Thailand Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

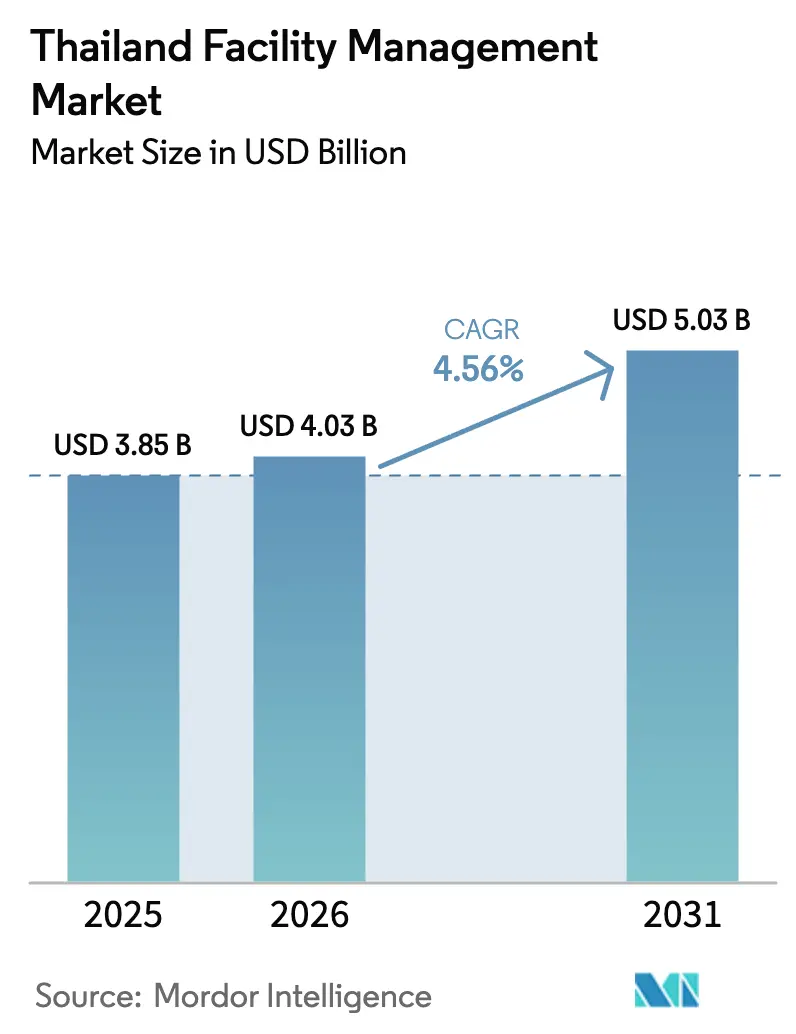

| Base Year Market Size (2025) | USD 3.85 Billion |

| Market Size (2026) | USD 4.03 Billion |

| Market Size (2031) | USD 5.03 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Facility Management Market Analysis by Mordor Intelligence

Thailand facility management market size in 2026 is estimated at USD 4.03 billion, growing from 2025 value of USD 3.85 billion with 2031 projections showing USD 5.03 billion, growing at 4.56% CAGR over 2026-2031. The growth trajectory is underpinned by Thailand 4.0 industrial upgrades, the Eastern Economic Corridor’s (EEC) infrastructure build-out, and a steady pivot toward technology-enabled outsourced models. Rising foreign direct investment, especially the 317 firms that entered the EEC during the first five months of 2024, is widening the addressable base for integrated hard and soft services. Digitalisation is reshaping service delivery as IoT platforms, AI-driven building analytics, and 5G connectivity improve asset uptime and energy performance. Growing corporate focus on employee wellbeing is amplifying demand for premium workplace experience offerings, while sustainability mandates are spurring retrofit work across commercial real estate. Nevertheless, labour shortages, regulatory fragmentation outside Bangkok, and volatile material costs are squeezing provider margins and intensifying competition.

Key Report Takeaways

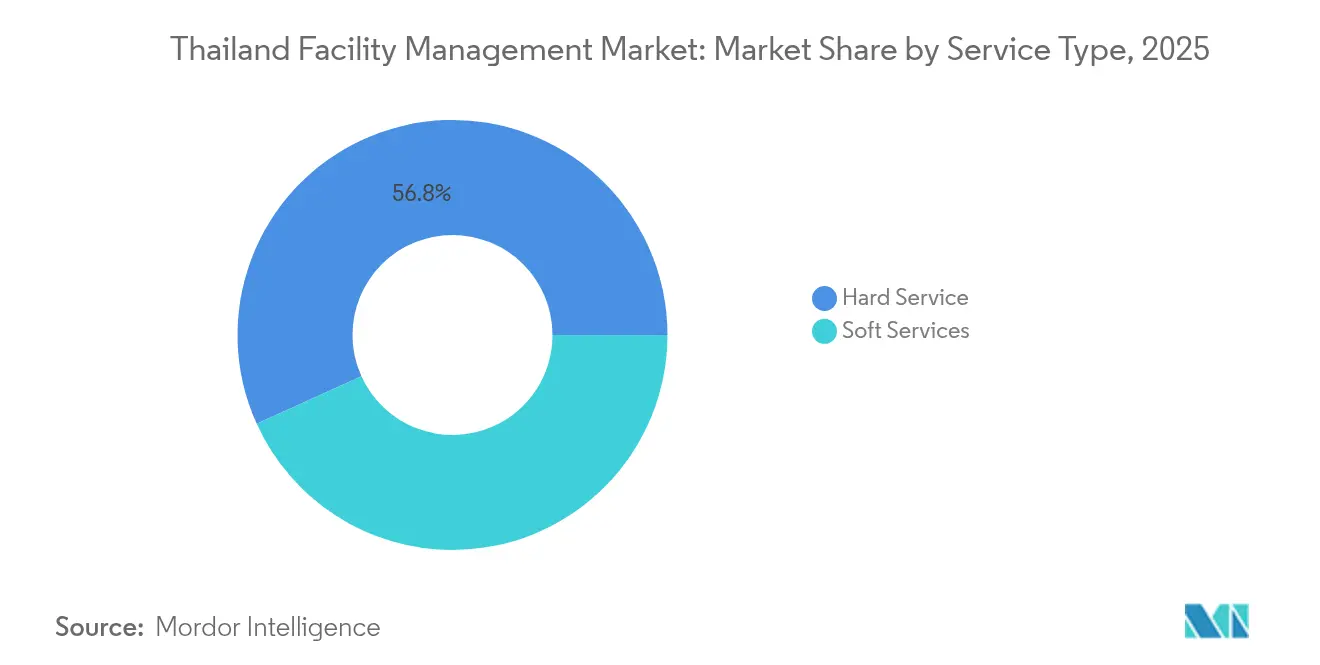

- By service type, Hard Services led with 56.78% revenue share in 2025; Soft Services is forecast to record the fastest 4.73% CAGR through 2031.

- By offering type, the Outsourced model accounted for 60.74% of the Thailand facility management market share in 2025 and is advancing at a 4.58% CAGR over the forecast window.

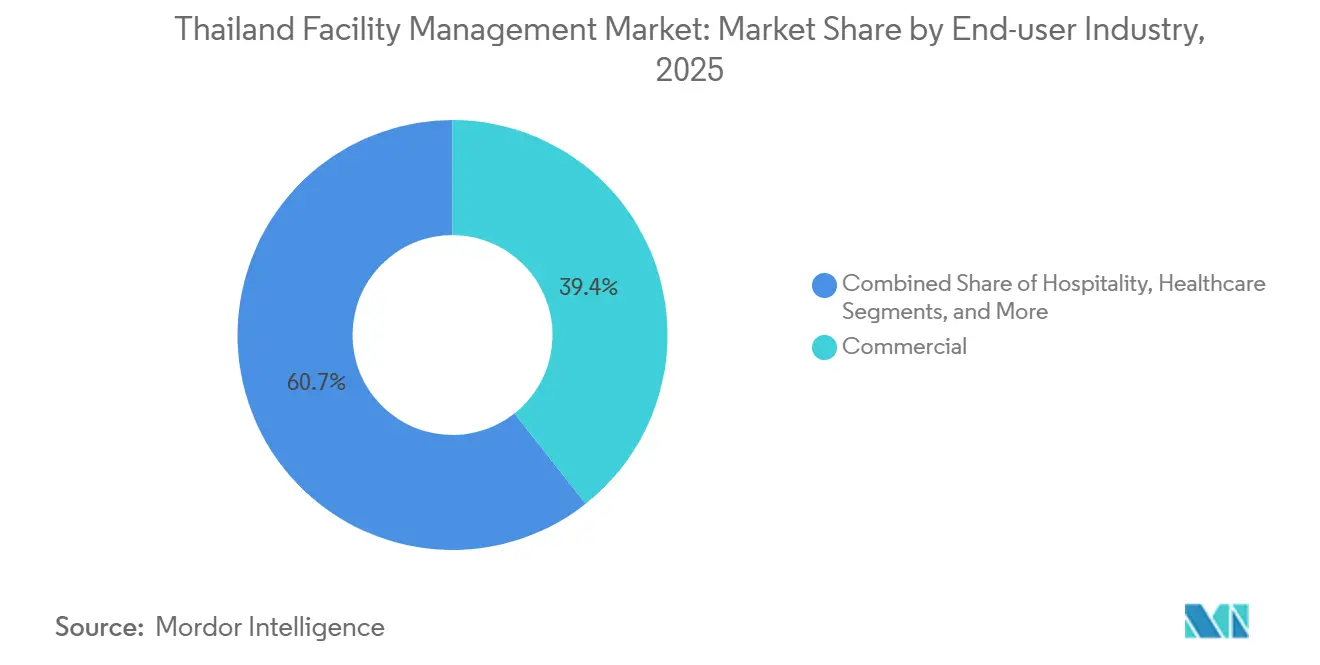

- By end-user industry, Commercial facilities held 39.35% of the Thailand facility management market size in 2025, while the Institutional and Public Infrastructure segment is set to expand at a 4.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid commercial real estate expansion | +1.2% | Bangkok; Chonburi, Rayong, Chachoengsao | Medium term (2-4 years) |

| Technology integration (IoT, AI, automation) | +0.8% | Nationwide; early gains in Bangkok and Chonburi | Long term (≥ 4 years) |

| Increasing outsourcing trend | +0.9% | Urban centres nationwide | Short term (≤ 2 years) |

| Rising focus on workplace experience | +0.6% | Bangkok; major metropolitan areas | Medium term (2-4 years) |

| Government incentives for FDI | +0.7% | EEC provinces; industrial estates nationwide | Long term (≥ 4 years) |

| Demand for green and energy-efficient assets | +0.5% | Bangkok; tourism-led secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Commercial Real Estate Expansion

Investment pledges for commercial projects surged 31% to USD 6.2 billion during Q1 2024, fuelling demand for cradle-to-grave facility solutions. [1]One Start One Stop Investment Center, “Thailand’s Jan-March Investment Pledges Soar,” OSOS.BOI.GO.TH Industrial-estate land sales within the EEC are rising 18–20% annually to 2025, compelling FM providers to scale asset-management and energy-services teams. WHA Group’s 2.9 million m² industrial portfolio and 154% jump in Q1 2024 profit underline how utility management revenues now rival rental income. Mixed-use icons like Central Pattana’s THB 15 billion (USD 0.43 billion) pipeline and the LEED-Gold SINGHA COMPLEX require multi-disciplinary FM programmes spanning security, HVAC, cleaning and ESG reporting. Concentration of new builds in Bangkok and the EEC lets service firms optimise route density and deploy shared mobile engineering hubs.

Technology Integration (IoT, AI, Automation)

Thailand’s IoT market is tracking toward USD 2.19 billion by 2030 as government smart-city incentives accelerate connected-building adoption. The St. Regis Bangkok achieved 9% energy savings after installing AI-based chiller analytics, validating quick pay-backs for data-driven plant optimisation. [2]AltoTech, “St. Regis Boosts Energy Efficiency,” ALTOTECH.AI AIS’s 5G mmWave deployment at Alliance Laundry’s factory in Chonburi delivers millisecond telemetry, enabling predictive maintenance for mission-critical equipment. Hitachi’s Lumada Center in Bangkok provides portfolio-wide dashboards that cut delivery lead times, and KaaIoT–Sensative partnerships bundle sensors with cloud platforms to offer subscription-based FM analytics. As digital-twin rollouts mature, providers embedding software skills alongside traditional trade capabilities are capturing premium contracts, positioning the Thailand facility management market for sustained tech-led growth.

Increasing Outsourcing Trend

The outsourced model already accounts for 61.23% of 2024 spend and will remain pivotal as corporates double down on core business focus. Dusit Hospitality Services’ three-year contract for the luxury MARQUE Sukhumvit condominium signals a migration of high-rise residential assets toward professional FM operators. Epicure Catering’s 70% healthcare share demonstrates how sector-specific expertise and food-safety certifications give outsourcing specialists a structural edge. Partnerships such as Tuya Smart and AiTAN integrate IoT backbone into outsourced bundles, letting FM firms provide remote equipment monitoring and mobile-first tenant apps. Labour-law complexity, including the Employee Welfare Fund starting October 2025, further encourages firms to pass compliance risk to seasoned FM suppliers. Collectively, these forces cement outsourcing as the dominant value-delivery channel within the Thailand facility management market.

Rising Focus on Workplace Experience and Employee Wellbeing

Hybrid work adoption and talent competition are amplifying demand for experiential workplaces. Knight Frank Thailand has delivered over 100 optimisation projects that reconfigure layouts, integrate sensor-based desk booking, and trim occupancy spending without sacrificing collaboration. Gaysorn Tower’s ‘Work-Live-Play-Grow’ model embeds hot-desking, wellness zones and community events, driving usership beyond pure square-footage metrics. AWS research shows Thai professionals with AI skills can earn 41% higher salaries, prompting enterprises to add digital amenities and continuous-learning zones inside their offices. Centara Hotels’ renewable-energy agreement with SCG Cleanergy targets a 20% carbon cut, aligning ESG credentials with employee expectations. These shifts enlarge soft-service scopes ranging from concierge to health and safety bolstering average revenue per contract in the Thailand facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and skill gaps | -0.7% | Nationwide; acute in Bangkok and industrial corridors | Short term (≤ 2 years) |

| Margin pressure from rising operational costs | -0.5% | Urban centres country-wide | Medium term (2-4 years) |

| Fragmented provincial regulatory compliance | -0.3% | Provinces outside Bangkok | Medium term (2-4 years) |

| High client churn among price-sensitive SMEs | -0.4% | Secondary cities nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Skill Gaps

Security, cleaning, and engineering roles face chronic scarcity, compelling providers to embrace robotics and software to ease labour intensity. Metthier’s security-as-a-service platform and autonomous cleaning fleet exemplify automation responses to staff deficits. Cross-border worker management remains cumbersome; academic studies urge clearer frameworks for Myanmar, Lao, and Cambodian migrants before ASEAN free-labour rules deepen mobility.[3]Publications at WASET, “Foreign Worker Migration in Thailand,” PUBLICATIONS.WASET.ORGEmployers prize AI fluency, but 64% struggle to find qualified candidates, straining digital-FM rollouts. Government “AI Ready” training has up-skilled 50,000 people, yet scale lags demand, pushing wages upward and compressing margins. Consequently, competitive advantage shifts toward companies melding human expertise with tech augmentation.

Margin Pressure from Rising Operational Costs

Construction-material prices swung down 2-3% in 2024 but are forecast to rebound 4.5-5.5% in 2025-2026, heightening cost-planning complexity for FM contracts that bundle repair works. Energy volatility remains acute; Siam Cement’s 55% profit drop in 2022 despite 7% revenue growth highlights utility cost exposure in large campuses. Labour inflation is poised to tick higher once the Employee Welfare Fund levy reaches 0.5% of wages by 2030. Hotel benchmarking reveals operating-cost per worker climbed 29% between 2015-2019, outrunning revenue and demonstrating bottom-line squeeze. Providers deploying robotics and energy dashboards, such as Frasers Property Industrial, can partially offset these pressures with productivity gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Market Foundation

Hard Services represented 56.78% of 2025 revenue, confirming their status as the structural backbone of the Thailand facility management market. NS-Siam United Steel’s Prime Minister’s Award for energy-efficient maintenance proves how process plants look to FM crews for sustainability wins. Asset-management assignments inside EEC estates are proliferating; Amata Corporation’s 1,322 MW co-generation portfolio now features data-driven scheduling that trims gas usage 10-15%. High-density Bangkok offices likewise heighten HVAC retrofits, with commercial buildings cutting average electricity use 18.1% after targeted upgrades.

Soft Services, though smaller today, post the briskest 4.73% CAGR, anchored by hospitality, healthcare and premium office complexes. Metthier’s robotic cleaners and AI patrol bots illustrate how technology compresses task times while meeting higher hygiene standards. Catering continues to professionalise; Epicure’s 70% share in healthcare and corporate dining demonstrates appetite for nutritionally-balanced menus and strict food-safety protocols. The fusion of technical and experiential offerings is blurring historic silos, encouraging integrated contracts that lift spend per property while improving user satisfaction.

By Offering Type: Outsourcing Accelerates Market Evolution

The outsourced channel captured 60.74% spend in 2025 and is expanding at a 4.58% CAGR, underscoring a decisive shift toward external specialists. Landmark multi-service awards such as ISS’s USD 135 million annual UK DWP deal demonstrate appetite for single-point accountability even beyond Thailand’s borders. In Thai real estate, Dusit Hospitality’s MARQUE Sukhumvit contract signals growing trust in third-party stewardship for luxury residential towers. Centara Hotels bundles energy management, housekeeping and AI chatbots into integrated packages that compress response cycles and drive occupancy.

In-house FM remains prevalent among large industrial operators that must guard intellectual property and mission-critical processes. Some SMEs choose single-service contracts to maintain tighter cost controls. However, regulatory complexity and skills scarcity are tilting the calculus toward hybrid models, where a retained client core team governs strategy while outsourcing transactional workloads to scalable vendors. Technology platforms supplied by Tuya Smart let clients pivot seamlessly between insourced and outsourced execution, reinforcing partnership flexibility.

By End-user Industry: Commercial Sector Leads Diversification

Commercial assets spanning offices, retail, logistics and data centres command 39.35% share, mirroring Bangkok’s prominence as a regional business hub. Central Pattana’s THB 15 billion roll-out of mixed-use properties, worth USD 0.43 billion, exemplifies pipeline depth that sustains year-round FM demand. Institutional and Public Infrastructure emerges as the quickest-growing bracket at 4.78% CAGR, propelled by the THB 253.45 billion (USD 7.24 billion) transport budget earmarked for 223 projects in 2025.

Hospitality is rebounding, with Centara reporting 12% revenue growth in 2024 and pledging nine new hotels by 2027, each requiring tech-enabled housekeeping and energy analytics. Healthcare facilities tap FM firms for stringent infection-control cleaning and energy management that imitates best-in-class hospital retrofits. Industrial and process owners, such as Betagro’s THB 297 million (USD 8.49 million) Lampang plant, integrate smart utilities at commissioning, ensuring long-run service contracts. Residential, entertainment and sports venues round out a diversified client mix, pressing providers to customise playbooks for widely varying occupant patterns.

Geography Analysis

Bangkok remains the epicentre of the Thailand facility management market, hosting premium offices like Gaysorn Tower (THB 3.74 billion or USD 0.11 billion) that mandate high-complexity FM regimes blending security, concierge, and green-building compliance. Dense CBD clusters enable vendors to create micro-zones, unlocking gains in technician utilisation and shortening response times.

The EEC provinces of Chonburi, Rayong, and Chachoengsao account for 54% of 2024 investment pledges, reflecting factory relocations and logistics park rollouts that are expanding facilities' footprints toward the eastern seaboard. Annual land-lease growth of 18-20% is driving demand for bilingual engineering crews, energy services consultants, and environmental, health, and safety audits. Highway upgrades and port expansions such as Laem Chabang’s Phase 3 raise long-term need for specialised infrastructure operations teams.

Northern and southern Thailand are emerging as catchment areas. Lampang’s agro-industrial build-outs and Chiang Mai’s data centre interest drive upticks in hard-service contracts. Phuket and Krabi tourism corridors adopt smart-city tech funded through Digital Economic Protection Agency grants, fostering remote monitoring solutions and green-hotel programmes. As 5G coverage widens, national providers can move from regionally siloed depots to network operating centres overseeing multi-site portfolios, driving consistent service quality across Thailand facility management market geographies.

Competitive Landscape

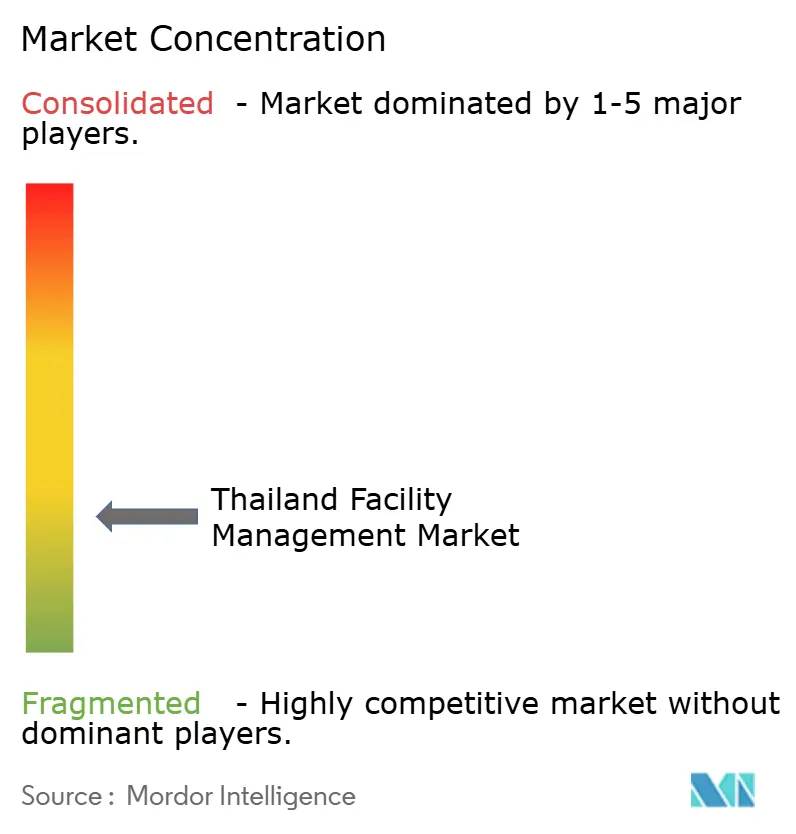

The Thailand facility management market is fragmented, with global incumbents such as ISS, Sodexo, and G4S competing with agile local names including Plus Property, Swift Dynamics, and Amata Facility Service. The top five operators collectively control well under 30% of spending, leaving ample headroom for mid-tier specialists. International firms leverage process discipline and cross-border key performance indicators, appealing to multinationals seeking uniformity across ASEAN footprints.

Local players counter with cultural fluency, faster decision cycles, and cost agility. Swift Dynamics, for instance, tailors ASEAN labour-sourcing schemes to minimise overtime costs, while Plus Property leans on parent Siam Piwat’s retail knowledge to secure mall-centric portfolios. Amata Facility Service leverages its industrial estate presence to cross-sell ancillary utilities and environmental monitoring services.

Technology is driving a competitive shake-out. Metthier, rebranded from GFIN, has amassed 380 contracts by embedding security robotics and data analytics in its service bundles. Tuya Smart’s platform alliances allow smaller firms to deploy smart-building stacks without heavy capex, narrowing the digital gap with multinationals. M&A interest is rising as operators seek scale economies to offset labour inflation and fund R&D; recent talks involve bundling soft-service specialists into hard-service-dominant portfolios to assemble end-to-end solutions.

Thailand Facility Management Industry Leaders

IFS Inc.

PCS Security And Facility Services Limited (OCS Group Holdings Ltd)

G4S Security Services (Thailand) Limited (G4S plc)

Sodexo Facilities Management Services (Sodexo Group)

Plus Property Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Betagro Public Company Limited opened a THB 297 million (USD 8.49 million) high-tech, eco-friendly chicken processing plant in Lampang, featuring smart utilities and integrated waste management.

- March 2025: An Italian-Thai Development-led JV signed a THB 9.34 billion (USD 0.27 billion) contract to build a 30 km stretch of the Thai–Chinese high-speed railway, adding new FM opportunities in rail infrastructure.

- January 2025: NS-Siam United Steel received the Prime Minister’s Industry Award for energy-efficient DX maintenance practices.

- November 2024: ONYX Hospitality and Equatorial Group announced the THB 2.5 billion (USD 0.07 billion) EQ Phuket luxury development with sustainability-centric FM designs.

Thailand Facility Management Market Report Scope

Facility Management is a function within organizations that combines people, space, and operations in the physical working environment to enhance the well-being of individuals and the efficiency of the main business operations.

The scope of the study has been segmented based on the type (in-house facility management and outsourced facility management (single FM, bundled FM, and integrated FM)), offering type (hard FM and soft FM), and end user (commercial, institutional, public/infrastructure, industrial, and other end users) across Thailand.

Thailand facility management market is segmented by type (in-house facility management, outsourced facility management [single FM, bundled FM, integrated FM]), offering type (hard FM, soft FM), end user (commercial, public/infrastructure, industrial, other end users). The market sizes and forecasts are provided regarding value (USD) for all the above segments.

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Thailand facility management market?

The Thailand facility management market size reached USD 4.03 billion in 2026 and is projected to grow to USD 5.03 billion by 2031.

Which service type dominates the Thailand facility management market?

Hard Services led with 56.78% share in 2025, mainly due to intensive industrial and infrastructure maintenance requirements.

How fast is the outsourced model growing?

Outsourced facility management is progressing at a 4.58% CAGR, driven by companies focusing on core business while externalising non-core operations.

Which end-user segment is expanding the quickest?

Institutional & Public Infrastructure facilities are forecast to grow at a 4.78% CAGR through 2031 as Thailand scales its transport and civic-works pipeline.

What are the principal challenges for providers in Thailand?

Acute labour shortages, rising operational costs and fragmented provincial regulations pressure margins and complicate nationwide service consistency.

How is technology influencing competitive dynamics?

IoT sensors, AI analytics and 5G connectivity allow providers to shift from reactive to predictive maintenance, improving asset uptime and differentiating service quality across the Thailand facility management market.

Page last updated on: