B2B2C Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.27 Trillion |

| Market Size (2031) | USD 1.85 Trillion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

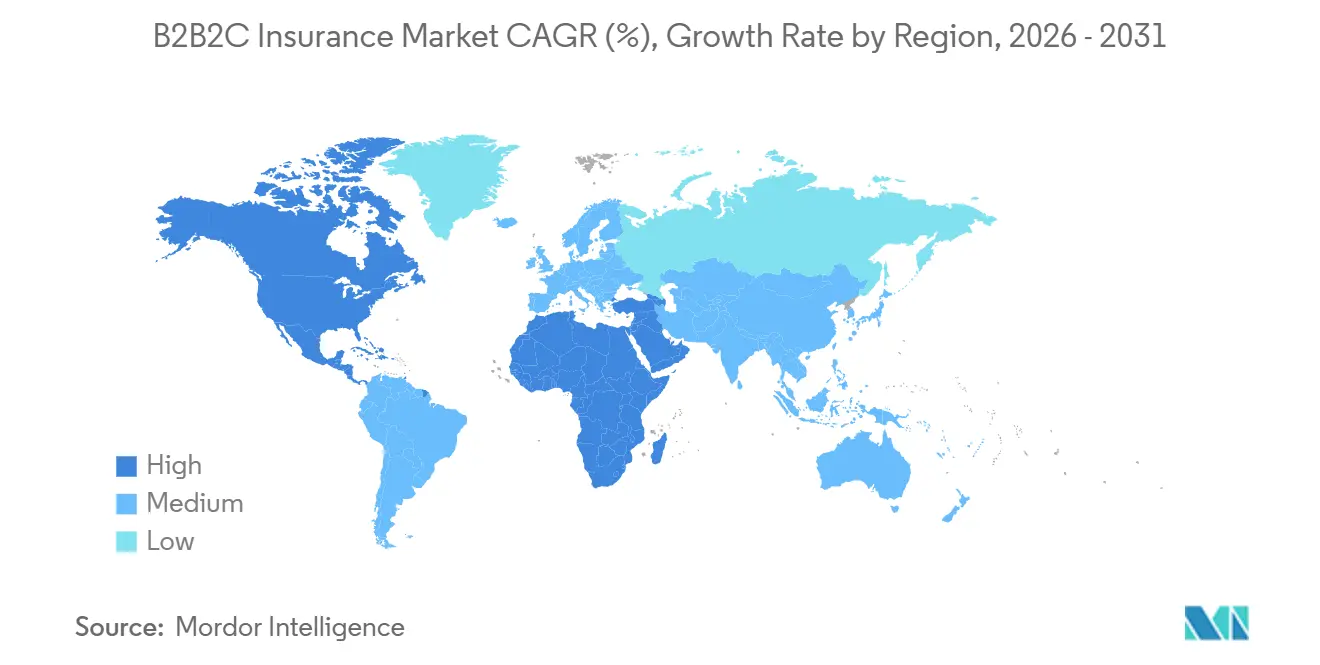

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

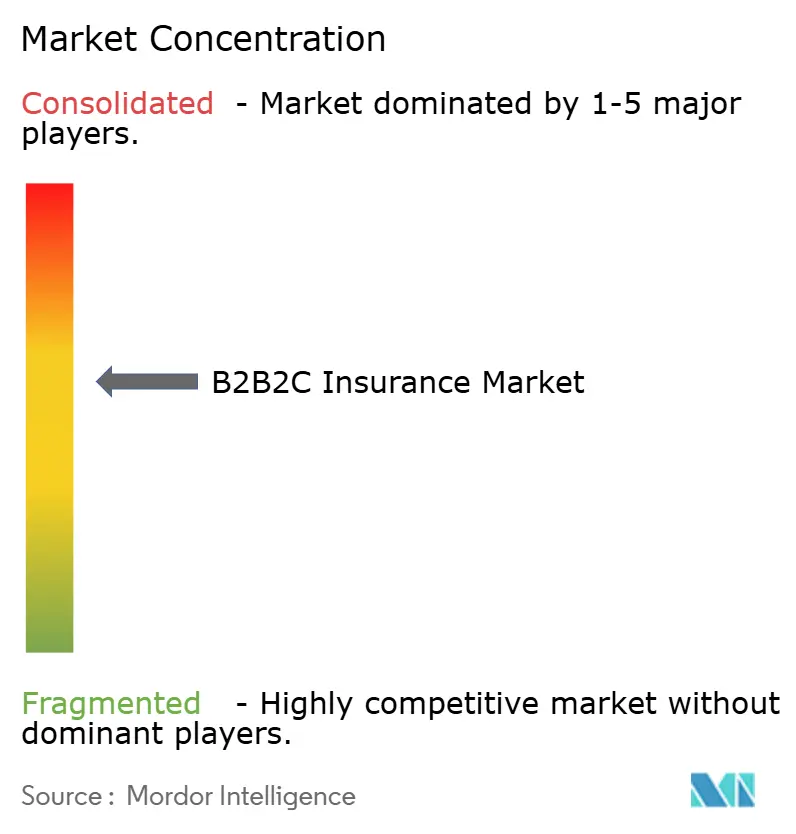

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

B2B2C Insurance Market Analysis by Mordor Intelligence

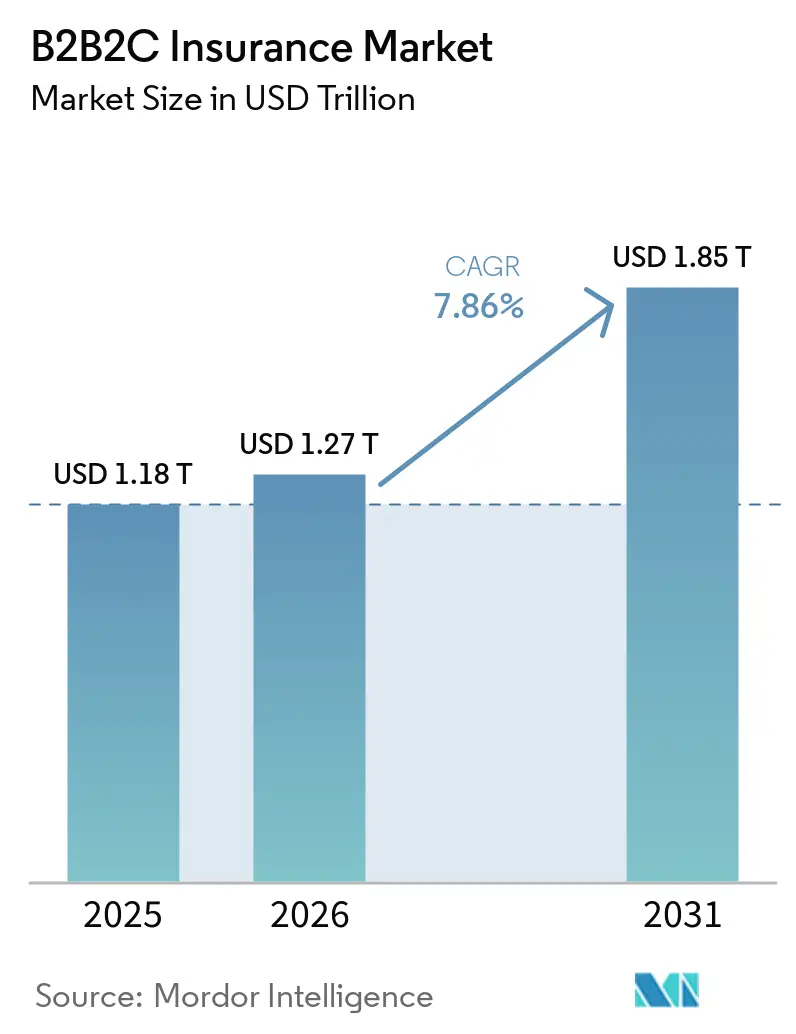

The B2B2C Insurance Market size is expected to increase from USD 1.18 trillion in 2025 to USD 1.27 trillion in 2026 and reach USD 1.85 trillion by 2031, growing at a CAGR of 7.86% over 2026-2031.

Growth in the B2B2C insurance market is being supported by the convergence of banking infrastructure, API-first distribution technology, and policy pressure to narrow protection gaps in emerging markets. The model has moved into a more scalable phase because insurers can now distribute through non-insurance partner businesses with less integration friction, and white-label protection can be added by platforms of very different sizes. Capital is still flowing into the infrastructure underpinning this shift, with global insurtech investment rising to USD 8.6 billion in 2025, supporting product design, policy administration, claims automation, and partner integration across the B2B2C insurance market. Competitive positioning is separating between global insurers that are extending partner-led distribution through their own digital rails and neutral orchestration platforms that aggregate carriers, products, and geographies for the B2B2C insurance market. The strongest opportunities sit where partner traffic is already active at the point of sale, while the main near-term drag on the B2B2C insurance market remains the cost and complexity of multi-jurisdiction compliance for cross-border deployments.

Key Report Takeaways

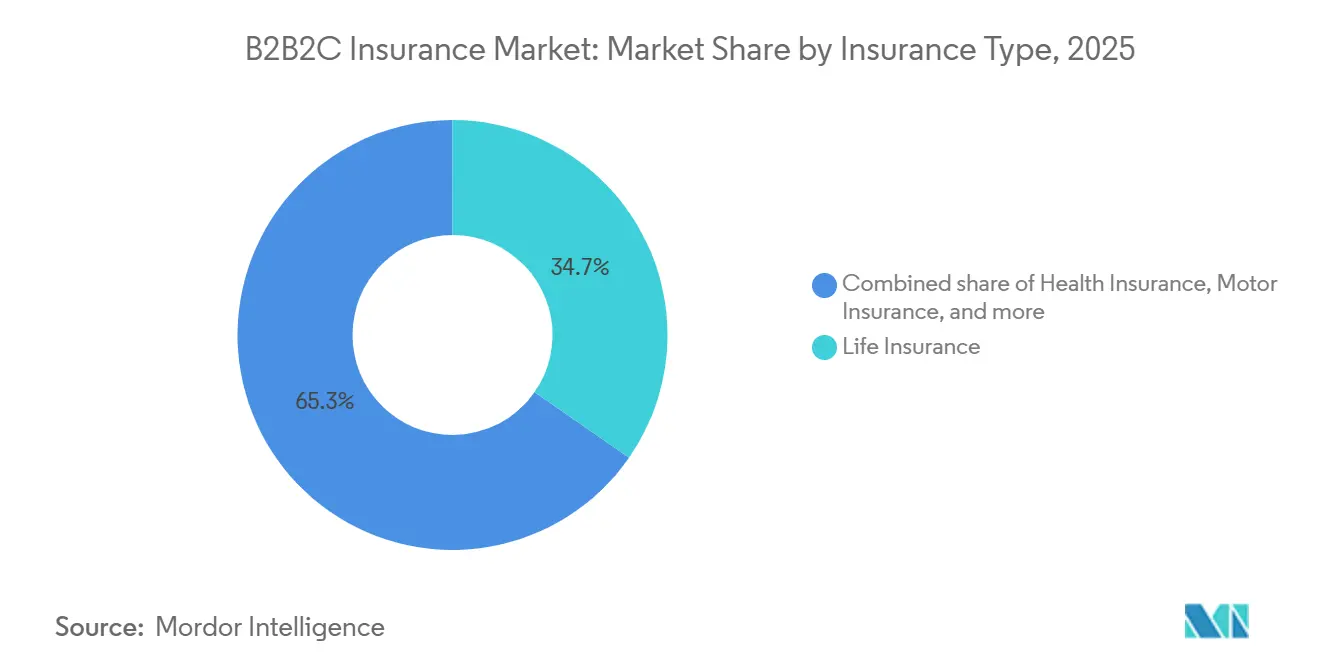

- By insurance type, life insurance accounted for 34.7% of the B2B2C insurance market share in 2025, while device, gadget, and electronics insurance is projected to grow at a 11.9% CAGR through 2031.

- By distribution model, bancassurance held 56.4% of the B2B2C insurance market share in 2025, while embedded, point-of-sale, and ancillary partnerships are projected to grow at 12.5% CAGR through 2031.

- By geography, Asia-Pacific accounted for 35.2% of the B2B2C insurance market size in 2025, while the Middle East and Africa are projected to grow at 10.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global B2B2C Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seamless Digital Checkout Demand Surge | +2.0% | Global, concentrated in North America, Western Europe, and the Asia-Pacific | Short term (≤ 2 years) |

| Embedded Distribution Lowers Customer Acquisition Cost | +1.6% | Global, with early gains in Europe and North America | Short term (≤ 2 years) |

| Regulatory Push to Close the Protection Gap | +1.0% | Asia-Pacific, MEA, South America, national programs in India, GCC, Nigeria | Medium term (2-4 years) |

| API First Partnerships With BigTech and Fintechs | +1.3% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Vertical SaaS Platforms Targeting SME Coverage | +0.6% | North America, Western Europe | Medium term (2-4 years) |

| Real-Time IoT Data Enabling Micro Policies | +0.7% | Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seamless Digital Checkout Demand Surge

The push toward point-of-purchase insurance in the B2B2C insurance market reflects a broader shift in customer behavior, in which buyers are more willing to accept protection when it appears within a familiar transaction flow. In this setting, the offer is not treated as a separate shopping journey, which improves visibility, lowers friction, and makes context-based coverage easier to understand. BCG noted in 2025 that embedded models were already posting stronger conversion than standalone propositions, with platforms using real-time checkout behavior to support dynamic pricing for micro-policies[1]Boston Consulting Group, “Embedded Insurance Success, Get Your Tech Stack Right,” BCG, bcg.com. The same work also stated that non-insurance companies bundling insurance with products and services are expected to control more than one-third of global property and casualty business in the coming years, which raises the strategic cost of delaying investment in the B2B2C insurance market. As more partners own the checkout layer, insurers that cannot connect their products directly into those moments risk losing both conversion and the data feedback loop that improves pricing over time.

Embedded Distribution Lowers Customer Acquisition Cost

Customer acquisition costs in the B2B2C insurance market are often lower than direct or agency models because the partner already owns the customer relationship and absorbs much of the origination effort inside its core sale. Cover Genius stated in 2026 that it had protected more than 41 million customers globally and sold over 100 million policies through API integrations, demonstrating how a single technical architecture can support policy issuance at scale across many countries[2]Cover Genius, “Turkish Airlines Renews Multi-Year Partnership with Cover Genius to Accelerate the Future of Embedded Protection,” Cover Genius, covergenius.com. This cost advantage matters most for lower-premium lines, such as travel micro-cover, device protection, and modular lending-linked products, which have struggled to support agent economics. The B2B2C insurance market is also separating between firms that offer basic quote retrieval and firms that provide real-time binding, claims automation, and partner orchestration on a single stack. As partner economics tighten, the fastest-scaling operators in the B2B2C insurance market are moving away from one-off integrations and toward repeatable multi-partner infrastructure that can defend margins at higher volume.

API First Partnerships with BigTech and Fintechs

API-first orchestration has become a core growth lever in the B2B2C insurance market because it reduces integration time, simplifies partner onboarding, and enables a single connection to support multiple insurance lines across multiple countries. bolttech’s June 2026 partnership with ING, launched across the Netherlands, Italy, Poland, and Belgium, shows how a single orchestration layer can help a major bank deliver protection products inside its subscription banking model without building each insurer link separately[3]bolttech, “ING Selects bolttech as Strategic Partner for Insurance and Protection Solutions,” bolttech, bolttech.io. This kind of setup gives the platform more control over product placement, renewal design, and customer experience, while carriers compete for access within the same digital framework. The Geneva Association reported that Chubb Studio handled 2.5 billion API calls in 2023 through more than 200 partners across banking, e-commerce, and mobility, which illustrates the scale benchmark now shaping competitive expectations in the B2B2C insurance market. Over time, platforms that collect pricing, claims, and renewal data across many insurers will hold a stronger informational position, which can shift bargaining power away from carriers that do not secure comparable data rights.

Real-Time IoT Data Enabling Micro Policies

IoT-linked cover is opening a more granular product layer in the B2B2C insurance market, where pricing and protection can respond to device signals rather than relying only on static annual assumptions. Munich Re and HSB launched Meshify Defender Slim sensors in May 2025, connected through Amazon Sidewalk, to support real-time leak detection, immediate alerts, and more dynamic property risk management[4]Munich Re HSB, “HSB’s New Slim Sensors Expand IoT Program to Habitational Buildings and Homes Through Amazon Sidewalk,” Munich Re, munichre.com. Zurich Insurance in Hong Kong expanded its robotics-related embedded protection through a June 2026 partnership with YAS, in which monthly micro-premiums were bundled into robotics-as-a-service fees and largely remained invisible to the buyer. These examples show that the B2B2C insurance market is moving toward shorter-duration coverage, more event-linked coverage, and easier attachment to service subscriptions. The underwriting challenge is equally important because insurers that cannot ingest and use real-time operational data may face adverse selection against competitors that price monitored assets with greater precision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fractured Multi-Jurisdiction Compliance Burden | -1.3% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Data Privacy and Consent Management Hurdles | -0.9% | Europe, evolving Asia-Pacific frameworks, North America | Medium term (2-4 years) |

| Channel Conflict with Agents and Aggregators | -0.6% | Europe, North America, and emerging Asia-Pacific | Short term (≤ 2 years) |

| Sparse Actuarial History for Granular Cover | -0.5% | Global, most acute in MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fractured Multi-Jurisdiction Compliance Burden

Cross-border scaling remains one of the clearest cost pressures on the B2B2C insurance market because licensing, product approval, intermediary status, and disclosure obligations still vary widely across national regimes. Even where a common framework exists, practical interpretation can differ enough to slow rollouts and add fixed legal and operational expense for each market entered. This burden favors large insurers and established platforms that can absorb recurring compliance costs across many jurisdictions, while smaller operators face thinner unit economics as their footprint expands. KPMG Law has highlighted that embedded insurance structures require careful legal design of roles, responsibilities, and distribution arrangements, reinforcing the idea that compliance can shape commercial viability as much as demand does. The B2B2C insurance market, therefore, grows fastest where technical scale is matched by regulatory readiness, because distribution traffic alone does not convert efficiently when approval pathways remain fragmented.

Data Privacy and Consent Management Hurdles

Data governance is another meaningful brake on the B2B2C insurance market because transactional and behavioral data can improve underwriting, but data-use permissions do not keep pace with partner integration. GDPR purpose-limitation rules make it harder to repurpose platform data for pricing and underwriting refinements without distinct consumer consent, reducing some of the efficiency advantages that embedded models would otherwise capture. This creates uneven operating conditions across regions, as markets with more flexible consent frameworks can support broader behavioral data use and faster product tuning. Assurant stated in 2025 that one European insurer cut compliance costs by 30% through a cloud-native platform migration with embedded regulatory controls, which shows that privacy-by-design architecture can protect economics even under stricter rules. In the B2B2C insurance market, the issue is not only legal risk but also whether data permissions, policy systems, and partner journeys are designed together from the start rather than pieced together later.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Device Disrupting Life's Long-Standing Distribution Lead

Life insurance held 34.7% of the B2B2C insurance market share in 2025, supported by the long-standing fit between savings-oriented products and bancassurance distribution. Banks already manage deposit, salary, lending, and wealth relationships, so they can place long-duration life products into a customer journey that is built on trust and recurring contact. That alignment supports higher persistence, especially for endowment and whole-life structures where product economics benefit from multi-year retention. Within the broader B2B2C insurance industry, this gives life products a structural advantage that is tied less to short-term pricing and more to channel design. Health, motor, property, travel, and credit or payment protection also remain important, but their growth patterns depend more on their placement within lending, retail, mobility, and service transactions.

Credit and payment protection illustrate that shift clearly, because coverage becomes easier to scale when it is built into a borrowing event rather than sold after the fact. BNP Paribas Cardif’s 2026 embedded creditor protection program for BanCoppel in Mexico shows how digital lending platforms can extend modular cover to underserved borrower groups through API-led infrastructure. Device, gadget, and electronics insurance is the fastest-growing segment of the B2B2C insurance market, with an 11.9% CAGR from 2026 to 2031, as replacement costs rise and telecom, retail, and platform partners make protection a more standard part of the purchase flow. Other personal lines, such as pet and cyber coverage, are still smaller, but they are forming around the same logic, where partner-owned traffic can surface cover at the exact point of need. Across the B2B2C insurance market, the move toward shorter-duration, event-linked micro-policies is slowly eroding the dominance of the traditional annual policy structure.

By Distribution Model: Bancassurance Scale Versus Embedded Velocity

Bancassurance accounted for 56.4% of the B2B2C insurance market in 2025, reflecting the scale advantages created by long-established exclusivity agreements, dense customer data, and broad physical and digital reach. The model still benefits from the fact that banks can embed insurance into existing financial relationships rather than build separate acquisition funnels for every product line. In China, the bancassurance channel passed a key milestone in 2025 when new single premiums overtook agency channel volumes for the first time in 14 years, and the channel share among major insurers rose to 63%. That result matters because it shows how a mature part of the B2B2C insurance market can still gain share when regulation, product fit, and household savings behavior align. It also explains why long-duration partnerships between banks and carriers continue to attract investment and why newer entrants struggle to displace them quickly.

Embedded, point-of-sale, and ancillary partnerships are projected to expand at a 12.5% CAGR from 2026 to 2031, making them the fastest-growing distribution format in the B2B2C insurance market. ING’s 2026 managing general agent model, enabled by Qover’s orchestration platform, showed that banks are no longer satisfied with acting only as referral channels and are moving toward greater control over applications, premium collection, and claims flows. Affinity, association, and loyalty partnerships remain relevant because employer schemes, member pools, and recurring program relationships still provide stable access to defined customer groups. What is changing is the context, as loyalty structures are increasingly linked to airline ecosystems, ride-hailing memberships, and retail subscriptions rather than only traditional associations. This leaves the B2B2C insurance market with two parallel engines, one built on bank scale and one built on digital partner speed, and both are likely to coexist for years rather than replace each other outright.

Geography Analysis

Asia-Pacific captured 35.2% of the B2B2C insurance market in 2025, making it the largest regional base for current revenue. The region combines strong bancassurance infrastructure with super-app behavior, high mobile engagement, and a policy environment that has generally been more willing to support testing of digital distribution. An Ageas, bolttech, and Open Finance & Insurance Observatory report stated that embedded insurance in Asia-Pacific accounts for 10% of total non-life gross written premiums through embedded channels, which is double Europe’s 5% share and highlights the region’s stronger adoption curve. In China, 10 bank-affiliated insurance companies generated CNY 477.5 billion (USD 66 billion) in premiums in 2025 and recorded sharp profit growth, underscoring the improvement in channel economics as fee discipline strengthened. Regional momentum also widened in 2026 when MSIG Asia appointed Peak3 as its digital platform partner for multi-market distribution, reinforcing the operational depth already present in the Asia-Pacific B2B2C insurance market.

North America and Europe are more mature parts of the B2B2C insurance market, but both continue to evolve as insurers push beyond traditional agency structures and deepen partner-led distribution. In North America, vertical SaaS, lender ecosystems, and platform commerce are broadening, enabling small-business and consumer coverage, which matters because partner-owned traffic reduces acquisition friction. Europe remains a critical proving ground for retail and financial services partnerships, where insurers are using existing brands and customer journeys to place protection more directly into daily transactions. Allianz UK’s agreement with Sainsbury’s Bank, which began in November 2025, reflects how a large incumbent can extend its reach through retail-linked financial distribution without relying on a traditional standalone insurance sales path. South America is still in earlier stages of development, but activity in digital banking and app-based financial services suggests that the region’s B2B2C insurance market has room to grow as embedded protection becomes a more standard feature across broader financial platforms.

The Middle East and Africa are the fastest-growing geographies in the B2B2C insurance market, with a forecast CAGR of 10.8% from 2026 to 2031. Growth is being shaped by mandatory health coverage expansion in the GCC and by mobile-led financial ecosystems in sub-Saharan Africa that can support more scalable insurance access. The B2B2C insurance market in this region benefits when insurers can attach protection to payment, payroll, lending, or service usage, because these channels solve parts of the distribution problem that agency models have struggled to address. The African Insurance Organization’s 2026 Pulse study found that mobile financial networks already reach close to half of the adult population in several low-income African markets, giving insurers a usable data layer for product design, pricing, and claims engagement. Even so, low insurance penetration and structural limits in distribution and reinsurance depth mean that the B2B2C insurance market in the Middle East and Africa will likely remain partnership-led rather than agent-led for the foreseeable future.

Competitive Landscape

The B2B2C insurance market remains moderately concentrated at the insurer level, where Allianz, AXA, Chubb, Zurich, and Generali hold broad technical, regulatory, and balance-sheet capabilities across several product lines and territories. At the same time, the orchestration and intermediary layer is more fragmented, with insurtech platforms competing on API quality, partner coverage, analytics depth, and jurisdictional reach. The Geneva Association reported in 2024 that more than 80% of surveyed reinsurance and insurance firms were already working with technology companies to build digital platform ecosystems, while fewer than 40% had adopted a pure partner model on existing third-party platforms. That split suggests that many incumbents in the B2B2C insurance market still prefer proprietary infrastructure, even as neutral platforms gain relevance in partner distribution. Competitive pressure is rising because banks, retailers, OEMs, and service platforms increasingly want control over the customer journey, reducing the bargaining power of insurers that cannot integrate quickly or flex their product design.

The most open areas in the B2B2C insurance market continue to be underpenetrated SME commercial lines, climate-sensitive micro-protection in low-coverage regions, and embedded life and health offerings within digital banking and app ecosystems. What separates winners is not the existence of a product but the ability to connect pricing, policy issuance, servicing, and claims into a single partner journey without heavy manual work. Aviva’s March 2026 launch of an insurance app on ChatGPT, in partnership with OpenAI, showed how distribution experiments are moving beyond price-comparison architecture into conversational digital interfaces. Investment patterns support that direction, with AI-led underwriting and embedded distribution platforms continuing to attract capital that strengthens integration, automation, and partner analytics across the B2B2C insurance market. Firms that already hold regulatory approvals across many countries can convert new partnerships faster than newer entrants, which widens a structural moat as compliance demands become harder to manage.

Strategic moves in 2025 and 2026 show that the B2B2C insurance market is being shaped by partnership depth rather than only by product breadth. AXA Partners and bolttech announced a long-term partnership in September 2025 to launch embedded insurance and assistance solutions across the EU, the United Kingdom, and Switzerland, covering telecom, financial services, travel, OEM, and retail use cases. Cover Genius renewed and expanded its embedded travel insurance work with Turkish Airlines in May 2026, scaling the relationship across 57 countries and reporting stronger gross written premium growth and customer experience outcomes since the original launch. Hippo Holdings also added homeowners' products to Progressive’s HomeQuote Explorer platform across 8 United States states in March 2026, another example of partner-led distribution as a faster route to reach policyholders. Together, these moves show that the B2B2C insurance market is rewarding carriers and platforms that can combine distribution access, digital operations, and product modularity within a single partner-facing model.

B2B2C Insurance Industry Leaders

Allianz SE

AXA S.A.

UnitedHealth Group Incorporated

Prudential Financial, Inc.

Munich Re Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ING and bolttech announced a strategic partnership to expand embedded insurance across 4 European markets: the Netherlands, Italy, Poland, and Belgium, with further 2026 expansion planned as part of ING's new global subscriptions model, marking a material acceleration of bancassurance-to-embedded migration in European retail banking.

- May 2026: Turkish Airlines renewed its multi-year embedded travel insurance partnership with Cover Genius, now scaled to 57 countries, reporting 3x organic Gross Written Premium growth and a 37% increase in NPS since the 2023 launch. The renewal expands into Australia, Latin America, and tailored United States and EU passenger segments.

- March 2026: Aviva launched an insurance app on ChatGPT in partnership with OpenAI, initially offering home insurance quotes, marking the first large-language-model-assisted insurance distribution deployment by a major United Kingdom insurer.

- November 2025: Allianz United Kingdom began offering home and motor insurance to Sainsbury's Bank customers under a new strategic agreement, expanding its United Kingdom retail bancassurance footprint alongside its existing partnership with Volkswagen Financial Services United Kingdom.

Global B2B2C Insurance Market Report Scope

| Life Insurance |

| Health Insurance |

| Motor Insurance |

| Property Insurance |

| Travel Insurance |

| Credit and Payment Protection Insurance |

| Device, Gadget and Electronics Insurance |

| Other Personal Lines (Pet insurance, Cyber Insurance, etc.) |

| Bancassurance |

| Embedded / Point-of-Sale / Ancillary Partnerships |

| Affinity / Association / Loyalty Partnerships |

| Other Structured B2B Partnerships |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Australia | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Insurance Type | Life Insurance | |

| Health Insurance | ||

| Motor Insurance | ||

| Property Insurance | ||

| Travel Insurance | ||

| Credit and Payment Protection Insurance | ||

| Device, Gadget and Electronics Insurance | ||

| Other Personal Lines (Pet insurance, Cyber Insurance, etc.) | ||

| By Distribution Model | Bancassurance | |

| Embedded / Point-of-Sale / Ancillary Partnerships | ||

| Affinity / Association / Loyalty Partnerships | ||

| Other Structured B2B Partnerships | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the B2B2C insurance market?

The B2B2C insurance market stood at USD 1.3 trillion in 2026 and is forecast to reach USD 1.9 trillion by 2031, with a 7.9% CAGR.

Which insurance line leads revenue today?

Life insurance led with 34.7% share in 2025 because it fits well with bank-led savings and protection distribution.

Which product area is growing the fastest through 2031?

Device, gadget, and electronics insurance is projected to expand at an 11.9% CAGR from 2026 to 2031 as replacement costs rise and partner-led sales become more common.

Which region is the largest and which is growing the fastest?

Asia-Pacific was the largest region with 35.2% share in 2025, while Middle East and Africa is the fastest-growing region with a 10.8% CAGR through 2031.

Why is bancassurance still ahead of other distribution models?

Bancassurance held 56.4% share in 2025 because banks combine customer trust, financial data, and recurring contact points that make insurance easier to place and retain.

What is shaping competition most strongly right now?

Competition is being shaped by API orchestration, embedded partnerships, and the ability to control the customer journey across banks, retailers, OEMs, and digital platforms.

Page last updated on: