Thioglycolic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

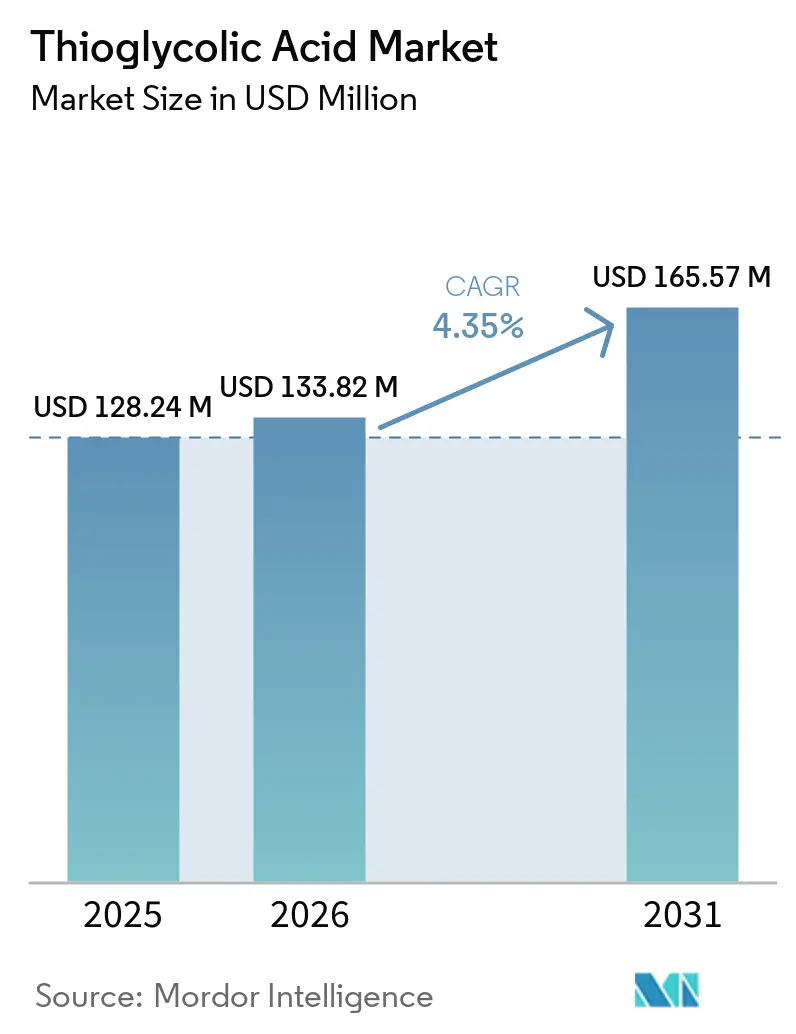

| Market Size (2026) | USD 133.82 Million |

| Market Size (2031) | USD 165.57 Million |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thioglycolic Acid Market Analysis by Mordor Intelligence

The Thioglycolic Acid Market size is expected to increase from USD 128.24 million in 2025 to USD 133.82 million in 2026 and reach USD 165.57 million by 2031, growing at a CAGR of 4.35% over 2026-2031. Upstream oil and gas operators are increasingly turning to TGA-based corrosion inhibitors, which maintain their effectiveness at temperatures above 70 degrees Celsius and a pH of 7.5. At the same time, optoelectronics companies are making strides in the aqueous synthesis of TGA-capped CdTe quantum dots, achieving a notable photoluminescence quantum yield. While feedstock volatility in monochloroacetic acid (MCA) is squeezing margins, vertically integrated producers are countering cost shocks by overseeing both chlor-alkali and acetic-acid streams. Capacity expansions, such as the specialty-chemicals plant at Daya Bay, scheduled for launch in 2028, highlight the rising demand for high-performance additives sourced from TGA. In the EU, tightening regulations now restrict consumer hair products to TGA, channeling more potent formulations into licensed professional outlets.

Key Report Takeaways

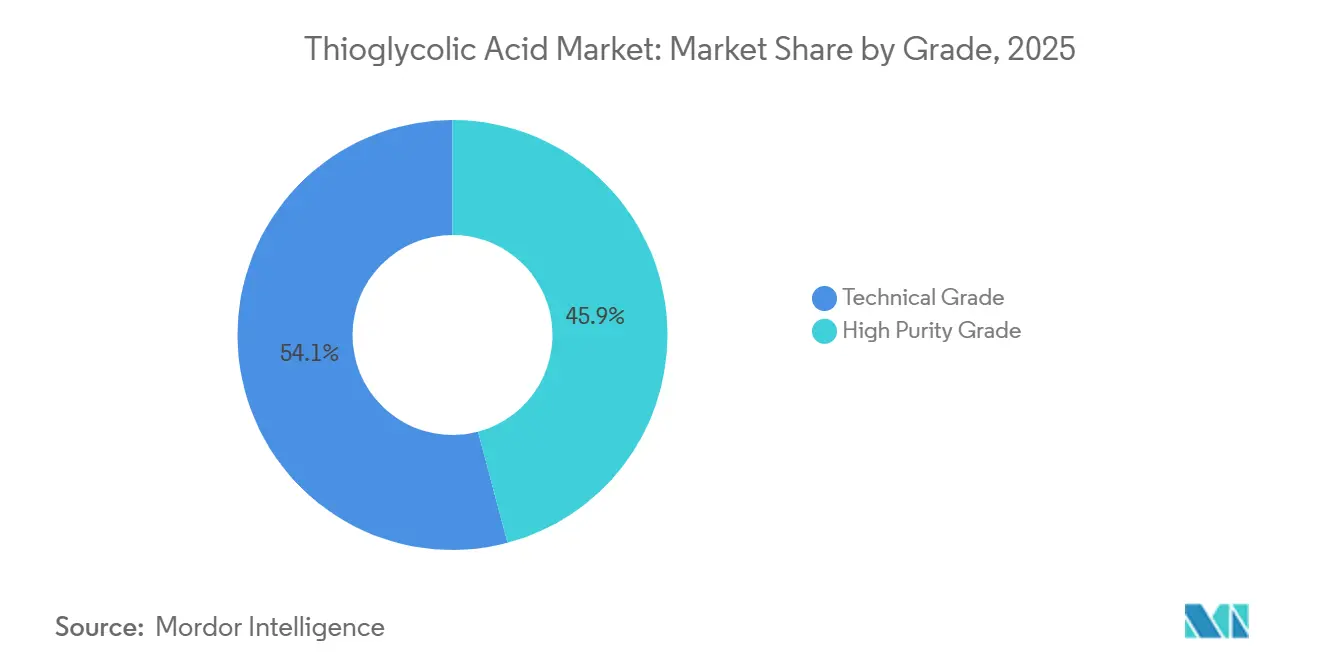

- By grade, technical grade led with 54.11% of the thioglycolic acid market share in 2025. High purity grade is poised to rise at a 4.66% CAGR through 2031, the fastest among grades.

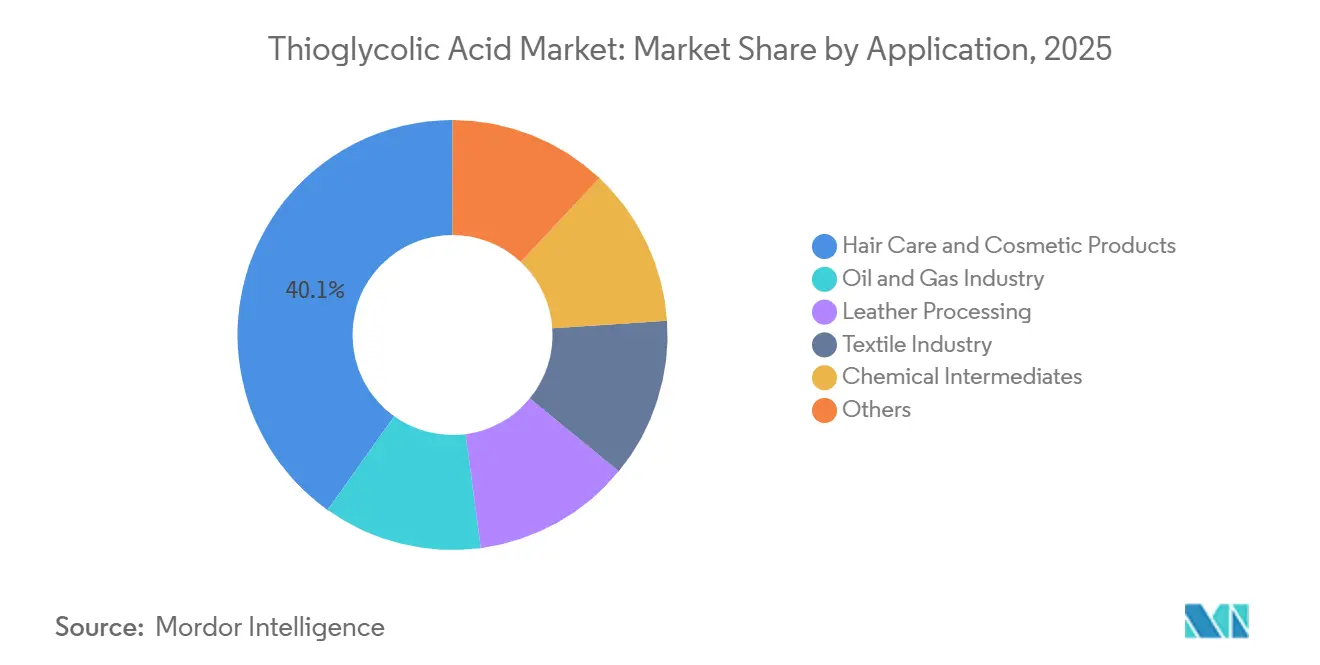

- By application, hair care and cosmetic products accounted for 40.12% of the thioglycolic acid market size in 2025 and are projected to advance at a 4.92% CAGR through 2031.

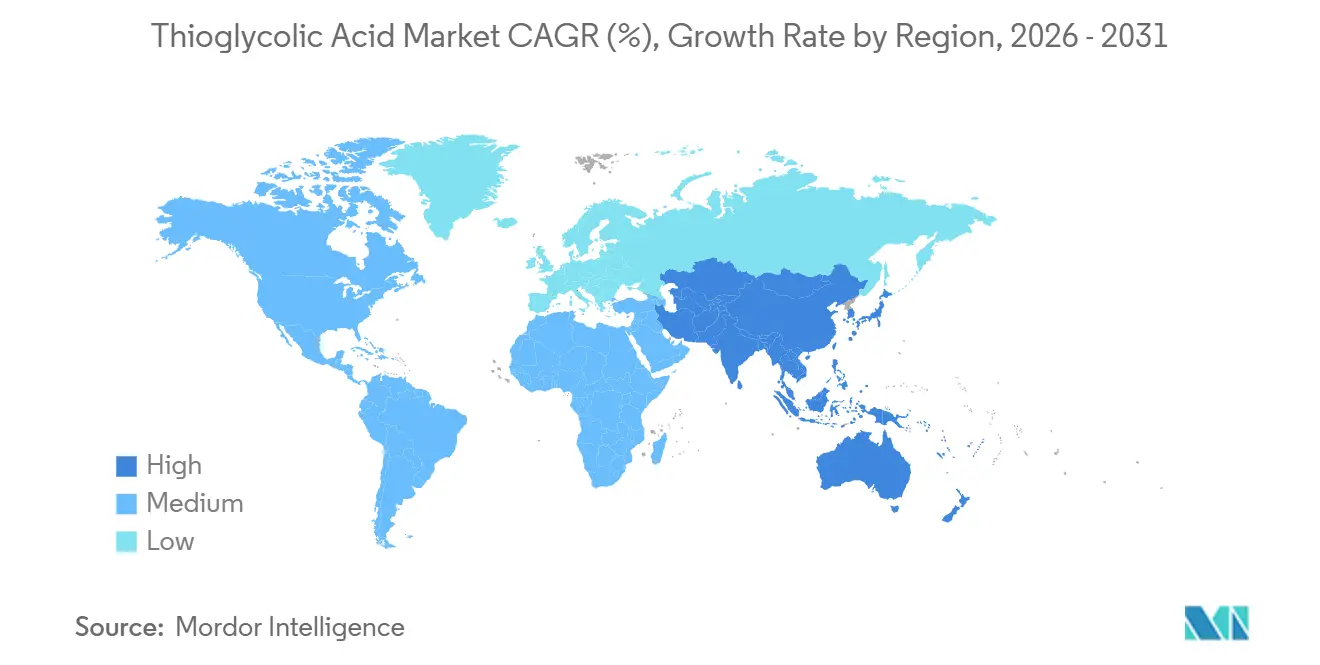

- By geography, Asia-Pacific accounted for 47.79% of 2025 revenue and is projected to expand at a 5.07% CAGR through 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thioglycolic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising use as corrosion inhibitor in oil and gas well acidizing | +1.20% | North America shale plays, Middle East high-salinity completions | Medium term (2-4 years) |

| Growing consumption as PVC heat stabilizer and other intermediates | +0.90% | Asia-Pacific PVC hubs, Europe specialty demand | Long term (≥ 4 years) |

| Adoption in quantum-dot passivation for optoelectronics | +0.60% | South Korea, Japan display clusters, North America Research and Development | Long term (≥ 4 years) |

| Emerging non-cyanide gold-leaching chemistries using TGA ligands | +0.30% | Brazil, Argentina, South Africa mining | Long term (≥ 4 years) |

| Low-odor, low-H₂S syntheses boosting EHS compliance and uptime | +0.50% | EU and North America chemical plants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Use as Corrosion Inhibitor in Oil and Gas Well Acidizing

Thioglycolic acid (TGA) serves a dual purpose: as a reducing agent and a chelating ligand. It is particularly effective in controlling iron during the matrix acidizing of carbonate reservoirs. In these reservoirs, ferric hydroxide precipitation can hinder near-wellbore permeability, reducing stimulation effectiveness. TGA operates efficiently at low concentrations, converting Fe³⁺ to the more stable chelated Fe²⁺ form. Unlike traditional chelants, such as citric acid, EDTA, and NTA, or reducers like erythorbic and ascorbic acids, TGA remains stable even at high temperatures and acidic pH levels[1]Arkema, “Thioglycolic Acid (TGA) Sell Sheet,” arkema.com . Additionally, TGA's thiol group forms a protective Fe-S film on mild steel at elevated temperatures. This film inhibits corrosion in concentrated salt solutions and high-H₂S environments, conditions often encountered in deepwater and unconventional wells. Small sulfur-containing molecules, including TGA, bond through Fe-S connections. When paired with intensifiers like tungstate or thiourea, they can drastically cut corrosion rates. As the industry pivots to ultra-high-temperature wells (over 150 degrees Celsius) and extended-reach horizontal laterals in shale plays, there is a rising demand for thermally stable, low-dosage inhibitors. These inhibitors not only minimize formation damage but also reduce chemical logistics costs.

Growing Consumption as PVC Heat Stabilizer and Other Intermediates

Organotin thioglycolates are being adopted as thermal stabilizers in PVC formulations, especially for food-contact packaging and potable-water piping. Given the stringent regulatory standards emphasizing low toxicity and minimal migration, these esters have gained approval for use in PVC water pipes, pumps, and food-processing equipment, boosting both transparency and thermal stability. The global move away from lead and cadmium-based stabilizers, due to regulatory crackdowns, has expanded the market for calcium-zinc and organotin alternatives. Yet, challenges persist, primarily due to cost and integration hurdles. The ramp-up of calcium-based PVC stabilizer capacity highlights the regulatory push steering a transition from liquid to solid stabilizer systems. Beyond PVC, TGA finds application as a chain-transfer agent in the emulsion polymerization of acrylic acid and acrylates. Its complete water miscibility and nucleophilic reactivity allow for precise molecular-weight control in aqueous environments. While TGA holds a niche yet crucial position in polymer additives, the Asia-Pacific region leads in production capacity, thanks to its closeness to downstream PVC and acrylic resin manufacturers.

Adoption in Quantum-Dot Passivation for Opto-Electronics

The aqueous synthesis of TGA-capped cadmium telluride quantum dots presents a greener, scalable method for producing size-tunable photoluminescent nanocrystals. These nanocrystals have applications in LEDs, bioimaging, and sensors, replacing traditional organometallic precursors that necessitate anhydrous solvents and inert atmospheres. By optimizing synthesis at specific pH levels and TGA:Cd molar ratios, one can achieve CdTe QDs with emissions tunable from green to red wavelengths. The concentration of TGA plays a pivotal role in crystal growth kinetics: lower TGA concentrations lead to mixed oriented-attachment and Ostwald-ripening mechanisms, while higher concentrations favor oriented attachment. This shift results in broader photoluminescence peaks and extended lifetimes due to the presence of internal defects. The ability to adjust QD size and optical properties through reflux time and TGA concentration, alongside water solubility and thiol/carboxylate functionality for bioconjugation, positions TGA-capped QDs as frontrunners for next-generation displays and diagnostic assays. However, TGA-capped CdTe QD thin films show high resistivity due to grain-boundary density, necessitating further engineering for effective charge-transport applications.

Emerging Non-Cyanide Gold-Leaching Chemistries Using TGA Ligands

Growing environmental and regulatory pressures to phase out cyanide in gold extraction have catalyzed research into sulfur-based complexing agents. Among these, thiol-containing lixiviants emerge as promising low-toxicity alternatives for extracting gold from refractory ores. Methods for non-cyanide gold leaching have spotlighted sulfur-containing, low-toxicity reagents as viable options. These alternatives not only aim to lighten the burden of wastewater treatment but also strive to align with regulatory standards. While TGA has not been directly evaluated in kinetic studies, research on cyanide substitutes reveals that thiosulfate and thiourea grapple with challenges like passivation and excessive reagent use. Their dissolution rates, however, are on par with or even lag behind cyanide. Given TGA's structural resemblance to thiourea, both being thiol-carboxylic compounds, there is potential for TGA to function as a complexing or reductive agent in non-cyanide leaching. This potential hinges on its oxidative stability, resistance to passivation, and economic feasibility for large-scale use. Mining firms experimenting with non-cyanide methods emphasize the importance of oxygen control, pH stability, and reagent recovery. These factors are crucial for curbing costs and minimizing environmental impacts, setting a high standard for commercial adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict consumer-safety limits on TGA concentration | -0.70% | EU, ASEAN | Short term (≤ 2 years) |

| Feedstock volatility (MCA, H₂S) | -0.50% | Global, non-integrated producers | Medium term (2-4 years) |

| Bio-based reductants replacing TGA in premium cosmetics | -0.40% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Consumer-Safety Limits on TGA Concentration

Recent amendments to the European Union's Cosmetic Products Regulation impose stringent limits on TGA and its salts in cosmetic products. The regulation sets maximum concentrations for hair-waving or straightening products, varying for general consumers and professionals based on the product's pH. Depilatories and rinse-off hair-care items also face defined concentration caps[2]European Commission, “Commission Regulation (EU) 2015/1190,” legislation.gov.uk . Due to potential eye irritation risks, products for eyelash waving are restricted to professional use, making them unavailable to general consumers. Compliance mandates, such as labeling warnings like "Avoid eye contact; rinse immediately if contact occurs; wear suitable gloves; contains thioglycolate; follow instructions; keep out of reach of children," not only increase costs but also limit formulation flexibility. ASEAN member states have mirrored these restrictions, establishing a stringent regulatory landscape across major consumer markets. In general-use hair-waving products, the cap on the combined concentration of TGA and thiolactic acid limits formulators' blending capabilities, reducing revenue potential per unit and pushing higher-margin professional formulations into licensed channels, fragmenting the market.

Feedstock Volatility (Monochloroacetic Acid, H₂S)

Monochloroacetic acid, the main precursor for TGA, is produced via the catalytic chlorination of acetic acid. Its global production and consumption have been steadily increasing, underscoring its market significance. Key cost determinants include the price volatility of acetic acid, the availability of chlorine (a co-product of caustic soda in chlor-alkali electrolysis), and energy costs for distillation and crystallization. Producers with integrated facilities, encompassing on-site chlor-alkali, acetic acid supply, and hydrochloric acid valorization, enjoy structural cost benefits. In contrast, non-integrated buyers face margin pressures amid feedstock price fluctuations. The Asia-Pacific region, with China at the forefront, stands as the largest consumer and producer of monochloroacetic acid. Major chemical groups are expanding regional capacities and backward integrating feedstocks, concentrating supply and heightening the risk of price volatility during demand spikes or feedstock shortages. Hydrogen sulfide, another vital input for TGA synthesis, poses notable challenges. Being toxic, corrosive, and flammable, it mandates stringent handling and emission controls, inflating both capital and operational costs for TGA producers. Manufacturers lacking vertical integration confront heightened challenges from feedstock price volatility, steering them toward consolidation and forging long-term supply agreements with upstream producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Technical Dominance Meets High-Purity Upside

In 2025, the Technical Grade accounted for 54.11% of the revenue, highlighting its pricing edge in PVC stabilizers, oilfield chemicals, and leather dehairing. Meanwhile, the High Purity Grade, driven by demand in pharmaceutical intermediates and optoelectronics, where color and trace metals are critical, experienced a robust CAGR of 4.66% during the forecast period of 2026-2031. Innovations such as Inline GC/FTIR techniques and the melt crystallization of MCA have effectively minimized dichloroacetate impurities, ensuring a flawless high-purity output.

Demand dynamics reveal a split. Industrial buyers may tolerate minor dithioglycolic acid residues, but quantum-dot manufacturers and biotin producers are willing to pay a premium for water content strictly below 0.1% and metals limited to 1 ppm. With ESG-driven upgrades in melt crystallizers and the integration of ISCC+ mass-balance feedstocks, producers are capitalizing on specialty margins in the thioglycolic acid market.

By Application: Hair-Care Core Faces Diversification

In 2025, Hair Care and Cosmetic Products accounted for 40.12% of the revenue, driven by professional straighteners powered by 10-20% ammonium TGA. This segment is projected to grow at a CAGR of 4.92% during the forecast period of 2026-2031. Although the European Union (EU) Annex III restricts the concentration of consumer wave lotions, this limitation reduces volumes while enhancing the sales value in salons. The oil and gas sector, a significant market, is experiencing expansion due to the increasing demand for low-dosage iron control in high-temperature shale wells.

Sodium TGA has become the preferred alternative to sodium hydrosulfide in leather processing, leading to a reduction in wastewater sulfide levels. In textile finishing, TGA salts function as reducing agents for vat dyes, while the range of chemical intermediates extends from pesticides to polythiols. Although diversification provides the thioglycolic acid market with a buffer against shifts in cosmetic policies, it simultaneously increases the demand for purity and performance across all sectors.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 47.79% share of the revenue and is set to expand at a CAGR of 5.07% through the forecast period of 2026-2031. China, a key player in the region's MCA supply, is solidifying its stance with the 2028 commissioning of a cracker and a high-performance unit at Daya Bay. This strategic move targets the burgeoning downstream demand for PVC stabilizers and quantum-dot materials. Concurrently, India's castor supply not only supports bio-based products but also intensifies competition in the thioglycolic acid market. Research hubs in Japan and South Korea are successfully commercializing TGA-capped CdTe QDs, setting their sights on the next-generation display market.

North America asserts its significance, with shale operators increasingly opting for TGA corrosion inhibitors over EDTA for their wells. This shift is largely driven by OSHA's exposure regulations advocating for low-odor synthesis. Europe, despite experiencing slower volume growth, is witnessing a surge in demand for High Purity Grade products, particularly in the pharmaceutical and professional beauty sectors. The REACH initiative is guiding the industry towards melt-crystallized MCA and a closed-loop sulfur handling approach, elevating European plants to the forefront of low-emission technologies.

While South America, the Middle-East and Africa remain niche players, they are beginning to show potential. Mines in Brazil and Argentina are trialing non-cyanide leaching methods, and Saudi Arabia's high-salinity reservoirs are paving the way for TGA-based acidizing blends. The future growth trajectory in these regions hinges on cost validations and the regulatory acceptance of TGA over conventional cyanide or thiosulfate methods.

Competitive Landscape

The thioglycolic acid market is moderately fragmented. Arkema, Bruno Bock, Daicel, and Merck KGaA hold significant shares. Companies are vertically integrating into chlor-alkali and acetic acid to hedge against MCA fluctuations, ensuring consistent mid-cycle profitability. Arkema’s ISCC+ mass-balance grades, which notably cut scope 3 emissions in comparison to fossil PA12, have become the eco-label choice for downstream users.

Nouryon introduced Expancel BIO microspheres, aiming at lightweight coatings where TGA acts as a chain transfer agent. Bruno Bock is investing in melt crystallization at its Marschacht facility, with plans to boost its High-Purity capacity in the near future. At the same time, Daicel is utilizing its patented solvent-free, low-H₂S synthesis method to reduce odors, aligning with Japanese workplace standards.

New prospects are emerging in gold-ore lixiviants, printable quantum-dot inks, and ultra-low-odor products for salons. During the forecast period of 2026-2031, suppliers in the thioglycolic acid market who merge quality data with regulatory insights and offer formulation support are expected to see increased customer loyalty.

Thioglycolic Acid Industry Leaders

Arkema

BRUNO BOCK

Merck KGaA

Daicel Corporation

Qingdao LNT Chemical Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The National Institutes for Food and Drug Control (NIFDC) released six draft Technical Guidelines for public consultation, including one on hair dye cosmetics. These guidelines regulate the use of thioglycolic acid, as outlined in the Cosmetic Safety Technical Specification (CSTS). For general-use perming products, the maximum concentration is 8%, while for professional-use products, it is 11%.

- March 2025: Health Canada revised its Cosmetic Ingredient Hotlist, an essential document that specifies ingredients prohibited or restricted in cosmetic products in Canada. As part of the updates, thioglycolic acid esters have been added to the list of prohibited substances due to their potential to cause skin sensitization.

Global Thioglycolic Acid Market Report Scope

Thioglycolic acid is a chemical compound widely used in cosmetics, particularly in hair removal products. This compound primarily functions by breaking down the protein structure of hair, making it more flexible and easier to remove. It is a key ingredient in depilatory creams and lotions, where it disrupts the disulfide bonds in the keratin protein of hair. This chemical reaction weakens the hair shaft, enabling its mechanical removal or dissolution. Although effective for hair removal, products containing thioglycolic acid should be used cautiously due to the risk of skin irritation.

The Thioglycolic Acid Market is segmented by grade, application, and geography. By grade, the market is segmented into technical grade and high purity grade. By application, hair care and cosmetic products, oil and gas industry, leather processing, textile industry, chemical intermediates, and others. The report also covers the market size and forecasts for thioglycolic acid in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Technical Grade |

| High Purity Grade |

| Hair Care and Cosmetic Products |

| Oil and Gas Industry |

| Leather Processing |

| Textile Industry |

| Chemical Intermediates |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Technical Grade | |

| High Purity Grade | ||

| By Application | Hair Care and Cosmetic Products | |

| Oil and Gas Industry | ||

| Leather Processing | ||

| Textile Industry | ||

| Chemical Intermediates | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the thioglycolic acid market?

The thioglycolic acid market stands at USD 133.82 million in 2026 and is forecast to reach USD 165.57 million by 2031 at a 4.35% CAGR from 2026 to 2031.

Which region grows fastest for thioglycolic acid demand?

Asia-Pacific advances at a 5.07% CAGR through 2031, the quickest among all regions.

Which grade shows the highest growth?

High Purity Grade records a 4.66% CAGR between 2026-2031, outpacing technical grade.

Why are oil companies switching to TGA-based inhibitors?

TGA maintains iron control at temperatures above 70 °C and reduces corrosion 80-95%, unlike EDTA or citric acid.

How do EU rules impact hair-care formulations?

EU limits consumer products to 8% TGA and restricts eyelash use to professionals, pushing high-strength products into salon channels.

Page last updated on: