipping Companies Bear Complex Exposure as Freight Forwarders Expand Coverage

Shipping companies held a 37.1% share in 2025, making them the largest end-user group in the marine insurance market, as they carry the broadest mix of hull, machinery, war risk, P&I, and fuel-transition liability exposures. This group also faces the most direct effect from higher repair costs, older vessel profiles, machinery failures, and fire-related losses, all of which are increasing technical pressure across the marine insurance market. Cargo owners remained a large and stable user base because their cover demand continued to track commodity trade cycles and higher declared shipment values. Traders and importers stayed focused on shipment-specific cargo cover, and their sensitivity to route conditions increased as corridor disruptions changed voyage lengths and risk selection in the marine insurance market. The result is that shipping companies still anchor premium demand because they sit closest to the full chain of vessel operation, legal liability, and route-specific exposure.

Freight forwarders are projected to grow at 4.8% CAGR between 2026 and 2031, and the marine insurance market size for this end-user group is rising as logistics providers take on a larger role in transport coordination and insurance placement. QBE noted that tariff volatility was already reshaping Asian logistics flows in 2026, which increased routing complexity and raised cargo liability considerations for freight intermediaries. Ports and terminals are drawing more underwriter attention because fire incidents at port storage facilities accounted for 71% of all storage-related cargo losses in 2024, which makes accumulation risk a more visible issue in the marine insurance market. Other end users include oil and gas charterers, national commodity traders, and offshore infrastructure operators, each of whom relies on more tailored structures across the marine insurance industry. This broader end-user mix is widening the need for specialized underwriting even when core premium volumes remain centered on shipping companies and cargo owners.

Geography Analysis

Europe held 44.0% of global premiums in 2025, maintaining its position as the largest regional base in the marine insurance market. The region also posted hull premiums above USD 5.1 billion in 2024, supported by stronger vessel values and active sale-and-purchase activity. The marine insurance market in Europe benefits from the concentration of Lloyd’s syndicates, major commercial carriers, and Scandinavian P&I and hull specialists that provide long-established underwriting depth. European cargo loss ratios improved steadily over the past six years, moving from above 65% to below 45% by 2024, demonstrating stronger technical performance than in several higher-volatility regions. North America accounted for 7.8% of global premiums, and the marine insurance market there remained distinct, as cargo loss ratios reached 70% in 2024 while liability pricing remained firmer under the weight of social inflation and large verdict risk.

Asia-Pacific is projected to grow at a 4.1% CAGR between 2026 and 2031, and the marine insurance market in the region is supported by cargo growth, manufacturing exports, and stronger domestic insurance capacity. China remained the central growth engine, as hull premiums rose 9% in 2024 and cargo premiums increased 9.7%, offsetting flatter conditions in several neighboring markets. QBE also pointed to a global shortfall of nearly 90,000 maritime officers by 2026, which adds crew-related liability and operating pressure that regional insurers must price into the marine insurance market. Singapore, Indonesia, Malaysia, Vietnam, and South Korea continue to add relevance through containerized goods, commodity export routes, and growing insured cargo values across the broader marine insurance market.

South America remains centered on Brazil, where premium activity is closely linked to exports of iron ore, soybeans, and crude oil, and the marine insurance market also reflects recurring volatility tied to trade flows and settlement conditions. Latin America recorded paid cargo loss ratios of 72% in 2024, which was well above European benchmarks and highlighted the effect of route-specific risk and claims infrastructure gaps on the marine insurance market. The Middle East and Africa remains the smallest regional premium base, but the marine insurance market there carries strategic weight because Gulf and Red Sea transit conditions can change underwriting demand far beyond the region’s own premium pool. The Joint War Committee’s 2025 expansion of listed high-risk waters reinforced the region’s influence on voyage pricing, route planning, and specialty capacity demand across the marine insurance market.

Competitive Landscape

The global marine insurance market is moderately consolidated in specialty business and fragmented in standard commodity lines. A relatively small group of Lloyd’s syndicates, Allianz Commercial, AXA XL, Chubb, Zurich, Tokio Marine, and HDI Global, shapes much of the underwriting capacity in hull, war risk, and offshore energy across the marine insurance market. International Group P&I clubs, including Gard, NorthStandard, Skuld, West of England, Britannia, and UK P&I, continue to cover the substantial majority of ocean-going tonnage through their mutual structure, which gives that part of the marine insurance market a different competitive model from commercial cargo and hull lines. Standard cargo and hull business remains more competitive because multiple carriers, MGAs, and newer platforms are pursuing placement share in the same accounts. That leaves the marine insurance market with a split structure where specialist expertise commands stronger strategic value than broad commodity capacity alone.

One clear pattern is expansion through targeted acquisitions that add specialized product knowledge to the marine insurance market. Optio Group acquired Norwegian hull specialist S Insurance in 2025 and then agreed to acquire Gardian Marine Limited in March 2026, which strengthened its position in builders’ risks, ship repairers’ liability, voyage, and towage insurance. Rokstone also acquired Post & Co in 2025, which gave it a stronger Continental European marine underwriting platform and widened its reach in the marine insurance market. Another clear pattern is technology-led underwriting, as Chaucer and Ceto launched a Lloyd’s coverholder MGA in March 2026 that uses high-frequency vessel machinery and performance data, with Tokio Marine Kiln adding capacity support to that model.

A second area of competition is product development in newer risk categories where the marine insurance market still has limited depth. Parametric cargo delay cover, cyber-linked marine liability, and ESG-aligned hull solutions for alternative fuel vessels remain less crowded spaces than standard cargo and hull business. IUMI’s work on digital cargo insurance document standards suggests that data architecture will matter more in the marine insurance market because faster document flow supports tighter underwriting control and shorter servicing cycles. Overhaul and Navium also launched a Lloyd’s-backed insurance solution for AI infrastructure cargo in 2025 with limits up to USD 75 million per agreement, which showed how the marine insurance market is beginning to build cover around newly emerging asset classes. Over time, the firms that combine specialty judgment with structured, real-time operating data are likely to hold the strongest position in the marine insurance market.

Marine Insurance Industry Leaders

Lloyd's of London

Allianz SE

Zurich Insurance Group

Aon plc

Chubb Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BIMCO published the Biofuel Clause for Time Charter Parties 2026 on June 25, 2026, establishing the first standardized contractual framework for biofuel supply, storage, and liability allocation between shipowners and charterers. The clause assigns primary liability for degraded or non-compliant biofuel to charterers and directly affects P&I and hull underwriting exposure profiles under FuelEU Maritime compliance.

- March 2026: Optio Group agreed to acquire Gardian Marine Limited, a Lloyd ’s-backed MGA specializing in marine builders’ risks, ship repairers’ liability, voyage, and towage insurance. The deal followed Optio’s 2025 acquisition of Norwegian hull specialist S Insurance, making the group one of the fastest-building specialty marine MGA platforms in London.

- March 2026: Chaucer Group and Ceto launched a new Lloyd’s coverholder MGA using high-frequency vessel machinery and performance data to underwrite marine hull risks. Tokio Marine Kiln participates as an additional capacity provider, representing a significant step in AI-assisted, data-driven marine hull underwriting within the Lloyd’s ecosystem.

- March 2026: Parsyl Inc. launched Chauncey for Brokers, a chat-based AI risk submission tool enabling marine cargo brokers to upload documents, receive indicative quotes, track submissions, and move to binding, all within a single conversational interface integrated directly with Parsyl’s underwriting workbench.

Global Marine Insurance Market Report Scope

| Cargo Insurance |

| Hull and Machinery Insurance |

| Marine Liability Insurance |

| Offshore or Energy Insurance |

| War Risks & Political Risks Insurance |

| Other / Ancillary Covers |

| Direct Sales |

| Brokers |

| Online and Digital Platforms |

| Shipping Companies |

| Cargo Owners |

| Traders and Importers |

| Ports and Terminals |

| Freight Forwarders |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Line of Business | Cargo Insurance | |

| Hull and Machinery Insurance | ||

| Marine Liability Insurance | ||

| Offshore or Energy Insurance | ||

| War Risks & Political Risks Insurance | ||

| Other / Ancillary Covers | ||

| By Distribution Channel | Direct Sales | |

| Brokers | ||

| Online and Digital Platforms | ||

| By End User | Shipping Companies | |

| Cargo Owners | ||

| Traders and Importers | ||

| Ports and Terminals | ||

| Freight Forwarders | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for marine insurance worldwide?

The sector is projected to rise from USD 40.9 billion in 2026 to USD 48.1 billion by 2031 at a 3.3% CAGR, supported by trade volumes, higher insured values, and stronger demand for specialty cover.

Which line of business leads premium generation?

Cargo insurance led with 56.8% share in 2025, supported by strong global trade exposure and continued importance across commodity and container shipments.

Which segment is growing the fastest?

War and political risk insurance is the fastest-growing line of business, with a 6.7% CAGR between 2026 and 2031, while online and digital platforms lead distribution growth at 7.3% CAGR.

Why is underwriting becoming more complex?

Older vessels, more large-vessel fires, route disruption, and alternative fuel liabilities are all increasing risk complexity and making technical underwriting more important.

Which region is most important for premiums?

Europe remained the largest regional base with 44.0% share in 2025, while Asia-Pacific is expected to post the fastest growth at 4.1% CAGR through 2031.

How is digitalization changing placement and servicing?

Digital tools are speeding up cargo submissions, document flow, and quote turnaround, especially for SME cargo, embedded logistics cover, and broker-facing workflows.

Page last updated on: