Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

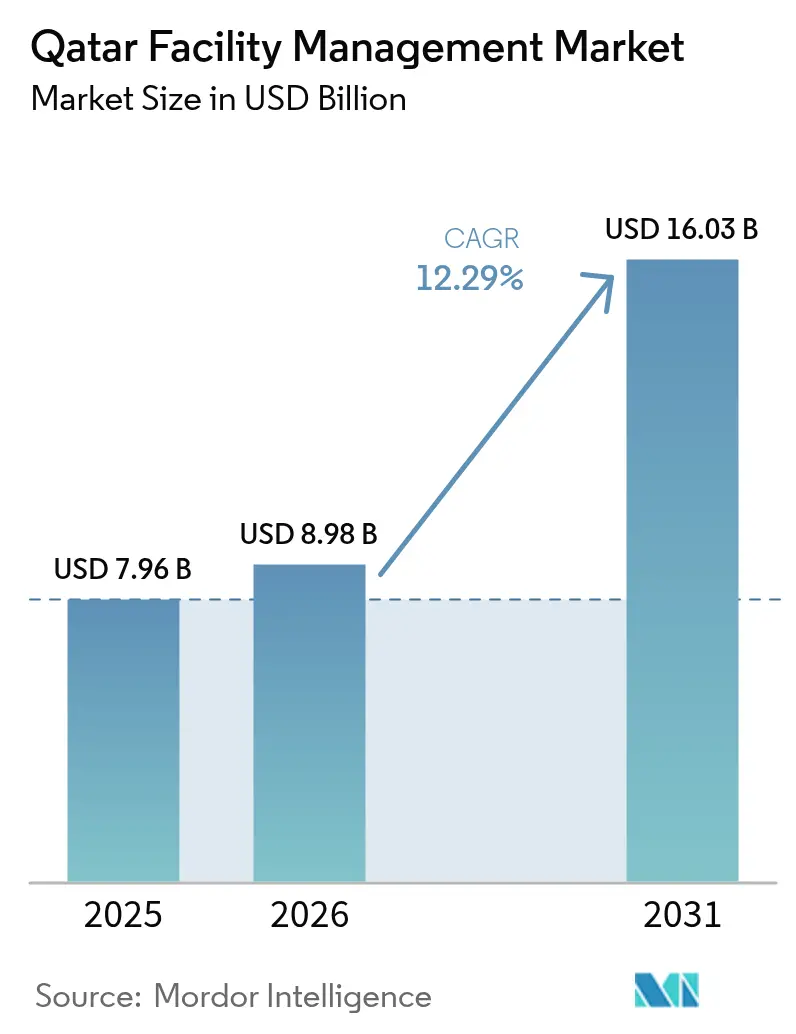

| Base Year Market Size (2025) | USD 7.96 Billion |

| Market Size (2026) | USD 8.98 Billion |

| Market Size (2031) | USD 16.03 Billion |

| Growth Rate (2026 - 2031) | 12.29% CAGR |

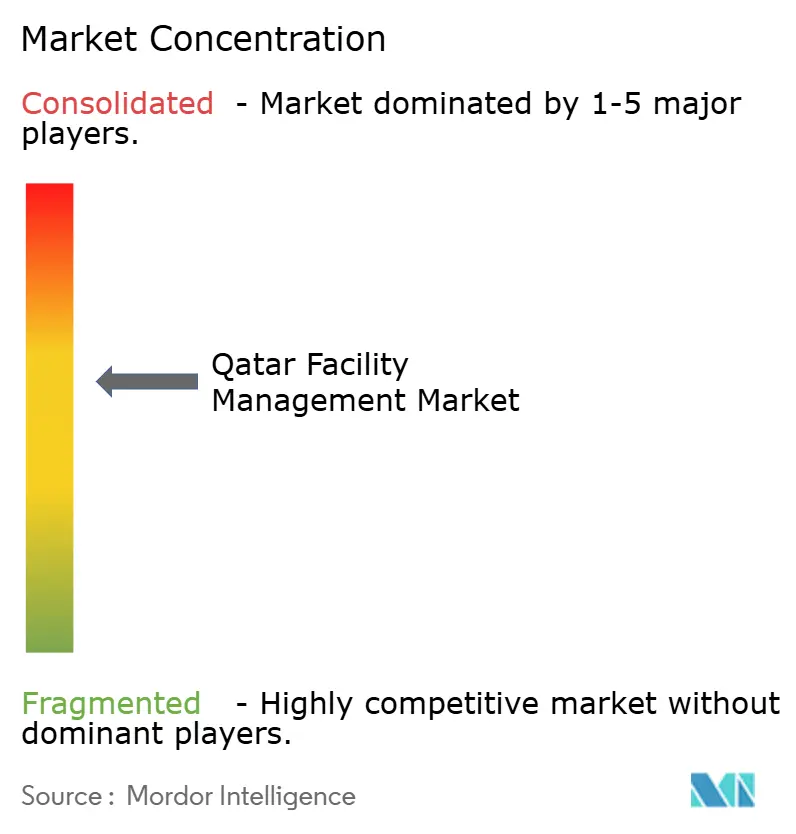

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Facility Management Market Analysis by Mordor Intelligence

The Qatar facility management market size is projected to expand from USD 7.96 billion in 2025 and USD 8.98 billion in 2026 to USD 16.03 billion by 2031, registering a 12.29% CAGR between 2026 to 2031. Robust demand is shifting from World Cup-era construction toward long-term asset optimization, and the emphasis on outcome-based contracts is widening margins for providers that can deliver measurable energy savings. The Qatar National Vision 2030 framework is accelerating digital adoption, particularly Internet-of-Things sensors and computerized maintenance management platforms, which are now baseline requirements in most public tenders. Regulatory support for public-private partnerships is deepening the pipeline of 20-to-25-year concessions that bundle financing with operations, while district-cooling mandates are steering hard-service revenues away from chiller plants toward secondary distribution networks and metering. Labor-market reforms that favor skilled technicians over low-skill expatriate labor are raising operating costs but also opening opportunities for local upskilling alliances with vocational institutes.

Key Report Takeaways

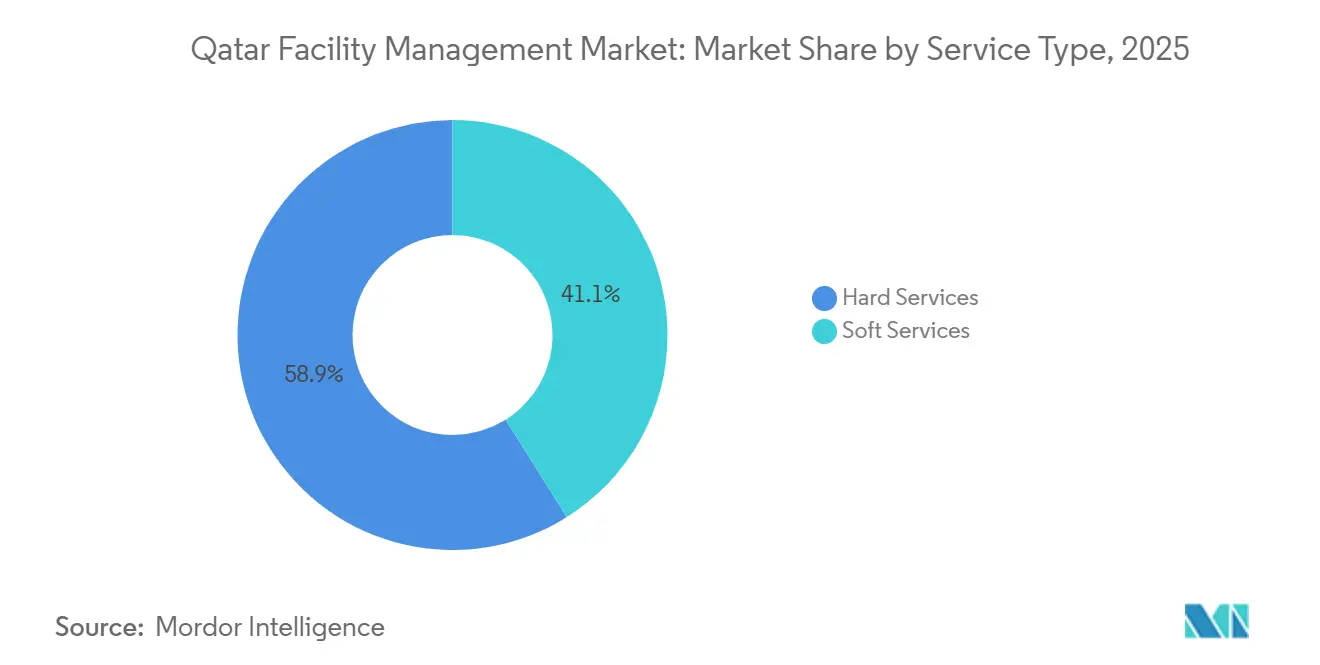

- By service type, hard services led with 58.92% of Qatar facility management market share in 2025, while Soft Services are forecast to post the fastest growth at a 12.41% CAGR through 2031.

- By offering type, outsourced models commanded 62.87% of the Qatar facility management market in 2025, and Integrated Facility Management is projected to register a 12.32% CAGR between 2026 and 2031.

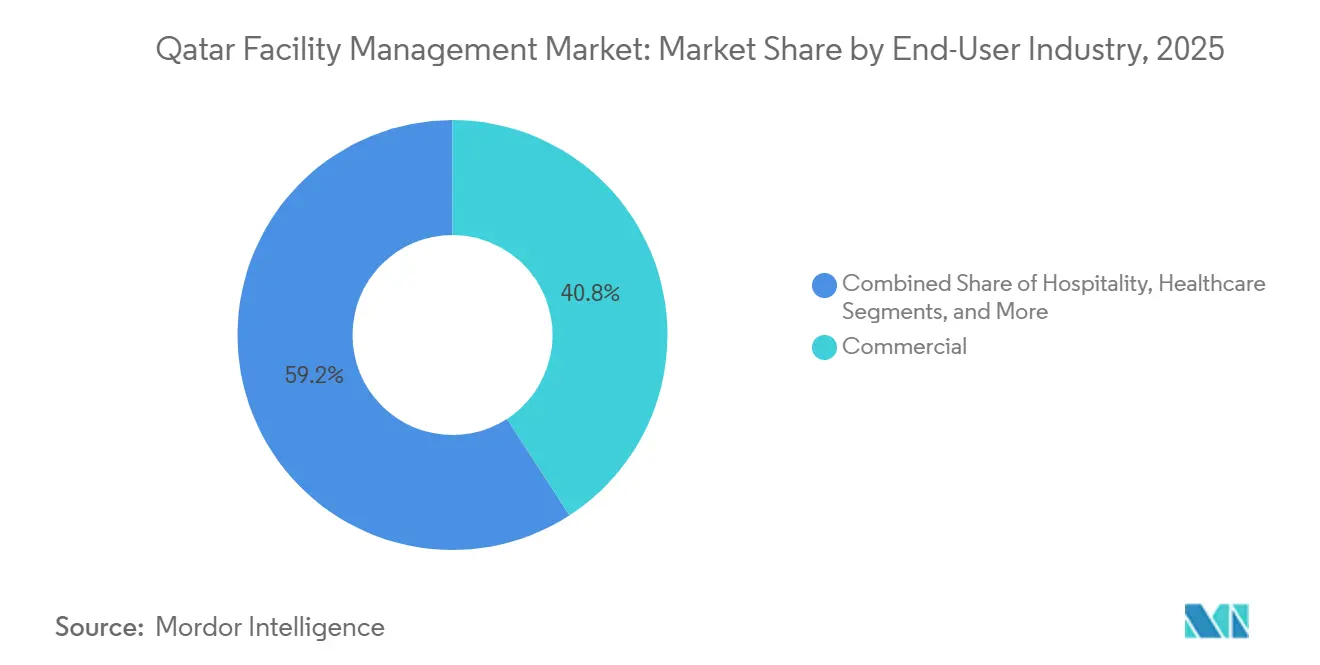

- By end-user industry, the Commercial segment contributed 40.84% of 2025 revenue, whereas the Industrial and Process segment is expected to expand at a 12.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-World Cup Infrastructure Utilization | +2.8% | National, Doha-Lusail Corridor | Medium Term (2–4 Years) |

| Technological Innovation And Smart-City Integration | +2.3% | Lusail, Msheireb, Nationwide Roll-Out | Long Term (≥ 4 Years) |

| Regulatory Evolution And Labor-Market Transformation | +1.9% | National | Medium Term (2–4 Years) |

| Sustainability And Energy-Efficiency Imperatives | +1.7% | New-Build Districts Country-Wide | Long Term (≥ 4 Years) |

| Growth Of Hyperscale Data Centers And Critical-Infrastructure Requirements | +1.5% | Ras Laffan And Doha Clusters | Long Term (≥ 4 Years) |

| Rise Of PPP Models For Facility Operations In Special Economic Zones | +1.2% | Education, Healthcare, Hospitality Hubs | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Post-World Cup Infrastructure Utilization

Seven permanent stadiums, a 76 km metro and more than 100 new hotels have shifted from event-mode to daily operation. These assets together add roughly 1.5 million m² that require continuous MEP upkeep, pitch care, crowd-flow management and soft services that can flex with tourism peaks. Metro ridership running near 60% of tournament highs is sustaining multi-year predictive-maintenance contracts, while Ashghal’s 2025-2029 program prioritizes lifecycle extension over new builds, locking in stable workloads for incumbent FM providers.[1]Supreme Committee for Delivery and Legacy, “World Cup Legacy Report 2023,” sc.qa

Technological Innovation and Smart-City Integration

Lusail’s city-wide operating platform aggregates data from some 10,000 IoT sensors, enabling central command centers to dispatch FM crews based on real-time energy, traffic and waste metrics. Msheireb Downtown achieved a 31% cut in cooling intensity after linking 100 buildings to a district-wide BMS, setting a benchmark now written into public procurement. Government Digital Agenda 2030 rules that all new public buildings comply with ISO 16484 are pushing bidders to show proven competence in analytics-driven maintenance and cyber-secure BMS deployment.[2]Lusail Real Estate Development Company, “Smart City Operating System,” lusail.com

Regulatory Evolution and Labor-Market Transformation

Law No. 12 of 2024 fixes Qatarization at 10% for firms with 50-plus staff, requiring FM contractors to recruit nationals into supervisory and technical roles historically filled by expatriates. Abolition of the kafala system has improved mobility, yet payment-cycle delays of up to 12 months are straining cash flow, accelerating consolidation among vendors able to absorb working-capital shocks.[3]Ministry of Labour, “Workforce Strategy 2024-2030,” mol.gov.qa Heat-stress regulations banning outdoor work in summer daylight hours further compress maintenance windows, increasing reliance on night operations and modular workshops.

Sustainability and Energy-Efficiency Imperatives

KAHRAMAA’s district-cooling mandate for projects above 10,000 m² is steering value toward secondary distribution and metering services bundled with energy-performance guarantees. New rules requiring 50% of makeup water to come from treated effluent saved 18.5 million m³ in 2024, lowering plant operating costs by 12%. National solar targets and the region’s first USD 2.5 billion green sukuk are stimulating demand for FM providers that can pair PV maintenance with traditional hard services under gain-share contracts.[4]Qatar Central Bank, “Green Sukuk Issuance Report 2024,” qcb.gov.qa

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive Pricing Pressures | -1.4% | National | Short Term (≤ 2 Years) |

| Skilled Labor Shortages | -1.2% | National | Medium Term (2–4 Years) |

| Lengthy Payment Cycles In Government-Led FM Contracts | -0.9% | National | Short Term (≤ 2 Years) |

| Data Residency And Cybersecurity Constraints On Cloud-Based FM Solutions | -0.6% | National | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Competitive Pricing Pressures

The lowest-qualified-bidder rule on public tenders below QAR 5 million has commoditized routine cleaning and security. A 2024 news-agency tender drew 33 offers, with the winner priced 18% under the incumbent, exemplifying margin squeeze. Slower non-hydrocarbon GDP growth and fewer new builds narrow the contract pipeline, keeping renewal competition fierce and encouraging vendors to seek scale economies or transition into higher-margin hard services.

Skilled Labor Shortages

Only 20% of expatriate workers are classified as skilled, yet demand for certified HVAC, electrical and BMS technicians is rising alongside smart-building roll-outs. Wage premiums of 30% over general operatives, plus regional poaching by Saudi megaprojects, elevate direct labor costs. Visa-linked employment limits mobility and average technician tenure is just 3-4 years, challenging service consistency and inflating recruitment and training outlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Revenue, Soft Services Accelerate

Hard Services contributed 58.92% of 2025 revenue, confirming the capital intensity of MEP, HVAC and fire-safety upkeep in critical facilities. Within this basket, MEP services benefit from the expansion of district cooling, shifting focus from chiller plants to energy-transfer stations and smart metering. Fire-system upgrades mandated for public schools in 2025 have further buoyed demand. Asset-management contracts now routinely stipulate ISO 55000-compliant computerized systems, evidencing the digital pivot. Soft Services are expected to outpace with a 12.41% CAGR to 2031, buoyed by hospitality and commercial landlords outsourcing cleaning, catering and security to trim fixed payrolls. A crowded low-barrier vendor pool keeps price competition high, but differentiation through green cleaning and infection-control certifications is emerging.

The Qatar facility management market size for Soft Services is set to expand rapidly as hotels and malls rebound in visitor numbers, while Hard Services retain the largest Qatar facility management market share owing to mandatory technical compliance in hospitals, metros and data centers. Catering gains tailwinds from offshore energy sites requiring cold-chain logistics, whereas security contracts increasingly bundle access-control technology with manned guarding. Market leaders are investing in robotics for floor care and drones for façade inspection to curb labor exposure and meet night-shift work windows imposed by heat-stress rules. The Qatar facility management industry therefore shows a clear bifurcation: volume remains in Hard Services, but growth momentum is tilting toward tech-enabled Soft Services.

By Offering Type: Outsourced Models Dominate, Integrated FM Gains Traction

Outsourced delivery held 62.87% share in 2025 as state entities and multinationals pursued risk transfer and variable‐cost structures. Single-service contracts prevail in retail and hospitality, yet bundled agreements are rising as procurement teams chase administrative simplicity. Integrated Facility Management, coupling hard and soft scopes under KPI-linked fees, is the fastest-growing niche at a projected 12.32% CAGR. Recent large awards, such as the five-year Qatar Foundation deal covering 25,000 assets, underscore the pivot toward single-provider accountability.

Integrated contracts often tie remuneration to energy savings, uptime or occupant satisfaction, positioning vendors with IoT analytics capability to command premiums. PPP frameworks embed 20- to 25-year operate-maintain clauses that align the Qatar facility management market size for integrated services with asset-lifecycle horizons, enhancing revenue visibility. In-house models persist at critical-security entities, yet even these organizations trial partial outsourcing for non-core tasks. Consequently, the Qatar facility management market is transitioning from transactional purchasing to partnership-oriented models that reward performance rather than headcount.

By End-User Industry: Commercial Leads, Industrial Accelerates

Commercial real estate generated 40.84% of 2025 turnover on the back of Doha’s 12 million ft² of Grade A offices and an extensive mall footprint. However, the Industrial and Process segment is forecast to deliver the quickest growth at 12.47% CAGR through 2031, fueled by petrochemical expansions and data centers that demand 24/7 critical-environment support. Hospitality remains the second-largest user base, though lower occupancy versus tournament peaks restrains price uplift for premium soft services.

Healthcare facilities call for infection-control expertise and continuous engineering presence, raising entry barriers and supporting price resilience. Industrial clusters at Ras Laffan and Mesaieed require NEBOSH-qualified teams, creating a moat for specialized providers. Data-center growth, led by projects scaling beyond 50 MW, blends mechanical, electrical and cybersecurity upkeep, forging a distinct sub-vertical within the Qatar facility management industry. Overall, the Qatar facility management market size attached to industrial users is expanding faster than commercial stock, altering the service-mix outlook toward high-reliability contracts.

Geography Analysis

Doha and its satellite municipalities account for roughly three-quarters of national revenue, anchoring the Qatar facility management market in a dense corridor of ministries, towers, hotels and World-Cup legacy venues. Lusail’s 38 km² smart-city grid serves as a live laboratory for IoT-driven FM, with successes expected to spill into older districts. Msheireb Downtown’s energy-intensity gains illustrate how district-wide BMS can command premium service fees.

Ras Laffan and Mesaieed host LNG and petrochemical assets that demand specialist industrial FM, including hazardous-material handling and emergency-response readiness. Hamad Port’s logistics zone, targeting 3 million TEU by 2030, is a growth pocket for temperature-controlled storage, pest control and security contracts that bundle electronic surveillance with perimeter patrols.

Al Khor municipality, centered on Al Bayt Stadium and adjacent mixed-use districts, is transitioning into a year-round events hub, sustaining pitch maintenance and crowd-flow services. Nationwide, Ashghal’s USD 22.2 billion plan to 2029 emphasizes maintenance over new build, widening the geographic footprint of recurring contracts and requiring vendors to demonstrate coverage across all eight municipalities.

Competitive Landscape

The top five providers, Mannai (CBMFM), Elegancia Facility Management, G4S Qatar, Sodexo Qatar and Khidmah, collectively held about 35%-40% of 2025 revenue, indicating moderate fragmentation. Technology adoption is the primary differentiator: CBMFM’s deployment of enterprise asset-management software secured the Qatar Foundation contract, while other leaders invest in drones, robotics and real-time dashboards to evidence KPI compliance.

Outcome-based commercial models are gaining ground, tying fees to energy savings and uptime. Vendors capable of underwriting performance risk report margins 15%-20% higher than time-and-materials contracts. Qatarization quotas are prompting investments in training academies and digital upskilling to elevate national participation in technical roles. Regional expansion remains a growth lever, with Elegancia leveraging its domestic track record to secure airport and healthcare contracts across the Middle East and Central Asia.

Price competition in commoditized cleaning and security continues to squeeze smaller local firms, accelerating consolidation. Simultaneously, ISO 55000 asset-management requirements are raising entry barriers, favoring providers with mature computerized systems and data-analytics capacity. The strategic landscape therefore balances cost-driven rivalry in soft services against capability-led differentiation in integrated, technology-rich offerings.

Qatar Facility Management Industry Leaders

Mannai Corporation QPSC

G4S Qatar WLL

Elegancia Facility Management (Estithmar Holdings QPSC)

Mosanda Facilities Management Services

Cayan Facility Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Elegancia Facility Management won a PPP contract to manage 14 schools, covering integrated hard and soft services and aligning with the government’s 45-school PPP program.

- September 2025: Ashghal awarded USD 3.3 billion across 13 contracts that include five-year AI-enabled operations and maintenance for roads and drainage.

- September 2025: KAHRAMAA released tender 4004/2025 for smart-building FM at its new Lusail tower, requiring ISO 55000-compliant CMMS deployment.

- September 2025: QatarEnergy issued tender GT25106100 for onshore and offshore catering, underscoring remote-site logistical complexity.

Qatar Facility Management Market Report Scope

The Qatari facility management market is defined based on the revenues generated from services used in various end-user applications across the country. Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. Hard services include physical and structural services like fire alarm systems and lifts, among others. Soft services include cleaning, landscaping, security, and similar human-sourced services, providing solutions to end-user industries.

The Qatar Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the projected value of the Qatar facility management market by 2031?

It is forecast to reach USD 16.03 billion by 2031 under a 12.29% CAGR.

Which service type currently leads spending in Qatari facilities?

Hard Services led with 58.92% revenue share in 2025 thanks to MEP, HVAC, and fire-safety work.

Which end-user group is expanding the fastest in facility management demand?

Industrial and Process facilities are expected to grow at a 12.47% CAGR through 2031, outpacing all other sectors.

How significant are outsourced delivery models in Qatar?

Outsourced contracts held 62.87% of 2025 revenue and remain the dominant service model.

What key regulation is shaping the FM labor market?

Law No. 12 of 2024 imposes a 10% Qatarization quota for firms with at least 50 employees.

Why are smart-city districts important for FM providers?

Projects such as Lusail and Msheireb embed district-wide IoT and BMS platforms, creating premium opportunities for technology-driven facility managers.

Page last updated on: