Qatar Printing And Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

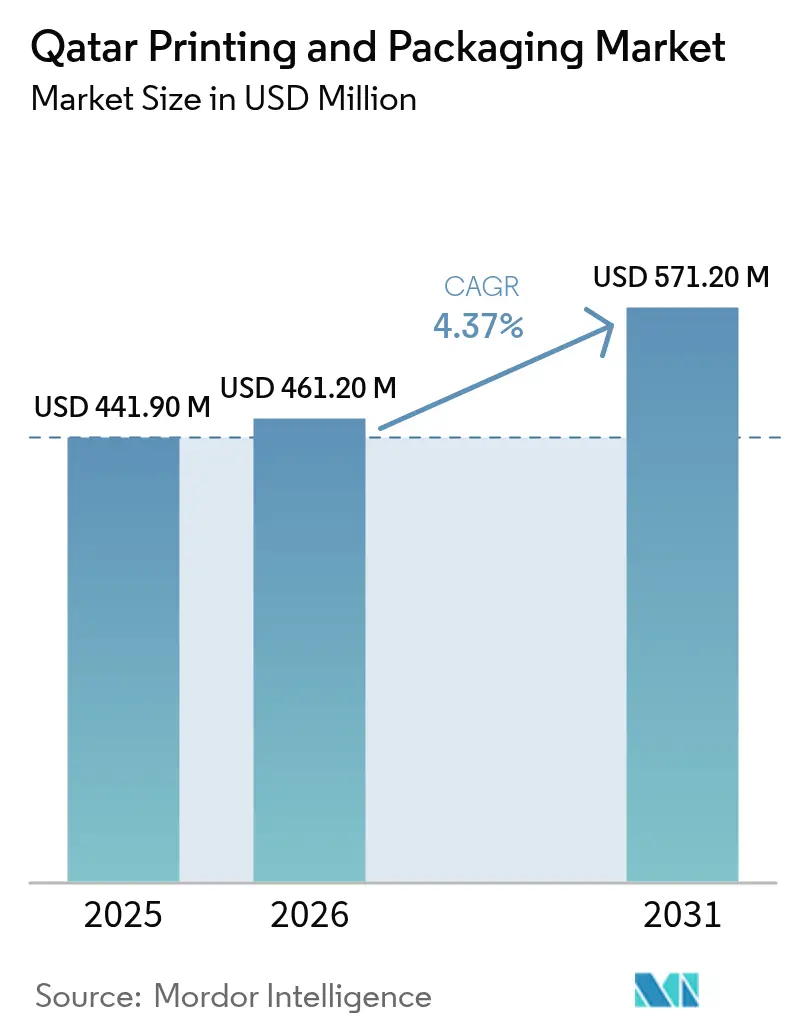

| Base Year Market Size (2025) | USD 441.9 Million |

| Market Size (2026) | USD 461.2 Million |

| Market Size (2031) | USD 571.2 Million |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

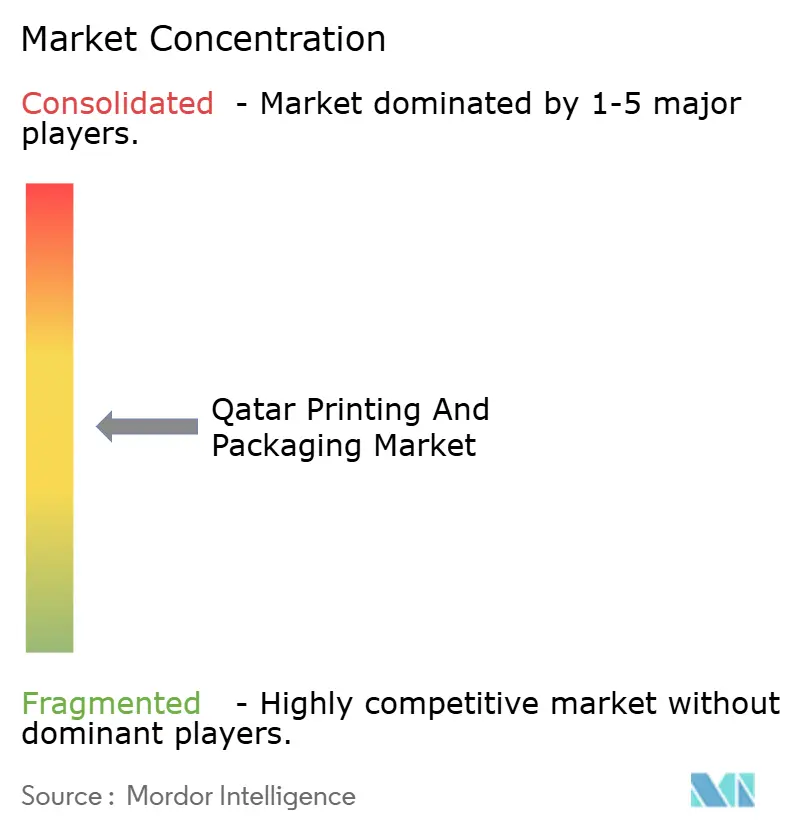

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Printing And Packaging Market Analysis by Mordor Intelligence

The Qatar printing and packaging market size is expected to grow from USD 441.9 million in 2025 to USD 461.2 million in 2026 and is forecast to reach USD 571.2 million by 2031 at 4.37% CAGR over 2026-2031. Rising private-sector participation, sustained non-energy PMI readings above the neutral 50-point mark, and pro-manufacturing policies embedded in the Third National Development Strategy keep demand on an upward path. Offset lithography anchors current volumes, but digital presses gain share as SMEs request short-run, variable-data work. Plastics dominate primary formats, yet paper and paperboard record the fastest growth as the 2022 single-use-plastic bag ban accelerates demand for recyclable substrates. High-barrier films linked to LNG cold-chain exports, and packaging for fast-moving consumer goods made locally under import-substitution programs, round out the main growth vectors.

Key Report Takeaways

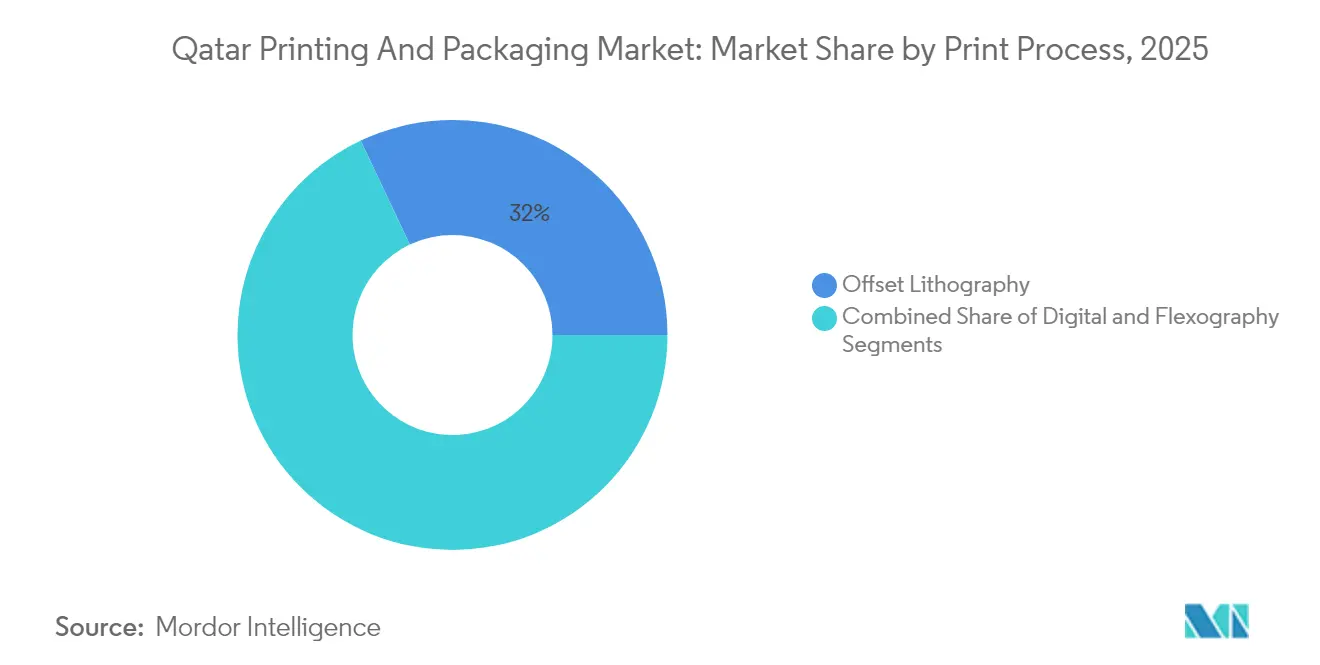

- By print process, offset lithography led with 32.02% of the Qatar printing and packaging market share in 2025, while digital printing is projected to expand at a 5.04% CAGR through 2031 .

- By packaging material, plastics captured 43.12% share of the Qatar printing and packaging market size in 2025, whereas paper and paperboard are forecast to advance at a 5.49% CAGR during 2026-2031 .

- By end-user industry, food packaging accounted for a 46.98% share of the Qatar printing and packaging market size in 2025, while pharmaceuticals is growing fastest at a 5.24% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Printing And Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfilment boom | +1.8% | National; GCC spill-over | Medium term (2-4 years) |

| Growth of domestic FMCG manufacturing | +1.0% | National | Long term (≥ 4 years) |

| FIFA legacy infrastructure spurring retail formats | +0.7% | Doha, Al Rayyan, Lusail | Medium term (2-4 years) |

| Mandatory single-use-plastic bag ban (Nov 2022) | +0.6% | National | Short term (≤ 2 years) |

| Rapid rise of digital label-on-demand for SMEs | +0.2% | National | Short term (≤ 2 years) |

| LNG cold-chain exports requiring high-barrier films | +0.2% | National; export links | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce fulfilment boom

Double-digit order-volume growth on leading platforms since 2024 is reshaping pack design toward lightweight, tamper-evident mailers that fit automated sortation lines. Streamlined customs processes shorten inbound-material lead times and free capital for converters to invest in digital presses. Brand owners now request on-box advertising, driving variable-data printing. Fulfilment centers near Hamad Port prefer locally converted corrugated boxes to cut dwell time. Consequently, the Qatar printing and packaging market receives a 1.8 percentage-point lift to its CAGR from this driver.

Growth of domestic FMCG manufacturing

Tax incentives and Factory One’s smart-manufacturing program encourage local food, beverage, and personal-care lines, each demanding primary and secondary packs that match international shelf impact. On-site artwork changes speed product refreshes, favoring digital workflows. Local converters enjoy proximity to end-users and real-time QC feedback, reinforcing the Qatar printing and packaging market’s pull for quality substrates. As more SKUs launch, run lengths shrink, raising demand for quick-change flexo and digital assets. The net effect is a 1.0 percentage-point gain in CAGR.

FIFA legacy infrastructure spurring retail formats

New malls and entertainment venues opened for the 2022 World Cup remain fully leased, sustaining premium point-of-sale packaging orders. Temporary promotions and limited-edition merchandising amplify short-run printing. Retail operators now specify FSC-certified paper and compostable films, aligning with national sustainability targets. These requirements benefit converters with certified supply chains, deepening the Qatar printing and packaging market’s value add. This driver contributes +0.7 percentage points to growth over the medium term.

Mandatory single-use-plastic bag ban (Nov 2022)

Retail grocers switched 100 million annual checkout bags to paper or reusable fabric in the first 12 months of the ban. Paper-sack converters increased capacity utilization to near 90% in 2024. Local biopolymer film trials received fast-track approvals from the Ministry of Municipality and Environment, signaling future demand for PHA and PLA blends. Small converters face capex pressures to adapt, yet overall packaging volumes edge up by 0.6 percentage points in the short term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile imported pulp and resin prices | -1.1% | National; import-dependent | Short term (≤ 2 years) |

| Low economies-of-scale versus UAE and KSA converters | -0.8% | National; cross-border impact | Long term (≥ 4 years) |

| Cap-ex intensity of high-spec flexo presses | -0.5% | National | Medium term (2-4 years) |

| Compliance cost of GCC food-contact directives | -0.3% | National; GCC-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile imported pulp and resin prices

Global freight surcharges and currency swings pushed kraft-liner quotes up 18% between Q4 2023 and Q2 2025, squeezing SME margins. Converters hesitate to hold inventory, delaying order cycles. While index-linked contracts are under discussion, none has achieved market acceptance, shaving 1.1 percentage points from the Qatar printing and packaging market’s CAGR.

Low economies-of-scale versus UAE and KSA converters

Regional peers operate plants exceeding 250 kt/y of board and flexible substrate, versus Qatar’s sub-50 kt/y sites, resulting in a 12% cost disadvantage on commodity. Higher unit costs curtail export wins and subtract 0.8 percentage points from growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Print Process: Digital Acceleration Reshapes Value Chain

Offset lithography generated the largest slice of the Qatar printing and packaging market in 2025, holding 32.02% as its cost efficiency favors large batch runs. Digital presses, though, are projected to grow at a 5.04% CAGR, scaling the Qatar printing and packaging market size for short-run and variable-data jobs. Brand owners value rapid artwork swaps, and e-commerce mailers now demand QR-code integration. The Ministry of Commerce’s Industry 4.0 roadmap has earmarked grants for digital upgrades, further stimulating uptake.

Greater inkjet resolution, inline finishing, and substrate versatility let digital lines encroach on mid-volume offset work. Converters combine hybrid offset-digital workflows to hedge cost and lead-time pressures. Flexography retains relevance for flexible packs but sees slower adoption due to high capex and operator-skill gaps. Consequently, the Qatar printing and packaging industry reallocates investment toward roll-to-roll digital presses, especially in labels and shrink sleeves.

By Packaging Material: Paper and Board Edge Ahead of Plastics

Plastics dominated with 43.12% of the Qatar printing and packaging market share in 2025 as HDPE and PET remain staples for food, beverage, and pharma. However, paper and paperboard are advancing fastest at a 5.49% CAGR, buoyed by the 2022 bag ban and retailer sustainability pledges. Corrugated producers add inline flexo folders to service e-commerce shippers, and folding-carton plants report capacity utilization above 80%. The forthcoming Ras Laffan ethylene complex will improve polymer supply security, yet much of the incremental resin may target export, leaving domestic plastics converters cautious.

Brand owners experiment with mono-material laminates that simplify recycling. Emerging micro-flute boards substitute rigid plastics in electronics gift packs. The Qatar printing and packaging market size for fiber-based substrates expands as printers secure FSC and PEFC chain-of-custody certifications to win multinational contracts.

By Packaging End-User Industry: Food Dominates, Pharma Surges

Food applications claimed 46.98% of 2025 revenue thanks to rising urban retail channels and expanded domestic processing lines. Pharmaceuticals, while still smaller, post the strongest trajectory at a 5.24% CAGR, underpinned by hospital expansions and cold-chain investment.Specialty laminates with aluminum barriers gain share to protect humidity-sensitive drugs. Beverage packaging remains robust as hotels and restaurants benefit from sustained tourism inflows. Household and personal-care segments adopt stand-up pouches with spouts, reflecting consumer demand for convenience.

E-commerce further stimulates secondary packs void-fill papers, printed mailers, and subscription boxes diversifying converter revenue. The Qatar printing and packaging industry’s value proposition evolves toward compliance, traceability, and smart-pack features such as NFC tags for anti-counterfeiting.

Geography Analysis

Doha, Al Rayyan, and Lusail generate more than half of the Qatar printing and packaging market’s volume, driven by dense retail footprints and FMCG headquarters. Post-World-Cup infrastructure keeps visitor traffic high, translating into steady packaging throughput for food, beverage, and souvenir items. Large offset houses clustered in Doha Industrial Area enjoy quick access to both the airport and Hamad Port, optimizing supply chain responsiveness.

Ras Laffan Industrial City is emerging as a strategic base for plastics packaging following the USD 6 billion ethylene cracker start-up, which shortens feedstock lead times and stabilizes film extrusion schedules. Industrial zones near Al Khor leverage free-zone incentives to attract corrugated converters focused on export packing for petrochemical equipment. Nonetheless, these zones face higher certification costs when shipping to GCC markets under new food-contact rules.

Corridors connected to Hamad Port and the Orbital Highway offer real-estate for greenfield plants targeting e-commerce shippers in the wider GCC. While land grants lower capex hurdles, utilities tie-in delays remain a risk. Overall, geographic diversification broadens the Qatar printing and packaging market’s customer base, though urban centers will continue to dominate volume.

Regulatory Landscape

Packaging and printed pack supply in Qatar is governed through a mix of national oversight and GCC-aligned technical requirements. The Ministry of Commerce and Industry (MOCI) enforces market control and inspection, including restrictions on goods bearing logos, symbols, or phrases that do not comply with Islamic values, customs, and traditions. These rules influence packaging artwork approvals and can raise reprint risk for brand owners and converters. Standards adoption is led by Qatar General Organization for Standardization (QS), which commonly aligns with GCC Standardization Organization (GSO) requirements used across the region.

For food-contact applications, compliance with GCC standards acts as a gatekeeper for both locally produced and imported packaging. GSO 839:2021 covers general requirements for all food packages, while GSO 1863:2021 sets requirements for plastic packages, including chemical migration and material composition expectations. Import processes also shape time-to-market for packaging materials and printed inputs: Qatar Customs documentation norms (commercial invoice, certificate of origin, and packing list with HS codes and weights, typically attested) raise the cost of non-compliance. Ministry of Public Health halal-related guidance for food imports further reinforces restrictions on non-halal substances and labeling practices, including date marking on original containers rather than stickers.

Value Chain Analysis

Qatar’s printing and packaging value chain starts with largely imported paper, board, inks, plates, and additives, while polymer feedstocks benefit from proximity to the country’s petrochemical base. This supports domestic conversion of polyethylene and related flexible formats. Conversion and printing are handled by a mix of local specialists across flexible packaging, labels, and cartons, alongside industrial packing and transit packaging players, including Qatar Plastic Products Company (flexible polyethylene), First Pack Factory W.L.L. (labels and flexible packaging), and Al Jattal Industry Co. (PET/PP roll sheets, thermoformed products, paper cups, and aluminum foils).

Secondary and industrial packaging needs are served by companies such as AWMPACK (pallets and industrial crating), while regional foodservice and paper-board packaging supply is supported by Hotpack Global’s operations in Qatar. Demand flows from food (including import handling and domestic processing), beverage, pharma, retail, and e-commerce shippers, with fulfillment nodes near Hamad Port shaping corrugated and protective packaging orders and turnaround requirements. The downstream chain is increasingly shaped by sustainability and circularity initiatives under the Ministry of Commerce and Industry’s National Manufacturing Strategy 2024-2030, which prioritizes plastics, food and beverage, and medical-related manufacturing and references a target to lift circular economy adoption among Qatari factories to 35% by 2030. This policy direction is pulling converters toward recyclable substrates, bio-based materials development, and tighter compliance workflows for food-contact packaging destined for GCC markets.

Competitive Landscape

The Qatar printing and packaging market remains fragmented: no player exceeds a double-digit share, and the top five collectively hold roughly 35%. Qatar National Printing Press leverages sheet-fed offset automation to win high-volume corporate stationery contracts. Aspire Printing Press blends offset and digital to address variable-data labels for healthcare. Galaxy Carton Factory expanded die-cutting capacity in 2024, targeting rising e-commerce box demand.

Digital-native start-ps deliver packaging-as-a-service platforms that let SMEs design, price, and order online, shifting competition toward turnaround speed. Regional giants from the UAE and Saudi Arabia challenge local firms on commodity runs using scale advantages and integrated resin supply. Compliance with GCC food-contact directives and the single-use-plastic ban has become a differentiator; converters offering certified compostable films secure retail rollouts more easily.[1] PackagingLaw.com, “Regulation of Food Contact Materials in the GCC Member States,” packaginglaw.com

Strategic investments continue. QatarEnergy and Chevron Phillips Chemical broke ground on the Ras Laffan petrochemicals project in February 2024, securing future HDPE supply.[2]QatarEnergy, “Annual Review 2023,” qatarenergy.qa Aspire Printing announced a USD 12 million digital-press upgrade in July 2025, adding seven-color inkjet capacity suitable for shrink sleeves. Larger converters evaluate joint ventures for recycled-content linerboard, but financing costs temper immediate execution.

Qatar Printing And Packaging Industry Leaders

Green Print W.L.L.

Galaxy Carton Factory W.L.L.

Aspire Printing Press Publishing and Distribution

Matco Packaging L.L.C.

Arabian Packaging Co. L.L.C.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Import substitution in FMCG and regulated segments remains a visible whitespace for Qatar-based converters. National industrial programs prioritize local manufacturing in areas that directly consume packaging (food and beverage and medical products) and build execution through multi-project initiative pipelines under the National Manufacturing Strategy 2024-2030. The opportunity for packaging suppliers is strongest where compliance and lead-time matter, including food-contact packs aligned to GSO 839:2021 and GSO 1863:2021, short-run and variable artwork changes enabled by digital workflows, and pharma packs that incorporate traceability features described by end users as value-add requirements.

Sustainable materials and circularity-linked capacity adds are another active pathway, supported by both enforcement momentum on single-use plastic reduction and private investment signaling. Papercut’s acquisition of a 60% stake in Enavra (announced in 2025) to develop a large-scale bioplastics manufacturing center points to upstream material localization that can expand availability of biodegradable or bio-based inputs for local film and bag converters. In parallel, industrial-logistics integration around Hamad Port, including food-security oriented facilities that combine processing, packaging, and distribution, creates a defined customer cluster for converters that can supply standardized secondary packaging, compliant labels, and fast replenishment cycles connected to port-centric inventory operations.

Recent Industry Developments

- April 2026: Speedline Printing Press announced a milestone marking 25 years of operations in Qatar, highlighting its offset printing and custom packaging capabilities serving retail and hospitality demand. The communication underscores continued local capacity in printed packaging and commercial print services as brand owners balance turnaround time with compliance-driven artwork control.

- November 2025: Papercut acquired a 60% stake in Enavra to advance a large-scale domestic biodegradable plastics manufacturing center. The move supports local sourcing of sustainable packaging materials and creates a pathway for Qatar-based converters to access bio-based resin alternatives aligned with national sustainability priorities.

- February 2024: QatarEnergy and Chevron Phillips Chemical broke ground on the Ras Laffan petrochemicals project, including an ethylene complex, strengthening the upstream feedstock base for polyethylene and related packaging substrates. This investment supports longer-term supply security for plastic packaging conversion and can reduce dependence on fully imported polymer supply chains for some formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the Qatar printing and packaging market as the value of packaging formats and printing activities used to serve end-user demand inside Qatar, captured at the country level and expressed in current USD for the base year and forecast years.

Scope exclusions: This sizing excludes printing that is not linked to packaging demand (for example, standalone commercial print for offices or marketing) and it excludes exports that are not consumed in Qatar.

Segmentation Overview

- By Print Process

- Offset Lithography

- Flexography

- Digital

- By Packaging Material

- Plastics

- Paper and Paperboard

- Glass

- Metal

- By Packaging End-User Industry

- Food

- Beverage

- Pharmaceuticals

- Personal and Household Care

- Other Packaging End-User Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to build the first set of demand signals for packaging and packaging printing in Qatar. Public sources such as Planning and Statistics Authority releases, Qatar Customs trade summaries, UN Comtrade country import data, and UN Industrial Development Organization manufacturing statistics helped us cross-check packaging use direction and the material mix.

We also reviewed policy and regulation updates that can shift packaging choices (for example, restrictions on single-use plastic bags), along with packaging-related standards and circular economy guidance published by local authorities. Company annual reports, investor presentations, and reputable press were used to understand capacity additions, product mix shifts, and end-use demand themes in food, beverages, and pharmaceuticals. In a few cases, paid subscriptions for company financials and import and export shipment-level data were used to validate specific assumptions. The sources listed here are illustrative, since we used many more references to clarify and verify the model.

Primary Interviews and Surveys

Primary work focused on validating how printing and packaging demand is contracted and priced in Qatar, and then pressure-testing model assumptions that are not visible in public data. We spoke with packaging converters, printing houses, material distributors, and large buyers across food, beverages, personal care, and pharmaceuticals. This helped us confirm typical order sizes, capacity utilization ranges, and the pace of the technology shift toward digital for short runs.

Because this is a single-country market, the fieldwork was balanced across national operations and different customer groups rather than by global region. We also re-contacted respondents when we saw mismatches between trade signals, capacity indicators, and implied consumption.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 18% | |

| Mid tier: 55% | Functional/Unit leaders: 25% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

The model starts with a top-down approach where end-use packaging demand in Qatar is reconstructed using consumption-linked indicators and trade flows, and then converted into value using typical pricing levels by material and print intensity. To keep the totals realistic, we corroborated the output using selective bottom-up checks, such as rolling up a sampled set of converter and printer revenues, and using ASPs times estimated volumes for common packaging formats.

Key inputs were chosen because they can be repeatedly tracked year to year, even with limited public disclosure. These include packaging material mix shifts (plastics versus paper and paperboard), print process adoption (offset, flexography, and digital), demand trends in packaged food and beverages, pharmaceutical packaging needs, and the effect of regulation on lightweight and reusable packaging. Forecasting was built using scenario analysis, where the base case is anchored to expected demand growth in core end-use categories and then adjusted using expert views on pricing pass-through and capacity additions. When bottom-up proxies were incomplete, gaps were handled using conservative ranges agreed with interview feedback, followed by a consistency check against trade and production signals.

Data Validation & Update Cycle

Model outputs were tested through multiple checks so that unusual jumps in value or mix could be explained before sign-off. We compared implied demand against independent signals such as packaging material imports, shifts in paper and paperboard usage, and observed pricing direction from channel feedback. If the driver behind an outlier could not be validated, we reviewed and corrected it.

A separate analyst review is completed to confirm assumptions, arithmetic, and year-over-year logic. Respondents are re-contacted when a key variable moves outside the expected band. Reports are refreshed annually, and interim updates are made when major events occur, such as material regulation changes or meaningful capacity expansions. Before delivery, a fresh pass is performed so clients receive the latest updated view.

Mordor Intelligence's Qatar Printing and Packaging Market Size Measured Against Other Published Estimates

Published market sizes for Qatar printing and packaging often do not match because the counted activities can differ, and so can the year used for currency conversion and pricing. Some estimates also mix packaging materials with broader commercial printing services, which changes the total even if the growth story sounds similar.

A second driver is how demand is linked to real usage inside Qatar. Some published figures lean heavily on a supplier revenue roll-up without fully separating packaging printing from non-packaging print jobs. In Mordor Intelligence, the value is counted only when printing and packaging demand is tied back to packaging end uses in Qatar, which keeps trade signals, material mix, and pricing progression aligned to the same consumption pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.44 B (2025) | |

| Trade Journal A | USD 0.62 B (2025) | Uses a broader interpretation that can include non-packaging commercial print and design services, and it applies a single blended price per output that can overstate value when digital short-run work rises. |

| Industry Association B | USD 0.38 B (2026) | Leans on member-reported production and does not fully adjust for non-member output and imported packaging consumption, and the year difference can shift totals when currency timing and material price changes are significant. |

The spread in the table mainly comes from what is counted as printing activity and how imports, local output, and pricing are brought together in one model. By keeping the scope tied to packaging-linked demand and by cross-checking totals against trade and end-use indicators, the estimate stays traceable to inputs that can be rechecked each year.

Key Questions Answered in the Report

How large is the Qatar printing and packaging market in 2026?

The market stands at USD 461.2 million in 2026 and is projected to reach USD 571.2 million by 2031.

Which print process is gaining the most momentum?

Digital printing records the fastest growth, expanding at a 5.04% CAGR through 2031 on the back of SME demand for short runs.

What material is growing quickest after the single-use plastic bag ban?

Paper and paperboard lead growth with a 5.49% CAGR as retailers shift to recyclable substrates.

Which end-user segment is the quickest to expand?

Pharmaceutical packaging advances at a 5.24% CAGR due to hospital and cold-chain investments.

How does the Ras Laffan ethylene complex influence local converters?

The complex secures domestic HDPE and ethylene supply, reducing feedstock risk and supporting high-barrier film production.

What is the key restraint for small converters?

Volatile imported pulp and resin prices erode margins, especially for firms without hedging capacity.

Page last updated on: