Purified Terephthalic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

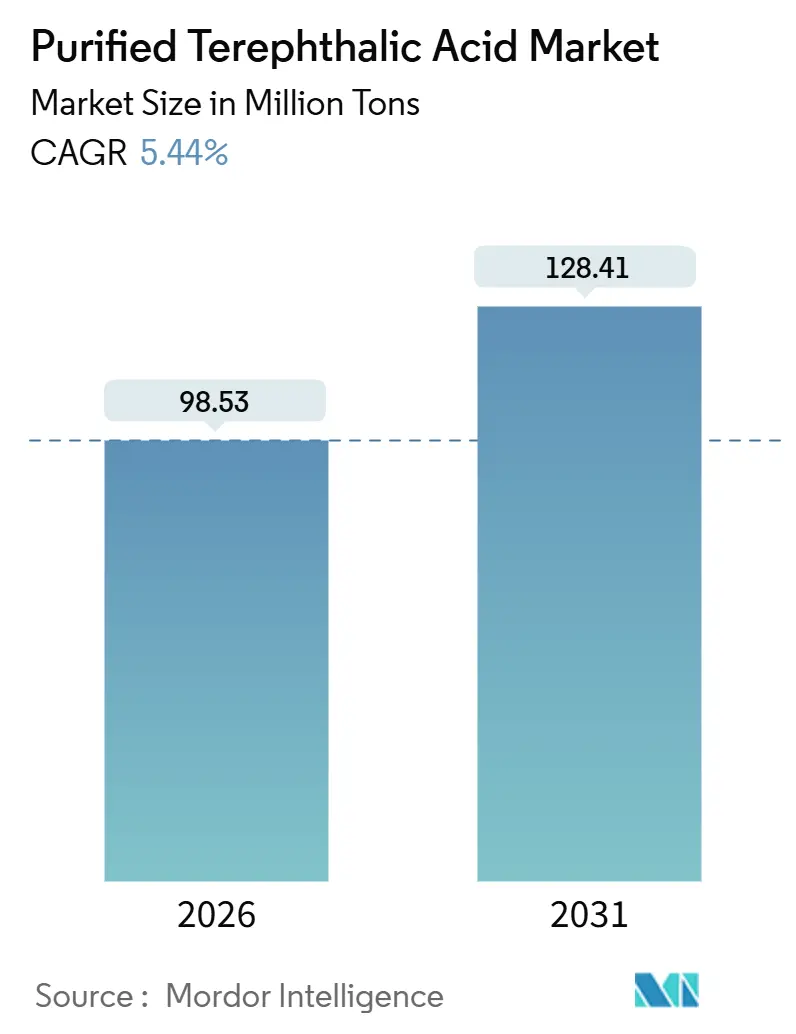

| Market Volume (2026) | 98.53 Million tons |

| Market Volume (2031) | 128.41 Million tons |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

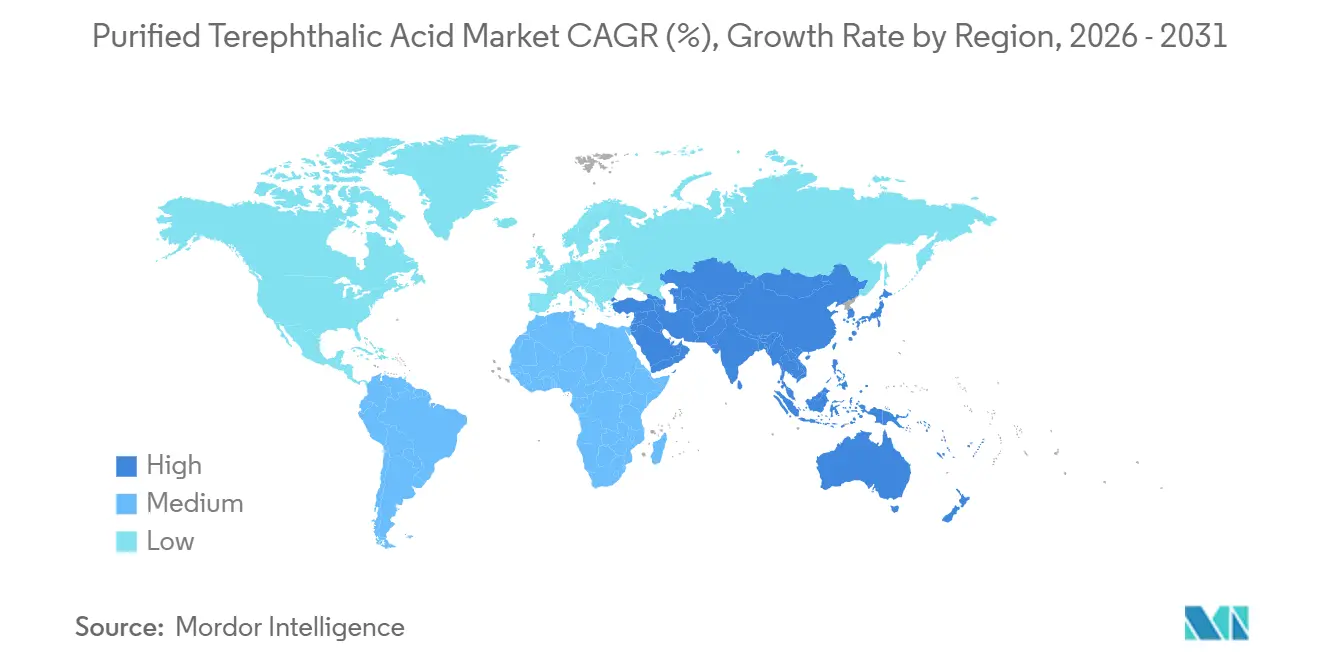

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

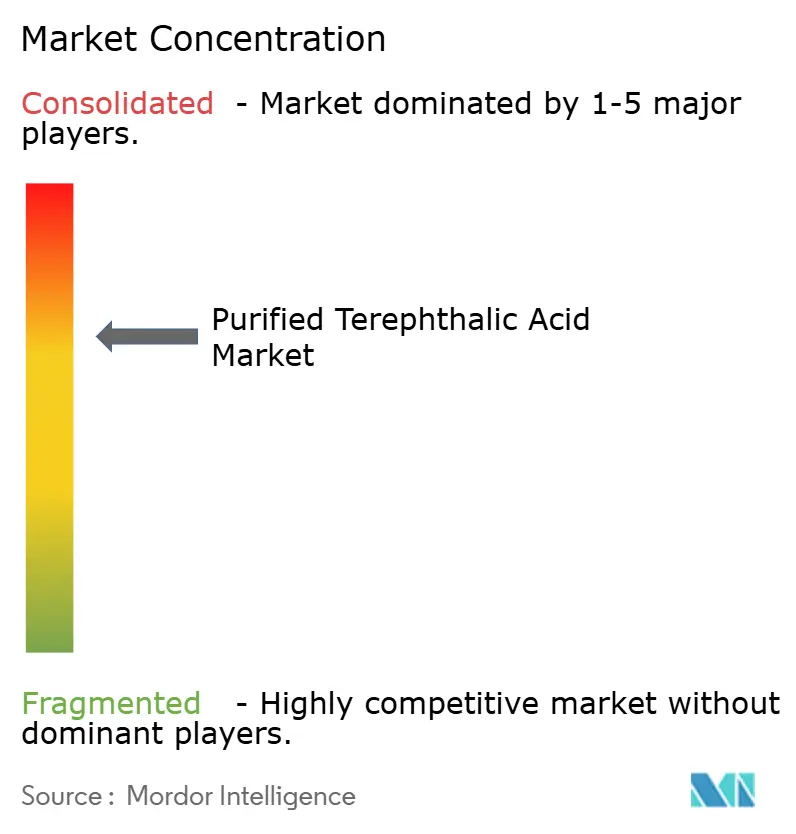

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Purified Terephthalic Acid Market Analysis by Mordor Intelligence

The Purified Terephthalic Acid Market size is estimated at 98.53 Million tons in 2026, and is expected to reach 128.41 Million tons by 2031, at a CAGR of 5.44% during the forecast period (2026-2031). This expansion stems from structural shifts in downstream polymer demand rather than transient packaging cycles, as integrated Asian producers scale PTA assets to serve both polyester-fiber and PET resins for export beverage packaging. Rising e-commerce, recycled-content mandates, and lightweighting initiatives in automotive interiors elevate long-term visibility for the purified terephthalic acid market, while sustained paraxylene availability and continued technology upgrades underpin cost competitiveness. Competitive intensity is moderate: five vertically integrated suppliers control close to half of installed capacity, yet second-tier participants remain fragmented and vulnerable to margin swings tied to crude-oil volatility. Parallel momentum in chemical recycling and bio-based PTA, although nascent, introduces differentiation opportunities as brand owners internalize carbon-footprint targets.

Key Report Takeaways

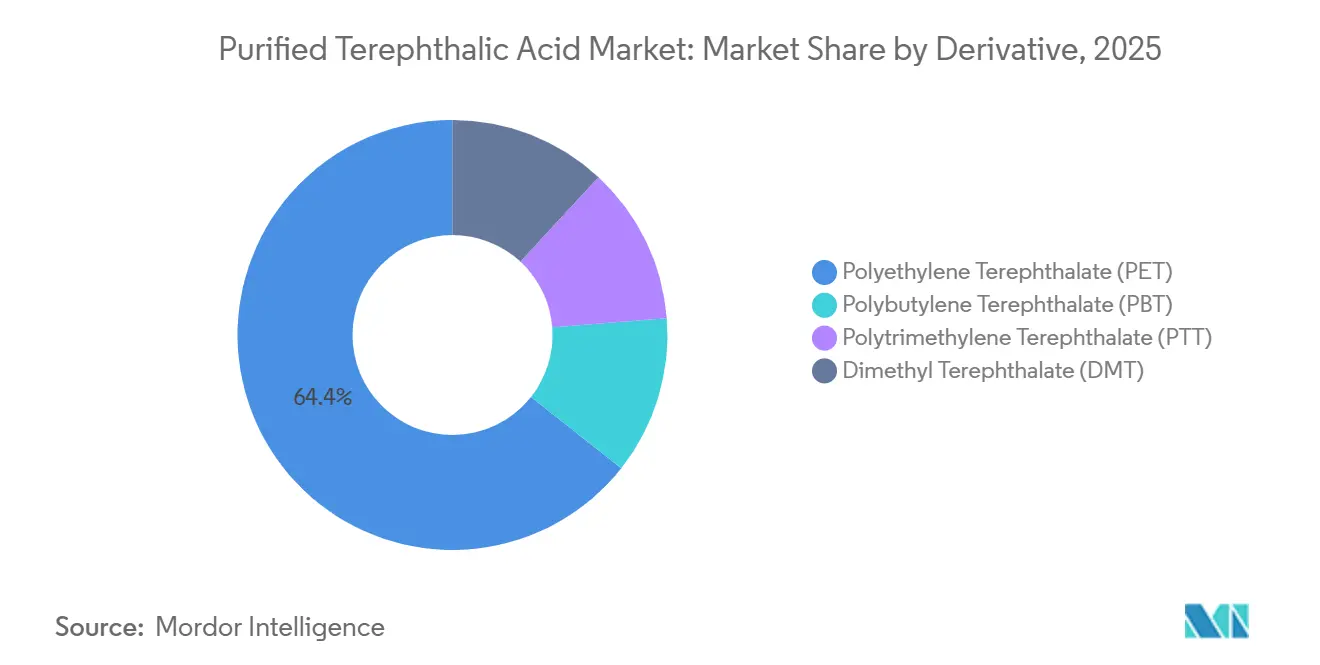

- By derivative, polyethylene terephthalate (PET) commanded 64.35% of the purified terephthalic acid market share in 2025; the segment is forecast to advance at a 6.51% CAGR to 2031.

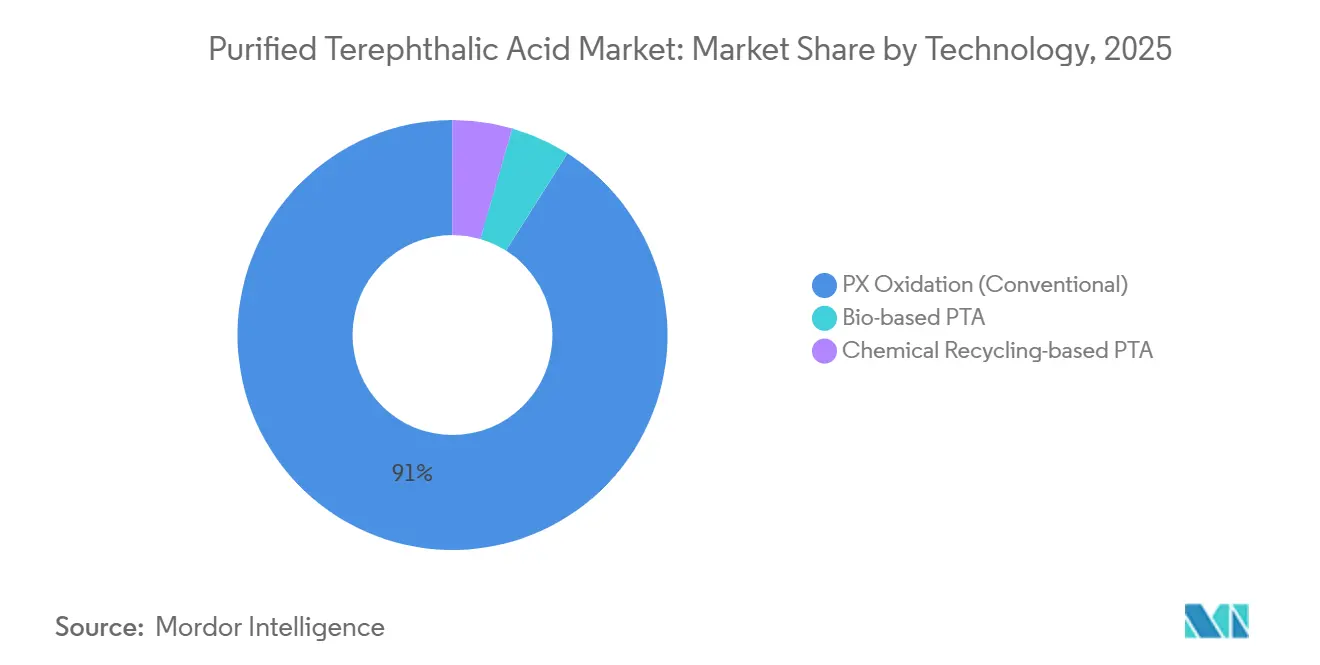

- By technology, PX oxidation (conventional) retained 91.03% revenue share in 2025; bio-based PTA is forecast to post the highest 6.87% CAGR through 2031.

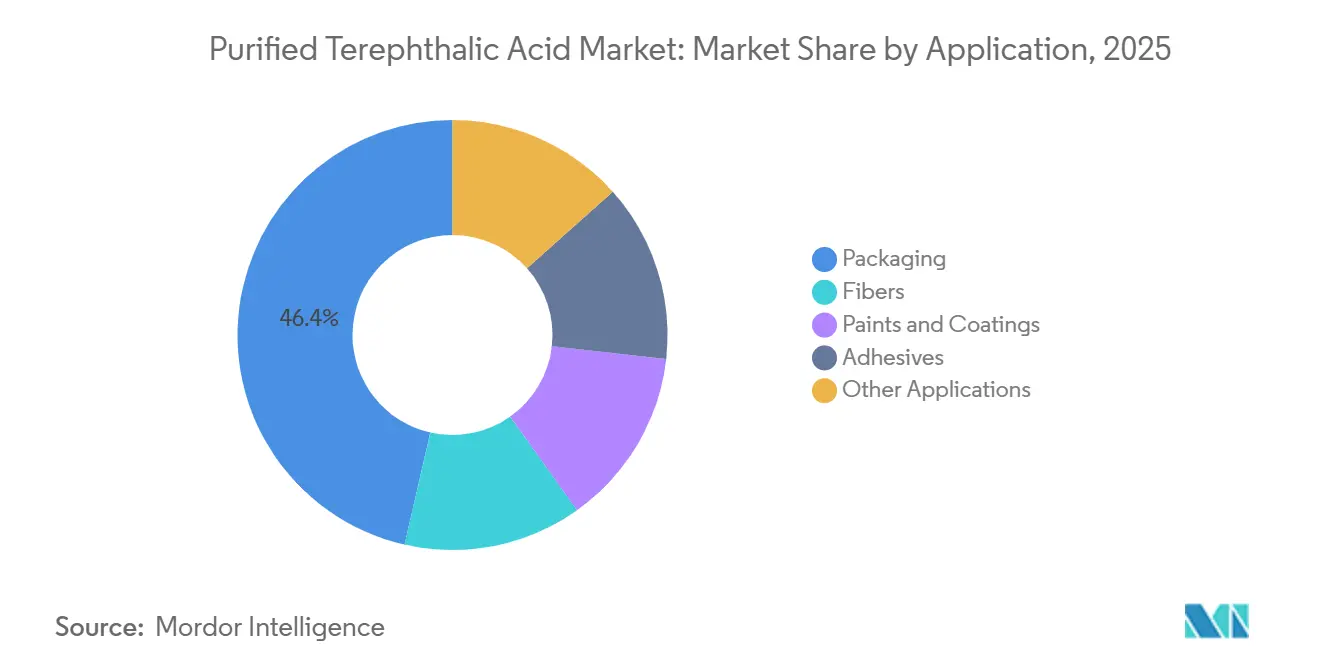

- By application, packaging captured 46.41% of purified terephthalic acid market size in 2025 and is set to grow at 6.22% CAGR through 2031.

- By geography, Asia-Pacific controlled 53.75% of 2025 volume and will outpace all regions with a 7.12% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Purified Terephthalic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong PET-Packaging Demand from E-Commerce | +1.2% | Global, with concentration in North America, Europe, and APAC urban corridors | Medium term (2-4 years) |

| Polyester-Fibre Capacity Additions in Asia | +1.5% | APAC core (China, India, Vietnam, Bangladesh), spill-over to Middle-East | Long term (≥ 4 years) |

| Automakers' Shift to Lightweight PET Composites | +0.6% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Recycled-PET (rPET) Closed-Loop Mandates | +1.0% | Europe (EU27), North America (California, New York), select APAC markets (Japan, South Korea) | Short term (≤ 2 years) |

| Battery-Separator-Grade PTA Uptake | +0.4% | APAC (China, South Korea, Japan), North America (EV manufacturing hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong PET-Packaging Demand from E-Commerce

The steady rise of online grocery and meal-kit delivery boosts demand for lightweight, shatter-resistant PET containers that withstand complex fulfillment chains. Brazil recycled 410,000 tons of PET in 2024 yet still operated at 23% idleness, underscoring feedstock shortages even as a new decree forces a 32% recovery rate in 2026 and 50% by 2040. Brand owners must fund roughly USD 2 billion a year for collection and recycling capacity, while virgin PTA producers weigh backward-integration strategies to secure rPET supply.

Polyester-Fiber Capacity Additions in Asia

Chinese and Indian producers brought 4.2 million tons of new polyester-fiber capacity online between 2024 and 2025. Reliance Industries alone generated 2.59 million tons of PTA during FY 2024-25 to feed its captive yarn lines. Overcapacity suppresses Zhengzhou PTA futures but favors large integrated firms that wield paraxylene advantages and withstand price troughs better than merchant players.

Automakers’ Shift to Lightweight PET Composites

Automotive OEMs employ PET-based composites in interior panels to trim vehicle weight by up to 12%. Eastman Chemical reports a 20% cost savings versus carbon fiber and a 40% weight reduction versus steel, helping global manufacturers meet U.S. CAFE and forthcoming Euro 7 emission limits. PTA suppliers must meet higher IV and purity thresholds, spurring capex upgrades worth USD 50-70 per ton.

Recycled-PET Closed-Loop Mandates

EU Regulation 2022/1616 enforces 30% recycled content in PET bottles by 2030. California’s AB 793 scales to 50% by 2030, driving offtake premiums of USD 100-150 per ton over virgin resin[1]European Commission, “Single-use plastics directive and recycled content targets,” europa.eu . Chemical depolymerization technologies deployed by Eastman and Loop Industries unlock hard-to-recycle feedstock streams that mechanical recycling cannot service, bifurcating demand between virgin and circular PTA grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicological Concerns Around PTA Dust Exposure | -0.3% | Global, with acute pressure in North America and Europe due to stricter OSHA/ECHA enforcement | Short term (≤ 2 years) |

| Paraxylene and Crude-Oil Price Volatility | -0.8% | Global, with highest impact in import-dependent regions (Europe, Southeast Asia) | Medium term (2-4 years) |

| Bio-Based PEF and Other Polymer Substitutions | -0.5% | Europe, North America (early-adopter markets for sustainable packaging) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicological Concerns Around PTA Dust Exposure

OSHA maintains a 5 mg/m³ TWA for terephthalic acid dust, compelling retrofit investments of USD 10-15 million for older 500,000-ton units[2]OSHA, “Terephthalic acid dust permissible exposure limits,” osha.gov. INEOS shuttered a Belgian plant in 2023 over compliance costs, and Mitsubishi Chemical divested Indonesian assets, illustrating tightening regulatory economics for sub-scale producers.

Paraxylene and Crude-Oil Price Volatility

Paraxylene represents 60-65% of PTA cash cost. A USD 20 per-barrel fluctuation in Brent translates into 8-12% PTA netback swings, squeezing non-integrated suppliers that sell under fixed contracts. Integrated projects such as Lotte Chemical’s USD 3.9 billion Indonesia complex illustrate the stabilizing effect of scale and vertical integration on netbacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: PET Dominance Anchors Volume Growth

Polyethylene Terephthalate (PET) absorbed 64.35% of purified terephthalic acid market share in 2025 and is forecast to grow at 6.51% CAGR through 2031, reinforcing its central role in packaging and textiles. PBT retains a lower market share, serving high-temperature automotive connectors, while PTT remains niche in carpets and specialty textiles. DMT’s role has dwindled as direct esterification prevails, yet Koch Technology Solutions’ PolyVolve process renews interest by integrating recycled streams and cutting energy consumption 9%.

The derivative mix tilts further toward PET over the outlook as e-commerce orders and rPET mandates accumulate. However, achieving recycled-content goals hinges on sufficient post-consumer supply, a variable that could temper PET’s growth advantage. Producers increasingly deploy continuous-polymerization lines compatible with depolymerized monomers, enhancing circularity credentials for the purified terephthalic acid market.

By Technology: Conventional PX Oxidation Retains Scale Advantage

PX oxidation (conventional) captured 91.03% of 2025 output due to established catalyst systems and cost structures near USD 600-700 per ton in integrated settings. INVISTA’s P8 design, licensed widely across Asia, trims capital intensity by 15% through thermosyphon reactors and nitrogen spargers. Bio-based PTA enjoys a 6.87% CAGR but lacks feedstock economics; facilities below 10,000 tons remain demonstrative, awaiting cheaper bio-paraxylene pathways. Methanolysis and glycolysis plants led by Eastman and Loop reach commercialization by 2027, yet capital costs of USD 1,500-2,000 per installed ton limit diffusion outside regions with robust recycled-content laws.

Integrated majors such as Hengli Petrochemical already run single-site complexes exceeding 16 million tons, leveraging scale and captive paraxylene to fend off entrants. The technology mix shift thus favors incremental retrofits rather than wholesale replacement, sustaining conventional oxidation’s volume lead within the purified terephthalic acid market.

By Application: Packaging Leads, Fibers Follow

Packaging accounted for 46.41% of 2025 demand and will grow at 6.22% CAGR through 2031, supported by single-serve beverages in Asia and Latin America plus rising rPET content targets. Fiber use grows at a slower pace amid Chinese overcapacity, but consolidated integrated players still backfill volumes for fast-fashion and home-textile exports.

Coatings and adhesives progress at mid-single-digit rates, with PTA enabling higher crosslink density in alkyd resins for marine and industrial applications. Advanced niches such as battery separator films require ultrapure PTA grades, commanding 30-40% margin premiums. Although these volumes are modest, they deepen PTA’s role in emerging energy value chains, broadening the purified terephthalic acid market beyond traditional segments.

Geography Analysis

Asia-Pacific held 53.75% of 2025 consumption and is tracking a 7.12% CAGR, the purified terephthalic acid market’s fastest regional pace. New PTA lines in China’s Jiujiang and India’s Maharashtra add more than 8 million tons by 2027, underpinning vertically integrated polyester chains. India’s Reliance plans an additional 3 million-ton module at Dahej by 2027, while Adani-Indorama’s USD 3 billion JV fast-tracks a 3.2 million-ton plant using port proximity to slash freight costs.

In North America, Alpek’s 1.2 million-ton Mexican unit supplies U.S. converters, yet Chinese imports cap pricing. Eastman’s depolymerization plant in France will export recycled PTA to North American brand owners, offering premium feedstock for closed-loop bottles.

Europe lags growth as high energy prices restrain new builds. INEOS’s 2023 closure highlights compliance burden under REACH, driving investment into chemical recycling rather than virgin capacity. South America contributes 6% led by Brazil, which must quadruple selective collection by 2040 to meet new decrees, generating opportunities for recycling ventures. Middle-East and Africa collectively command lower share; SABIC channels capital into Chinese downstream assets rather than local PTA, focusing on capturing value in end-use growth hubs.

Competitive Landscape

The five largest players (Reliance Industries, Indorama Ventures, Yisheng Pet Resin, Hengli Petrochemical, and FCFC) command about 47% of installed capacity, imparting moderate concentration. Strategy revolves around end-to-end integration, from paraxylene through PTA into polyester resins or fibers, insulating margins from crude swings. Reliance’s INR 75,000 crore expansion will raise Indian PTA capacity to nearly 10 million tons within five years and deepen its export reach across Southeast Asia.

Indorama pursues regional diversification with joint ventures and depolymerization projects in Europe and North America, positioning itself for recycled-content premiums. Sinopec and Hengli leverage coastal mega-complexes exceeding 16 million tons that exploit scale economies and favorable logistics for both domestic and bonded exports. BP retains sizable European capacity but weighs technology licensing and partnerships to hedge against high continental energy costs.

Technology licensors such as INVISTA and Koch Technology Solutions emerge as competitive enablers, reducing capital intensity and energy demand. Meanwhile, Middle Eastern producers mull downstream equity stakes; Saudi Aramco’s interest in Hengli typifies efforts to lock in paraxylene outlets. Closures of marginal players in Belgium and Indonesia affirm a trend toward scale and compliance capability, reinforcing the competitive moat of integrated majors within the purified terephthalic acid market.

Purified Terephthalic Acid Industry Leaders

HENGLI PETROCHEMICAL ( DALIAN ) CHEMICAL CO., LTD.

Reliance Industries Limited

Indorama Ventures Public Company Limited

Yisheng Pet Resin

FCFC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Circular Plastics Company (CPC), a Singapore-based plastics recycler, commenced operations at its new PET bottle recycling facility in Vietnam. Situated in the Chau Duc Industrial Park in Ba Ria, a coastal city in Southeast Vietnam, the plant had an initial annual production capacity of 30,000 tonnes of flakes and 14,000 tonnes of food-grade rPET flakes.

- March 2025: The Food Safety and Standards Authority of India (FSSAI) approved the use of food-grade recycled polyethylene terephthalate (rPET) for food and beverage contact applications. Recycling methods such as Super-Clean Recycling, Melt-in Recycling, Paste-in Recycling, and Enhanced Chemical Recycling were recognized as capable of producing food-grade rPET.

Global Purified Terephthalic Acid Market Report Scope

Terephthalic Acid, chemically known as Benzene-1,4-dicarboxylic acid, is a condensation polymer and an essential industrial aromatic precursor for polyethylene terephthalate (PET). These other petrochemical derivatives find usage in diverse industries such as packaging, textile, etc. Crude terephthalic acid obtained from the oxidation reaction of p-xylene contains impurities such as 4-carboxy benzaldehyde and several colored polyaromatics. Hence, terephthalic acid is first subjected to purification before exploiting it as an intermediate in the petrochemical industry.

The purified terephthalic acid market is segmented by derivative, technology, application, and geography. By derivative, the market is segmented into polyethylene terephthalate (PET), polybutylene terephthalate (PBT), polytrimethylene terephthalate (PTT), and dimethyl terephthalate (DMT). By technology, the market is segmented into PX oxidation (conventional), bio-based PTA, and chemical recycling-based PTA. By application, the market is segmented into packaging, fibers, paints and coatings, adhesives, and other applications (engineering plastics, pharmaceuticals and intermediates, etc.). The report also covers the market size and forecasts for the purified terephthalic acid in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Polyethylene Terephthalate (PET) |

| Polybutylene Terephthalate (PBT) |

| Polytrimethylene Terephthalate (PTT) |

| Dimethyl Terephthalate (DMT) |

| PX Oxidation (Conventional) |

| Bio-based PTA |

| Chemical Recycling-based PTA |

| Packaging |

| Fibers |

| Paints and Coatings |

| Adhesives |

| Other Applications (Engineering Plastics, Pharmaceuticals and Intermediates, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Derivative | Polyethylene Terephthalate (PET) | |

| Polybutylene Terephthalate (PBT) | ||

| Polytrimethylene Terephthalate (PTT) | ||

| Dimethyl Terephthalate (DMT) | ||

| By Technology | PX Oxidation (Conventional) | |

| Bio-based PTA | ||

| Chemical Recycling-based PTA | ||

| By Application | Packaging | |

| Fibers | ||

| Paints and Coatings | ||

| Adhesives | ||

| Other Applications (Engineering Plastics, Pharmaceuticals and Intermediates, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global purified terephthalic acid market?

The purified terephthalic acid market size reached 98.53 million tons in 2026 and is forecast at 128.41 million tons by 2031.

Which derivative segment grows fastest through 2031?

Polyethylene terephthalate records a 6.51% CAGR, the highest among derivatives.

Why is Asia-Pacific expanding PTA capacity rapidly?

China, India, and ASEAN producers build multi-million-ton plants to feed polyester fibers and export PET bottles, lifting regional CAGR to 7.12%.

What risk does paraxylene volatility pose?

A USD 20 per-barrel crude swing alters PTA production costs by 8-12%, squeezing non-integrated suppliers.

Page last updated on: