Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

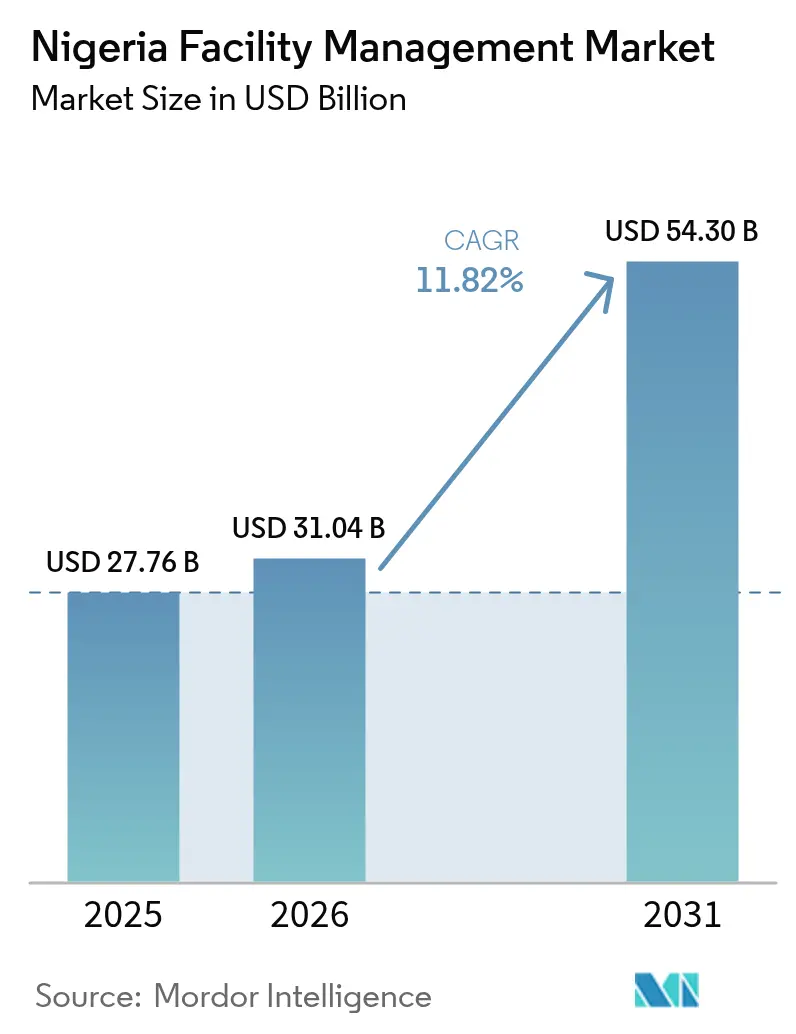

| Base Year Market Size (2025) | USD 27.76 Billion |

| Market Size (2026) | USD 31.04 Billion |

| Market Size (2031) | USD 54.3 Billion |

| Growth Rate (2026 - 2031) | 11.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Facility Management Market Analysis by Mordor Intelligence

The Nigeria facility management market size was valued at USD 27.76 billion in 2025 and estimated to grow from USD 31.04 billion in 2026 to reach USD 54.3 billion by 2031, at a CAGR of 11.82% during the forecast period (2026-2031). Rapid urban expansion in Lagos, Abuja and Port Harcourt, mounting infrastructure investments such as the USD 20 billion Ogidigben Gas Revolution Industrial Park, and investor insistence on ISO 41001-aligned ESG programs continue to pull demand upward. Power-grid unreliability—averaging 32 monthly outages—pushes clients toward service providers that can integrate renewable generation, IoT-based energy monitoring, and predictive maintenance into a single offering. Lower IoT sensor prices—now below USD 5 per unit—plus nationwide 4G and emergent 5G coverage have slashed adoption barriers for smart-building systems that cut operating costs by 15-30%. Meanwhile, cement market concentration and the 2024 minimum-wage hike are intensifying cost pressures, encouraging a shift to outcome-based, integrated contracts that deliver measurable savings across energy, labour and materials.

Key Report Takeaways

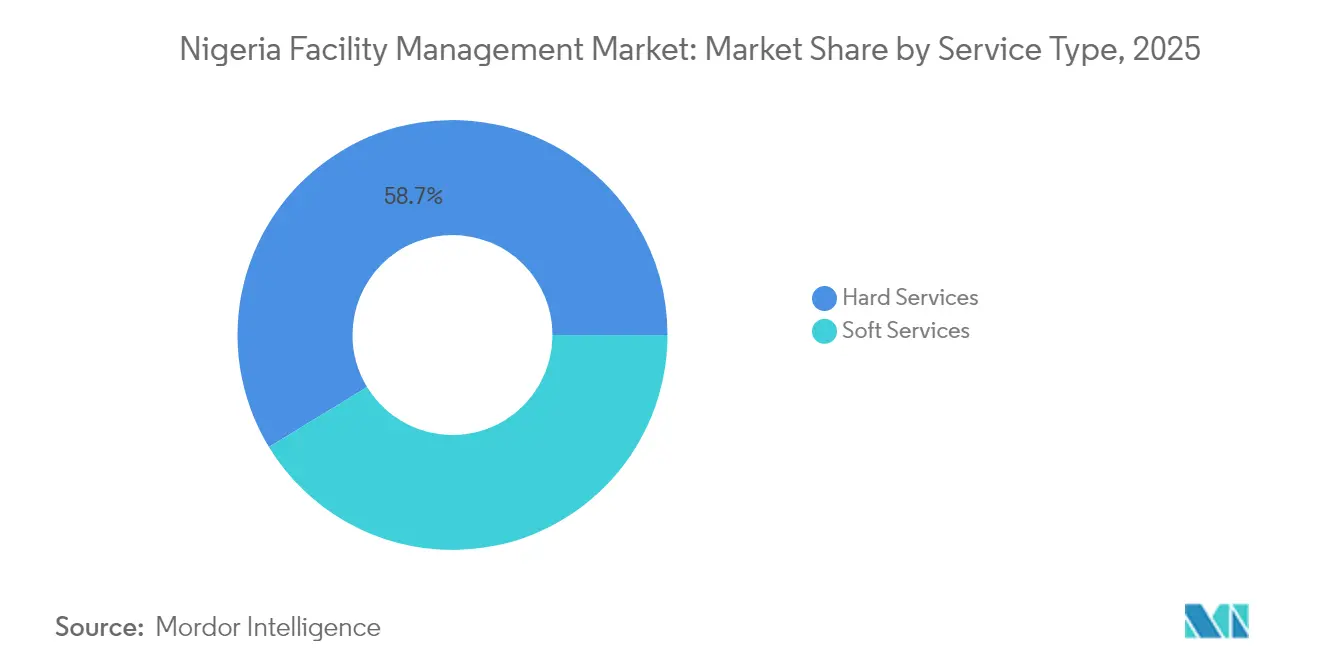

- By service type, hard services held 58.71% of the Nigeria facility management market share in 2025; soft services are on track to expand at a 13.02% CAGR through 2031.

- By offering, the outsourced model captured 66.02% share of the Nigeria facility management market size in 2025 and is projected to grow at a 13.86% CAGR between 2026-2031.

- By end-user, commercial facilities commanded 39.62% market share in 2025, while institutional and public-infrastructure properties are advancing at a 14.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and population growth | +2.1% | Lagos, Abuja, Port Harcourt with spillover to secondary cities | Medium term (2-4 years) |

| Infrastructure investment priorities | +1.8% | National, with concentration in Lagos-Abuja corridor | Long term (≥ 4 years) |

| Occupancy-rate fluctuations | +1.2% | Lagos Central Business District, Abuja Federal Capital Territory | Short term (≤ 2 years) |

| Labor and safety regulations | +0.9% | National, with stricter enforcement in Lagos and Abuja | Medium term (2-4 years) |

| Green-bond investors requiring ISO 41001-aligned ESG-compliant FM programs | +1.5% | Lagos, Abuja commercial districts | Long term (≥ 4 years) |

| Falling IoT sensor costs and nationwide 4G coverage | +2.2% | Urban centers with 4G infrastructure, expanding to tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanisation and Population Growth Drive Facility Demand

Urban Nigeria now houses nearly 120 million residents, with Lagos alone growing at 13.6% annually and generating 25% of national GDP.[1]African Cities Research Consortium, “Lagos: City Scoping Study,” african-cities.org By 2050, 70% of citizens will live in cities, fuelling long-term need for professional property upkeep across housing estates, commercial towers and mixed-use hubs. This demographic momentum pushes portfolio owners to outsource preventive maintenance, security and waste services to meet tenancy expectations despite electricity and water shortfalls. The Nigeria facility management market therefore captures recurring revenue streams from both brownfield retrofits and greenfield megaprojects that require cradle-to-grave asset support. Facility managers that pair community-level services—sanitation, lighting, public-space care—with digital dashboards are emerging as partners of choice for municipal authorities seeking cost-efficient urban management. Concurrently, state governments’ push to formalise informal settlements expands addressable stock for compliant providers as residents demand reliable water, lighting and waste solutions.

Infrastructure Investment Priorities Shape Market Opportunities

Flagship schemes such as the USD 20 billion Ogidigben Gas Revolution Industrial Park and the Abuja African Medical Centre of Excellence create direct, multi-decade O&M opportunities for hard-service contractors, energy specialists and soft-service vendors. Public-private-partnership models overseen by the Infrastructure Concession Regulatory Commission guarantee 20- to 30-year concession windows, anchoring predictable cashflows. Construction majors such as Julius Berger are vertically integrating into FM, leveraging their civil-works track records to secure whole-life service contracts on projects like the 48,400 m² NUPRC HQ in Abuja. The Nigeria facility management market therefore rewards firms that can bridge capital-project execution with lifecycle O&M, offering bundled MEP, energy and cleaning services under performance-linked SLAs.

Green-Bond Investors Mandate ESG-Compliant FM Programs

Green-bond issuances funding new offices and logistics parks now stipulate ISO 41001-aligned operations throughout the lease term. Buildings certifying to LEED or EDGE during construction must retain those credentials post-handover, shifting accountability to facility managers for energy, waste, water and occupant wellbeing metrics. Empirical work on Nigerian listed firms links higher ESG scores to stronger ROA and ROE, illustrating tangible financial upside for owners that partner with compliant FM providers.[2]Oyegunle-Esimaje, “ESG Score and Corporate Financial Performance,” preprints.org Consequently, Nigeria facility management market leaders embed renewable-energy microgrids, recycling programs and digital indoor-air-quality monitoring to help asset owners access lower-cost capital.

IoT Sensor Cost Reductions Enable Smart-Building Adoption

Sensors priced below USD 5 and rising 5G coverage—12.3 million expected connections by 2025—have moved predictive maintenance from luxury to baseline requirement.[3]GSMA Intelligence, “5G in Africa 2023,” gsma.com A typical 20-storey Lagos office deploying 1,200 LoRaWAN nodes can recover installation costs in 36 months via 18% electricity savings validated by Harold Brothers’ BMS benchmarks. Nigeria facility management market incumbents now bundle cloud analytics, energy meters and flexible workspace software to provide CFOs with live dashboards linking OPEX, occupancy and ESG metrics. This technology layer differentiates providers amid a fragmented field of informal vendors lacking data capability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Profitability squeeze among FM firms | -1.4% | National, with acute pressure in Lagos and Abuja | Short term (≤ 2 years) |

| Workforce participation and skills gap | -0.8% | National, with concentration in technical roles | Medium term (2-4 years) |

| National grid outages forcing 18-25% higher OPEX | -2.1% | National, with severe impact in manufacturing regions | Short term (≤ 2 years) |

| Large informal FM workforce offering cut-rate services | -1.2% | Urban centers, particularly Lagos informal settlements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Profitability Squeeze Among FM Firms

The 2024 minimum-wage increase to NGN 70,000 (USD 90.25) per month lifted direct labour costs by 133%, tightening margins on fixed-price FM contracts. Simultaneously, cement prices doubled to NGN 10,000 (USD 6.25) per 50 kg bag on Lagos retail shelves as Dangote, BUA and Lafarge—who jointly hold 100% clinker capacity—passed energy costs to downstream buyers. Facility managers reliant on civil-works and MEP spare-part inventories must now renegotiate annual escalators, pivot to outcome-based SLAs or integrate renewable microgrids that lower diesel spend by 25–35%. Capitalising on this transition, Nigeria facility management market leaders bundle energy-as-a-service with long-term material sourcing agreements to lock-in cost visibility.

National Grid Outages Force Higher OPEX

An academic comparison of grid versus generator costs shows a 3.9× price differential for a 20 kVA diesel set operating six hours daily, forcing facilities to budget NGN 157,095 (USD 98.18) each month solely for fuel. Compounded by 32 collapses of the transmission network every month, FM providers allocate up to one-quarter of contract value to backup power, undermining profitability and sustainability. Leading operators respond by installing rooftop PV arrays sized at 30 kWp for mid-rise offices, integrated with lithium-ion storage that provides three-hour autonomy and pays back in under five years when diesel is USD 1.60 per L. As a result, Nigeria facility management market buyers increasingly specify renewable-energy performance guarantees in bid documents, favouring firms that can model load curves and interconnectivity with distribution companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Dominance With Rapid Soft-Service Upswing

Hard services accounted for 58.71% of the Nigeria facility management market size in 2025 as power-system unreliability, water scarcity and safety regulations required continuous MEP, HVAC and fire-protection expertise. The segment’s depth ranges from 24/7 generator maintenance to corrosion control of structural steel in coastal zones. Within hard services, asset-management contracts exceed five years on average, reflecting owners’ need for lifecycle cost certainty. IoT-enabled vibration analytics, deployed on centrifugal chillers, detect faults seven days earlier than manual inspection, reducing unplanned downtime by 30%. Soft services, although smaller, are accelerating at 13.02% CAGR as multinationals outsource cleaning, catering and mailroom tasks to comply with stricter ESG and labour laws. A bank headquartered in Victoria Island cut overtime by 18% after migrating 41 roles to an integrated soft-service bundle, proving cost-effectiveness amid wage inflation.

Soft services are benefiting from Lagos State’s 2025 mandatory building-hygiene regime, which requires licensed providers to submit quarterly pathogen audits. Firms leveraging electrostatic-spray cleaning cut chemical spend 14% and achieve 25% quicker room-turn times in hospitality settings. These metrics underpin the Nigeria facility management market share shift toward providers integrating robotics for floor-care and AI chatbots for occupant-service requests. Over the forecast window, bundled solutions that unify technical, security and janitorial tasks under single governance structures are expected to capture another 5–7 percentage-points of contract awards.

By Offering Type: Outsourcing Secures Clear Leadership

Outsourced contracts controlled 66.02% of the Nigeria facility management market share in 2025 and are expanding at a 13.86% CAGR, reflecting organisations’ appetite for single-invoice, KPI-driven partnerships. Integrated Facility Management (IFM) grew fastest, buoyed by international corporates demanding regional alignment with global SLAs. IFM providers commit to 5-year tenures, achieving 8–12% OPEX cuts through vendor consolidation and data-driven asset strategies.

In-house management’s 33.98% share is projected to erode as regulatory complexity around fire, labour and environmental compliance rises. Small-and-medium landlords, previously reliant on informal caretakers, now face mandatory safety-file submissions and insurance audits. Outsourced specialists provide compliance matrices, continuous training and digital document vaults, eliminating penalties that can reach NGN 2 million per infringement. These factors underpin sustained migration toward external partners, keeping the Nigeria facility management industry strategically attractive for global entrants such as CBRE and ISS that import process discipline and scale procurement.

By End-User Industry: Commercial Reigns, Institutional Outpaces

Commercial buildings contributed 39.62% of 2025 revenue but institutional and public infrastructure facilities are projected to post a 14.79% CAGR through 2031, powered by health, education and transport modernisation programs. In the commercial segment, Nigeria facility management market size for Grade-A offices in Lagos CBD surpassed USD 1.91 billion in 2026 on the back of fit-out densification and co-working uptake. Retail malls are adopting destination-experience strategies, outsourcing guest-services and event-management to FM providers to keep footfall resilient against e-commerce headwinds. Public-sector contracts show rising professionalism as ministries adopt UK-style NEC4 service agreements that allocate risk through KPIs. Transport-hub facilities—rail, airport and BRT depots—now demand crowd-flow analytics and anti-tamper surveillance as security becomes paramount. Meanwhile, manufacturing plants in the Niger Delta apply integrated safety, environmental and asset-care programs to satisfy both local regulators and overseas financiers. These cross-sector shifts affirm the Nigeria facility management market’s trajectory toward complex, outcome-linked engagements rather than commodity manpower supply.

Geography Analysis

Lagos State remains the linchpin of the Nigeria facility management market, representing more than one-third of national spending due to its 12 million urban residents and concentration of Grade-A offices. The city hosts 410,000 m² of premium workspace—71% of national supply—and depends on advanced HVAC, lift and security systems that require continuous monitoring to offset 32 average grid failures per month. Abuja’s share is expanding as state-backed office complexes adopt IFM contracts to guarantee uptime for policymaking and diplomatic missions. Facilities such as the 48,400 m² NUPRC headquarters employ digital command centres that link access control, energy dashboards and predictive MEP maintenance under single governance, reducing unplanned downtime by 27% year-over-year.

Port Harcourt and the wider Niger Delta present high-value, specialised demand profiles. Oil-and-gas processing facilities contract FM firms for hazardous-area maintenance, flare-stack inspections and corrosion-monitoring programs. Providers that combine ATEX-certified technicians with IoT sensors secure multi-year deals that carry above-market margins. The Nigeria facility management market size for industrial sites in Rivers State exceeded USD 916 million in 2026, despite security premiums embedded in guard-force contracts. Parallelly, Kano, Kaduna and Ibadan illustrate frontier growth where commercial real estate and light-manufacturing clusters leverage expanding 4G backbone to onboard remote BMS and workforce-management apps. National broadband coverage—94% 4G and 11% 5G as of Q1 2025—creates ubiquity for cloud-based FM platforms, permitting Lagos-based command centres to manage buildings in Kebbi or Calabar with identical SLA sophistication. As transport corridors such as the Lagos-Calabar Coastal Highway unlock new logistics parks, early mover FM firms are embedding design-for-maintenance principles before ground-breaking, securing annuity streams at reduced competitive intensity. Over the forecast horizon, regional diversification suggests the Nigeria facility management market will shift from its current coastal concentration toward an evenly distributed national footprint.

Competitive Landscape

The market remains moderately fragmented: the top five formal players hold roughly 35-40% revenue, while more than 500 informal micro-providers service single sites. Global majors CBRE, ISS and Knight Frank extend process rigour, technology toolkits and ESG audit know-how, whereas indigenous leaders Alpha Mead and UPDC FM provide cultural proximity and cost-adapted solutions. Julius Berger’s FM division leverages EPC heritage to win lifecycle deals in government and oil-&-gas segments, often bundling civil alterations with preventive maintenance. CBRE’s 2025 integration of Turner & Townsend created a USD 3 billion project and facility management arm that offers Nigerian clients unified design-build-operate pathways.

Strategic plays revolve around technology. ISS assigns site teams handheld apps for real-time work-order tracking; this delivered a 16% productivity jump on a six-site pilot in Lagos. Alpha Mead recently unveiled an IoT platform co-developed with a local telco, enabling property owners to view generator load factors and diesel stock levels via mobile dashboard, preventing fuel-theft shrinkage. Commercial bundling is rising: a 2025 tender by a pan-African bank awarded IFM plus co-working fit-out services in a single 10-year contract—illustrating convergence of property, workplace and energy management scopes.

Price competition remains intense at the low-complexity end, where informal providers undercut by 25–30% but lack compliance assurance. Formal operators counter through value-engineering, offering performance-based energy savings that neutralise headline-price gaps within two years. ESG reporting competency is now a decisive bid criterion, leading CBRE and ISS to publish Nigeria-specific sustainability indices in 2025 tenders. Given these dynamics, the Nigeria facility management industry exhibits accelerating consolidation via M&A and strategic alliances, with scale players targeting a 50% share of formal revenue by 2030.

Nigeria Facility Management Industry Leaders

Total Facilities Management Limited

Global PFI Limited

Broll Property Group

Greenkey Facility Management Services

Solid Rock Facility Management Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: African Medical Centre of Excellence confirmed civil-works completion ahead of its June 2025 launch, signaling imminent FM mobilisation.

- January 2025: Alpha GRIP Management secured USD 20 billion financing for Ogidigben Gas Revolution Industrial Park, paving the way for multi-site FM contracts in Delta State.

- January 2025: CBRE agreed to acquire Industrious National Management Company, adding flexible-workspace services that meld with integrated FM offerings.

- January 2025: CBRE Group closed the Turner & Townsend combination, creating a USD 3 billion infrastructure and FM platform with enhanced capability in Nigerian public-sector projects.

Nigeria Facility Management Market Report Scope

Facility management refers to a set of services or tools that helps organizations reduce maintenance costs and ensure the well-being of employees. By addressing many of its immediate and long-term needs, these services add value to a business. The report provides an extensive analysis of the trends and dynamics of the Nigerian facility management services market.

The Nigeria facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-User Industry

| Commercial (IT and Telecom, Retail, Warehousing) |

| Hospitality (Hotels, Restaurants) |

| Institutional and Public Infrastructure (Govt, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, OandG, Mining) |

| Other End-user Industries (Multi-house Residential, Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-User Industry | Commercial (IT and Telecom, Retail, Warehousing) | |

| Hospitality (Hotels, Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, OandG, Mining) | ||

| Other End-user Industries (Multi-house Residential, Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Nigeria facility management market?

The market is valued at USD 31.04 billion in 2026 and is forecast to reach USD 54.3 billion by 2031, implying a 11.82% CAGR.

Which service segment dominates the market?

Hard services hold 58.71% share, largely due to persistent infrastructure gaps and the need for technical solutions such as MEP and power-backup maintenance.

Why are outsourced models gaining ground?

Organisations increasingly prefer integrated, KPI-driven contracts that transfer compliance and operational complexity to specialised providers, pushing outsourced penetration to 66.02% in 2025.

How do power outages influence facility management costs?

Grid unreliability forces facility managers to budget 18–25% higher OPEX for generators and fuel, spurring interest in solar-plus-storage microgrids that trim diesel consumption by up to 35%.

What role does ESG play in Nigeria’s facility management contracts?

Green-bond investors and new building codes require ISO 41001-aligned operations, prompting FM firms to integrate energy-efficiency, waste-reduction and worker-safety programs to secure long-term deals.

Which regions outside Lagos are emerging for facility management growth?

Abuja’s government district, Port Harcourt’s oil-and-gas corridor and secondary cities like Kano and Ibadan are expanding rapidly due to infrastructure investments and growing commercial real-estate stock.

Page last updated on: