Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

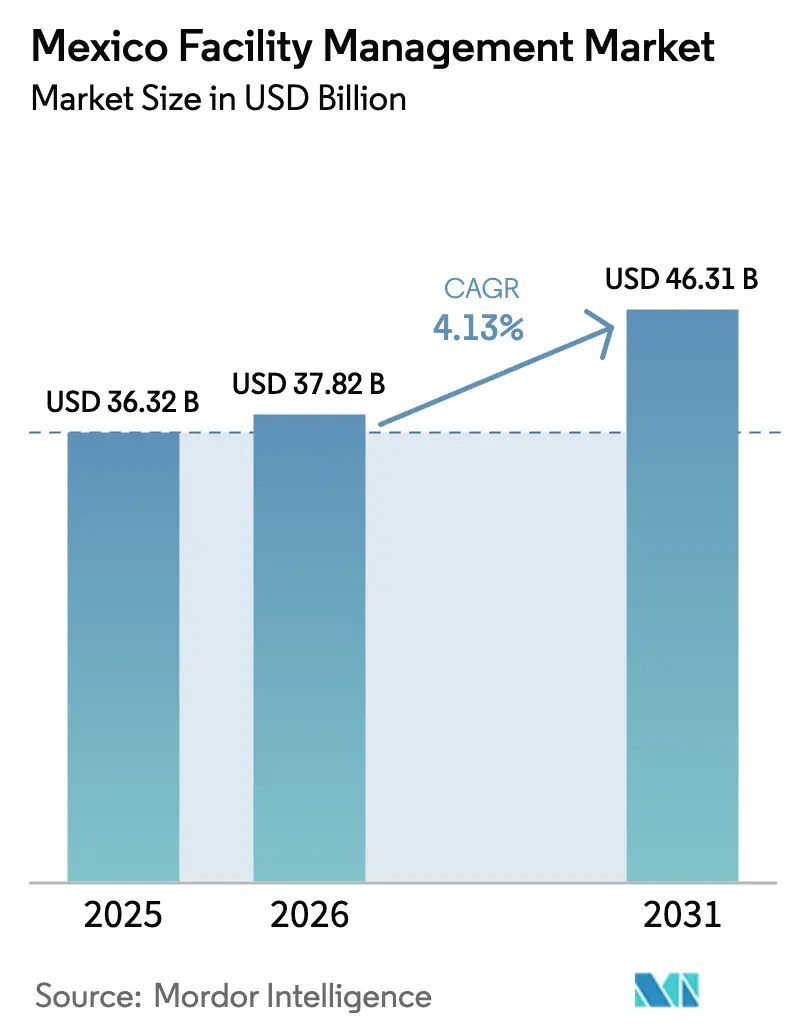

| Base Year Market Size (2025) | USD 36.32 Billion |

| Market Size (2026) | USD 37.82 Billion |

| Market Size (2031) | USD 46.31 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

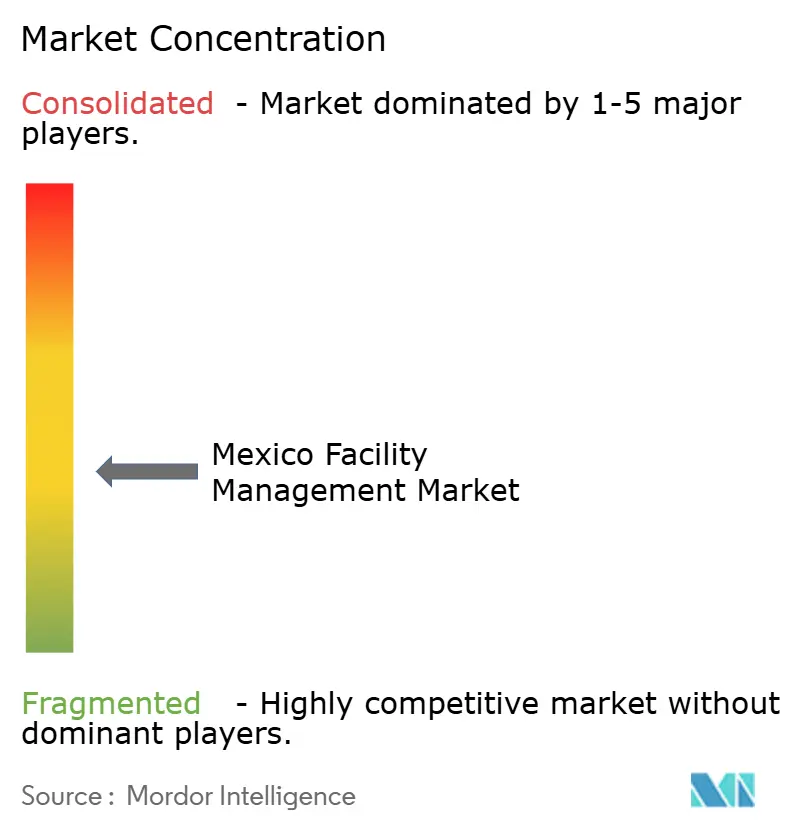

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Facility Management Market Analysis by Mordor Intelligence

The Mexico Facility Management Market size is expected to grow from USD 36.32 billion in 2025 to USD 37.82 billion in 2026 and is forecast to reach USD 46.31 billion by 2031 at 4.13% CAGR over 2026-2031.

This trajectory confirms the resilience of the Mexico facility management market amid accelerating nearshoring, large-scale infrastructure investment, and stricter labor-compliance frameworks. Intensified foreign direct investment, particularly from manufacturing companies relocating supply chains closer to the United States, is enlarging the national inventory of industrial plants that require outsourced maintenance and engineering support. Parallel federal commitments—such as the Federal Electricity Commission’s USD 23 billion modernization program—are raising demand for hard-service expertise spanning generation, transmission, and distribution assets. Corporations are also outsourcing real-estate operations to integrated facility management (IFM) providers to lower cost and meet rising ESG and USMCA labor-compliance mandates. Finally, PropTech adoption and IoT-enabled predictive maintenance platforms are reshaping service delivery models and creating data-driven value propositions within the Mexico facility management market.[1]Schneider Electric, “Why Mexico Is Central to Nearshoring Strategies,” schneider.com

Key Report Takeaways

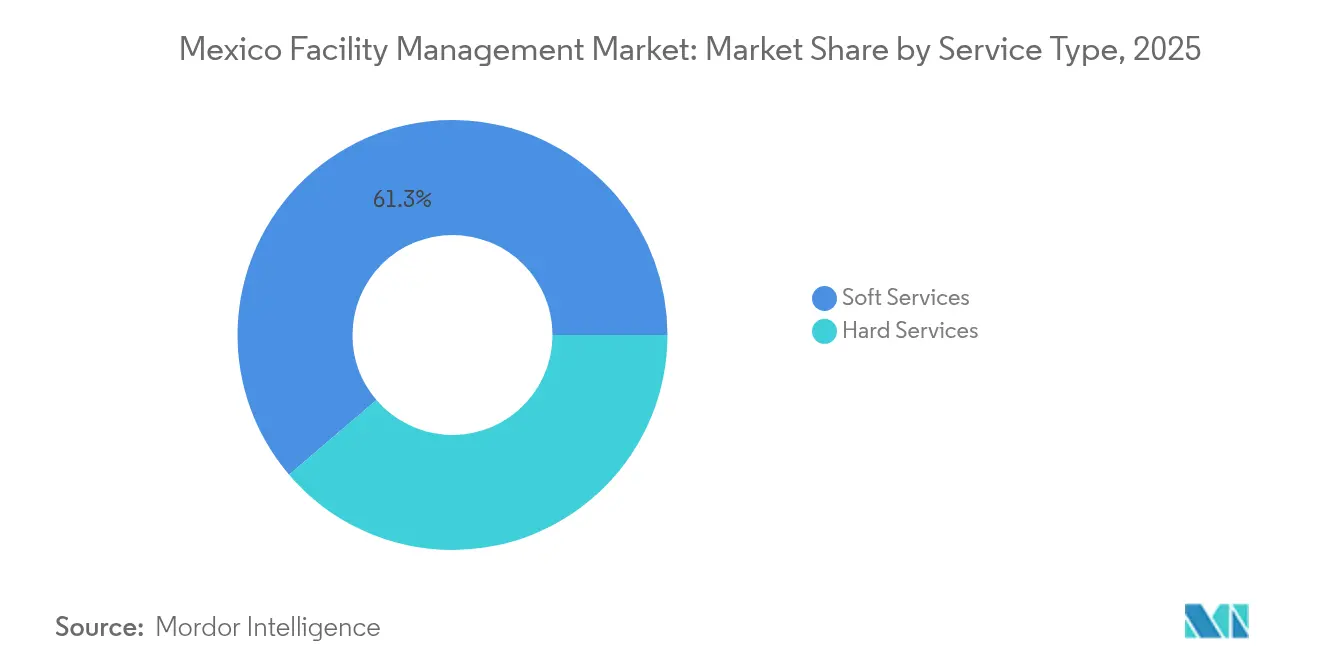

- By service type, soft services led with 61.25% of the Mexico facility management market share in 2025; hard services are projected to accelerate at a 7.88% CAGR through 2031.

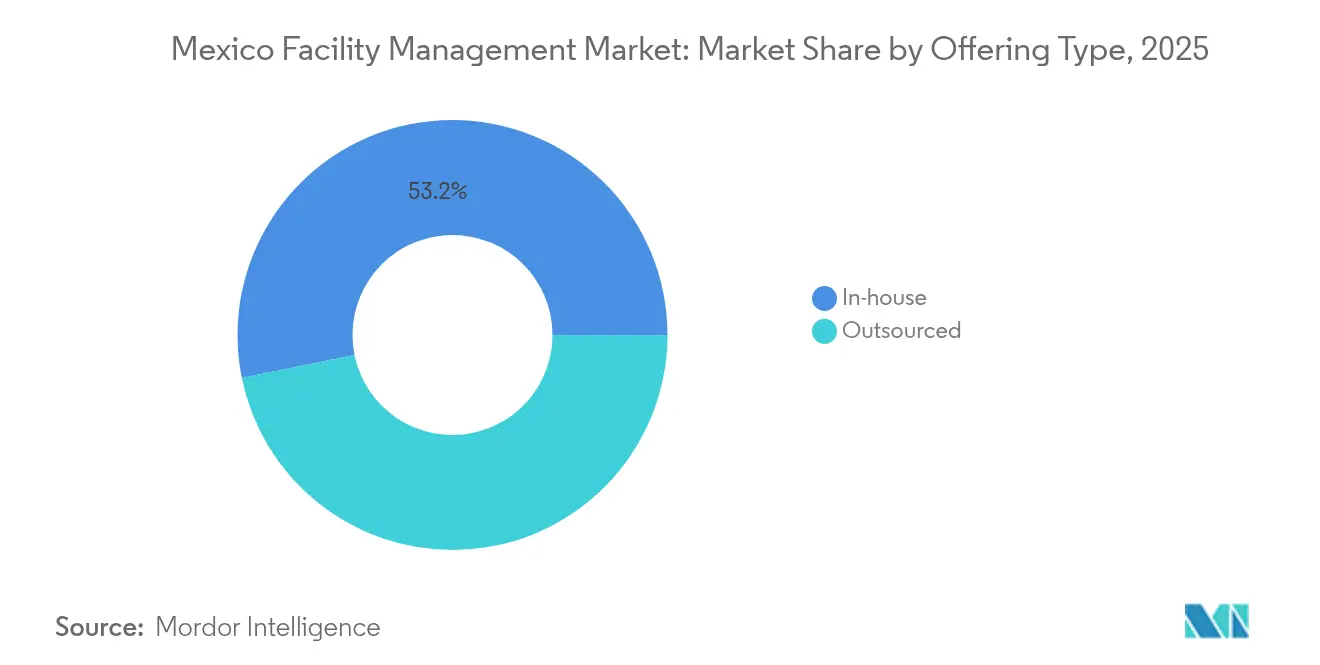

- By offering type, in-house solutions accounted for 53.20% share of the Mexico facility management market size in 2025, while integrated facility management is poised for the fastest growth at a 9.31% CAGR through 2031.

- By end-user industry, commercial facilities held 37.45% revenue share in 2025; healthcare facilities are forecast to expand at a 7.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring-driven expansion of industrial facilities | 1.20% | Northern Mexico, Bajío region | Medium term (2-4 years) |

| Uptick in corporate real-estate outsourcing to IFM providers | 0.80% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Federal mega-projects fueling hard-service demand | 0.60% | National, concentrated in southern states | Long term (≥ 4 years) |

| Growth in Grade-A office & mixed-use real-estate stock | 0.40% | Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| PropTech & IoT-enabled predictive maintenance platforms | 0.30% | Major metropolitan areas | Long term (≥ 4 years) |

| USMCA-linked ESG compliance push for certified green FM services | 0.20% | Border states, manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nearshoring-driven expansion of industrial facilities

Nearshoring has re-defined Mexico’s role in North American supply chains, with manufacturing contributing nearly 17% of national GDP in 2025 and industrial property requirements projected to surge 80% versus 2023 levels. Electronics, automotive, and aerospace producers have announced multi-billion-dollar upgrades, including French commitments totalling USD 3 billion that cover Valeo’s USD 800 million modernization and Hydrogène de France’s green-hydrogen projects. This wave of investment is swelling demand for specialized mechanical-electrical-plumbing (MEP) services, safety systems, and environmental monitoring—capabilities that the Mexico facility management market must scale rapidly. Semiconductor consortiums analysing USD 3 trillion in global fab outlays over the next decade identify Mexico as an emerging node, further underpinning long-term service demand. Providers that combine local labour expertise with global engineering standards stand to capture high-value contracts as plant operators seek turnkey compliance and operational continuity.[2]Co-Production International, “French Companies Accelerate Nearshoring Investments,” co-production.net

Uptick in corporate real estate outsourcing to IFM providers

Corporations headquartered in Mexico City, Monterrey, and Guadalajara are transitioning from fragmented, in-house maintenance to bundled IFM contracts that consolidate cleaning, security, technical, and energy-management services. Healthcare networks illustrate the value proposition, reporting 10-15% cost savings and tighter regulatory compliance after adopting unified solutions. The December 2023 rollout of NOM-037 telework standards added complexity to workplace oversight, propelling companies toward professional providers who track space utilization, air quality, and ergonomic parameters in hybrid offices. Digital dashboards that visualize service-level metrics in real time are now standard bid requirements, pushing the Mexico facility management market toward data-centric operations and performance-based pricing.

Federal mega-projects fuelling hard-service demand

Mexico’s National Infrastructure Program allocates USD 196 billion to energy, transport, and public-works schemes, with signature undertakings such as the Maya Train, Tulum International Airport, and hydropower refurbishments demanding sophisticated maintenance regimes. ANDRITZ’s USD 892 million contract to modernize nine hydro plants exemplifies the specialized industrial services pipeline that facility managers must support. Hard-service providers skilled in fire protection, HVAC optimization, and security electronics are negotiating multi-year agreements covering preventive maintenance, spares logistics, and remote system diagnostics. The concentration of projects in the south is reshaping geographic footprints, compelling firms to recruit and train technicians in states historically underserved by corporate FM.

Growth in Grade-A office & mixed-use real-estate stock

Developers are adding smart, amenity-rich towers in core urban zones, integrating building-management systems that require continuous fine-tuning and cybersecurity oversight. Luxury hotel investment climbed 50% in 2024, and the hospitality pipeline foresees expansion from USD 107.77 billion to USD 157.59 billion by 2029, catalysing premium service contracts. Parallel momentum in carrier-neutral data centers—expected to generate 14,688 indirect jobs—demands strict uptime and environment control specifications. Facility managers capable of coupling sustainability reporting with occupant-experience analytics are differentiating their bids as ESG metrics weigh heavily in tenant decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High informality of FM labor market limits service quality & scalability | -0.90% | National, acute in rural areas | Long term (≥ 4 years) |

| Intense price competition and low switching costs compress margins | -0.60% | Major metropolitan areas | Short term (≤ 2 years) |

| Stricter labor-safety regulations increasing compliance costs | -0.40% | Manufacturing hubs, border states | Medium term (2-4 years) |

| Frequent regional power outages causing unplanned maintenance spikes | -0.30% | National, severe in industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High informality of FM labour market limits service quality & scalability

Around 60% of Mexico’s workforce operates in the informal economy, depriving many facility services of standardized training, social-security coverage, and quality certifications. Past initiatives to formalize 200,000 service workers under International Labour Organization guidance achieved only partial success, hampered by high payroll taxes and weak enforcement. Multinational clients now insert clauses mandating documented worker benefits, forcing FM providers to shoulder added administrative burdens or risk disqualification. Informality perpetuates a pricing gap, squeezing formal firms that comply with taxes and benefits yet compete against cheaper, unregistered vendors.

Intense price competition and low switching costs compress margins

Cleaning, security, and landscaping contracts are frequently rebid on annual cycles, with clients leveraging low barriers to exit to negotiate steep discounts. The abundance of small local vendors drives a race to the bottom in metro areas, eroding profitability for large IFM operators that invest in technology and training. Some global players respond by tiering service levels, offering “lite” packages that meet basic performance metrics while reserving advanced analytics and ESG reporting for premium tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard services accelerate despite soft-service dominance

Soft services retained 61.25% revenue weight within the Mexico facility management market in 2025, reflecting enduring demand for cleaning, catering, reception, and security across commercial and institutional premises. However, the hard-service category is registering the fastest CAGR at 7.88% through 2031, driven by modernization of energy plants, smart-building retrofits, and rising legal mandates for fire and life-safety systems. Hard-service sub-segments such as MEP maintenance are benefiting from predictive analytics that can raise equipment availability by 25% and trim repair spend 20%.The segment’s outlook is also influenced by high-performance automation offerings like Johnson Controls’ Metasys BAS v14.0, which supports 800 IP devices and integrates BACnet clients for streamlined energy management. As clients adopt these platforms, the Mexico facility management market size for hard services is expected to expand steadily, rewarding vendors that pair engineering depth with data analytics. By 2025, asset owners view preventive maintenance compliance scores as a decisive KPI when awarding long-term contracts, tilting the landscape toward qualified, tech-enabled providers

By Offering Type: Integrated FM emerges as growth leader

In-house teams still control 53.20% of 2025 spending, particularly in government offices and state-owned utilities that Favor direct oversight. Yet demand for integrated outsourcing is climbing at a 9.31% CAGR, the fastest within the Mexico facility management market. Single-service and bundled offerings remain relevant for organizations testing outsourcing or focusing on niche activities, but IFM unlocks economies of scale and coordinated compliance. Healthcare systems cite 10-15% cost gains after migrating from scattered vendor rosters to master agreements managed by a single provider.

Digital command centers that consolidate building systems, labour scheduling, and supply chains underpin the IFM value case. Providers differentiate by embedding IoT sensors that feed AI engines capable of flagging anomalies in real time, thereby improving asset uptime and ESG metrics. Consequently, the Mexico facility management market size addressed by IFM vendors is expanding both in absolute dollar terms and in strategic importance to C-suite agendas.

By End-User Industry: Healthcare drives growth amid commercial stability

Commercial facilities—including offices, retail warehouses, and telecom switching centers—accounted for 37.45% of 2025 expenditure, providing a steady revenue base for soft-service specialists. The healthcare segment, however, is forecast to log the quickest 7.72% CAGR to 2031, propelled by new hospital builds, biomedical lab expansions, and stringent sterility and traceability standards. Baxter-owned Vantive’s nationwide home-delivery network highlights the operational complexity that specialized FM must support.

Hospitality receives a boost from luxury hotel pipelines and wellness resorts growing at 13% annually, demanding front-of-house excellence and back-of-house technical precision. Institutional and public infrastructure projects tied to the Maya Train and new airports require multi-disciplinary FM frameworks spanning crowd management, structural monitoring, and multi-utility integration. Industrial and process facilities remain the backbone of nearshoring, adding clean-room, battery-assembly, and hydrogen-handling infrastructure that widens the technical scope—and revenue potential—of the Mexico facility management market.

Geography Analysis

Mexico facility management market, anchored by near-border manufacturing clusters in Baja California, Nuevo León, and Chihuahua. Tijuana’s industrial vacancy breached 2% for the first time in three years during mid-2024 as developers raced to deliver factories for electronics and EV suppliers. Monterrey alone has added 22 million ft² of new industrial space since 2022, with construction costs rising a contained 3.2% year on year. A dense ecosystem of suppliers, logistics corridors, and bilingual workforce keeps service demand high for both soft- and hard-FM specialists.

Central Mexico—Mexico City, Guadalajara, Querétaro—represents the fastest-growing geography through 2030 as tech campuses, cloud data centers, and corporate headquarters proliferate. Developers are integrating LEED-certified systems and tenant-experience applications that favour IFM providers with digital competencies. The Mexico facility management market size for Central Mexico thus carries an outsized share of high-margin, technology-rich contracts.

Competitive Landscape

The Mexico facility management market remains moderately fragmented, with global conglomerates competing alongside regional specialists. ISS reports global revenue of DKK 83.7 billion and 5.8% organic growth in Q2 2024, balancing broad service catalogs with local regulatory expertise. Sodexo generated EUR 12.5 billion in H1 2025, leveraging integrated food and FM packages and prioritizing sustainability innovation. Johnson Controls, a frontrunner in building systems, posted USD 5.4 billion Q1 2025 sales and grew its Building Solutions backlog to USD 13.2 billion, underscoring appetite for automation platforms.

Strategic moves include CBRE’s January 2025 acquisition of Industrious National Management Company, merging workplace experience with operations and targeting USD 20 billion in BOE revenue. Aramark’s December 2024 purchase of Quantum Cost Consultancy Group added nearly USD 500 million in procurement spend, strengthening supply-chain leverage across Latin America. Meanwhile, ISS has embedded ESG officers at corporate level to align Mexican contracts with global decarbonization goals, reinforcing credibility with multinational tenants.

White-space opportunities revolve around IFM for mid-market manufacturers and data-center operators, plus specialized services for renewable-energy assets. PropTech entrants offering AI-assisted fault detection and drone-based façade inspections are forging partnerships to penetrate large portfolios. Competitive intensity is most pronounced in cleaning and security, where low entry barriers and informal labour keep prices under pressure. Providers that can certify labour practices, deploy IoT-backed transparency, and finance technology upgrades are positioned to consolidate share in the evolving Mexico facility management market.

Mexico Facility Management Industry Leaders

ISS Mexico

Sodexo Facilities Management Services

CBRE Mexico

Grupo EULEN Mexico

JLL Mexico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Feb 2025: Johnson Controls reported USD 5.4 billion Q1 2025 sales, up 4% year over year, and lifted full-year guidance as Building Solutions backlog reached USD 13.2 billion.

- January 2025: CBRE acquired Industrious National Management Company, creating a Building Operations & Experience segment projected at USD 20 billion in revenue.

- January 2025: Mexico unveiled Plan 2025, offering immediate tax deductions for new investments and extended incentives for training and innovation until Sept 2030.

- December 2024: Aramark finalized the acquisition of Quantum Cost Consultancy Group via Avendra International, adding nearly USD 500 million in managed spend.

Mexico Facility Management Market Report Scope

Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. While Hard services include physical and structural services like fire alarm system lifts, among others, soft services include cleaning, landscaping, security, and similar human-sourced services, providing a solution to end-users such as Commercial Buildings, Retail, and Government, Public Entities, etc.

The Mexico facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Mexico facility management market?

The market was valued at USD 37.82 billion in 2026 and is projected to reach USD 46.31 billion by 2031.

Which service type is growing fastest?

Hard services are expected to post a 7.88% CAGR through 2031, driven by infrastructure upgrades and smart-building adoption.

Why is integrated facility management gaining traction?

Integrated contracts deliver 10-15% cost savings, simplify compliance, and leverage IoT analytics for better asset performance.

Which end-user industry offers the highest growth potential?

Healthcare facilities are forecast to expand at a 7.72% CAGR because modernization demands specialized compliance and sterility controls.

How does nearshoring influence facility management demand?

Foreign manufacturers relocating to Mexico are adding millions of square meters of industrial space, boosting demand for technical FM services.

What regions present new opportunities for service providers?

Southern states benefit from mega-projects like the Maya Train and Dos Bocas Refinery, requiring providers to establish new operations there.

Page last updated on: