Alkyl Polyglycoside Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

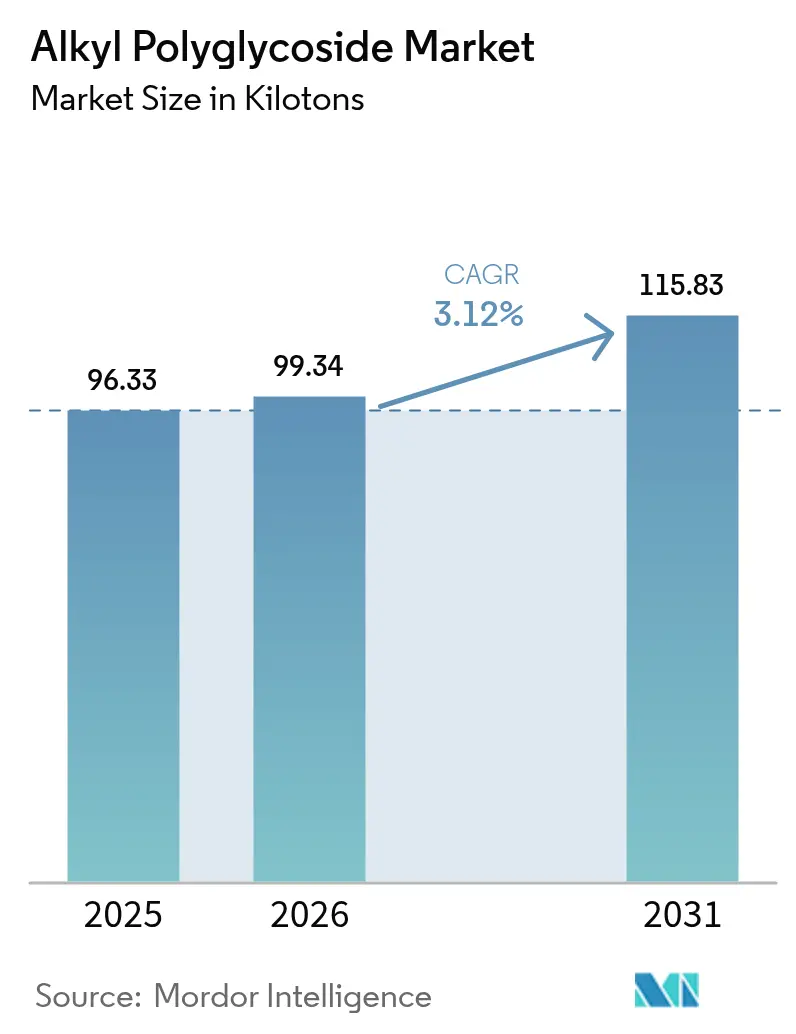

| Market Volume (2026) | 99.34 kilotons |

| Market Volume (2031) | 115.83 kilotons |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

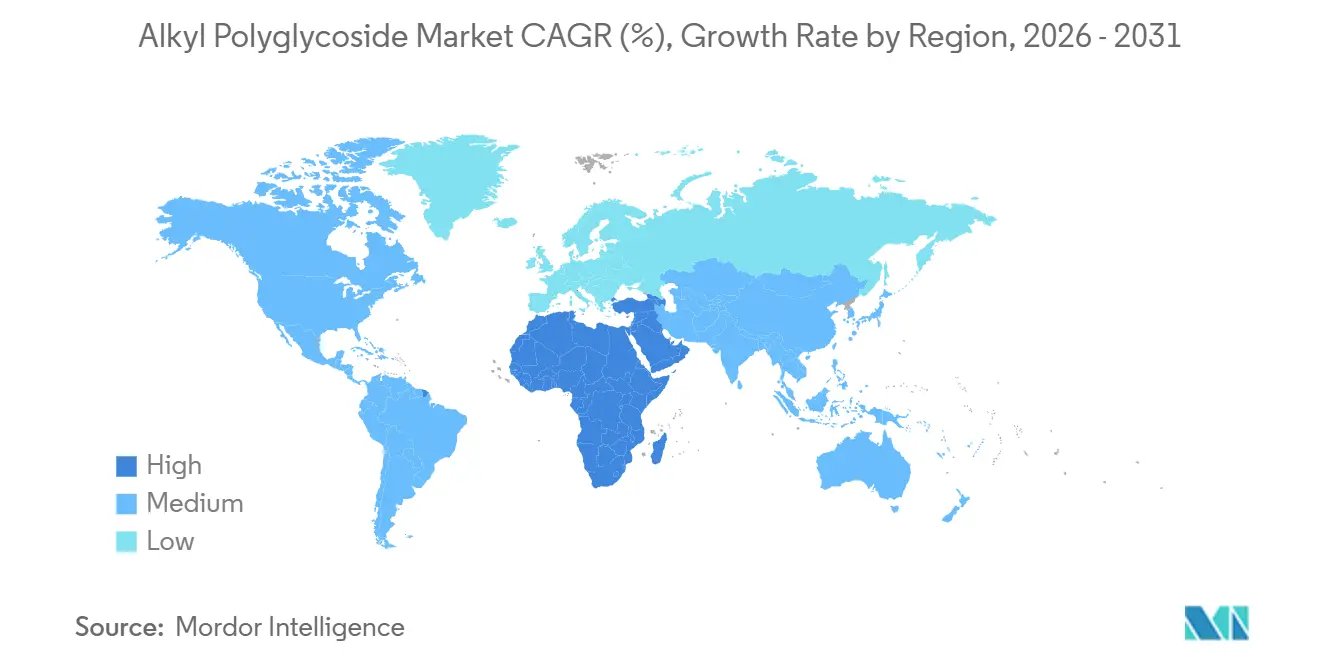

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alkyl Polyglycoside Market Analysis by Mordor Intelligence

The Alkyl Polyglycoside Market size is projected to be 96.33 kilotons in 2025, 99.34 kilotons in 2026, and reach 115.83 kilotons by 2031, growing at a CAGR of 3.12% from 2026 to 2031. Demand is buoyed by the rapid phase-out of nonylphenol ethoxylates, rising consumer preference for bio-based cleaning agents, and the willingness of multinational brands to pay premiums for ingredients that meet clean-label criteria. Surfactant producers are shifting investment toward glycoside platforms that balance performance, cost, and sustainability, while capacity expansions across Asia and Europe affirm confidence in long-run structural demand. Feedstock integration among fatty-alcohol suppliers is lowering unit costs in Southeast Asia, and process innovations such as enzymatic glycosylation are shrinking carbon footprints, enabling premium pricing in North America and Europe. Nonetheless, the Alkyl polyglycoside market confronts substitution threats from betaines and energy-intensive spray-drying costs that curb margins in regions with high natural-gas prices.

Key Report Takeaways

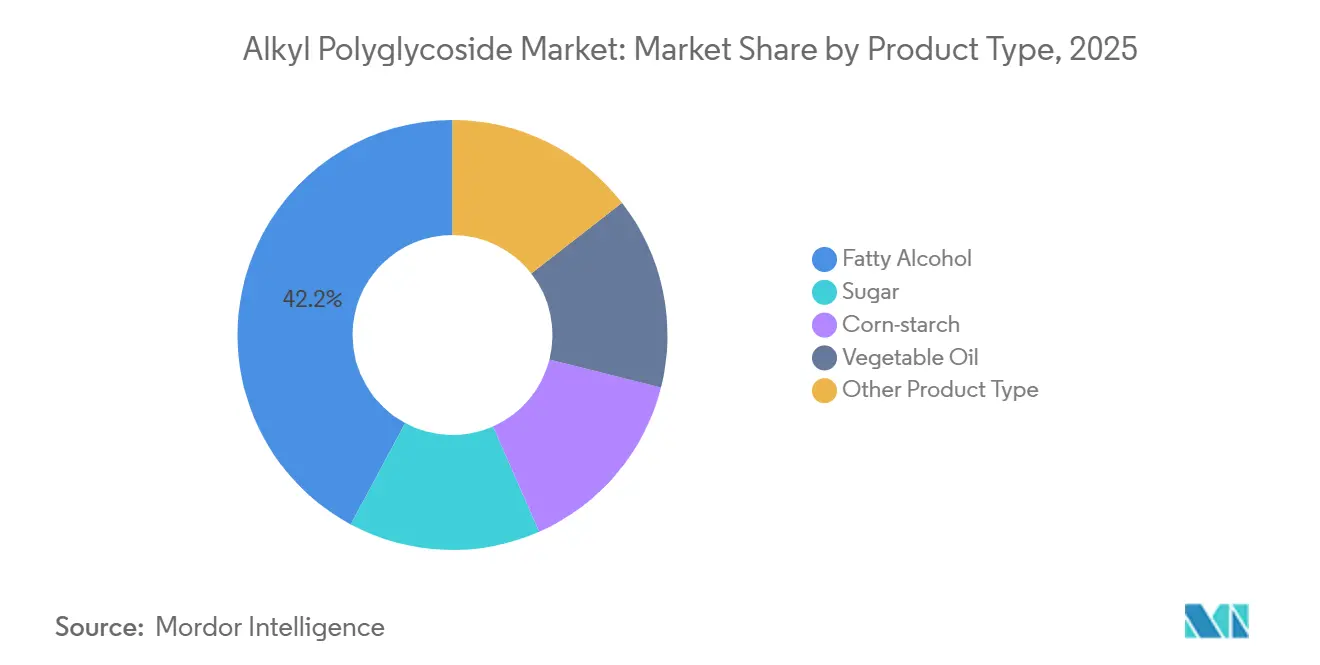

- By product category, fatty alcohol-based grades held 42.16% of the Alkyl Polyglucoside market share in 2025. The market share of vegetable oil is expected to grow at the fastest CAGR of 3.58% during the forecast period.

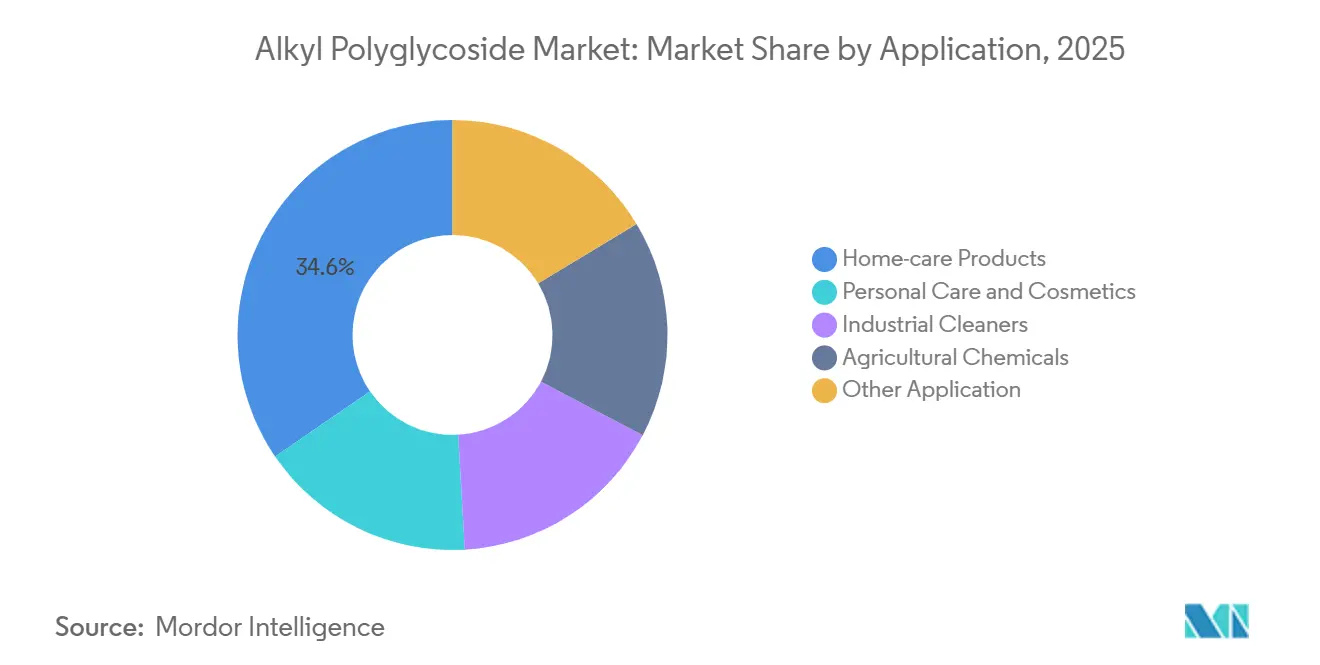

- By application, home-care products comprised the largest share of 34.55% of the market in 2025. Industrial cleaners are projected to grow at a 3.79% CAGR through 2031, outpacing all other applications.

- By geography, Asia-Pacific accounted for 45.96% of the 2025 volume, while the Middle East and Africa are poised for a 3.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alkyl Polyglycoside Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bio-based surfactants boom in home and personal-care | +0.9% | Global, with peak adoption in EU & North America | Medium term (2-4 years) |

| Regulatory phase-out of NPEs and other hazardous surfactants | +0.7% | EU core, spill-over to North America & APAC export-oriented manufacturers | Short term (≤ 2 years) |

| Capacity additions and backward integration among fatty-alcohol suppliers | +0.5% | APAC core (China, Malaysia, Indonesia), secondary in EU | Medium term (2-4 years) |

| APG penetration in industrial cleaning and oil-field fluids | +0.6% | Middle East & North America (oilfield), Global (industrial cleaners) | Long term (≥ 4 years) |

| Enzymatic and continuous-flow APG production cutting CO₂ footprint | +0.3% | EU & North America (sustainability-driven), early APAC adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bio-Based Surfactants Boom in Home and Personal-Care

Brand owners in Western Europe and North America report that 68% of households prioritized ingredient transparency over price in 2025, tipping reformulation economics decisively toward APG inclusion[1]NielsenIQ, “2025 Sustainable Home-Care Consumer Report,” nielseniq.com. Procter & Gamble increased APG to 12% of its fabric-care surfactant load, reducing exposure to future ethoxylate bans. Personal-care lines substitute C8-C10 APG for sulfates to curb irritation, while Unilever registered a 22% rise in APG procurement, reinforcing a demand floor that shelters the Alkyl polyglycoside market from swings in discretionary spending.

Regulatory Phase-Out Of NPEs And Other Hazardous Surfactants

An EU REACH amendment in 2024 capped NPEs at 0.01 % in consumer detergents, compelling an industry-wide switch to APG[2]European Chemicals Agency, “REACH Annex XVII Restriction on Nonylphenol Ethoxylates,” echa.europa.eu. Henkel attributed 18% of its European surfactant growth in 2025 to NPE-to-APG substitution and invested EUR 25 million in pilot trials. California’s Safer Consumer Products program echoed the restriction, nudging North American brands to harmonize formulations and magnifying extraterritorial demand.

Capacity Additions And Backward Integration Among Fatty-Alcohol Suppliers

Oleochemical producers in Southeast Asia are leveraging their captive palm-kernel and coconut-oil feedstocks to enter APG synthesis, a vertical-integration strategy that compresses the value chain and threatens merchant APG suppliers who lack upstream assets. Wilmar International’s 15,000 t plant in Johor delivers a 15-20 % landed-cost edge versus European peers, exemplifying Southeast Asia’s integrated model. KLK Oleo’s 12,000 t Selangor line targets Chinese converters, while BASF’s 8,000 t upgrade in Ludwigshafen leverages enzymatic routes to trade on carbon credentials rather than price.

APG Penetration In Industrial Cleaning And Oil-Field Fluids

Oilfield-service companies in the Permian Basin and the Middle East are specifying APG-based drilling muds and production chemicals to comply with offshore discharge regulations that prohibit persistent surfactants in produced water. Halliburton lifted APG’s share in drilling-fluid surfactants to 9% in 2025 on stricter offshore discharge rules. OECD 301B biodegradation rates above 90% mean operators meet OSPAR limits without costly water treatment. Ecolab’s institutional-cleaning launches used APG to cut customers’ wastewater-treatment costs by up to 20%, reinforcing industrial pull-through.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from other mild surfactants (betaines, amine-oxides) | -0.40% | Global, with peak intensity in North America & EU personal-care formulations, moderate impact in APAC | Medium term (2-4 years) |

| High-energy demand for powder-grade APG spray-drying | -0.30% | EU & North America (high energy costs), limited impact in APAC and Middle East | Short term (≤ 2 years) |

| Licensing barriers from processive-glycosyltransferase patents | -0.20% | Global, with highest impact on mid-tier producers in APAC lacking capital for licensing fees, limited impact on integrated EU & North America players | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition From Other Mild Surfactants

Betaines and amine oxides are capturing share in premium personal-care formulations where formulators prioritize foam stability and sensory attributes over biodegradability alone. Cocamidopropyl betaine, in particular, offers superior foam density and skin-feel in sulfate-free shampoos, and it costs 10-15% less than C8-C10 APG on an active-matter basis, creating a persistent pricing headwind for APG suppliers. Evonik’s betaine volumes rose 8% year-over-year in 2025, outpacing APG growth in mid-tier brands that prize cost control. The Alkyl polyglycoside market thus leans increasingly on premium labels where biodegradability and carbon metrics can command higher prices.

High-Energy Demand For Powder-Grade APG Spray-Drying

Spray-drying APG solutions to 50-70% active-matter powders consumes 1,200-1,500 kWh per metric ton, a significant energy burden that erodes margins when natural-gas and electricity prices spike. European producers faced acute pressure in 2024 when natural-gas prices averaged EUR 45 per megawatt-hour, up from EUR 30 in 2023, prompting some converters to shift production toward liquid APG concentrates that bypass the drying step. Clariant cut powder output 12% in 2025, slicing energy needs by 60% per kilogram of active matter. In Asia-Pacific, lower energy tariffs sustain powder preference, but any LNG price shock or carbon levy could narrow that cost gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Feedstock Diversity Drives Margin Defense

Fatty-alcohol APG dominated at 42.16% volume in 2025, giving this grade the largest Alkyl polyglycoside market share among product types. Vegetable-oil-derived variants, buoyed by palm-kernel and coconut integration, are projected to grow at a 3.58% CAGR and outpace the broader Alkyl polyglycoside market size through 2031. The shift mitigates palm-oil sustainability risk and lowers Scope 3 emissions, helping suppliers secure multi-year contracts with European detergent groups. Corn-starch and sugar routes appeal to North American formulators seeking domestic or non-GMO inputs, yet elevated corn prices in 2025 squeezed margins and reduced competitiveness against imported fatty alcohols. Enzymatic processes show strong compatibility with vegetable-oil substrates, avoiding color-body formation and shortening purification cycles.

Downstream, premium personal-care brands in Japan and South Korea favor low-carbon, vegetable-oil APG even at an 8-12% cost premium, while commodity home-care lines in Indonesia still rely on fatty-alcohol grades for price discipline. Sugar-based APG remains niche, reserved for certified-organic lines in Europe, where cost pass-through is viable. Synthetic-alcohol APG objects remain confined to agrochemical adjuvants where long regulatory approval cycles discourage feedstock changes, reinforcing a hybrid product landscape that cushions suppliers from single-feedstock shocks.

By Application: Industrial Cleaners Outpace Traditional Home-Care

Home-care detergents led demand with 34.55% of total volume in 2025, yet their growth slightly trails the broader Alkyl polyglycoside market as private-label price pressure lingers. Industrial cleaners headline the fastest trajectory at 3.79% CAGR, reflecting regulatory curbs on discharge toxicity and a total-cost-of-ownership calculus that favors APG despite higher per-kilogram prices. Oilfield uptake is material; North Sea operators saved USD 1.2 million per well by avoiding water reinjection after switching to APG-based muds, underscoring financial incentives.

Personal-care volumes advance steadily but face competition from betaines that match foam aesthetics at lower cost. Nevertheless, sulfate-free shampoos in Western markets continue to specify APG for its mildness, insulating some volume. Agricultural-chemical formulators employ APG to enhance leaf wetting and satisfy EU residue limits on exported crops, a niche yet sticky demand stream. Emerging uses in textile auxiliaries and leather tanning point to further diversification that could buffer future cyclical shocks.

Geography Analysis

Asia-Pacific retained 45.96% of global tonnage in 2025, the largest regional slice of the Alkyl polyglycoside market. Integrated oleochemical complexes in China’s Jiangsu and Guangdong provinces stream fatty alcohol directly into APG kettles, minimizing logistics costs. India’s detergent heartland in Gujarat and Tamil Nadu underpins local demand as per-capita soap consumption climbs. Draft Chinese guidelines to curtail NPEs in 2026 could spark an internal switch, intensifying domestic APG pull and reinforcing the region’s supply-demand balance. Southeast Asia is cementing its role as the low-cost export hub after Wilmar and KLK Oleo added 27,000 t of integrated capacity, while Japan and South Korea act as innovation nodes that reward enzymatically produced, hypoallergenic grades.

North America and Europe contribute smaller volumes but higher unit margins to the Alkyl polyglycoside market size. EU REACH limits and the US Safer Choice scheme encourage APG adoption, and carbon pricing lets European producers levy premiums on low-CO₂ grades. Still, energy-intensive powder production faces profitability headwinds; Henkel sourced 68% of its 2025 APG in liquid form to reduce energy exposure. North American oilfields offer a stable demand stream that anchors baseline growth even when retail detergent volumes plateau.

In the Middle East and Africa, Gulf oilfield-service providers mandated biodegradable surfactants in offshore fluids, directly lifting APG offtake. Sub-Saharan detergent start-ups promote clean rivers messaging to urban consumers, accelerating substitution in powder laundry products. Brazil and Argentina remain important for agrochemical adjuvants linked to EU export standards, while cost sensitivity tempers wider consumer adoption across Latin America.

Competitive Landscape

The Alkyl Polyglycoside market is moderately consolidated. Wilmar International and KLK Oleo together added 27,000 t of capacity during 2024-2025, leveraging captive palm-kernel and coconut-oil feedstocks to compete on landed cost. Chinese converters are also scaling to meet domestic detergent demand, creating a supply base that limits the pricing power of long-established Western producers. The competitive balance is likely to tighten as new capacity exceeds demand growth in the short term, prompting price competition and potential consolidation among merchant producers that lack either upstream integration or patented technology.

Alkyl Polyglycoside Industry Leaders

Dow

Clariant AG

BASF

Kao Corporation

Shanghai Fine Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BASF unveiled a new plant for Alkyl Polyglucosides (APGs) at its Bangpakong site in Thailand. This expansion aims to bolster BASF's foothold in the burgeoning Asian market, enabling the company to respond more swiftly and flexibly to its customers' needs.

- June 2025: Shanghai Auway Daily Chemicals CO., Ltd., a subsidiary of Hunan Resun Auway Industrial Co., Ltd., officially launched its production line for APG (Alkyl Glycoside). This initiative is designed to meet the growing demand for eco-friendly surfactants.

Global Alkyl Polyglycoside Market Report Scope

Alkyl Polyglycoside, often referred to as APG, Sparteine, or Triton, is a sugar-based surfactant known for its biodegradability and non-toxicity. It is sourced from plant starch and fatty alcohols, with primary origins in coconuts, corn, and palm oil. This versatile ingredient finds its way into various products, ranging from personal care items like shampoos and body washes to household cleaners, including laundry detergents and bathroom cleaning solutions.

The alkyl polyglycoside market is segmented by product, application, and geography. By product, the market is segmented into fatty alcohol, sugar, cornstarch, vegetable oil, and other products. By application, the market is segmented into personal care and cosmetics, home care products, industrial cleaners, agricultural chemicals, and other applications. The report also covers the market sizes and forecasts for the global alkyl polyglycoside market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Fatty Alcohol |

| Sugar |

| Corn-starch |

| Vegetable Oil |

| Other Product Type |

| Personal Care and Cosmetics |

| Home-care Products |

| Industrial Cleaners |

| Agricultural Chemicals |

| Other Application |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Fatty Alcohol | |

| Sugar | ||

| Corn-starch | ||

| Vegetable Oil | ||

| Other Product Type | ||

| By Application | Personal Care and Cosmetics | |

| Home-care Products | ||

| Industrial Cleaners | ||

| Agricultural Chemicals | ||

| Other Application | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What volume is the Alkyl polyglycoside market projected to reach by 2031?

It is forecast to reach 115.83 kilotons by 2031, reflecting a 3.12% CAGR from 2026.

Which end-use segment is growing fastest?

Industrial cleaners lead growth at a 3.79% CAGR, driven by oil-field and food-processing demand.

Why are integrated Southeast Asian producers gaining share?

Proximity to palm-kernel and coconut-oil feedstocks gives suppliers such as Wilmar and KLK Oleo a 15-20% landed-cost edge over European rivals.

How are manufacturers reducing APG’s carbon footprint?

Enzymatic glycosylation and continuous-flow reactors trim CO₂ emissions per kilogram by up to 30%, enabling premium pricing.

Which competing surfactants pose the biggest threat to APG in personal-care formulations?

Taines and amine oxides offer similar mildness and foam density at a lower active-matter cost, pressuring APG uptake in mass-market lines.

Page last updated on: