Acetic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

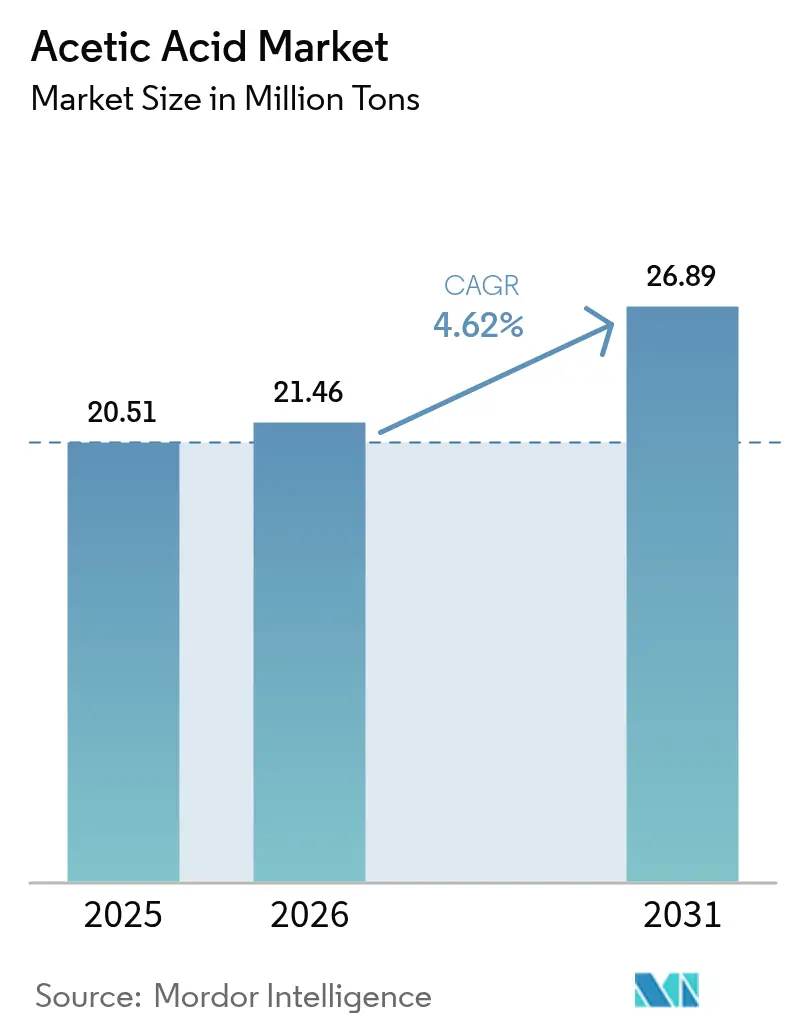

| Market Volume (2026) | 21.46 Million tons |

| Market Volume (2031) | 26.89 Million tons |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acetic Acid Market Analysis by Mordor Intelligence

The Acetic Acid Market size is projected to expand from 20.51 Million tons in 2025 and 21.46 Million tons in 2026 to 26.89 Million tons by 2031, registering a CAGR of 4.62% between 2026 to 2031. Strong derivative demand, led by vinyl acetate monomer (VAM) adhesives and polyester-chain purified terephthalic acid (PTA), anchors this expansion, while China’s capacity additions and North American low-carbon projects redraw the global supply map. Catalyst availability is tightening because methanol carbonylation dominates production and relies on rhodium and iridium, metals also coveted by fuel-cell makers. Regulatory tailwinds—most notably the U.S. Environmental Protection Agency’s 2025 low-VOC rule—are accelerating acetate-ester solvent substitution in coatings. Parallel decarbonization efforts, including Celanese’s ISCC-certified carbon-capture-and-utilization (CCU) methanol and Lenzing’s CO₂-neutral beech-wood route, show incumbents pivoting toward carbon-intensity as a selling point alongside price. Emerging electro-fuel pilots that convert captured CO₂ directly into acetate offer a long-term technology hedge, provided renewable electricity remains cheap.

Key Report Takeaways

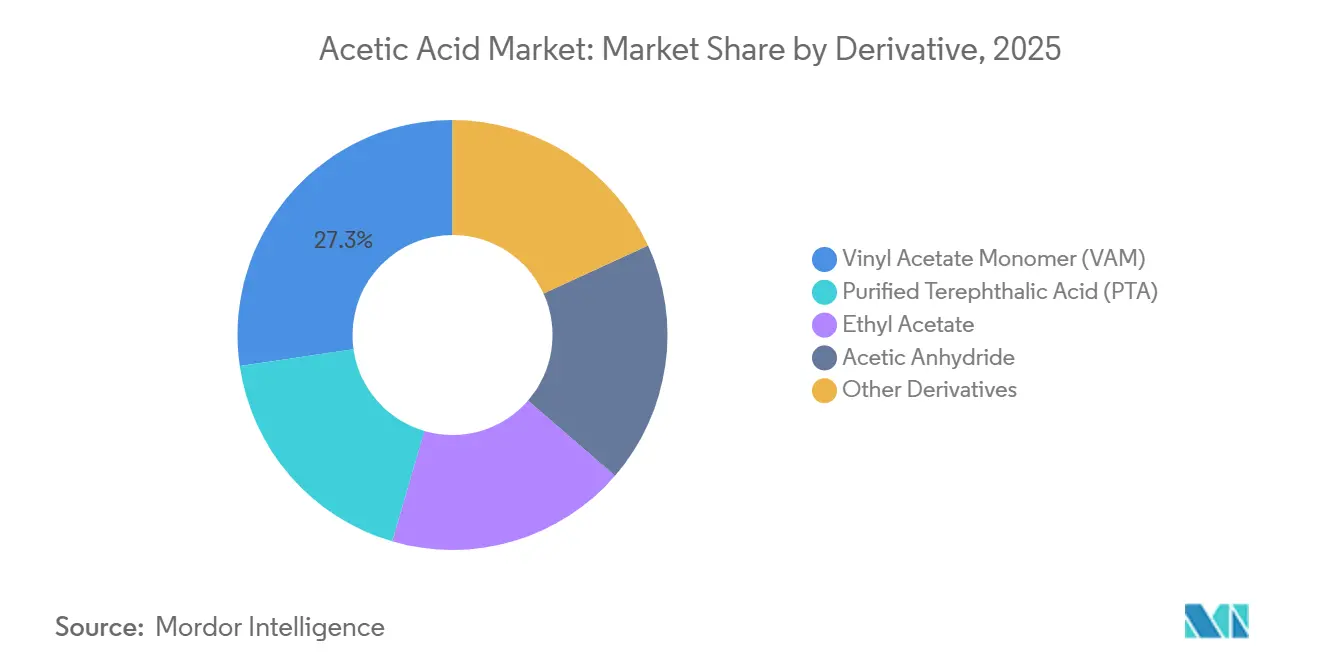

- By derivative, vinyl acetate monomer captured 27.30% of the acetic acid market share in 2025, while purified terephthalic acid is projected to record the fastest 4.98% CAGR through 2031.

- By production route, methanol carbonylation held 84.59% share of the acetic acid market size in 2025, while bio-based fermentation is on course for a 5.67% CAGR to 2031.

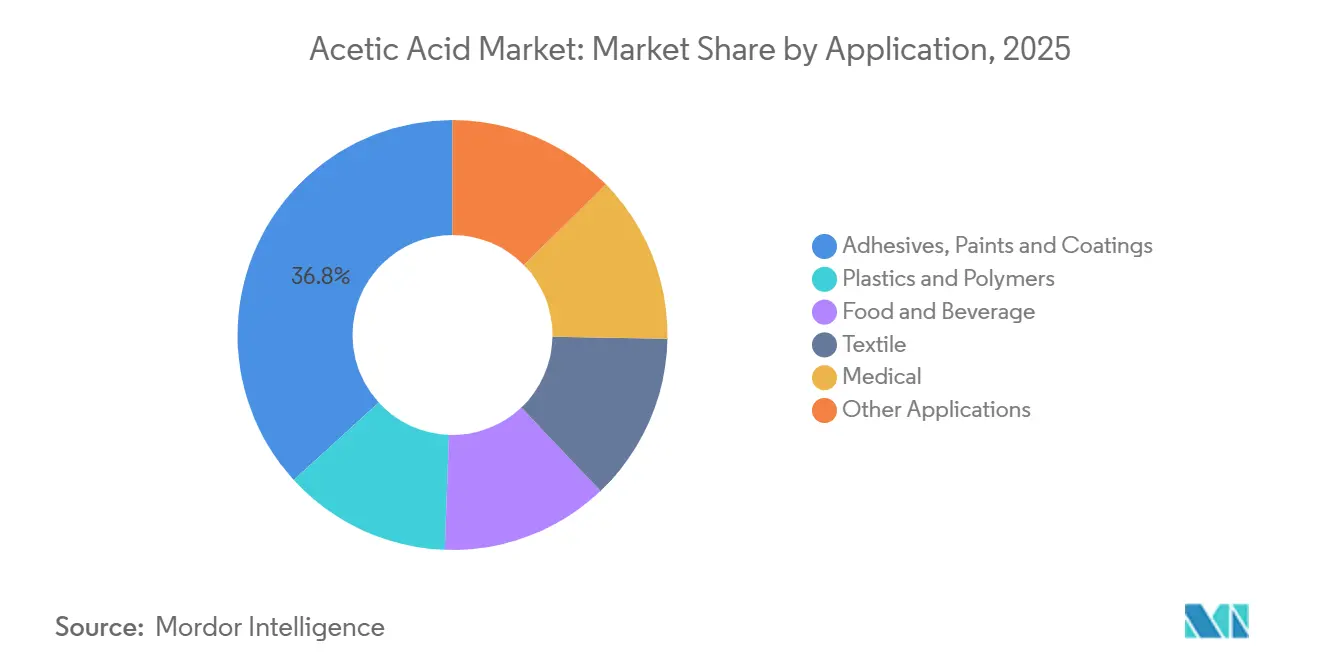

- By application, adhesives, paints, and coatings held 36.78% share of the acetic acid market size in 2025, while medical is on course for a 6.58% CAGR to 2031.

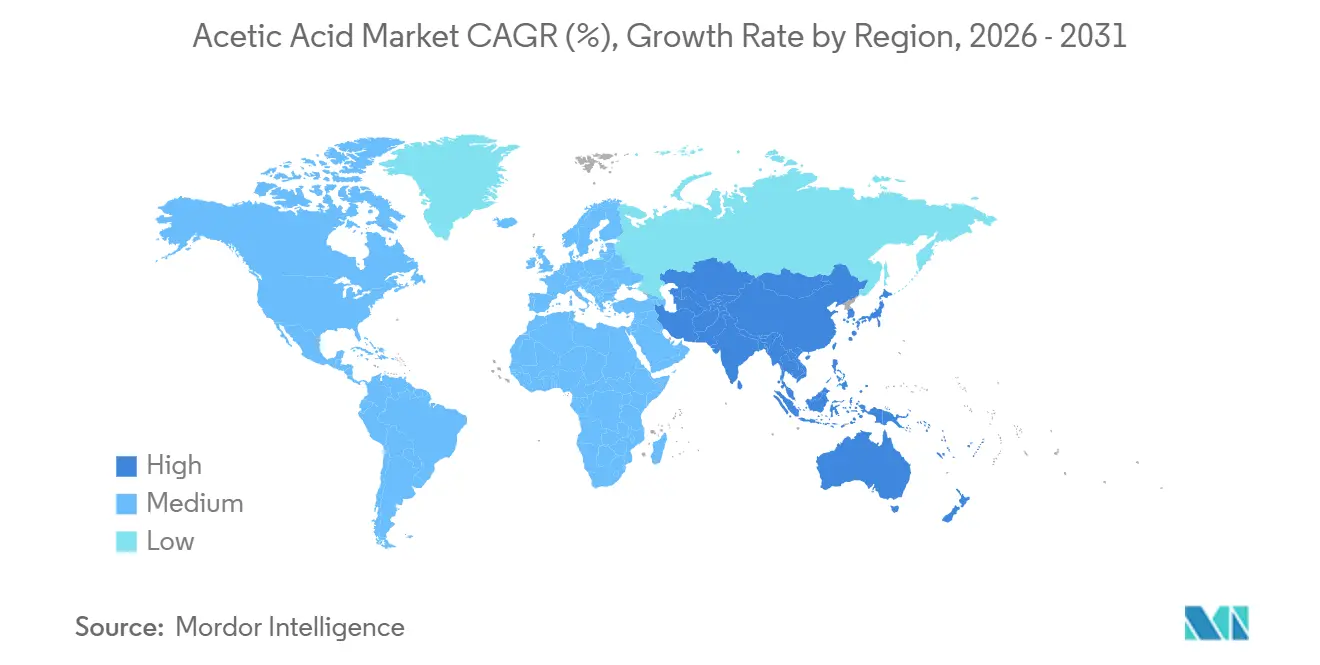

- By geography, Asia-Pacific accounted for 69.15% of the 2025 volume and is set to expand at a 5.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acetic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Vinyl Acetate Monomer Demand | +1.2% | Global, with concentration in Asia-Pacific (China, India, ASEAN) and North America | Medium term (2-4 years) |

| Steady PTA Capacity Additions in Asia | +0.9% | Asia-Pacific core (China, India, South Korea, Taiwan), spill-over to Middle-East | Long term (≥ 4 years) |

| Expansion of Acetate-Ester Solvents in High-Solids Coatings | +0.6% | North America and EU, with regulatory-driven adoption in California and EU Green Deal jurisdictions | Short term (≤ 2 years) |

| Bio-Based Acetic Acid Pathways Scaling Under Net-Zero Mandates | +0.4% | Europe (Sweden, Austria), India, and pilot zones in China; policy-linked adoption | Long term (≥ 4 years) |

| CO₂-to-Acetic Acid Electro-Fuel Pilots | +0.2% | Europe, China, and Middle-East (UAE); demonstration-phase with limited commercial scale | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Vinyl Acetate Monomer Demand

VAM consumed 27.30% of global acetic acid in 2025, and downstream converters continue to shift toward water-based adhesives and packaging films. Producer strategies now favor integrated ethylene-acetic acid complexes to buffer raw-material volatility; Celanese and LyondellBasell both advanced such assets in the United States. India remains entirely import-dependent for VAM, a gap that invites backward-integrated local projects. Technology licensing agreements—such as KBR’s tie-up with Showa Denko—have tightened regional intellectual-property control, further anchoring new VAM builds close to reliable acetic acid supply. Premium high-purity grades for photovoltaic encapsulants and barrier packaging are adding specification pressure upstream.

Steady PTA Capacity Additions in Asia

PTA producers in China, India, South Korea, and Taiwan continued to debottleneck or add lines through 2025, reinforcing a geographic clustering that localizes acetic acid pull. Indorama Ventures retained 4.1 million tons per year of PTA capacity in Asia after closing European and Canadian plants, a pivot that shifts oxidation-solvent demand eastward. PTA’s role as solvent user, coupled with rapid polyester fiber and bottle-resin growth, underpins the acetic acid market regardless of VAM cycles. Co-located acetyl chains lower freight risk—a lesson highlighted by 2024 supply disruptions in the Suez and Red Sea corridors. Over the forecast horizon, incremental PTA-driven demand will concentrate in coastal China and the Indian subcontinent, encouraging joint-venture acetic acid units or long-term offtake contracts.

Expansion of Acetate-Ester Solvents in Coatings

The U.S. EPA’s January 2025 aerosol-coatings amendment assigned acetic acid a Reactivity Factor of 0.68 g O₃ g-¹ VOC, well below the default 18.50 threshold[1]U.S. Environmental Protection Agency, “National Volatile Organic Compound Emission Standards for Aerosol Coatings,” epa.gov . Formulators are therefore substituting aromatic solvents with ethyl, butyl, and isopropyl acetates derived from acetic acid to meet July 2025 compliance. Parallel initiatives under the EU Green Deal amplify this switch in Europe, while California’s South Coast Air Quality Management District already mandates low-VOC paints. LyondellBasell and INEOS have each expanded glacial-grade supply chains to capture this solvent demand shift. Producers able to certify bio-attributed or ISCC-plus streams gain a pricing premium in jurisdictions that demand product-carbon-footprint disclosure.

Bio-Based Pathways Scaling Under Net-Zero Mandates

Bio-based fermentation-derived acetic acid is forecast to rise at 5.67% CAGR through 2031 as policy targets tighten. Sekab converts Nordic forestry residues to ethanol and then acetic acid under ISCC certification. Lenzing launched a CO₂-neutral beech-wood line in 2024, aimed at pharmaceutical and food users. In India, Godavari Biorefineries lobbies for bio-chemical incentives akin to the nation’s ethanol-blending scheme, reflecting emerging regulatory support. Although economics lag when fossil-methanol prices soften, scope-3 emission reporting under mechanisms such as the EU Carbon Border Adjustment Mechanism is pushing buyers to consider carbon-intensity alongside cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Methanol Feedstock Pricing | -0.8% | Global, with acute impact in China (coal-based methanol) and North America (shale-gas-derived methanol) | Short term (≤ 2 years) |

| Anti-Dumping and Tariff Actions on Chinese Exports | -0.5% | EU, India, and potential U.S. actions; affects trade flows and regional pricing | Medium term (2-4 years) |

| Rhodium/Iridium Catalyst Supply Risk Amid Fuel-Cell Boom | -0.3% | Global, with supply concentration in South Africa and Russia; acute for methanol-carbonylation producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Methanol Feedstock Pricing

Methanol represents the largest variable cost in carbonylation routes, and its price swings compress producer margins. Coal-based methanol in China is vulnerable to domestic energy curbs, while North American natural-gas methanol enjoys lower feedstock costs but faces logistics shocks when container supply tightens. Vertical integration, such as the Fairway Methanol joint venture that supplies Celanese’s Clear Lake unit, insulates against spot volatility. Green-methanol initiatives could offer a hedge, yet present volumes remain too small for broad price stabilization.

Anti-Dumping and Tariff Actions on Chinese Exports

China’s export surge—driven by overcapacity and sub-70% utilization—has already prompted antidumping reviews in related oxygenates. The European Commission used Colombian acetic acid as a benchmark in a 2024 glyoxylic-acid probe[2]European Commission, “Commission Implementing Regulation on Glyoxylic Acid,” europa.eu . India, now the world’s largest importer, has the legal precedent and political motivation to impose duties if volumes threaten domestic producers. Any trade remedy would distort regional price parity and reroute Chinese cargoes toward tariff-free destinations, adding uncertainty to the acetic acid market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: VAM Anchors Growth, PTA Accelerates

Vinyl acetate monomer held 27.30% of the acetic acid market share in 2025, while purified terephthalic acid (PTA) is forecast to post the quickest 4.98% CAGR, driven by polyester fiber and bottle-grade resin capacity in South and Southeast Asia. VAM’s footprint is mature in North America and Europe but still expanding in India, where total reliance on imports spotlights a strategic opportunity for integrated complexes.

PTA’s oxidation process uses acetic acid as a solvent; hence, each new reactor directly lifts the acetic acid market size allocated to this derivative. Indorama Ventures’ Asian PTA hub, coupled with China’s coastal mega-projects, ensures PTA remains the volume engine through 2031. Conversely, ethyl acetate and other acetate esters gain incremental share in high-solids coatings, spurred by regulatory VOC limits. Niche derivatives such as diketene and monochloroacetic acid offer higher margins, rewarding producers that can deliver pharmaceutical-grade purity.

By Production Route: Carbonylation Dominates, Bio-Fermentation Emerges

Methanol carbonylation commanded 84.59% of 2025 output, underlining the acetic acid market’s dependence on rhodium- and iridium-based catalysts. Ethylene and acetaldehyde oxidation routes persist as hedges against metal-supply risk, exemplified by LyondellBasell’s 2026 glacial-grade addition at La Porte.

Bio-based fermentation is modest but growing at a forecast 5.67% CAGR, thanks to Sekab’s forestry-residue pathway and Lenzing’s CO₂-neutral beech-wood acid. These streams carry verified life-cycle carbon reductions, positioning them for premium pricing in regions where buyers must disclose cradle-to-gate emissions. Electro-fuel pilots add a long-run wildcard: if energy-efficiency improves beyond the current 32% benchmark, direct CO₂-to-acetic-acid synthesis can decouple supply from fossil methanol entirely.

By Application: Coatings Lead, Medical Surges

Adhesives, paints, and coatings represented 36.78% of the acetic acid market size in 2025, reflecting VAM-based emulsions and expanding acetate-ester solvent demand under evolving VOC rules. Medical is projected to rise at 6.58% CAGR due to antiseptic formulations and excipient roles in fast-growing emerging-market drug manufacturing.

Textiles and polymers, including PTA-based polyester and cellulose acetate fibers, remain steady contributors, buoyed by Asia’s apparel and filtration-tow outlook. Food and beverage applications, principally vinegar, post slower but value-rich growth because of stringent food-grade purity requirements, a niche that bio-based routes can exploit by marketing natural provenance.

Geography Analysis

Asia-Pacific controlled 69.15% of global volume in 2025 and is expected to advance at 5.15% CAGR through 2031, propelled by Chinese capacity additions that will lift national nameplate to 17.06 million tons by end-2025. India’s offtake jumped 32% year-on-year between January 2024 and January 2025, underscoring both robust consumption and acute import reliance. ASEAN manufacturing expansion—USD 66 billion in apparel exports and USD 31 billion in electronics greenfields during 2024—adds steady downstream pull for dyes, coatings, and adhesives.

North America demand is anchored by Celanese’s 1.3 million ton CCU-enabled Clear Lake expansion and LyondellBasell’s ethylene-route project slated for 2026. Abundant shale gas underpins feedstock economics, while federal tax credits for carbon capture improve margins for CCU methanol.

Europe remains structurally short; producers are studying cracker conversions and circular-feed initiatives such as Mitsubishi Chemical’s super-critical water plastics-to-oil plant and Mitsui Chemicals’ bio-and-circular cracker roll-out. Carbon Border Adjustment Mechanism reporting, effective in its transitional phase, compels importers to reveal embedded emissions, indirectly favoring low-carbon acetic acid supply chains.

Middle-East capacity centers on Sipchem’s 460 kiloton Jubail unit, which feeds an internal VAM line and leverages abundant CO supply. Africa and South America remain net importers but hold localized demand in beverage, textile, and agrochemical processing.

Mordor Intelligence provides coverage of the acetic acid market across other key regional markets, including North America and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Value Chain Analysis

The acetic acid value chain starts with feedstocks (methanol from coal in China and natural gas in North America, plus CO) and noble-metal catalysts, then moves into production that is dominated by methanol carbonylation (84.59% share in 2025) using rhodium/iridium catalyst systems such as Monsanto/Cativa-type technologies. Many producers pursue vertical integration into methanol and utilities to manage exposure to methanol price swings and catalyst availability, while alternate routes (ethylene or acetaldehyde oxidation) remain key hedges for supply security when carbonylation inputs tighten.

On the downstream side, bulk volumes feed into major derivative chains (VAM, PTA solvent use, ethyl acetate, and acetic anhydride), with volumes split across contract supply for integrated complexes and merchant trade into regions that are structurally short, notably Europe. Logistics and operating reliability shape landed costs: disruptions around the Suez/Red Sea corridor in 2024-2025 highlighted freight-time and inventory risks for Europe and Africa, and routine turnarounds at large units can tighten spot availability. This dynamic reinforces the advantage of co-located acetyl chains and long-term offtake contracts for major consumers in adhesives, coatings, and polyester intermediates.

Competitive Landscape

The acetic acid market is moderately concentrated. Celanese and INEOS have invested in low-carbon or large-scale additions: Celanese’s CCU-methanol Clear Lake debottleneck and INEOS’s upcoming 1 million ton Daishan joint venture using Cativa technology. Shandong Hualu-Hengsheng Chemical leads Chinese production at roughly 1.5 million tons, illustrating domestic consolidation.

Technology differentiation is sharpening. Celanese earned U.S. Department of Energy validation for its ECO-CC low-carbon acid in 2024, while Lenzing commercialized CO₂-neutral wood-based volumes. LyondellBasell’s ethylene-oxidation unit hedges against rhodium-iridium risk. Smaller integrators such as Accord Organics in India are scaling ethyl acetate and related acetyls to cut import dependence and tap downstream profit pools.

Sustainability metrics now influence contract awards, particularly in Europe and Japan where customers must disclose scope-3 emissions. Producers able to certify ISCC Plus or mass-balance at scale gain early-mover advantage. Electro-fuel technology startups, supported by academic breakthroughs on high current-density acetate electrosynthesis, could upend the incumbent cost curve in the next decade if renewable power remains on a deflationary path.

Acetic Acid Industry Leaders

Celanese Corporation

INEOS

Eastman Chemical Company

LyondellBasell Industries Holdings B.V.

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regional import substitution and supply-chain localization form a clear opportunity, particularly where derivative demand is expanding faster than domestic acetyl capacity. India stands out as a structural gap, supported by the November 2024 MoU between INEOS Acetyls and GNFC to explore a 600 kt/y acetic acid plant at Bharuch. The proposed site is positioned around downstream needs in VAM-linked adhesives and broader acetyl derivatives, and it would also reduce exposure to freight disruption and duty risk.

Another whitespace is low-carbon and alternative-route acetic acid that aligns with customer carbon reporting and supports differentiated solvent and specialty demand. INEOS Acetyls' collaboration with Sandpiper Chemicals on a 1.1 MTPA low-carbon methanol plant in Texas City, with 300,000 t/y earmarked for INEOS acetic acid production, points to feedstock-side decarbonization as a commercial lever in North America. Kemvera completed a process design package for a 50,000 t/y bio-based acetic acid plant and commissioned a 20 t/y pilot reactor in January 2026, extending the pipeline for scalable non-fossil pathways. At the same time, large single-train additions in China, including Juzhengyuan (Jieyang) entering trial production for a 1.5 million t/y unit in late 2025/early 2026, increase the importance of export logistics, derivative integration (VAM/PTA), and reliability programs to manage utilization and pricing volatility as new capacity comes online.

Recent Industry Developments

- April 2026: INEOS Acetyls partnered with Sandpiper Chemicals to develop a 1.1 MTPA low-carbon methanol plant in Texas City, Texas, with 300,000 t/y earmarked for INEOS acetic acid production. The arrangement ties acetic acid economics more closely to lower-carbon feedstock availability and supports cost and compliance positioning for customers seeking reduced scope-3 intensity.

- May 2025: Kingboard Chemicals restarted its No. 2 acetic acid plant in Xingtai, improving upstream integration within its acetyl chain. The restart increased operating flexibility for downstream derivatives and reduced reliance on third-party supply during broader Chinese capacity shifts.

- June 2024: Celanese declared force majeure and implemented sales controls for acetic acid and vinyl acetate monomer (VAM) in the Western Hemisphere due to raw material supply disruptions and operational issues. The event tightened regional availability and highlighted the need for diversified sourcing and integrated feedstock strategies for downstream VAM and solvent consumers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers acetic acid sold for industrial and commercial use, counted as produced and consumed volumes across major producing and consuming regions, and then mapped to typical downstream derivative demand.

Scope exclusions: We exclude downstream derivative revenues and finished consumer products where acetic acid is only an input (for example, polymers, coatings, textiles, and packaged food items).

Segmentation Overview

- By Derivative

- Vinyl Acetate Monomer (VAM)

- Purified Terephthalic Acid (PTA)

- Ethyl Acetate

- Acetic Anhydride

- Other Derivatives

- By Production Route

- Methanol Carbonylation

- Acetaldehyde Oxidation

- Ethylene Oxidation

- Bio-based Fermentation

- By Application

- Adhesives, Paints and Coatings

- Plastics and Polymers

- Food and Beverage

- Textile

- Medical

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base around global chemical output, trade movement, and end-use demand signals that influence acetic acid consumption. We relied on public sources such as national statistics offices, UN Comtrade style customs statistics, the International Energy Agency for feedstock and energy direction, and peer-reviewed chemistry and process journals for route level cost and yield references.

To make the model practical, company annual reports, investor presentations, plant announcements, and reputable press were used to confirm capacity changes, operating status, and major debottlenecking timelines. Select paid subscriptions for company financials and intelligence, patent databases, and import or export shipment level views were referenced where they helped verify ownership, capacity rounding, and trade flows. The sources listed here are illustrative only, and many other references were also used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with producers, distributors, and large industrial buyers, followed by checks with process and procurement specialists who see price and availability shifts early. Because this is a global chemical commodity, we covered APAC, EMEA, and the Americas so assumptions on operating rates, trade balancing, and typical pricing terms could be cross checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 50% |

| Mid tier: 58% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 14% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

The market was built using a top-down and bottom-up approach, where production capacity by route, operating rates, and net trade are used to reconstruct apparent consumption by region, and then aligned to derivative level demand signals. To keep the totals realistic, selective bottom-up checks were run using sampled supplier volumes, typical contract and spot price bands, and customer side intake patterns, which are then used to adjust outliers.

Key inputs in the model included announced and operating nameplate capacity, utilization ranges by region, import and export balances, derivative demand indicators such as VAM and PTA activity, and feedstock direction (methanol and energy) that impacts run rates and pricing behavior. Where plant level data was incomplete, gaps were handled by using route level averages and regional utilization bands validated through interviews, and then pressure tested against trade movement and downstream demand trends.

For forecasting, scenario analysis was used so base case growth reflects expected capacity additions, typical operating rate normalization, and derivative demand outlook agreed by industry respondents. The scenarios were kept simple, with a conservative case around weaker run rates and a higher case around tighter supply and stronger derivative pull, before the final numbers were chosen.

Data Validation & Update Cycle

Model outputs were validated through triangulation across production, trade, and demand side signals, and then reviewed for unusual jumps in utilization, trade dependence, or implied consumption. When variances appeared, the assumptions were revisited, and respondents were re contacted if the change could not be explained through a known shutdown, commissioning, or policy shift.

A multi step review is followed before sign off so arithmetic, unit consistency, and regional rollups match the stated scope. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity changes or sustained price shocks. Before delivery, a fresh analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Acetic Acid Market Sizing Compared With Other Published Estimates

Published market sizes for acetic acid often look different because the studies do not always measure the same thing, even when the titles appear similar. The biggest drivers are the unit of measure (value versus volume), what is counted as in scope (acid only versus derivatives), and how pricing is assumed across regions and contract types.

The main gap comes from whether the estimate counts only acetic acid tonnage or also adds downstream derivative revenues, where Mordor Intelligence keeps the scope on acetic acid volumes (for example, 21.46 million tons in 2026) instead of mixing in VAM, PTA, or solvent market values that can inflate the total. Differences also show up when one publisher uses a single global average price, or a different base year and currency timing, which changes the USD conversion even if physical demand is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.46 M (2026) | |

| Trade Journal B | USD 18.33 B (2025) | Uses a value-based view and relies on assumed pricing progression across regions, which can shift totals materially versus a tonnage-first model, especially when contract and spot spreads widen. |

| Industry Publisher A | USD 13.20 B (2025) | Reports market value using its own application basket and base-year pricing, and the scope description does not clearly separate acetic acid from adjacent derivatives, which can lead to under or over counting depending on what is bundled. |

The comparison shows that part of the spread is explained by unit choice and what gets bundled into the definition, rather than a true disagreement on underlying demand. By keeping the steps traceable to capacity, utilization, trade balance, and derivative pull indicators, the final estimate stays easy to audit and repeat when new capacity or trade data becomes available.

Key Questions Answered in the Report

What is the projected volume of the acetic acid market by 2031?

It is forecast to reach 26.89 million tons by 2031, expanding at a 4.62% CAGR over 2026-2031.

Which derivative holds the largest share of global acetic acid demand?

Vinyl acetate monomer led with 27.30% of 2025 volume because of strong adhesive and packaging film consumption.

Why is Asia-Pacific so dominant in acetic acid consumption?

The region hosts rapid PTA and polyester capacity growth, integrated VAM chains, and China’s substantial new production units.

How are producers addressing catalyst-metal supply risk?

Strategies include ethylene-oxidation projects, CCU-methanol integration, and exploratory electro-fuel routes that eliminate rhodium or iridium.

Page last updated on: