Acid Proof Lining Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.27 Billion |

| Market Size (2031) | USD 8.37 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

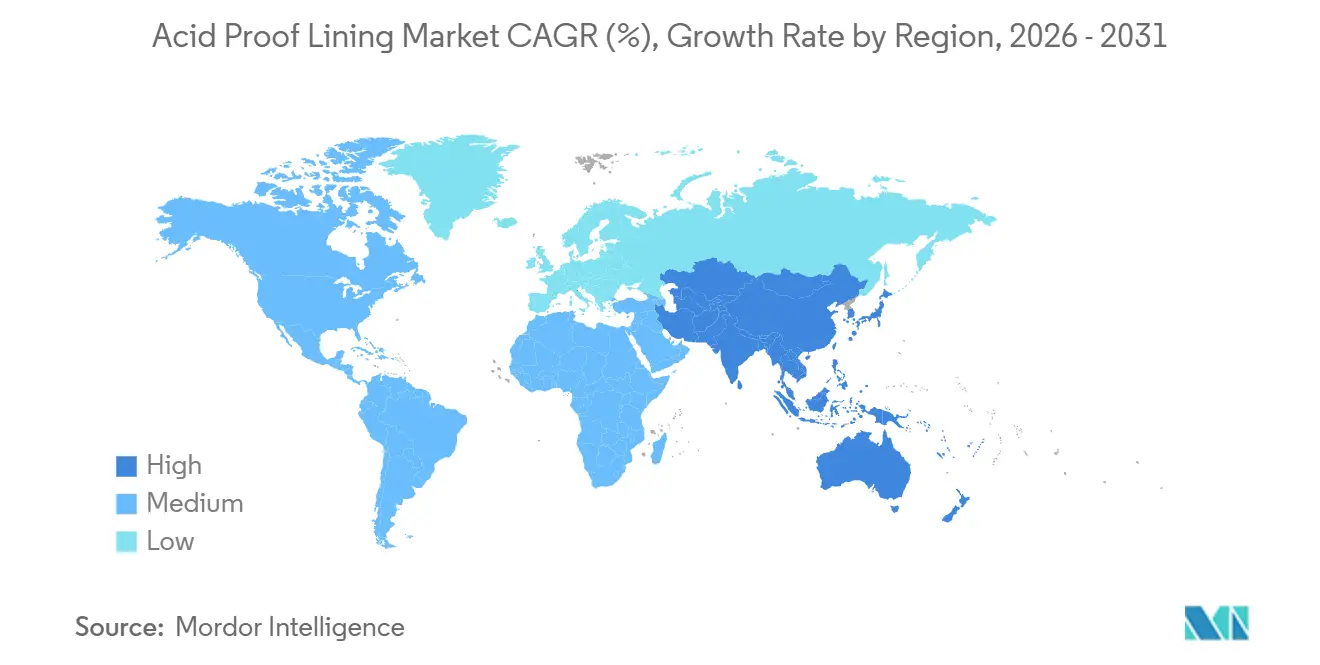

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

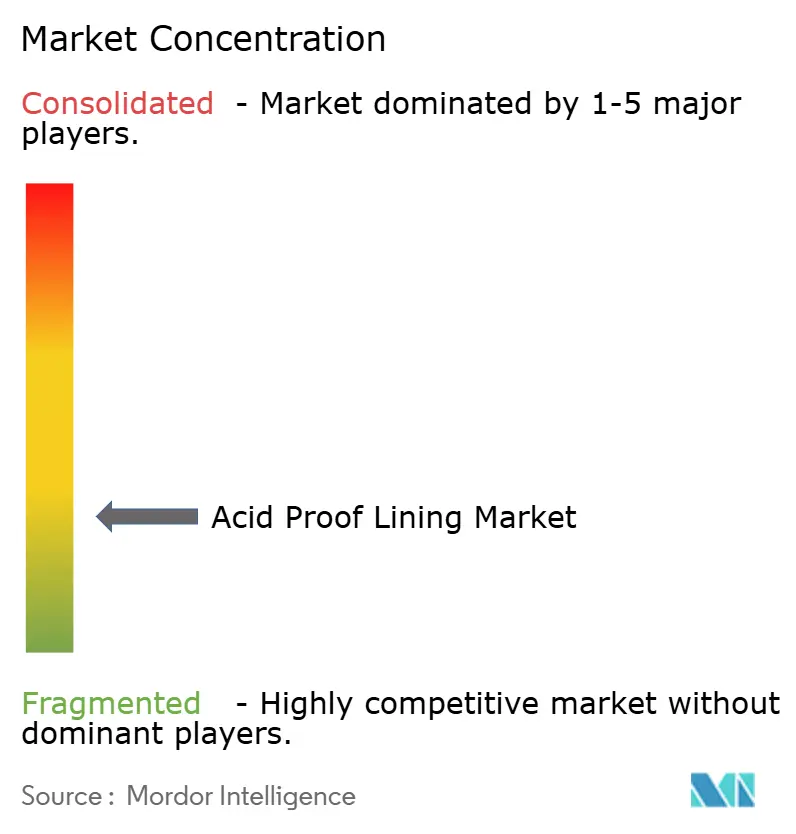

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acid Proof Lining Market Analysis by Mordor Intelligence

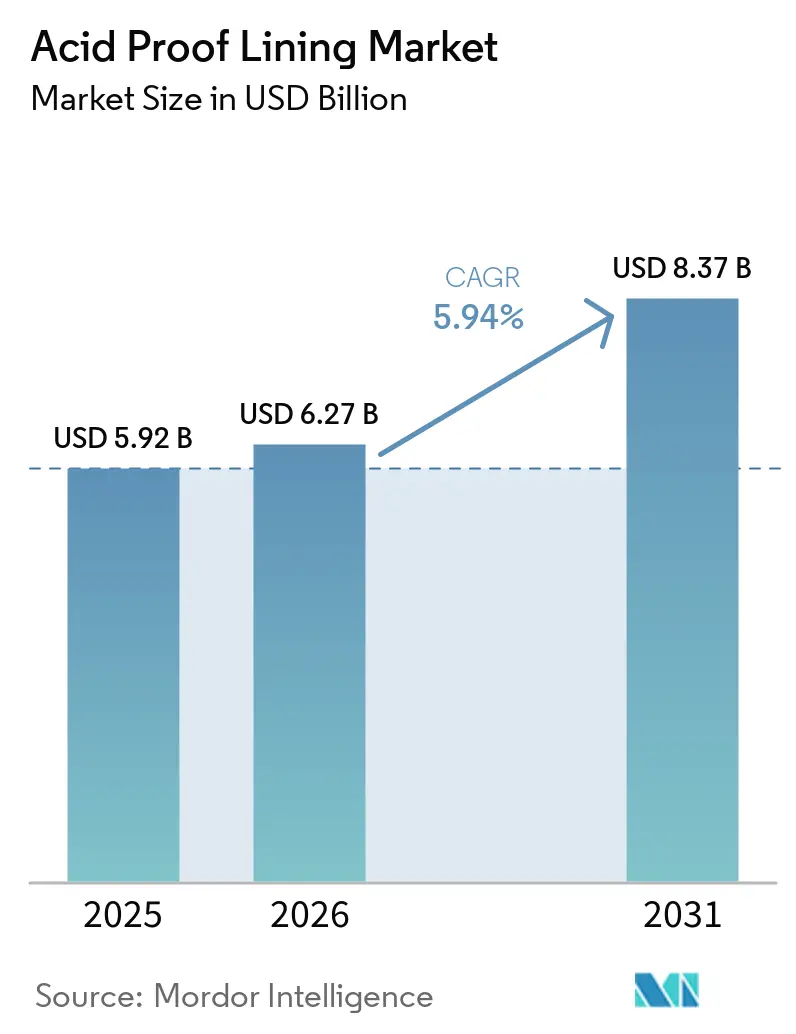

The Acid Proof Lining Market size is projected to be USD 5.92 billion in 2025, USD 6.27 billion in 2026, and reach USD 8.37 billion by 2031, growing at a CAGR of 5.94% from 2026 to 2031. Operators now treat corrosion protection as a capital-preservation tool, not a maintenance cost, because every day of unplanned downtime can erase millions in gross margin. China’s 2026-2029 petrochemical equipment plan mandates corrosion-resistant linings in all new and refurbished units, ensuring multi-year demand and reducing project-cycle volatility. A simultaneous wave of desalination investment in the Middle-East, led by Saudi Arabia’s USD 675 million Rabigh 4 IWP, favors ceramic brick and fluoropolymer linings that withstand hypersaline brine and chlorine biocides, offering better performance compared to legacy epoxy systems. Technological advancements in power, semiconductor, and hydrogen value chains are driving the acid proof lining market by introducing premium, high-performance systems into environments previously considered too harsh for polymers. Supply consolidation is progressing as global companies acquire certified applicators to maintain quality and manage rising compliance costs under new ISO standards.

Key Report Takeaways

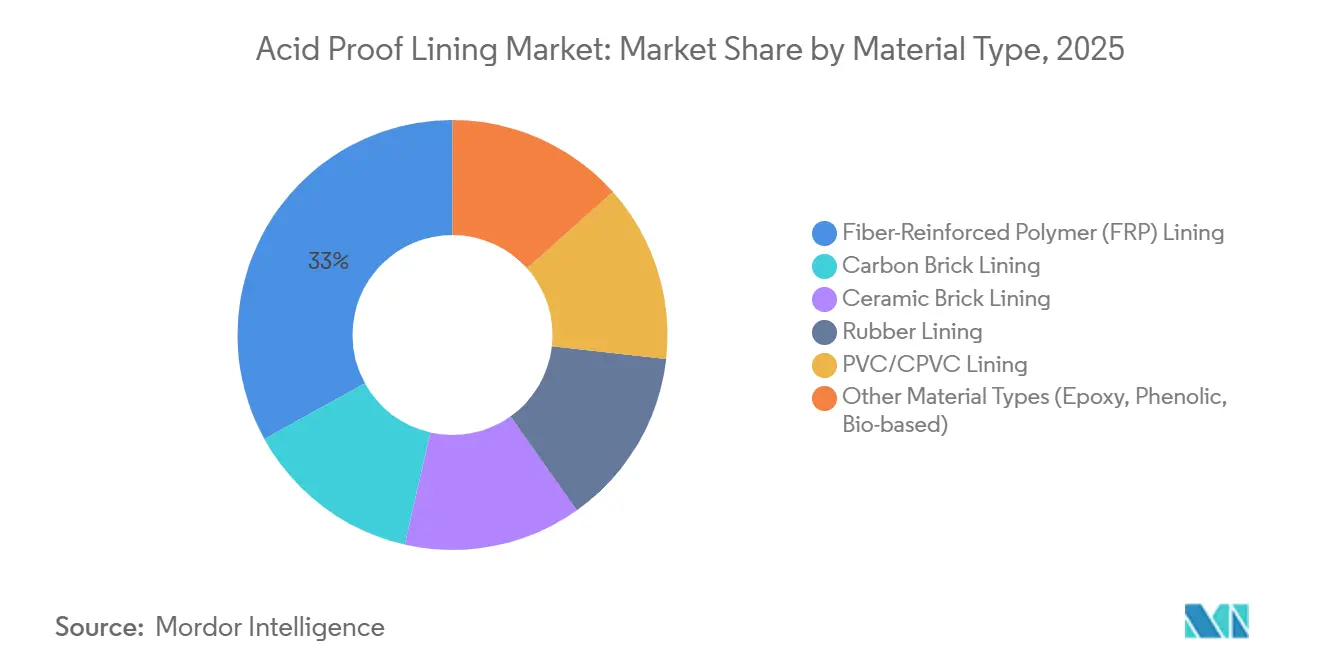

- By material type, fiber-reinforced polymer (FRP) lining captured 33.03% of the acid proof lining market share in 2025, while other materials (epoxy, phenolic, bio-based) are projected to advance at a 6.42% CAGR through 2031.

- By lining type, tile lining captured 75.75% of the acid proof lining market share in 2025; however, monolithic lining led growth at a 6.73% CAGR through 2031.

- By application, tanks and vessels held 25.88% of the acid proof lining market share in 2025, while towers and reactors are forecast to expand at a 6.89% CAGR through 2031.

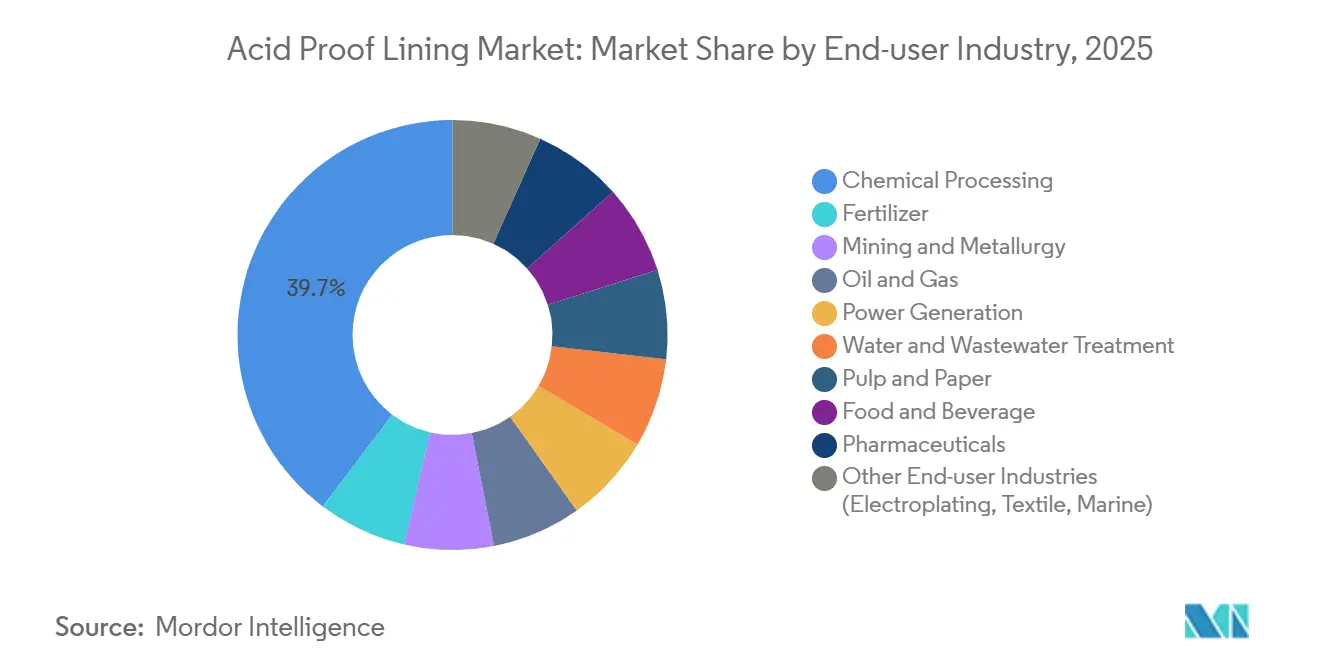

- By end-user industry, chemical processing anchored demand with 39.69% of the acid proof lining market share in 2025, whereas power generation is the fastest-growing vertical at a 7.20% CAGR through 2031.

- By geography, Asia-Pacific held 46.27% of the acid proof lining market share in 2025 and is set to grow at a 6.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acid Proof Lining Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising corrosion-resistant demand in chemical processing | +1.8% | Global, with concentration in Asia-Pacific and Middle-East | Medium term (2-4 years) |

| Expansion of wastewater and desalination infrastructure | +1.3% | Middle-East, Asia-Pacific (India, ASEAN), North America | Long term (≥ 4 years) |

| Refurbishment of aging industrial assets | +1.1% | North America, Europe, Japan | Short term (≤ 2 years) |

| Tightening worker-safety durability mandates | +0.9% | Global, led by EU and North America | Medium term (2-4 years) |

| Demand for HF-resistant linings in semiconductor etching | +0.6% | Asia-Pacific (Taiwan, South Korea, Japan), North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Corrosion-Resistant Demand in Chemical Processing

Process operators are increasing reaction conditions to boost yield, which accelerates corrosion on legacy carbon-brick systems and drives demand for duplex stainless and high-build glass-flake linings that extend service intervals from 18 months to 5 years. Unplanned shutdowns at large ammonia-urea complexes cost USD 2 million-USD 4 million per day, making durability a direct factor in protecting profit. Procurement tenders now require a minimum 15-year design life and ISO 16276-1:2025 certification, reducing the pool of approved vendors and increasing average bid values. Semiconductor fabs transitioning to 2-nanometer nodes have doubled hydrofluoric-acid exposure, increasing demand for premium PFA and PTFE linings that ensure zero ionic contamination. This has created a bifurcated acid proof lining market: commodity plants opt for cost-efficient vinyl-ester systems, while ultrapure environments pay three-to-five-times premiums for fluoropolymers.

Expansion of Wastewater and Desalination Infrastructure

Municipal and industrial wastewater capacity is expanding across the Asia-Pacific and the Middle-East as governments prioritize water security. Desalination plants expose linings to hypersaline brine, sulfuric-acid dosing, and continuous chlorine injection, conditions that ceramic brick can endure for 30 years with minimal permeation. Polyurea membranes, sprayed at 3 millimeters thickness, cure quickly and reduce downtime on retrofit work by 24 hours per tank, cutting maintenance budgets by 60% over a decade. Failure risk is costly: a single outage at a 500,000 m³-per-day plant triggers USD 1.5 million in water-purchase penalties. Regulatory tightening, such as China’s 2025 GB 8978 heavy-metal limits, requires manufacturers to install acid-resistant linings in neutralization vessels to prevent contaminant leaching.

Refurbishment of Aging Industrial Assets

Approximately 60% of North American and European chemical plants are over 25 years old, leading to a preference for refurbishment over replacement to save capital and expedite project approvals. HDPE retrofits in sulfuric-acid units at Austria’s Schwechat refinery extended design life by 20 years at one-fifth the cost of new vessels. Glass-flake epoxy restored 95% heat-transfer efficiency in a Florida coal plant’s FGD absorber, delaying a USD 30 million scrubber replacement by 8 years. Surface preparation is critical: achieving Sa2.5 blast cleanliness in humid climates can increase labor hours by 40%, while shortcuts halve adhesion and void warranties. Data from Japan shows piping failures decreased from three to one annually after disciplined preparation and PVC relining, reducing downtime by 75%.

Tightening Worker-Safety Durability Mandates

Regulators now link lining durability with occupational safety. OSHA’s 2024 revision requires firms to document service life and replacement schedules for vessels storing Category 1 corrosives[1]OSHA, “Hazard Communication Standard Update 2024,” osha.gov. Three new ISO standards published in 2025 (ISO 21207, ISO 16276-1, ISO 16701) outline mandatory surface-preparation, inspection, and system-selection steps, raising compliance requirements and eliminating under-equipped contractors. Europe’s Machinery Regulation, effective January 2025, shifts liability to OEMs, prompting equipment suppliers to specify proven linings to mitigate recall risks. Compliance costs are driving mergers and acquisitions, such as Sika’s USD 247 million purchase of Akkim, which added ISO-certified capacity in cost-sensitive emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and lifecycle cost | -0.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Skilled-applicator scarcity and complex procedures | -0.5% | North America, Europe, Middle-East | Medium term (2-4 years) |

| Low awareness among SMEs | -0.4% | Asia-Pacific (excluding Japan), South America, Middle-East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation and Lifecycle Cost

Installed costs range between USD 150 and USD 600 per m², with specialty fluoropolymers being twenty times more expensive than commodity rubber systems, deterring projects with 3-to-5-year payback periods. Humid environments further increase costs, as meeting Sa2.5 blast standards can account for 40% of total labor hours. Chinese methanol plants in 2026 attracted only three bids on a corrosion-reinforcement tender, indicating that price barriers are reducing the contractor base. Material costs also vary significantly; heavy-duty epoxies priced at CNY 50–150 per kg translate to installed costs of CNY 200–500 per m² when labor and scaffolding are included.

Skilled-Applicator Scarcity and Complex Procedures

ASTM reports fewer than 12,000 certified applicators in North America, a 20% decline since 2019, tightening labor availability and increasing wages. Fluororesin powder coating for semiconductor tools requires multi-stage baking that only 15 Japanese contractors can perform to pinhole-free standards. A single pinhole in a 500 m² tank can lead to lateral corrosion and necessitate recoating within two years. High-pressure polyurea spraying also requires dew-point management, limiting workable days to 60% of the calendar year in coastal China. ISO-certified firms achieve a 95% first-pass success rate, while uncertified contractors face 30% rework rates, doubling project costs and eroding buyer trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Fiber-Reinforced Polymer (FRP) Lining Holds Ground as Other Materials Accelerate

Fiber-reinforced polymer (FRP) lining accounted for 33.03% of 2025 revenue, emphasizing its adaptability across temperature ranges from −40 °C to 120 °C and compatibility with a wide range of chemical classes. Carbon brick remains relevant in reactors operating above 200 °C but is labor-intensive to install. Ceramic brick performs well in abrasive slurry applications but increases structural weight by 15%. Rubber continues to dominate in mining applications where impact resistance is critical.

The other materials segment, including epoxy, phenolic, and bio-based options, is projected to grow at a 6.42% CAGR through 2031, driven by a shift away from petroleum-based systems as buyers increasingly prioritize CO₂ footprint reductions in procurement decisions. Soy-based Soy-PK epoxy, which achieves tensile strength exceeding 25 MPa and reduces embodied carbon by 40%, is gaining traction in food-grade tank linings. PVC and CPVC remain key materials in pharmaceutical processing due to FDA compliance, but upcoming chlorine restrictions under REACH regulations may impact their medium-term outlook.

By Lining Type: Seamless Monolithic Lining Advance in Speed and Integrity

Tile linings accounted for 75.75% of 2025 revenue, supported by decades of field data demonstrating 25-year durability in sulfuric and phosphoric acid applications. Brick linings remain relevant in chimney and stack retrofits where refractory properties are essential.

Monolithic linings are expected to grow at a 6.73% CAGR through 2031, driven by the adoption of plural-component spray systems that cure within minutes, enabling 24-hour turnaround times and reducing outage windows by 50%. Glass-flake epoxies, which incorporate up to 40% flake by weight, reduce permeability tenfold compared to standard epoxy and meet ultrapure pharmaceutical standards. Seamless membranes also distribute stress more evenly than grouted tiles, as confirmed by finite-element simulations of cyclic pressure loads in hydrogen reactors.

By Application: Towers and Reactors Emerge as Growth Epicenter

Tanks and vessels accounted for 25.88% of 2025 demand, reflecting their widespread use across industries. However, growth in this segment aligns more closely with GDP trends than technological advancements. Storage and containment applications rely on standard specifications, making price a key factor in procurement decisions. Ducts and flues benefit from environmental retrofits but face limited growth due to plateauing coal capacity.

Towers and reactors are projected to grow at a 6.89% CAGR through 2031, driven by advancements in green hydrogen electrolyzers and high-temperature acid gas absorbers. The acid proof lining market for electrolyzer stacks is supported by projects like Austria’s H2FUTURE, which specifies PFA linings for a 10-year duty cycle in 80 °C KOH environments. Ceramic-lined caustic towers, such as those at Hamburg’s 100 MW hub, demonstrate a willingness among operators to invest in premium solutions for 30-year service life in hot alkali conditions.

By End-user Industry: Power Generation Surges, Chemical Processing Anchors

Chemical processing held a 39.69% revenue share in 2025, driven by the large number of plants and the variety of corrosive feedstocks. For example, new fertilizer complexes in India alone required approximately 250,000 m² of lining in 2025. Mining and metallurgy are maturing at a slower pace but are seeing material innovations, such as silicone-rubber linings that extend service life eightfold in gold leach tanks.

Power generation is the fastest-growing end-user industry, with a projected CAGR of 7.20% through 2031. This growth is fueled by coal station retrofits for flue gas desulfurization (FGD) systems and the scaling of green hydrogen infrastructure. The acid proof lining market for FGD absorbers is expanding as scrubbers expose carbon steel to pH 2-4 environments, necessitating glass-flake or vinyl-ester coatings with 15-year durability certifications. Additionally, proton-exchange-membrane electrolyzer projects funded by the U.S. Department of Energy in 2025 are driving demand for premium linings capable of withstanding acid circulation loops[2]U.S. Department of Energy, “PEM Electrolyzer Funding Awards,” doe.gov.

Geography Analysis

Asia-Pacific contributed 46.27% of global revenue in 2025 and is expected to grow at a 6.92% CAGR through 2031. Growth is supported by China’s petrochemical upgrade initiatives, India’s fertilizer plant expansions, and Japan’s refurbishment projects driven by diagnostic assessments. South Korea and Taiwan’s semiconductor industries require HF-resistant containment, while ASEAN’s waste-to-energy plants drive demand for FGD linings despite permitting delays.

North America faces challenges from an aging plant infrastructure and labor shortages, which have increased installation costs by up to 35%. U.S. federal funding for water infrastructure is driving demand for wastewater digester linings, while nearshoring in Mexico is boosting demand for electronics wastewater systems. However, contractor shortages are slowing project execution.

Europe’s market is shaped by regulatory mandates requiring lining upgrades in chemical and pharmaceutical facilities. Germany’s BASF is consolidating capacity while reinvesting in protective systems, and the UK’s post-Brexit pharmaceutical growth is driving demand for FDA-compliant epoxy linings. Nordic green hydrogen pilot projects are contributing small but strategic volumes.

South America, and Middle-East and Africa accounted for smaller shares of the market. In South America, Brazil’s pulp industry expansions and Argentina’s lithium brine projects are driving demand for caustic-resistant linings. In the Middle-East, Saudi Arabia’s Rabigh 4 and the UAE’s Hatta desalination projects are key contributors. South Africa’s mining sector faces challenges from power outages, delaying maintenance activities to 2026-2027.

Competitive Landscape

The acid proof lining market is characterized by low concentration, with key players including STEULER-KCH GmbH, Chemco International Ltd, Jotun, The Sherwin-Williams Company, and Saint-Gobain. Sika’s 2026 acquisition of Akkim expanded its certified application capacity in cost-sensitive regions and added proprietary polyurethane products. Saint-Gobain’s 2024 acquisition of Brazil’s Ovniver extended its ceramic solutions into South America’s pulp and mining industries.

Competition varies by application. Commodity tank linings are dominated by local suppliers like Kothari Corrosion Controllers, which operate at 12-18% gross margins. In contrast, semiconductor and pharmaceutical projects command higher margins of 35-45% due to stringent ISO 12944-8:2017 and FDA certification requirements. Hempel is leveraging its marine silicone technologies for process industries, as demonstrated by Hempaguard NB applications on Maersk hulls, which validate fouling-release chemistry for land-based assets.

Growth opportunities exist in green hydrogen, waste-to-energy, and bio-based linings. Startups developing graphene-enhanced epoxies show promise with self-healing capabilities, though none have yet passed the 10,000-hour accelerated aging test. The adoption of digital twins is widening performance gaps, with multinationals using sensor networks for predictive corrosion modeling, while smaller enterprises rely on traditional calendar-based inspections. This trend favors suppliers that integrate monitoring with maintenance services.

Acid Proof Lining Industry Leaders

STEULER-KCH GmbH

Chemco International Ltd

Jotun

Saint-Gobain

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BASF inaugurated an expanded and modernized dispersion production facility in Durban, South Africa. This development supported the acid proof lining market by enhancing the availability of high-quality dispersion materials used in protective coatings.

- February 2026: Hempel A/S applied its Hempaguard NB silicone coating to newbuild vessels for Maersk at Yangzijiang Shipyard in China. This demonstrated the relevance of advanced coating technologies in the acid proof lining market by showcasing their ability to provide durable protection and integrate seamlessly into industrial workflows.

Global Acid Proof Lining Market Report Scope

Acid proof lining is a corrosion-resistant protective system, typically utilizing tiles, bricks, or resins, applied to concrete and steel surfaces to prevent damage caused by acids, alkalis, and solvents. It is widely used in industrial settings to safeguard tanks, vessels, and floors in chemical, petrochemical, and food processing facilities.

The Acid Proof Lining Market is segmented into material type, lining type, application, end-user industry, and geography. By material type, the market is segmented into fiber-reinforced polymer (FRP) lining, carbon brick lining, ceramic brick lining, rubber lining, PVC/CPVC lining, and other material types (epoxy, phenolic, bio-based). By lining type, the market is segmented into tile lining, brick lining, monolithic lining, and membrane lining. By application, the market is segmented into tanks and vessels, storage and containment systems, ducts, pipes, and flues, floors and drains, towers and reactors, and chimneys and stacks. By end-user industry, the market is segmented into chemical processing, fertilizer, mining and metallurgy, oil and gas, power generation, water and wastewater treatment, pulp and paper, food and beverage, pharmaceuticals, and other end-user industries (electroplating, textile, marine). The report also covers the market size and forecasts for acid proof lining in 19 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Fiber-Reinforced Polymer (FRP) Lining |

| Carbon Brick Lining |

| Ceramic Brick Lining |

| Rubber Lining |

| PVC/CPVC Lining |

| Other Material Types (Epoxy, Phenolic, Bio-based) |

| Tile Lining |

| Brick Lining |

| Monolithic Lining |

| Membrane Lining |

| Tanks and Vessels |

| Storage and Containment Systems |

| Ducts, Pipes and Flues |

| Floors and Drains |

| Towers and Reactors |

| Chimneys and Stacks |

| Chemical Processing |

| Fertilizer |

| Mining and Metallurgy |

| Oil and Gas |

| Power Generation |

| Water and Wastewater Treatment |

| Pulp and Paper |

| Food and Beverage |

| Pharmaceuticals |

| Other End-user Industries (Electroplating, Textile, Marine) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Material Type | Fiber-Reinforced Polymer (FRP) Lining | |

| Carbon Brick Lining | ||

| Ceramic Brick Lining | ||

| Rubber Lining | ||

| PVC/CPVC Lining | ||

| Other Material Types (Epoxy, Phenolic, Bio-based) | ||

| By Lining Type | Tile Lining | |

| Brick Lining | ||

| Monolithic Lining | ||

| Membrane Lining | ||

| By Application | Tanks and Vessels | |

| Storage and Containment Systems | ||

| Ducts, Pipes and Flues | ||

| Floors and Drains | ||

| Towers and Reactors | ||

| Chimneys and Stacks | ||

| By End-user Industry | Chemical Processing | |

| Fertilizer | ||

| Mining and Metallurgy | ||

| Oil and Gas | ||

| Power Generation | ||

| Water and Wastewater Treatment | ||

| Pulp and Paper | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Other End-user Industries (Electroplating, Textile, Marine) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the acid proof lining market?

The acid proof lining market stands at USD 6.27 billion in 2026 and is projected to reach USD 8.37 billion by 2031.

Which material type leads revenue in 2025?

Fiber-reinforced polymer (FRP) lining led with a 33.03% share in 2025 due to their balance of chemical resistance and mechanical strength.

What drives demand in power generation industry?

Flue-gas desulfurization retrofits and acid-based hydrogen electrolyzers require durable linings that can survive low-pH, high-temperature media.

Why are monolithic linings gaining momentum through 2031?

Seamless polyurea and glass-flake epoxy systems cut outage windows in half and remove grout-line failure points, driving 6.73% CAGR growth through 2031.

Page last updated on: