Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

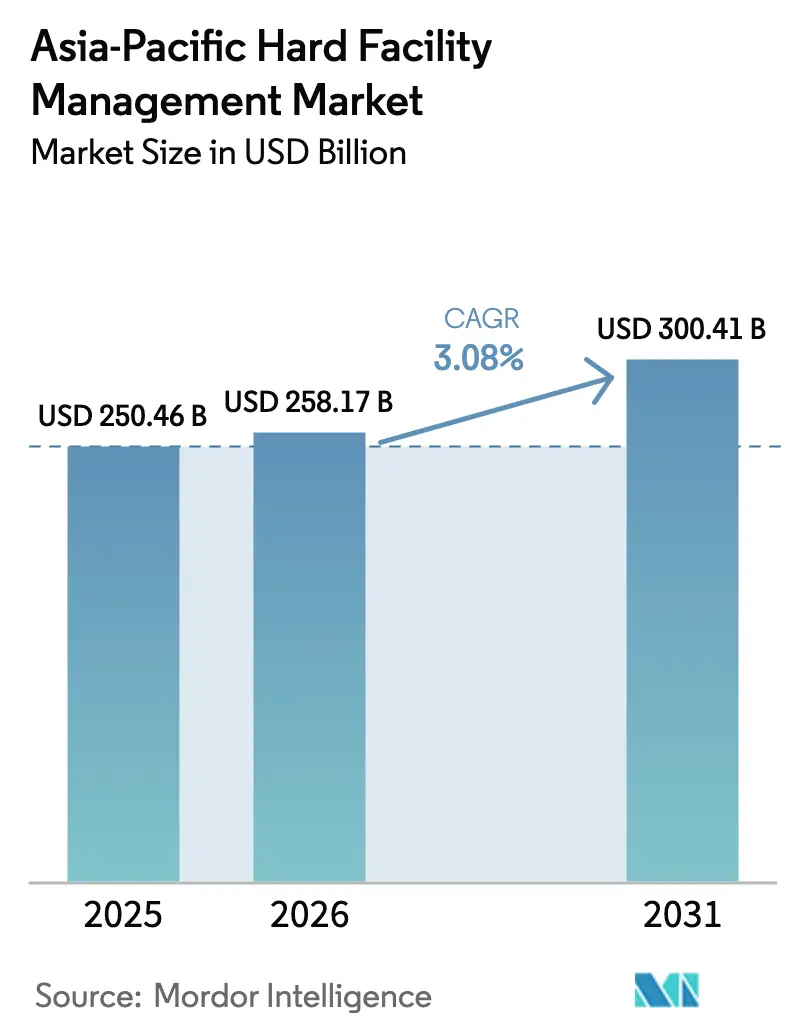

| Base Year Market Size (2025) | USD 250.46 Billion |

| Market Size (2026) | USD 258.17 Billion |

| Market Size (2031) | USD 300.41 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

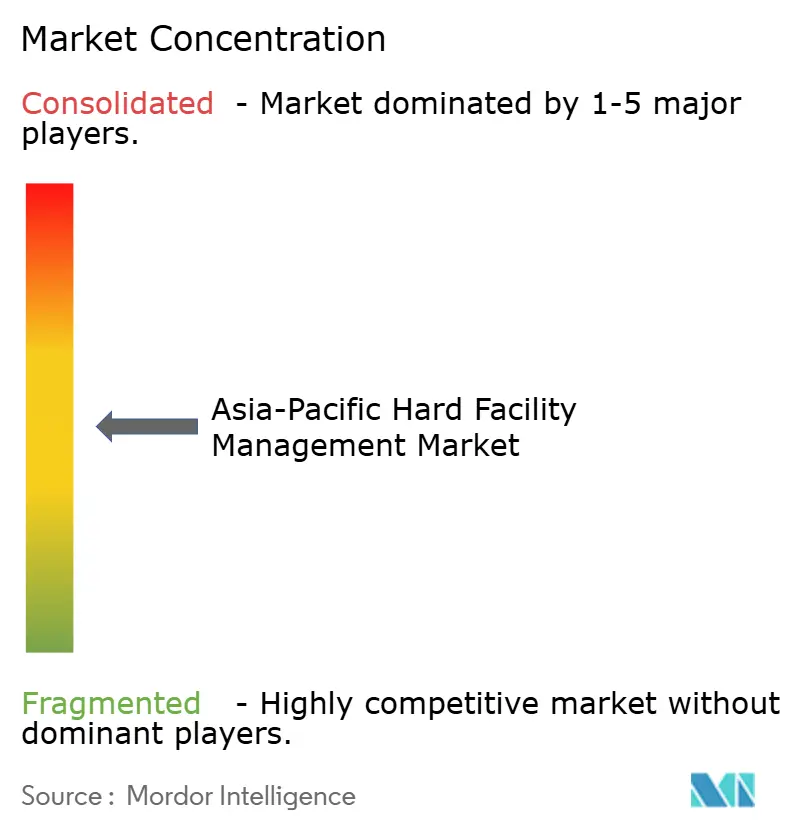

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Hard Facility Management Market Analysis by Mordor Intelligence

The Asia-Pacific hard facility management market size is expected to grow from USD 250.46 billion in 2025 to USD 258.17 billion in 2026 and is forecast to reach USD 300.41 billion by 2031 at 3.08% CAGR over 2026-2031. Growth is steady rather than spectacular, yet the shift in spending priorities is clear. Budgets are tilting toward energy-management programs, data-center uptime, and microgrid oversight as multinational tenants chase net-zero targets. At the same time, legacy HVAC upkeep remains the single largest service line because tropical climates drive year-round cooling demand. A construction boom in China’s tier-2 cities and industrial corridors across Vietnam and India is widening the installed base that must be serviced, although grid-capacity delays in Singapore and Malaysia are compressing provider margins.[1]CBRE Research, “Data Center Trends Asia Pacific 2024,” CBRE.com

Key Report Takeaways

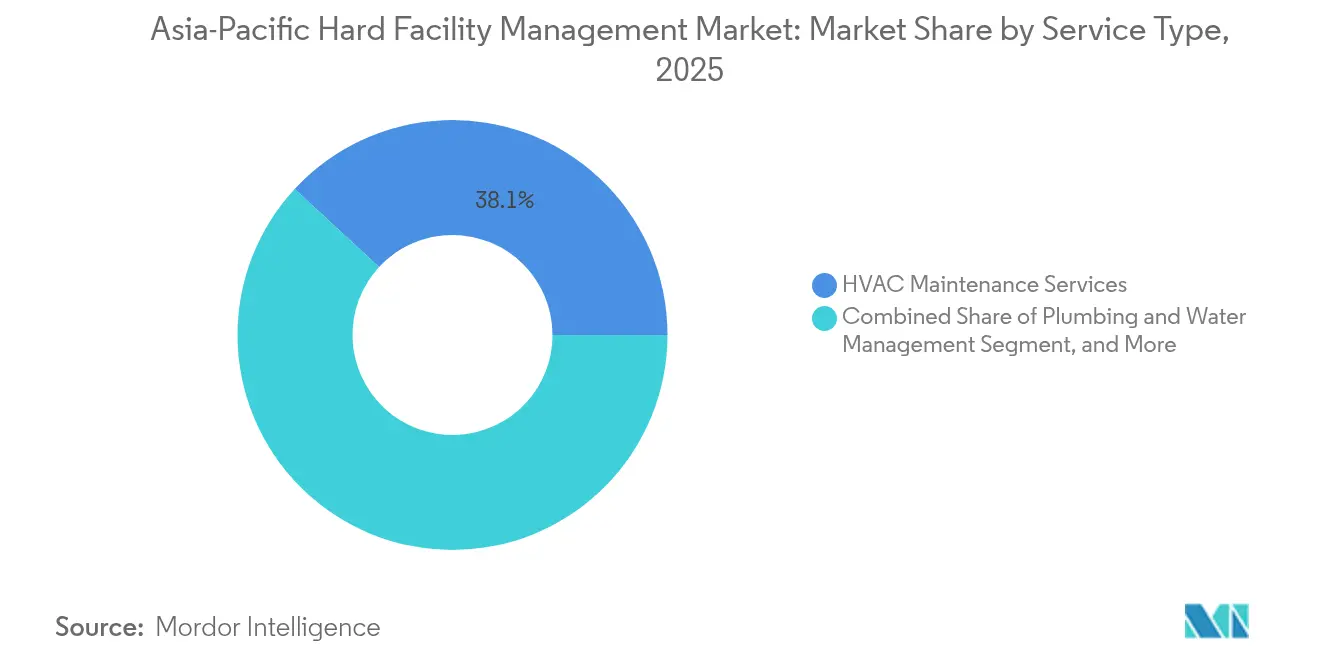

- By service type, HVAC maintenance held 38.12% of the Asia-Pacific hard facility management market share in 2025, while energy management and power systems is on course for the fastest 3.83% CAGR through 2031.

- By end user, commercial facilities led spending with 46.05% of the Asia-Pacific hard facility management market share in 2025, industrial and manufacturing is forecast to expand at a 4.18% CAGR to 2031.

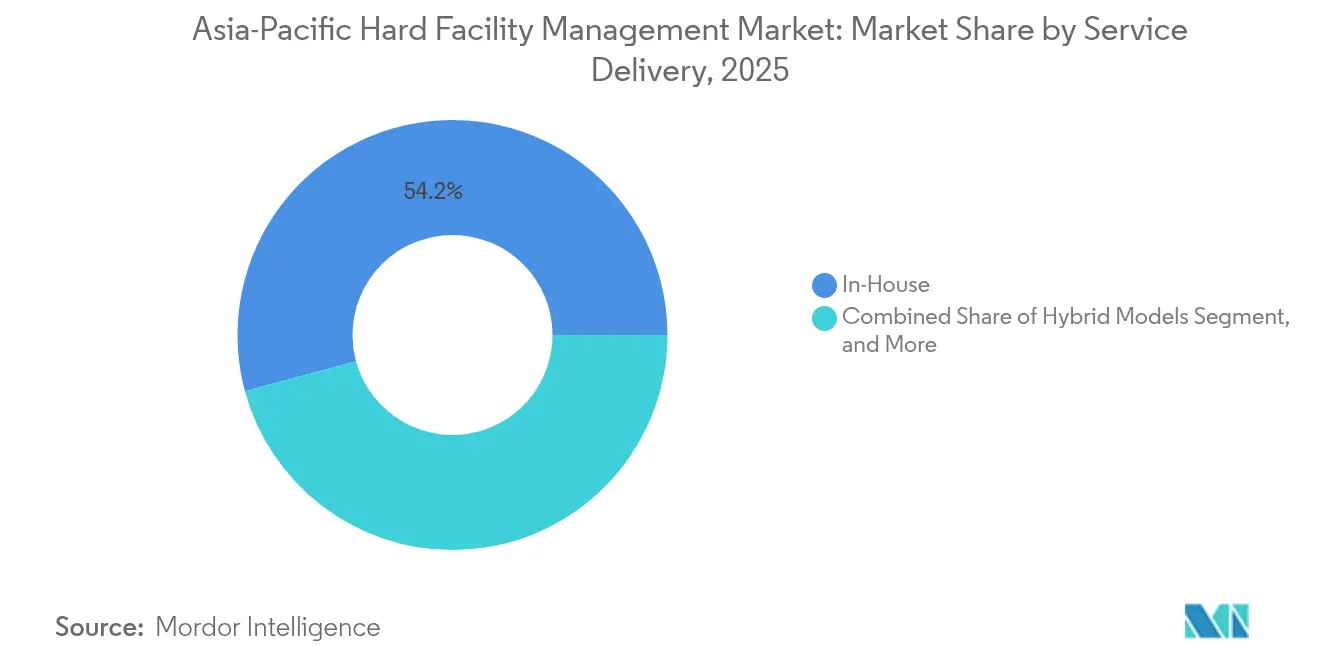

- By service-delivery model, in-house execution retained 54.21% of the Asia-Pacific hard facility management market share in 2025, whereas integrated facilities management contracts are growing at a 4.41% CAGR through 2031.

- By facility type, office and corporate campuses captured 40.02% of the Asia-Pacific hard facility management market share in 2025, yet data centers and critical environments are rising fastest at a 4.17% CAGR through 2031.

- By country, China commanded a dominant 36.35% share of the Asia-Pacific hard facility management market in 2025, whereas India is anticipated to register the fastest growth during the forecast period at a 4.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Hard Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of commercial and industrial construction activity | +0.8% | China, India, Vietnam, Indonesia, with spillover to Malaysia and Thailand | Medium term (2-4 years) |

| Rising demand for HVAC and MEP maintenance services | +0.7% | Tropical Asia-Pacific (Singapore, Malaysia, Indonesia, Thailand), urban China and India | Short term (≤ 2 years) |

| Outsourcing shift toward integrated FM contracts | +0.6% | Australia, Singapore, Japan, multinational-occupied facilities across Asia-Pacific | Medium term (2-4 years) |

| Energy-efficiency and green-building regulation push | +0.5% | Singapore, Hong Kong, Australia, Japan, with emerging adoption in China tier-1 cities | Long term (≥ 4 years) |

| Hyperscale data-centre build-out driving critical FM needs | +0.4% | Singapore, Japan, India, Australia, China (tier-2 cities), Indonesia (Jakarta, Batam) | Short term (≤ 2 years) |

| Corporate on-site renewable targets and micro-grid upkeep | +0.3% | Global, with early concentration in Australia, Japan, India, and Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Commercial and Industrial Construction Activity

Emerging industrial corridors are reshaping the Asia-Pacific hard facility management market. Commercial square footage in China’s tier-2 cities increased 18% in 2024, and Vietnam, Indonesia, and Thailand attracted USD 42 billion of manufacturing FDI the same year.[2]ASEAN Secretariat, “ASEAN Investment Report 2024,” ASEAN.org Developers often bundle three-year mechanical and electrical maintenance into turnkey packages, shortening the bid cycle and favoring integrators with pre-negotiated supplier networks. Providers are opening satellite depots in Chengdu, Pune, and Hanoi so they can meet service-level agreements within four hours. The result is a geographic realignment that rewards firms with regional logistics planning and local permitting expertise. Those unable to migrate beyond legacy urban cores risk missing a wave of opportunity that could define revenue pools for the rest of the decade.

Rising Demand for HVAC and MEP Maintenance Services

HVAC upkeep remains a key driver of the Asia-Pacific hard facility management market, as tropical humidity and dense urbanization increase cooling loads. Yet demand is becoming more technical than routine. Singapore’s district-cooling systems now require continuous refrigerant-leak detection and remote telemetry, which legacy preventive schedules cannot address. Malaysia’s chiller retrofits come with energy-savings guarantees that shift risk to service vendors. IoT-enabled diagnostics are normalizing forty-eight-hour fault remediation windows, so providers must invest in analytics talent and spare-parts inventory. Without that capability, mid-tier contractors lose premium accounts to firms that can underwrite performance.

Outsourcing Shift Toward Integrated FM Contracts

A broad outsourcing cycle is underway as multinationals consolidate vendor rosters and seek real-time data. Australian corporates led the trend; double-digit IFM contract wins at JLL and CBRE in 2024 flowed from unified dashboards that merge energy, work-order, and asset-life information. Singapore’s public agencies followed by stipulating software interoperability in tender documents. Platforms like Johnson Controls OpenBlue or Siemens Desigo CC are becoming table stakes. Entrance barriers are climbing because the capital and licensing costs of digital infrastructure outstrip the resources of smaller regional players. Consolidation is therefore likely to accelerate, compressing a fragmented supplier base into a hierarchy of scale.

Energy-Efficiency and Green-Building Regulation Push

Regulators have moved from voluntary labels to mandatory performance floors. Singapore’s Minimum Energy Performance Initiative requires a 10% reduction in energy intensity by 2030, with enforcement commencing in 2024.[3]Building and Construction Authority, “Minimum Energy Performance Initiative,” BCA.gov.sg Hong Kong raised building-efficiency standards 20% the same year. Malaysia’s 2024 Energy Efficiency and Conservation Act imposes annual reporting on large facilities. Compliance requirements have lifted demand for sub-metering, façade insulation, and HVAC recommissioning. Providers with in-house energy engineers are sealing multi-site deals that span beyond five years, as landlords prefer turnkey performance contracts over piecemeal upgrades. Smaller contractors risk being relegated to low-margin subcontracting roles if they cannot verify the savings that regulators and owners now expect.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled technical-labour shortage | -0.5% | Japan, Australia, Singapore, with emerging pressure in Malaysia and Thailand | Short term (≤ 2 years) |

| Volatile energy and materials costs squeezing margins | -0.4% | Global, with acute impact in import-dependent markets (Singapore, Hong Kong, Philippines) | Short term (≤ 2 years) |

| Fragmented Asia-Pacific compliance and certification landscape | -0.2% | Region-wide, most pronounced in cross-border contract execution | Medium term (2-4 years) |

| Grid-capacity shortfalls delaying facility handovers | -0.3% | Singapore, Malaysia (Johor), India (select states), Indonesia (Java grid) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Technical-Labor Shortage

Labor scarcity is the most immediate brake on the Asia-Pacific hard facility management market. Singapore reported a 12% deficit of certified HVAC engineers in 2024. Australian electricians experienced 15% wage inflation, while Malaysia’s construction sector faced a 15% headcount shortfall. Large integrators responded by opening training academies; ISS targets 500 graduates a year through its newly launched Southeast Asia center. Smaller companies lack the scale to replicate that model, so staff attrition funnels talent toward higher-paying data-center posts. The skills gap raises service costs and threatens SLA compliance, pushing buyers to favor vendors with formal workforce pipelines.

Grid-Capacity Shortfalls Delaying Facility Handovers

Power infrastructure lag is rippling through project timelines. Singapore capped new data-center connections in 2024 pending substation upgrades. Malaysia’s Tenaga Nasional Berhad delayed energization of Johor industrial parks, and Indian distribution companies postponed last-mile commissioning in several states. These bottlenecks stall construction close-outs and defer the start of maintenance revenue. FM firms now prequalify prospects based on power availability status and include escalation clauses that cover idled labor. Some are installing interim microgrids, allowing developers to test systems before full grid hookup; however, the added capital burden favors well-capitalized integrators over cash-constrained local contractors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Energy Management Extends Its Lead

Asia-Pacific hard facility management market size for energy management and power systems is poised to reach a significant value, advancing at a 3.83% CAGR, well ahead of legacy HVAC services. Energy-management contracts increasingly include on-site renewables, battery storage, and digital twins that predict load variance. Buyers value verified savings, so vendors who can bundle metering, analytics, and performance guarantees command premium prices. In contrast, HVAC maintenance, although still holding 38.12% of the Asia-Pacific hard facility management market share in 2025, faces slower growth because much of the installed base is aging equipment awaiting phased replacement. Mechanical and electrical maintenance will remain foundational, yet commoditization is likely as IoT sensors reduce the need for routine inspections. Fire and life-safety system upkeep is gaining regulatory tailwinds, while plumbing services climb the agenda in water-stressed geographies..

Routine tasks, such as filter changes, are migrating toward outcome-based pricing, rewarding firms that invest in remote-monitoring hardware. Johnson Controls recorded a 25% jump in Asia-Pacific bookings for performance-guaranteed contracts in 2024, illustrating the link between financial innovation and market capture. Providers that cannot underwrite energy savings will cede ground to platforms with stronger balance sheets. The battle lines are therefore drawn between scale-driven integrators and niche experts who master high-value micro-segments like liquid cooling or greywater recycling.

By End User: Industrial Growth Reconfigures Portfolio Mix

Industrial and manufacturing customers are poised to add notable value through incremental spending, growing at a 4.18% CAGR as supply-chain diversification prompts factories to relocate to Vietnam, Indonesia, and India. Semiconductor fabs and pharma plants require cleanroom HVAC, ultra-pure water, and redundant power, lifting per-square-meter revenue well above that of office towers. In 2025, commercial buildings still accounted for 46.05% of outlays; however, their expansion rate lags behind because saturated CBDs and hybrid work arrangements temper new space demand. Healthcare and education budgets are rising as governments fund hospital refurbishments and research campuses, a trend that insulates cash flows from economic cycles.

Residential complexes remain largely in-house managed, though luxury towers in Singapore and Sydney are trialing predictive-maintenance outsourcing to differentiate amenities. For FM providers, industrial diversification creates a need for regional dispatch hubs, spare parts logistics, and specialized certifications. Those who invested early in local technician training and OEM partnerships are winning multi-year contracts at higher margins. Late movers face a steep learning curve and risk being locked out of complex industrial niches.

By Service Delivery Model: IFM Wins Wallet Share

Integrated contracts are capturing wallet share as clients chase single-pane dashboards and predictive analytics. The Asia-Pacific hard facility management market is tilting toward IFM because platforms unify mechanical, electrical, cleaning, and security services under performance metrics that link directly to building life-cycle cost. In-house teams still dominate at 54.21% share, but their cost advantage erodes when technology investment is required. Hybrid-oversight models are emerging in Japan and Australia where institutional knowledge remains valuable but digital skills are scarce.

OpenBlue, Desigo CC, and Honeywell Forge serve as the digital backbone that enables monthly asset health reports and energy-variance alerts. Contracts increasingly include KPI penalties, so providers that cannot offer real-time data lose negotiating power. Smaller regional players often subcontract under the umbrella of an integrator, compressing their margin and brand visibility. The direction of travel is clear: scale, data, and capital determine competitive durability.

By Facility Type: Data Centers Raise the Technical Bar

Data centers and critical environments deliver the highest revenue per square foot in the Asia-Pacific hard facility management market because 99.99% uptime is non-negotiable. Power density in AI racks surpassed 20 kW in 2024, accelerating the shift to liquid cooling that requires unfamiliar maintenance protocols. Office campuses still hold a 40.02% spending share, but hybrid work and tenant downsizing are moderating new contract values. Industrial logistics parks, especially cold-chain warehouses, create steady work for precision HVAC teams, while airports and seaports secure long-term contracts but require security clearances that often favor incumbents.

Hospitals grant stable margins due to regulatory audits of infection-control systems, although negotiating cycles can be protracted. Hospitality properties remain price sensitive, prioritizing guest-facing investments over back-of-house upgrades. The key takeaway is that technical depth, not footprint size, drives profitability. Firms that can certify liquid-cooling engineers or cleanroom technicians secure an outsized share in the fastest-growing facility segments.

Geography Analysis

China remains the largest slice of the Asia-Pacific hard facility management market, propelled by commercial completions in Chengdu, Wuhan, and Chongqing. Multinationals often partner with state-owned enterprises to navigate local procurement rules, which limits direct exposure but provides volume. Japan follows, characterized by aging assets that need seismic retrofitting and energy-efficiency upgrades. Labor scarcity there raises wage costs and speeds up automation adoption.

India is moving quickly as FDI lands in Gujarat, Maharashtra, and Tamil Nadu. However, fragmented state regulations and uneven power reliability force providers to maintain decentralized depots. Singapore is a mature and competitive market; power-supply caps now prompt hyperscalers to relocate to Johor in Malaysia, creating cross-border service corridors. Australia leads the uptake of IFM, driven by corporate demand for transparency and tied to the broader renewable energy push.

Indonesia benefits from redirected data-center investment but faces grid constraints that require backup-generation strategies. South Korea’s tech giants embed proprietary building management systems that require API interoperability. Taiwan’s semiconductor fabs command premium maintenance prices due to cleanroom stipulations. Thailand’s automotive supply chain lifts industrial volumes, and tourism rebound supports hospitality budgets. Smaller markets such as Vietnam and the Philippines see sharp growth from low bases, though contractor ecosystems remain thin. The geographic picture is bifurcated: advanced economies seek digital twins and carbon accounting, while developing markets value cost efficiency and quick mobilization.

Competitive Landscape

Regional revenue is still fragmented as the top ten providers hold roughly 35% to 40% share, leaving the remainder to hundreds of local or single-trade firms. Global integrators leverage brand equity, proprietary platforms, and multinational-client portfolios to secure multi-site contracts. Yet regional specialists defend their share through lower overhead, flexible staffing, and faster permitting. Technology is the biggest separator. Johnson Controls OpenBlue, Siemens Desigo CC, and Honeywell Forge drive predictive maintenance and energy optimization that resonate with finance chiefs focused on controlling operating expenses.

Secondary cities such as Pune, Chengdu, and Hanoi represent white-space territory where demand outstrips qualified supply. ISS acquired three Southeast Asian firms in 2024 to capitalize on this tailwind, and other integrators are expected to follow suit. ISO 14001 and ISO 50001 certifications appear more frequently in tenders, increasing compliance costs and squeezing thin-capitalized players. The Asia-Pacific hard facility management industry, therefore, trends toward a barbell structure: large, digital-native integrators servicing multinational and institutional accounts on one end, and agile local specialists handling single-service domestic contracts on the other. Mid-tier providers with partial scale but limited technology look vulnerable to consolidation or exit.

Competition is also intensifying in niche segments. Liquid-cooling maintenance, microgrid management, and cleanroom services carry high technical entry barriers and premium margins. Early movers who secure OEM training and parts access lock in advantage. Late entrants face steep certification costs and low initial volumes, making organic entry difficult. Partnerships between software-only firms and execution partners are emerging as a workaround, though the jury is out on whether clients will accept split accountability.

Asia-Pacific Hard Facility Management Industry Leaders

Jones Lang LaSalle Incorporated (JLL)

Sodexo S.A.

CBRE Group Inc

Johnson Controls International

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: CBRE Group acquired a Jakarta-based facilities-services firm specializing in critical-environment maintenance, adding 1,000 employees and expanding its Indonesian data-center and manufacturing-site coverage to meet rising hyperscale demand.

- August 2025: Johnson Controls International signed a 10-year energy-performance agreement with a Singapore retail-mall portfolio totaling 1.2 million sq ft, bundling chillers, lighting, and microgrid management with minimum 15% annual energy-savings guarantees.

- April 2025: ISS A/S opened a technical-training academy in Ho Chi Minh City aimed at graduating 600 certified HVAC and electrical technicians annually to alleviate regional labor shortages and support upcoming data-center contracts.

- February 2025: Siemens AG secured a 10-year contract to deploy its Desigo CC platform across 50 commercial towers in Tokyo, covering HVAC analytics, fault detection, and energy-use-intensity guarantees tied to Japan’s 2030 carbon-reduction goals.

Asia-Pacific Hard Facility Management Market Report Scope

The Asia-Pacific hard facility management market report is segmented by Service Type (Mechanical Services Maintenance, Electrical Services Maintenance, HVAC Maintenance Services, Fire and Life-Safety Systems Maintenance, Plumbing and Water Management, Building Fabric and Structural Maintenance, Energy Management and Power Systems), End User (Commercial, Institutional, Public/Infrastructure, Industrial and Manufacturing, Residential and Mixed-Use), Service Delivery Model (In-House, Outsourced Single-Service, Integrated Facilities Management, Hybrid Models), Facility Type (Office and Corporate Campuses, Industrial and Logistics Facilities, Data Centres and Critical Environments, Healthcare Facilities, Hospitality and Leisure Properties, Transportation Hubs and Infrastructure), and Country (Australia, China, India, Japan, Indonesia, Malaysia, Singapore, South Korea, Taiwan, Thailand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Mechanical Services Maintenance |

| Electrical Services Maintenance |

| HVAC Maintenance Services |

| Fire and Life-Safety Systems Maintenance |

| Plumbing and Water Management |

| Building Fabric and Structural Maintenance |

| Energy Management and Power Systems |

By End User

| Commercial |

| Institutional (Education and Healthcare) |

| Public / Infrastructure |

| Industrial and Manufacturing |

| Residential and Mixed-Use |

By Service Delivery Model

| In-House (Self-Performed) |

| Outsourced Single-Service |

| Integrated Facilities Management (IFM) |

| Hybrid Models |

By Facility Type

| Office and Corporate Campuses |

| Industrial and Logistics Facilities |

| Data Centres and Critical Environments |

| Healthcare Facilities |

| Hospitality and Leisure Properties |

| Transportation Hubs and Infrastructure |

By Country

| Australia |

| China |

| India |

| Japan |

| Indonesia |

| Malaysia |

| Singapore |

| South Korea |

| Taiwan |

| Thailand |

| Rest of Asia-Pacific |

| By Service Type | Mechanical Services Maintenance |

| Electrical Services Maintenance | |

| HVAC Maintenance Services | |

| Fire and Life-Safety Systems Maintenance | |

| Plumbing and Water Management | |

| Building Fabric and Structural Maintenance | |

| Energy Management and Power Systems | |

| By End User | Commercial |

| Institutional (Education and Healthcare) | |

| Public / Infrastructure | |

| Industrial and Manufacturing | |

| Residential and Mixed-Use | |

| By Service Delivery Model | In-House (Self-Performed) |

| Outsourced Single-Service | |

| Integrated Facilities Management (IFM) | |

| Hybrid Models | |

| By Facility Type | Office and Corporate Campuses |

| Industrial and Logistics Facilities | |

| Data Centres and Critical Environments | |

| Healthcare Facilities | |

| Hospitality and Leisure Properties | |

| Transportation Hubs and Infrastructure | |

| By Country | Australia |

| China | |

| India | |

| Japan | |

| Indonesia | |

| Malaysia | |

| Singapore | |

| South Korea | |

| Taiwan | |

| Thailand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the 2026 value of the Asia Pacific hard facility management market?

The market stands at USD 258.17 billion in 2026.

How fast is the sector expected to grow by 2031?

It is projected to reach USD 300.41 billion, reflecting a 3.08% CAGR.

Which service type is expanding fastest?

Energy management and power systems lead with a 3.83% CAGR through 2031.

Which end-user segment is growing quickest?

Industrial and manufacturing facilities are forecast to rise at a 4.18% CAGR.

Why are integrated FM contracts gaining traction?

Multinationals prefer single-vendor accountability and data-rich platforms that enable predictive maintenance and cost transparency.

Page last updated on: