Sulfuric Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

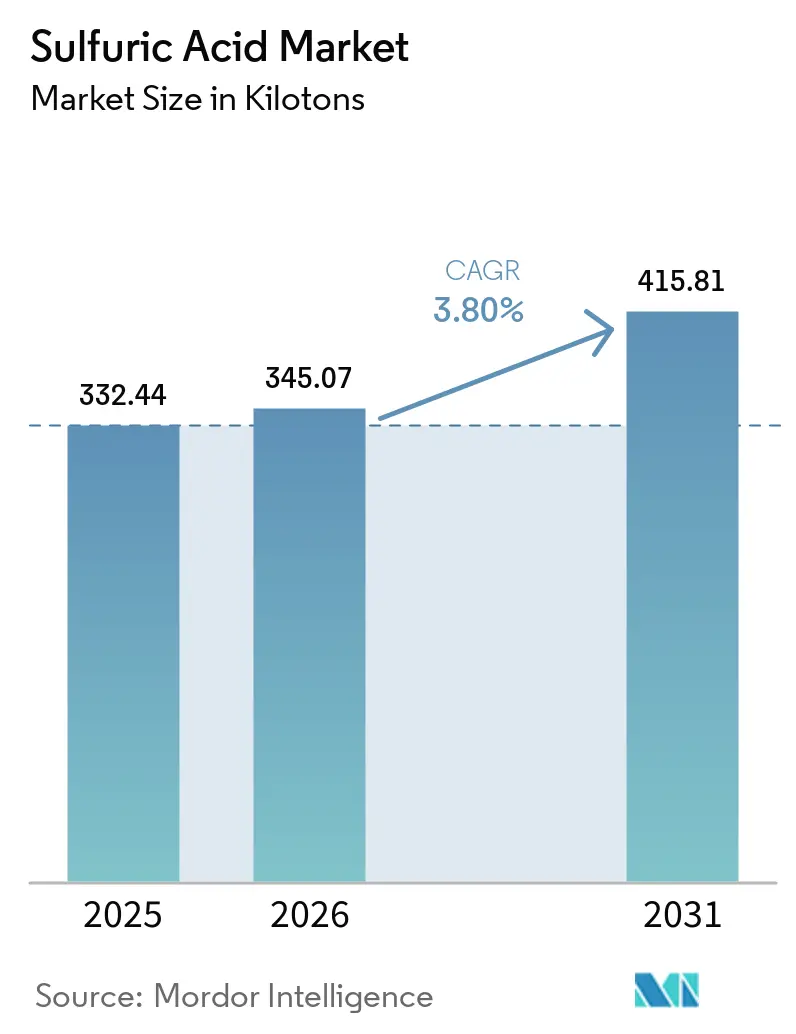

| Market Volume (2026) | 345.07 kilotons |

| Market Volume (2031) | 415.81 kilotons |

| Growth Rate (2026 - 2031) | 3.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

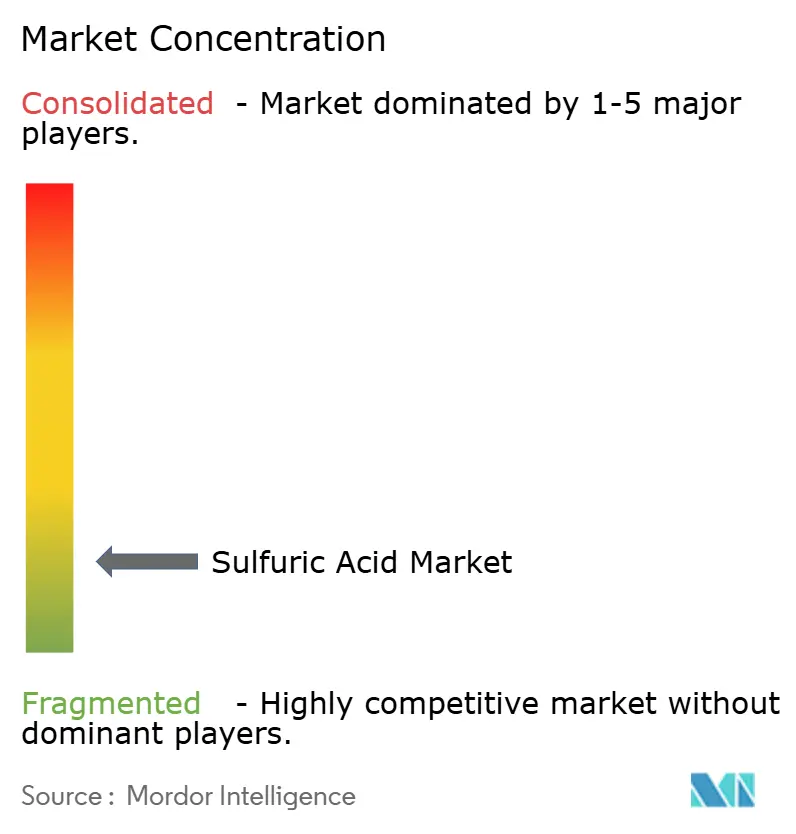

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sulfuric Acid Market Analysis by Mordor Intelligence

Sulfuric Acid market size in 2026 is estimated at 345.07 kilotons, growing from 2025 value of 332.44 kilotons with 2031 projections showing 415.81 kilotons, growing at 3.80% CAGR over 2026-2031. Robust demand from phosphate fertilizer producers, particularly across China, India, and Morocco, anchors this trajectory as governments prioritize food security and crop-yield resilience. Vertical integration in non-ferrous smelting and petroleum refining yields incremental captive supply, narrowing the historical divide between raw-material owners and downstream acid consumers. New battery-grade electrolyte requirements and tightening ultra-low-sulfur fuel regulations are diversifying the customer base and reshaping regional trade flows. Freight-rate volatility and rising ESG-driven compliance outlays compel margins, prompting operators to accelerate process-control upgrades and digital performance tools that curb energy intensity and tail-gas emissions.

Key Report Takeaways

- By raw material, elemental sulfur held 78.40% of the sulfuric acid market share in 2025; the pathway grows at 3.79% CAGR through 2031.

- By production process, the DCDA route captured 89.30% of the sulfuric acid market in 2025, and it is forecast to expand at a 3.86% CAGR to 2031.

- By concentration, standard-grade acid (93-98 wt%) accounted for 97.80% of the sulfuric acid market size in 2025, whereas oleum/fuming acid registers the fastest 3.72% CAGR.

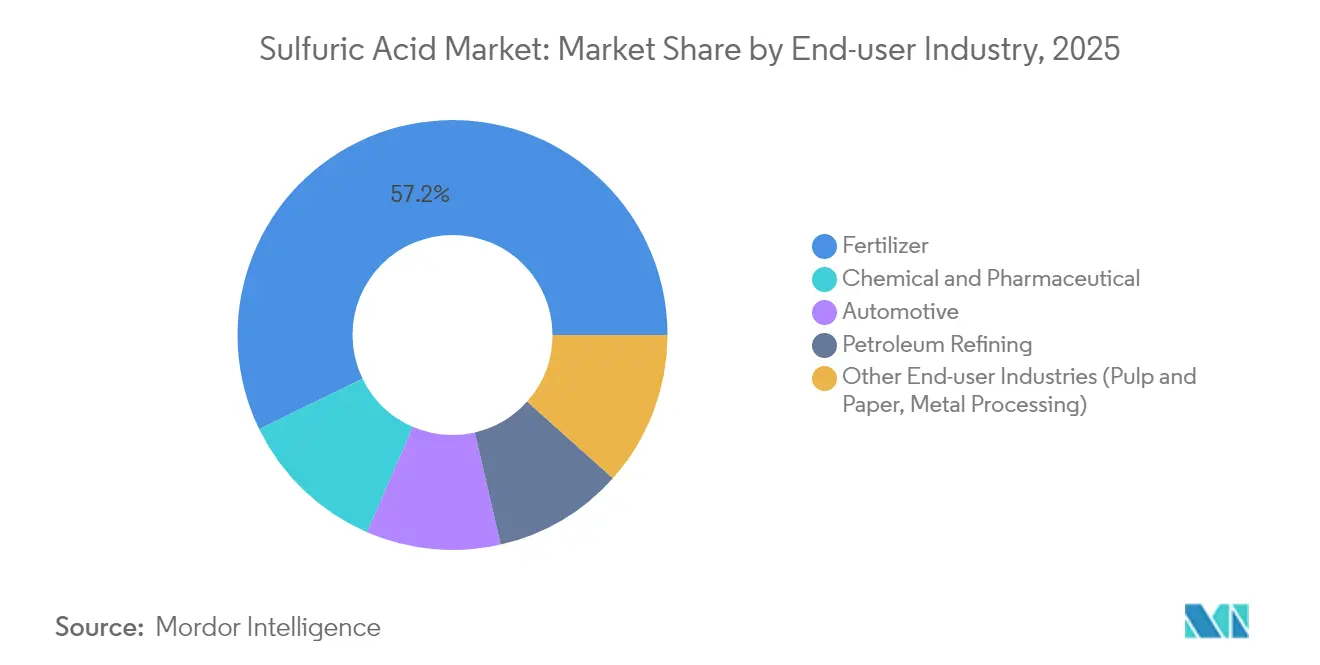

- By end-user industry, fertilizers commanded 57.20% revenue share in 2025; chemical and pharmaceutical applications are projected to advance at 4.32% CAGR, the highest among all segments.

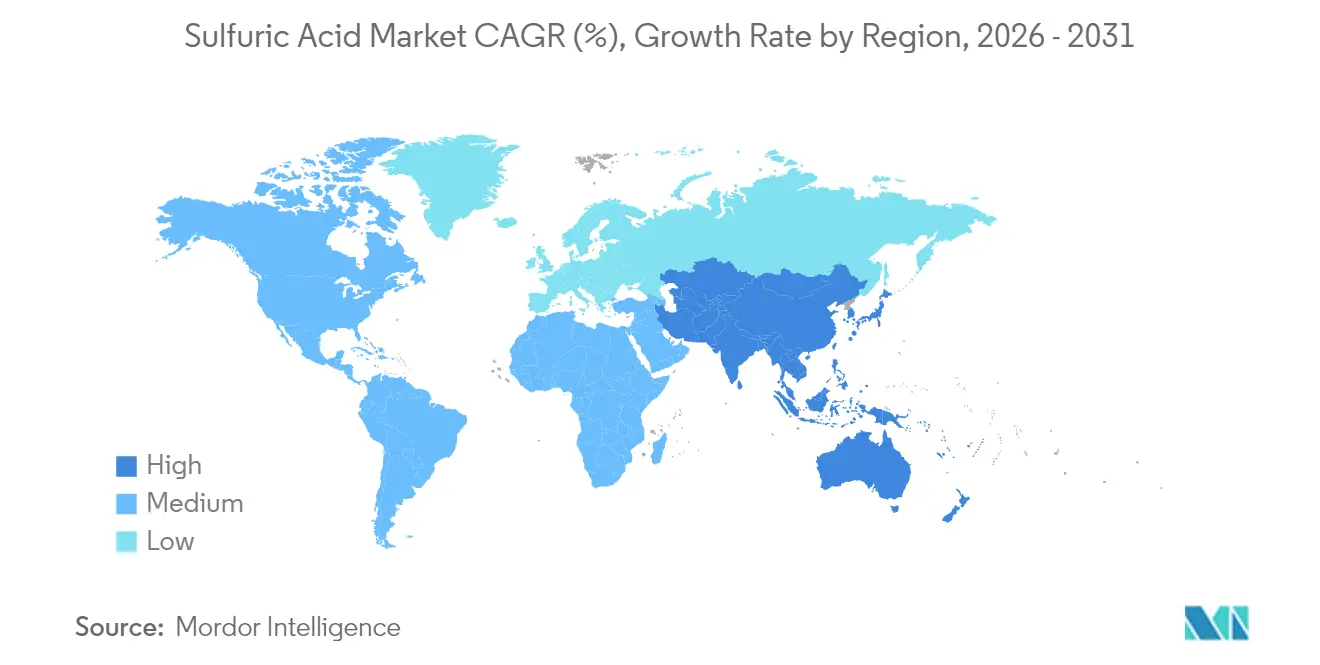

- By geography, Asia Pacific dominated with a 51.20% share of the sulfuric acid market in 2025, while also achieving the fastest 4.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sulfuric Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phosphate-fertilizer capacity expansions | +1.2% | Asia Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Tightening ultra-low-sulfur fuel specs | +0.6% | North America and Europe | Short term (≤ 2 years) |

| Battery-grade electrolyte demand from EVs | +0.7% | Asia Pacific, North America, Europe | Long term (≥ 4 years) |

| Copper and zinc smelter build-outs | +0.5% | South America | Medium term (2-4 years) |

| Rising consumption in chemicals and pharma | +0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Phosphate-Fertilizer Capacity Expansions in Asia and Africa

Morocco’s sulfur-burning projects, scheduled for commissioning in 2025, will raise local acid availability and bolster downstream phosphate output. In India, policy-backed import pacts with Mauritania ensure rock-phosphate feedstock security, supporting new phosphoric-acid reactors that intensify sulfuric acid drawdown. The U.S. Geological Survey expects global phosphate capacity to reach 69.1 million tons by 2027, with Brazil, Kazakhstan, Mexico, Morocco, and Russia expanding simultaneously[1]U.S. Geological Survey, “Mineral Commodity Summaries 2024,” usgs.gov . These additions cluster fresh demand around Atlantic and Indian Ocean shipping lanes, prompting traders to reposition spot cargoes and sign longer-tenor off-take contracts. Supply chains are shifting from historic Middle East–to–Asia routes toward intra-regional flows centered on North Africa and South Asia supporting the sulphuric acid market while compressing netback margins for independent blenders and distributors.

Tightening Ultra-Low-Sulfur Fuel Specifications Boosting Sulfur Recovery

North American and European fuel regulations that mandate sulfur contents below 10 ppm are compelling refiners to maximize Claus-unit recovery and convert larger volumes of recovered sulfur into captive acid streams[2]UK Health Security Agency, “Sulphuric Acid: General Information,” gov.uk . Integrated energy companies are retrofitting tail-gas treating units to achieve more than 99.7% SO₂ conversion, an upgrade that directly enlarges domestic supply pools for fertilizer complexes. These investments, while capital intensive, offset emission-penalty liabilities and allow refiners to monetize what was once a disposal cost center within the sulphuric acid market.

Battery-Grade Electrolyte Demand from EVs

The electrification wave is transforming the sulfuric acid market as high-purity electrolyte becomes indispensable for lithium, lead, and emerging zinc-ion batteries. Hard-rock spodumene conversion requires large quantities of sulfuric acid to generate lithium sulfate, an intermediate en route to battery-grade lithium chemicals. European gigafactory roadmaps envisage capacity growing from 190 GWh in 2024 toward 1,500 GWh by 2030. Such expansions demand stringent purity specifications that only vertically integrated or specialty acid producers currently meet, stimulating new investments in filtration, polishing, and dedicated storage infrastructure.

Copper and Zinc Smelter Build-Outs in Latin America

Operators such as Teck Resources and Codelco are installing contact-acid plants sized to process this off-gas, adding regional capacity that alters traditional import needs for fertilizer producers in Brazil and Peru. These acid streams lower logistics costs for agricultural hubs along the Pacific coast, boosting competitively priced supply for nitrate-phosphate-potash blenders in the sulphuric acid market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sulfur supply volatility from refinery rationalisation | -0.5% | Europe and North America | Short term (≤ 2 years) |

| Rising ESG-driven capex for tail-gas scrubbing | -0.8% | Europe and North America | Medium term (2-4 years) |

| Freight-rate spikes on key trade routes | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sulfur Supply Volatility Linked to Refinery Rationalisation

As mature-market refineries shutter capacity or shift toward bio-feedstocks, elemental-sulfur output fluctuates unpredictably. Operators in Western Europe report multi-month gaps in recovered sulfur availability, compelling fertilizer complexes to secure imports at elevated prices. Sulfuric acid market participants hedge this exposure by adopting flexible feedstock strategies, including Pyrite roasting or acid regeneration, although these options carry higher energy footprints and regulatory scrutiny.

Rising ESG-Driven Capital Expenditure for Tail-Gas Scrubbing

Regulators are tightening SO₂ emission thresholds, especially within the European Union and North American jurisdictions. Compliance requires wet-gas scrubbers, dry-absorption towers, and advanced heat-recovery systems that lift project capital intensity by 10-15%. Elessent Clean Technologies now markets a digital advisor that monitors catalyst activity and predicts stack-emission drift, yet deployment seldom occurs without costly hardware retrofits. Smaller standalone plants risk margin erosion and may defer refurbishments, risking production curtailments that ripple through the sulfuric acid market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material Type: Elemental Sulfur Maintains Predominance

Elemental sulfur contributed 78.40% of the 2025 output within the sulfuric acid market size and underpinned an anticipated 3.79% CAGR to 2031. Recovery from natural-gas processing and clean-fuel refining secures cost advantages that Pyrite roasting struggles to match. Volatile sulfur benchmarks, documented by Intratec Alerts, occasionally narrow this gap, but integration synergies still favor elemental pathways.

Refinery hydrogen-sulfide streams deliver predictable feedstock purity that simplifies catalyst control in DCDA converters, helping operators meet sub-250 ppm acid-mist targets. When crude slates swing toward higher sourness, the sulfuric acid industry calibrates output upswings, balancing fertilizer demand spikes. Conversely, refinery rationalisation in Europe removes supply, prompting traders to redirect Persian Gulf tonnage toward Antwerp and Hamburg terminals.

By Production Process: DCDA Technology Leads Environmental Compliance

The DCDA route accounted for 89.30% of global output in 2025 and is poised to outpace headline sulfuric acid market growth with a 3.86% CAGR. Replacement cycles favor vanadium-pentoxide catalysts with proprietary cesium promoters that deliver fast ignition and extended life.

Emerging plants in Indonesia and Saudi Arabia are specifying fully automated inter-pass temperature controls to minimize SO₃ slip, while retrofits in Poland exploit heat-recovery steam generators that trim net energy use by up to 25 MJ per tonne.

By Concentration: Standard Grade Delivers Versatility

Standard-grade acid (93-98 wt%) dominated 2025 demand, driving 97.80% of shipments. Its concentration offers an optimal trade-off between reactivity and safe handling, supporting applications from ore leaching to pigment production across the sulphuric acid market.

Oleum and other high-strength formulations advance at 3.72% CAGR, energised by semiconductor wet-etching and niche organic syntheses that mandate low water content. Specialty producers in Japan and Belgium install dedicated throughput lines featuring alloy-20 piping and chilled storage to maintain fuming acid stability. These investments create a modest but premium-priced sub-segment within the sulphuric acid market that cushions profit volatility.

By End-User Industry: Fertilizers Anchor Consumption

Fertilizer producers absorbed 57.20% of global volumes in 2025 of the sulfuric acid market size, driven by phosphate rock digestion to yield phosphoric acid. Expansion plans by OCP Group and Ma’aden keep utilization high, even during commodity downturns, because crop-nutrient demand correlates more with planted acreage than GDP.

Chemical and pharmaceutical facilities, though representing a smaller share, grow faster at 4.32% CAGR. They leverage sulfuric acid as a dehydrating agent, nitration catalyst, and pH regulator. The sulfuric acid industry increasingly tailors ultra-low-metal grades that meet ISO 9001-validated quality systems for drug intermediates. Automotive lead-acid batteries and petroleum refining together retain steady baseline demand but face long-run substitution threats from lithium-ion powertrains and green hydrogen, respectively.

Geography Analysis

Asia Pacific commanded 51.20% of global consumption in 2025, and is projected to widen its lead at a 4.03% CAGR to 2031. China’s phosphate-fertilizer complexes in Yunnan and Hubei continue brownfield debottlenecking, while India’s new phosphoric-acid reactors align with government subsidy schemes that reward local production. Battery-material parks in Zhejiang and Sichuan are contracting high-purity supply under multi-year offtakes, anchoring additional merchant-acid import needs within the sulphuric acid market ecosystem.

North America’s refinery-linked recovery network supplies a mature customer base, and the US Sulfuric Acid Market continues to benefit from this established supply chain, while capacity rationalisation in the U.S. Atlantic seaboard trims surplus. Europe maintains stringent environmental compliance, driving widespread DCDA retrofits and secondary scrubber installations across the sulphuric acid market. Fertilizer-grade demand grows modestly as land-application caps tighten, yet high-purity acid consumption rises within specialty chemical corridors in Germany and the Netherlands.

South America, led by Chile, Peru, and Brazil, records the strongest incremental supply growth outside Asia. Autogenous copper smelters generate captive acid that displaces seaborne cargoes from the U.S. Gulf. Agricultural hubs in Brazil’s Cerrado prefer regional supply due to shorter lead times and reduced freight premiums, stabilizing delivered prices in the sulphuric acid market during shipping upsets.

Competitive Landscape

The sulfuric acid market exhibits a highly fragmented structure. Vertical integration is the prevailing strategy, allowing smelters and refiners to monetize SO₂ off-gas while stabilizing their own reagent costs. Strategic alliances continue to reshape capacities and regional influence. Digital transformation differentiates operational performance. These capabilities are becoming prerequisites for environmental permit renewals and insurance premiums, raising the entry bar for smaller independents.

Sulfuric Acid Industry Leaders

Mosaic

Boliden Group

Aurubis AG

Jiangxi Copper Corporation

PhosAgro Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sumitomo Corporation formed a joint venture with NFC Public Company Limited to operate a sulfuric acid tank-terminal network in Thailand, establishing a regional logistics hub.

- July 2024: OCP Group awarded Worley Chemetics the contract for three new sulfuric acid plants at the Mzinda Phosphate Hub in Morocco, covering proprietary technology and detailed engineering services.

Global Sulfuric Acid Market Report Scope

Sulfuric acid, denoted by the chemical formula H2SO4, is a potent and corrosive mineral acid. It is colorless, lacks an odor, and exhibits a thick liquid texture. This acid is recognized for its robust reactivity with numerous substances. Its widespread application extends to various industrial processes, showcasing its significance in diverse chemical reactions and manufacturing procedures. The vigorous nature of sulfuric acid reactions underscores its role as a crucial component in numerous industrial sectors.

The sulfuric acid market is segmented by raw material type, end-user industry, and geography. By raw material type, the market is segmented into elemental sulfur, pyrite ore, and other raw material types (metal sulfides, sulfur dioxide). By end-user industry, the market is segmented into fertilizer, chemical and pharmaceutical, automotive, petroleum refining, and other end-user industries (pulp and paper, metal processing). The report also covers the market size and forecasts for the sulfuric acid market in 27 countries across major regions.

For each segment, the market sizing and forecasts have been done based on volume (tons).

| Elemental Sulfur |

| Pyrite Ore |

| Other Raw Material Types |

| Single Contact Process |

| Double Contact Double Absorption (DCDA) |

| Standard (93-98 wt%) |

| Oleum/Fuming Acid |

| Fertilizer |

| Chemical and Pharmaceutical |

| Automotive |

| Petroleum Refining |

| Other End-user Industries (Pulp and Paper, Metal Processing) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Raw Material Type | Elemental Sulfur | |

| Pyrite Ore | ||

| Other Raw Material Types | ||

| By Production Process | Single Contact Process | |

| Double Contact Double Absorption (DCDA) | ||

| By Concentration | Standard (93-98 wt%) | |

| Oleum/Fuming Acid | ||

| By End-user Industry | Fertilizer | |

| Chemical and Pharmaceutical | ||

| Automotive | ||

| Petroleum Refining | ||

| Other End-user Industries (Pulp and Paper, Metal Processing) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What drives the current growth of the global sulfuric acid market?

The strongest momentum stems from expanding phosphate fertilizer capacity in Asia and Africa, complemented by rising requirements in battery materials and non-ferrous smelting.

Why is DCDA technology dominant in sulfuric acid production?

DCDA offers superior sulfur-dioxide conversion efficiency, enabling operators to meet stringent emissions limits while generating higher acid yields per unit of sulfur feed.

How does refinery rationalization affect sulfuric acid supply?

Refinery closures reduce elemental sulfur generation, sometimes creating regional feedstock shortages that elevate sulfuric acid prices, especially during peak agricultural demand.

What role does sulfuric acid play in battery manufacturing?

High-purity sulfuric acid is essential for electrolyte preparation and for mineral processing steps such as converting spodumene concentrate into lithium sulfate.

Which region is expected to record the fastest sulfuric acid demand growth?

Asia Pacific is projected to grow at around 4.03% CAGR through 2031, driven by fertilizer expansion, battery manufacturing, and broad industrialization.

What is the current size of the sulfuric acid market?

The sulfuric acid market size is estimated at 345.07 kilotons in 2026, and is expected to reach 415.81 kilotons by 2031, at a CAGR of 3.80% during the forecast period.

Page last updated on: