Inkjet Printhead Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 4.06 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

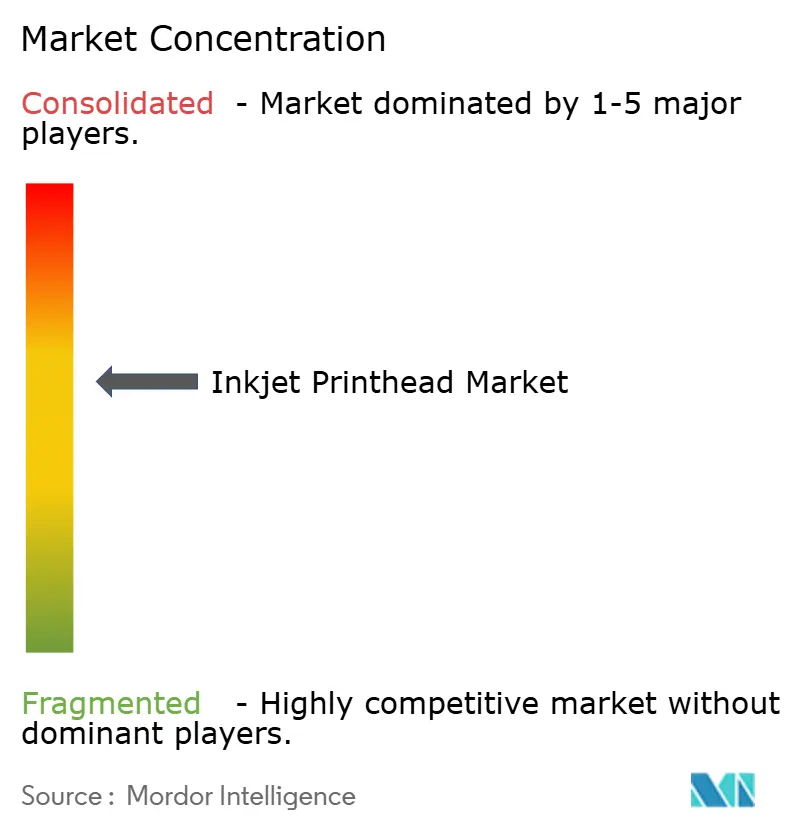

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inkjet Printhead Market Analysis by Mordor Intelligence

The inkjet printhead market size is expected to increase from USD 3.18 billion in 2025 to USD 3.32 billion in 2026 and reach USD 4.06 billion by 2031, growing at a CAGR of 4.11% over 2026-2031. A decisive shift toward industrial printing is redefining value creation as packaging, textile, and electronics plants demand single-pass precision heads that sustain web speeds above 300 meters per minute. Component miniaturization, rising adoption of water-based and UV-curable chemistries, and open-platform licensing by leading original-equipment manufacturers (OEMs) are expanding addressable volume but also compressing margins. Press integrators are now differentiating on software, color management, and predictive maintenance, while advances in piezoelectric MEMS stacks enable sub-2-picoliter drops at 50 kHz firing.

Key Report Takeaways

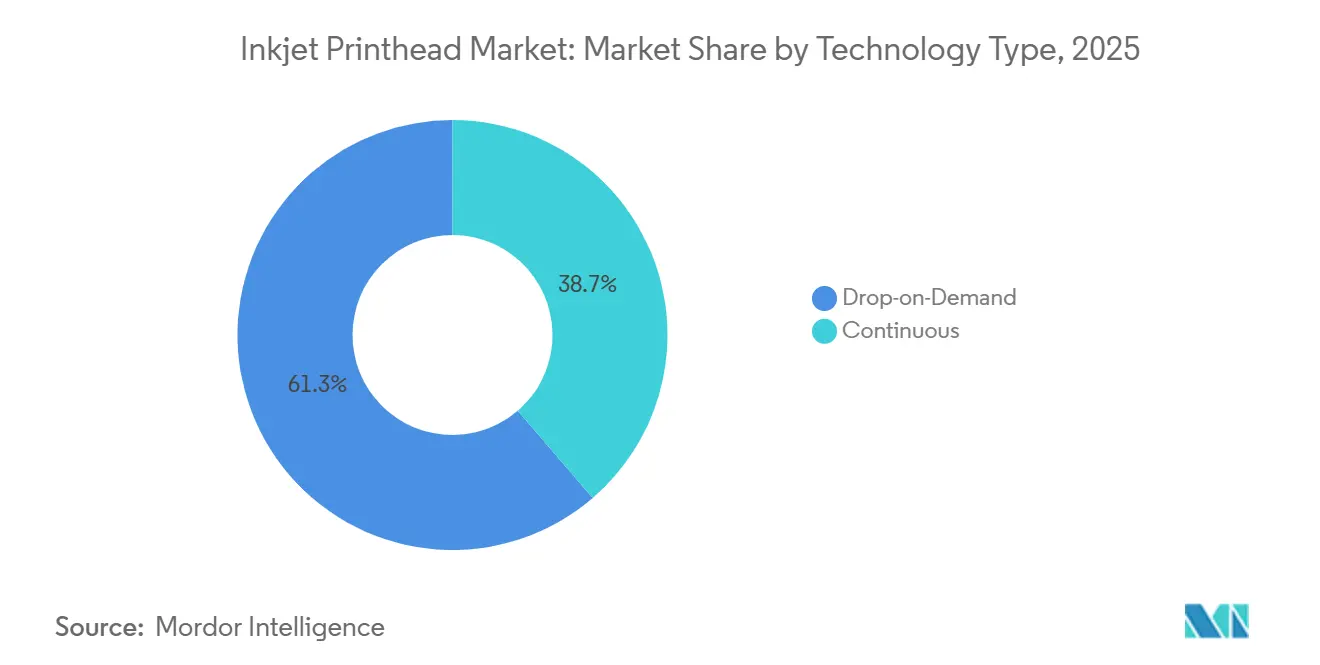

- By technology, drop-on-demand architectures led the inkjet printhead market with 61.3% market share in 2025, expanding at a 4.51% CAGR through 2031.

- .By ink chemistry, aqueous formulations captured 37.82% of the inkjet printhead market size in 2025, while UV-curable variants are projected to expand at a 5.09% CAGR through 2031.

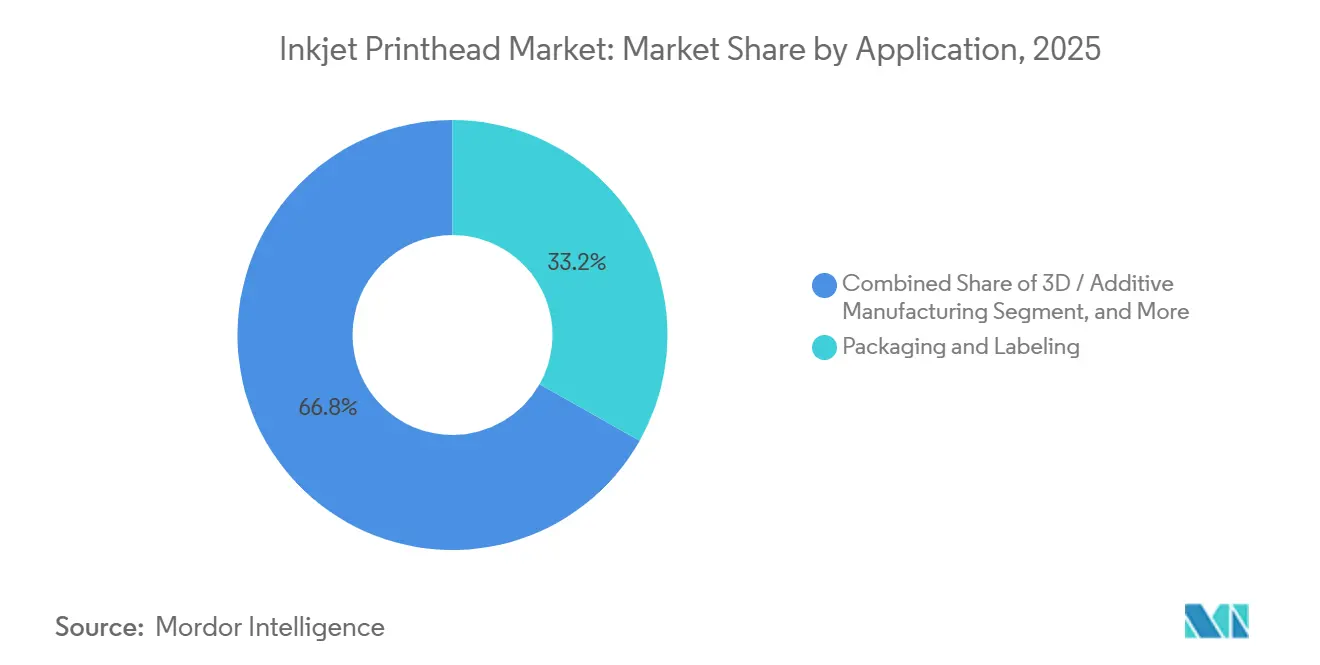

- By application, packaging and labeling accounted for 33.18% of revenue in 2025, and electronics printing is forecast to grow at a 5.23% CAGR through 2031.

- By end user, industrial printing accounted for 46.20% of the inkjet printhead market size in 2025, and graphic printing is advancing at a 4.81% CAGR toward 2031.

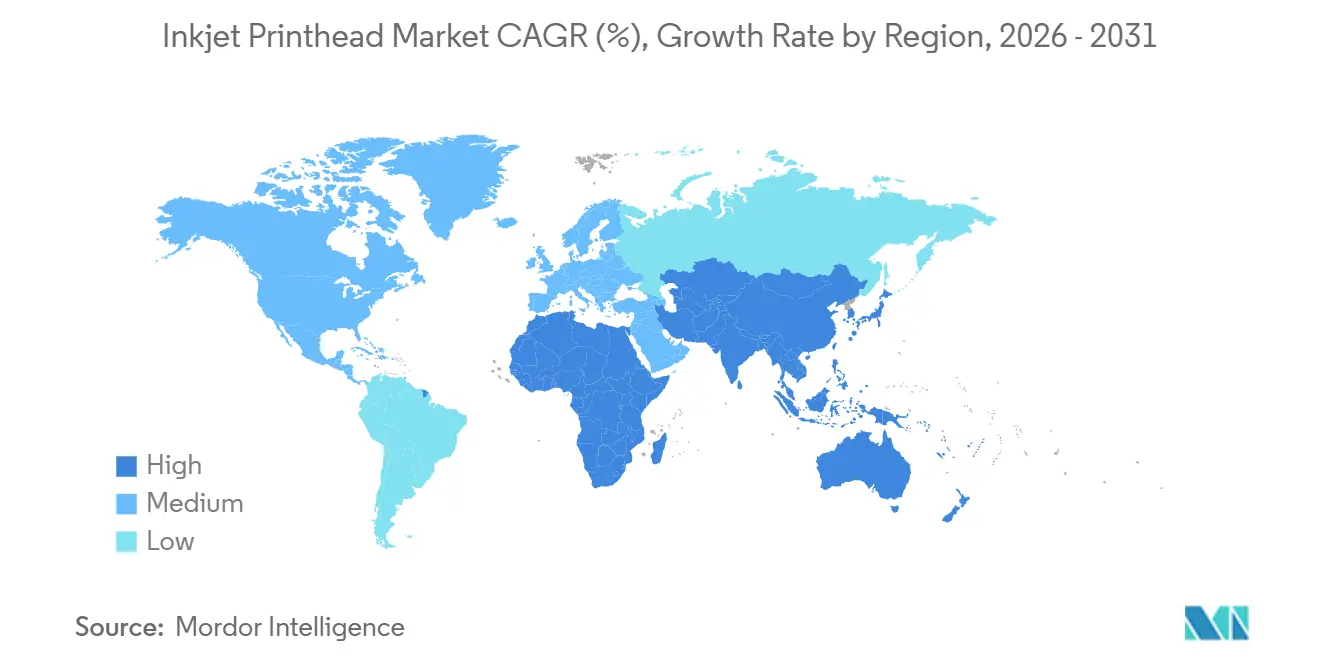

- By geography, Asia-Pacific accounted for 41.40% of revenue in 2025 and is set to record a 5.03% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inkjet Printhead Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion Of Single-Pass Digital Presses In Packaging And Textiles | +1.2% | Global, Concentrated In Europe And Asia-Pacific | Medium Term (2–4 Years) |

| MEMS And Thin-Film Piezo Allowing Below 2 pL Drops At 300 m/min | +0.9% | Japan And United States R&D Hubs | Long Term (≥4 Years) |

| OEM Shift To Open-Platform Printhead Sales | +0.7% | North America And Europe, Spillover To Asia-Pacific | Short Term (≤2 Years) |

| Sustainability Push For Water-Based Pigmented Inks | +0.6% | Europe, North America | Medium Term (2–4 Years) |

| AI-Driven Predictive Maintenance Lowering Downtime | +0.4% | Global | Medium Term (2–4 Years) |

| Emerging EHD Printheads For High-Viscosity Functional Fluids | +0.3% | Asia-Pacific And North America | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Explosion of Single-Pass Digital Presses in Packaging and Textiles

Packaging converters are moving from shuttle-based multipass setups to single-pass architectures that match flexographic speeds while eliminating plate-making delays. Field trials in late 2025 showed PrecisionCore heads sustaining 600 dpi on corrugated board at 200 m/min, enabling short-run labels without tooling.[1]Epson, “PrecisionCore Printhead Technology,” epson.com Textile mills in India and Bangladesh adopted direct-to-fabric units to meet fast-fashion cycles, dropping sample-to-production time from weeks to days. Although capital outlay per press exceeds USD 1 million, leasing and duty-rebate schemes in Vietnam and Turkey lower entry thresholds. Single-pass capability also supports printed-circuit solder-mask deposition, reinforcing the 5.23% CAGR projected for electronics applications.

MEMS and Thin-Film Piezo Allowing Below 2 pL Drops at 300 m/min

MEMS nozzle arrays paired with thin-film actuators achieve sub-2 picoliter droplets at line speeds of 300 m/min, unlocking precision tasks such as pharmaceutical coatings and fine-line circuitry. Xaar’s 2024 patent series details independent drive electronics for each nozzle that modulate volume on the fly. Kyocera’s KJ4 platform commercialized the concept with 600 nozzles/inch and variable drops from 1.5 to 42 pL, enabling both graphics and functional deposition.[2]Kyocera Corporation, “Industrial Printhead Solutions,” kyocera.com The advance reduces ink waste and lowers operating costs because smaller drops translate into less pigment usage per square meter. Over the long term, these heads underpin bioprinting and smart-packaging initiatives where accuracy outranks raw speed.

OEM Shift to Open-Platform Printhead Sales

In October 2025 Epson began licensing PrecisionCore modules to independent press builders, and Xerox followed with open-ink-set heads, dismantling the historical lock-step between hardware and consumables. Integrators can now source chemistry independently, swap printhead generations midcycle, and differentiate on workflow software rather than core jetting physics. Volume licensing expands the total addressable base but drives margin compression, pressing incumbents to derive more value from predictive-maintenance services and analytics instead of proprietary ink sales.

Sustainability Push for Water-Based Pigmented Inks

Europe’s Industrial Emissions Directive limits VOC discharge to 50 mg/m³, catalyzing the switch from solvent to aqueous pigment systems in corrugated and textile facilities.[3] European Commission, “Industrial Emissions Directive,” ec.europa.eu Water-based inks simplify waste handling and minimize operator exposure, aligning with brand sustainability pledges. Adoption remains highest on porous media because closed-cell substrates require forced-air drying that offsets energy savings. Although aqueous color gamut trails solvent alternatives, regulatory pressure plus customer preference keeps demand resilient, especially in jurisdictions imposing carbon-pricing on process emissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cap-Ex Premium Vs. Laser And Analog Heads | −0.8% | Global, Acute In South America And Africa | Short Term (≤2 Years) |

| Clogging Risk With Nanoparticle And White Inks | −0.5% | Global, High-Volume Industrial Sites | Medium Term (2–4 Years) |

| Patent Thickets Limiting New Entrant Scalability | −0.4% | North America And Europe | Long Term (≥4 Years) |

| Volatile Ceramics And Semiconductor Supply Chains | −0.3% | Global, Shortages In Asia-Pacific | Short Term (≤2 Years) |

| Source: Mordor Intelligence | |||

Cap-Ex Premium vs. Laser and Analog Heads

Industrial drop-on-demand installations range from USD 800,000 to USD 1.5 million per press, surpassing comparable flexo or laser lines by 40%-60%. Pay-per-print contracts shift cost distribution but raise lifetime outlay, deterring converters where financing costs exceed double-digit rates. South American and African plants with limited access to low-interest credit prolong analog reliance, especially in coding and marking where laser units deliver durable alphanumerics at lower service expense.

Clogging Risk with Nanoparticle and White Inks

Titanium dioxide and metallic particle formulations needed for white opacity or conductive paths tend to agglomerate below 200 nm, obstructing 50 µm nozzles.[4]Fujifilm, “Dimatix Inkjet Inks and Printheads,” fujifilm.com Daily purge cycles consume 5%-10% of inventory and incur USD 20,000-USD 50,000 in auxiliary recirculation hardware costs. Thermal heads exacerbate aggregation due to localized heating, whereas piezo designs mitigate stress but still require vigilant idle-state management. Downtime penalties are steep in 24/7 packaging lines where stop-start intervals cascade through upstream laminating and downstream die-cutting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Piezo Dominance Drives Precision Performance

Drop-on-demand heads held 61.3% revenue in 2025, and their 4.51% CAGR through 2031 underscores the inkjet printhead market's appetite for variable-data capability and substrate versatility. Piezoelectric actuation accommodates viscosities from 2 cP to 40 cP, enabling the deployment of UV, latex, and solvent inks on corrugated, fabric, and polymer films. Continuous-inkjet designs persist in coding niches that exceed 1,000 m/min while thermal heads remain entrenched in low-cost office devices.

MEMS miniaturization now halves energy draw per droplet, extending head life beyond 60 billion firings and widening the functional-fluid window to nanoparticle pastes. Thermal bubble heads struggle with high-viscosity chemistries and cannot independently modulate drop volume, limiting their industrial footprint. Continuous deflection systems still dominate egg and cable marking because charged droplets navigate curved or rough surfaces not feasible for slide-on shuttles. The reinforced R&D focus on piezo stacks signals prolonged leadership in the inkjet printhead market.

By Ink Type: UV-Curable Formulations Accelerate

Aqueous chemistry controlled 37.82% of the 2025 value as textile houses and corrugated plants prioritized low-VOC output, yet UV-curable inks will expand fastest at a 5.09% CAGR on the back of instant curing and food-contact compliance. Solvent inks persist in outdoor signage and vehicle wraps, where plasticized substrates need aggressive wetting and ultraviolet stability, while latex and sublimation occupy décor and polyester-apparel niches.

Eliminating infrared dryers shrinks floor space and trims energy by 30%-50%, a decisive incentive for narrow-aisle label facilities with high turnover. Nitrogen-inerted chambers add upfront cost but slash reject rates linked to oxygen inhibition. Water-based pigment systems remain dominant in cotton and cellulosics, though limited gamut and wash-fastness limit premium apparel print runs. UV growth trajectory confirms the inkjet printhead market preference for zero-dry-time workflows in pharmaceutical labels and smart-packaging prototypes.

By Application: Electronics Printing Outpaces

Packaging and labeling accounted for 33.18% of revenue in 2025, yet electronics and functional materials are forecast to grow at a 5.23% CAGR, reflecting demand for solder-mask deposition, legend printing, and conformal antenna patterns on flex circuits. Textile printing draws strength from fast-fashion cycles that require micro-batching of SKUs across Asia-Pacific mills. Coding and marking remain a staple application, but records only incremental growth as legislation mandates serialization on pharmaceuticals and beverages.

Electronics prototyping leverages sub-10 µm line widths delivered by piezo heads to iterate designs in days instead of photolithography weeks, aligning with agile hardware development. 3D and additive manufacturing use binder jetting to layer ceramics and metals, yet material qualification timelines and the dominance of powder-bed fusion temper near-term revenue. Packaging converters emphasize variable-data shipping cartons for e-commerce, driving further penetration of single-pass heads that integrate with warehouse management systems. Collective momentum maintains the inkjet printhead market on a diversification course beyond traditional graphic arts.

By End User: Industrial Printing Retains Lead

Industrial sites consumed 46.20% of 2025 shipments, spanning packaging converters, textile mills, and electronics fabs that operate three-shift production. Graphic printing, indicated to rise at a 4.81% CAGR, serves photo books, pop displays, and on-demand books where offset plate economics prove prohibitive at small volumes. Office and consumer devices recede in share as cloud storage reduces page counts and home working stabilizes post-pandemic.

High-throughput factories value uptime over per-liter ink price, accepting premium service contracts tied to predictive-maintenance dashboards. Graphic houses monetize variable-data imaging for personalized marketing, using wide-format heads with six-color sets to widen the gamut. Biomedical labs experiment with tissue-scaffold jetting, extending precision infrastructure into life sciences. The industrial cohort’s scale ensures the inkjet printhead market continues to orbit around high-duty-cycle use cases.

Geography Analysis

Asia-Pacific delivered 41.40% of the 2025 value and is set for a 5.03% CAGR as Beijing underwrites domestic MEMS lines and New Delhi’s Production Linked Incentive boosts textile digitalization. Shenzhen and Suzhou fabs raised printhead output by 25% in 2025, reducing import dependence and pivoting toward Southeast Asian consumption. Japanese firms still command over 60% of global piezo patents, but Taiwanese and South Korean challengers are eroding price premiums via simplified ceramic assembly.

North America posted the second-largest share, led by United States converters refitting corrugated presses for e-commerce logistics boxes and drug-makers integrating serialization heads ahead of full enforcement of the Drug Supply Chain Security Act. Canada benefits from adjacency to U.S. consumer-goods flows but suffers a mature installed base, lowering greenfield potential. Mexico’s maquiladora networks are piloting Legend Printing on automotive control modules, though adoption lags as Tier-1 suppliers validate reliability against screen-print incumbents.

Europe’s progress hinges on stringent VOC curbs that sideline solvent chemistries, driving the adoption of aqueous and UV-curable chemistries and thereby sustaining demand for compatible heads. Germany’s capital-equipment OEMs embed inkjet bars into hybrid offset lines, while Spain’s ceramic-tile sector exploits inkjet for decorative glazing impossible with analog rollers. South America and Middle East and Africa together form under 15% global share because financing constraints prolong analog dominance, though Brazil’s label converters and the United Arab Emirates’ tourist-oriented signage shops illustrate pockets of accelerated uptake.

Competitive Landscape

The top five vendors, Epson, Canon, HP, Ricoh, and Fujifilm, controlled roughly 55% of 2025 revenue, reflecting moderate concentration. Epson’s open-platform licensing marked a watershed that unlocked modular adoption by smaller press builders while compressing hardware gross margins. Canon extends thermal patents around bubble-formation physics, while HP advances thermo-inkjet for high-speed mail addressing. Ricoh and Fujifilm differentiate through ink recirculation and color-management firmware that embed predictive algorithms to flag early nozzle dropout.

Mid-tier players such as Xaar and Memjet challenge incumbents with field-replaceable arrays that minimize downtime and cut total cost of ownership, an appealing value proposition for converters running 24/7. Electrohydrodynamic and acoustic-wave startups target functional-fluid deposition at 50 cP or higher, potentially disrupting ceramic binder-jetting and conductive paste printing, though commercial volumes remain modest. Patent fences stay formidable but not impassable: new architectures operate outside piezo and thermal claims, illustrating how the inkjet printhead market is fragmenting into specialization zones anchored on viscosity range and fluid chemistry.

Service differentiation grows as vendors bundle IoT dashboards, AI-driven maintenance, and ISO-compliant color-profiling into annual subscription tiers. Customers evaluate total workflow cost rather than nozzle density alone, valuing software interoperability with ERP and design platforms. As supply chains for ceramic substrates and driver ASICs face allocation volatility, strategic supplier partnerships matter more than raw jetting metrics, and press builders hedge by dual-sourcing heads that share common nozzle-plate footprints.

Inkjet Printhead Industry Leaders

FUJIFILM Holdings Corporation

Canon Inc.

Ricoh Company, Ltd.

Seiko Epson Corporation

Kyocera Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kyocera launched a 1,584-nozzle head for ceramic-slurry jetting, enabling sub-20 µm layers in aerospace prototyping.

- October 2025: Epson began shipping PrecisionCore modules to third-party integrators, decoupling ink revenue from hardware.

- October 2025: Epson released the S3200-S1 head tuned for strong-solvent signage inks.

- September 2025: Fujifilm partnered with a European textile-equipment builder to integrate Dimatix heads into direct-to-fabric lines.

Global Inkjet Printhead Market Report Scope

The Inkjet Printhead Market Report is Segmented by Technology Type (Drop-on-Demand with Thermal and Piezo-based, Continuous), Ink Type (Aqueous, Solvent-Based, UV-Curable, Latex and Sublimation, Other Ink Types), Application (Packaging and Labeling, Textile Printing, Electronics and Functional Materials, 3D/Additive Manufacturing, Coding and Marking, Other Applications), End-User (Office and Consumer-Based, Industrial Printing, Graphic Printing, Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Drop-on-Demand | Thermal |

| Piezo-based | |

| Continuous |

| Aqueous |

| Solvent-Based |

| UV-Curable |

| Latex and Sublimation |

| Other Ink Types |

| Packaging and Labeling |

| Textile Printing |

| Electronics and Functional Materials |

| 3D / Additive Manufacturing |

| Coding and Marking |

| Other Applications |

| Office and Consumer-Based |

| Industrial Printing |

| Graphic Printing |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Technology Type | Drop-on-Demand | Thermal |

| Piezo-based | ||

| Continuous | ||

| By Ink Type | Aqueous | |

| Solvent-Based | ||

| UV-Curable | ||

| Latex and Sublimation | ||

| Other Ink Types | ||

| By Application | Packaging and Labeling | |

| Textile Printing | ||

| Electronics and Functional Materials | ||

| 3D / Additive Manufacturing | ||

| Coding and Marking | ||

| Other Applications | ||

| By End-User | Office and Consumer-Based | |

| Industrial Printing | ||

| Graphic Printing | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What Is The Projected Revenue For The Inkjet Printhead Market In 2031?

It Is Forecast To Reach USD 4.06 Billion By 2031 On A 4.11% CAGR Over 2026–2031.

Which Technology Type Leads Current Demand?

Drop-On-Demand Piezoelectric Heads Commanded 61.3% Revenue In 2025 And Show The Strongest Long-Term Momentum.

Which Application Segment Is Growing Fastest?

Electronics And Functional Materials Printing Is Projected To Advance At A 5.23% CAGR Through 2031.

Why Is Asia-Pacific The Largest Regional Market?

China’s Localization Subsidies, India’s Textile Incentives, And Japan’s MEMS Leadership Drive A 41.40% Share And A 5.03% CAGR.

What Is The Main Barrier To Broader Adoption Among Small Converters?

Upfront Acquisition Costs Remain 40%–60% Higher Versus Laser Or Analog Lines, Limiting Investment Capacity In Price-Sensitive Regions.

How Are OEMs Changing Competitive Dynamics?

Leading Vendors Now License Open-Platform Heads, Expanding Volume Potential Yet Compressing Unit Margins And Shifting Value To Service And Software.

Page last updated on: