Telecom Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 6.86 Billion |

| Growth Rate (2026 - 2031) | 11.25% CAGR |

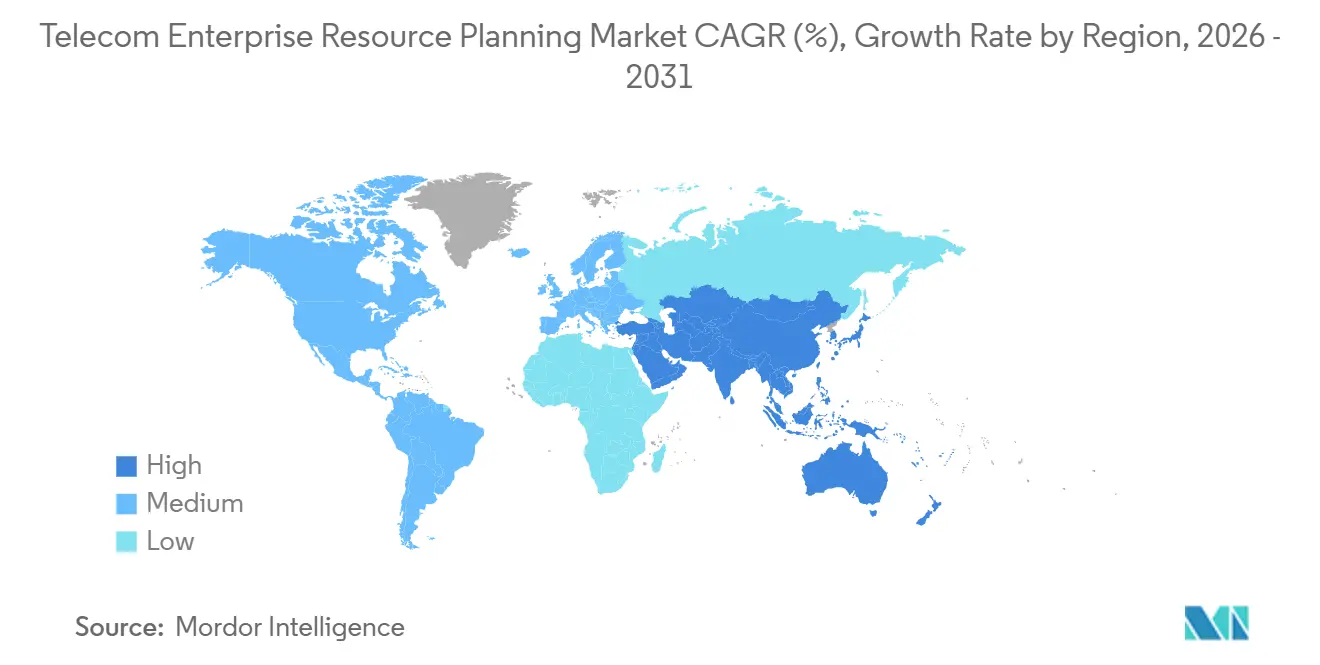

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

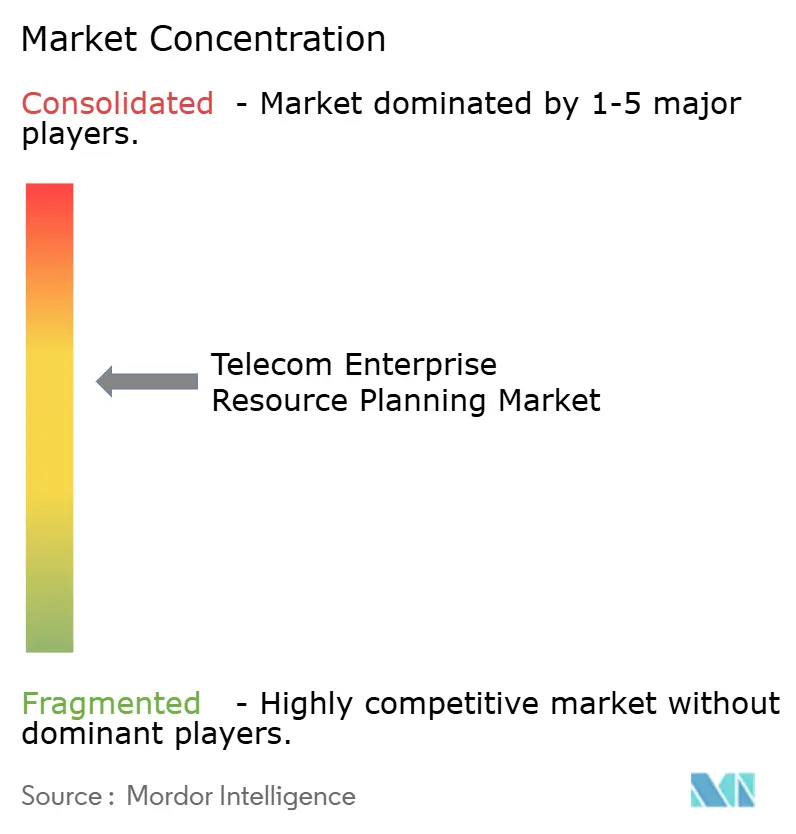

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Enterprise Resource Planning Market Analysis by Mordor Intelligence

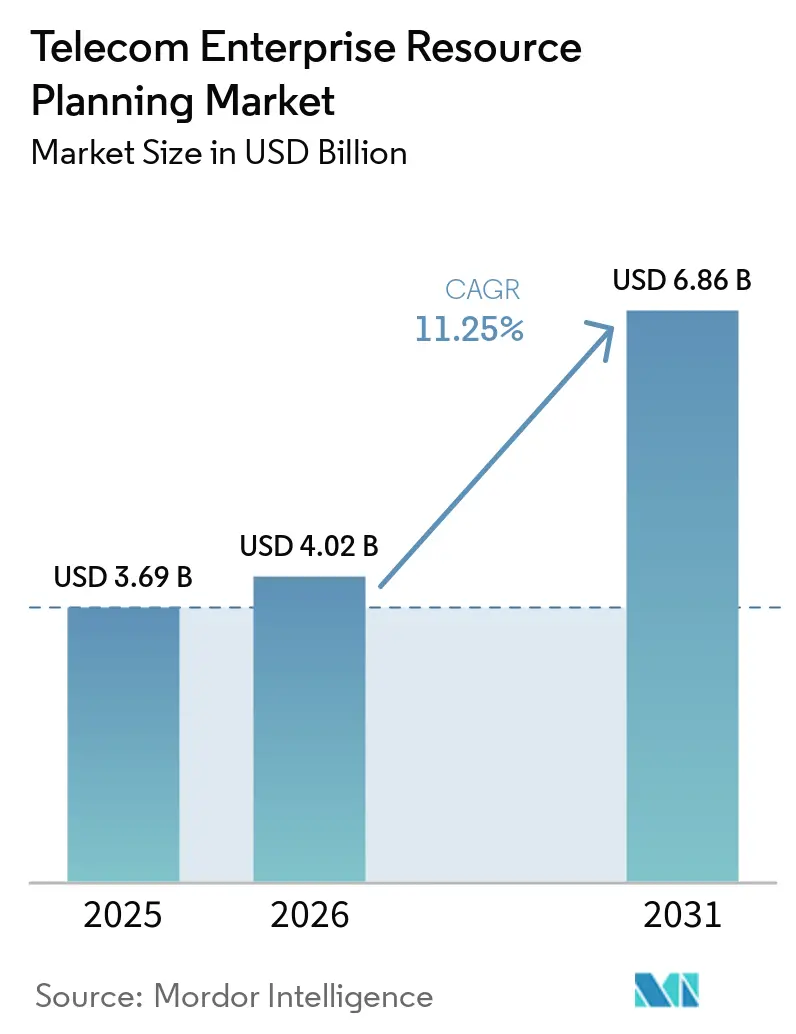

The telecom ERP market size is expected to increase from USD 3.69 billion in 2025 to USD 4.02 billion in 2026 and reach USD 6.86 billion by 2031, growing at a CAGR of 11.25% over 2026-2031. Operators are accelerating platform overhauls to handle 5G network complexity, monetize network slicing, and orchestrate multi-cloud workflows. Spending is pivoting from monolithic legacy suites to hybrid architectures that couple on-premise billing cores with cloud-based analytics, procurement, and AI-driven network modules. Tier-1 carriers are funding these upgrades through multi-year capital plans; AT&T alone has earmarked USD 14 billion through 2027, while tier-2 and tier-3 players are adopting SaaS offerings to bypass the heavy upfront costs of licenses. Vendors differentiate on open APIs and GSMA-aligned AI frameworks that compress deployment cycles and cut revenue leakage. Heightened regulatory scrutiny on real-time auditability further cements the business case for modern, cloud-native ERP.

Key Report Takeaways

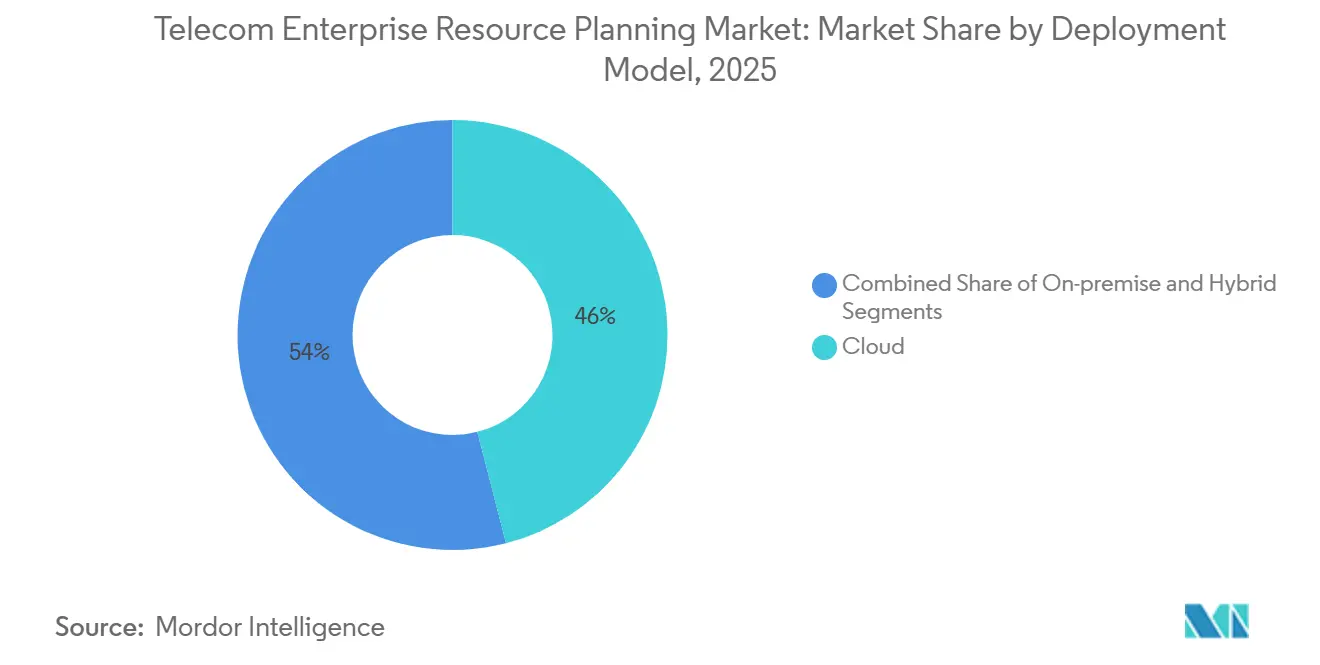

- By deployment model, cloud deployments led with 46% revenue share in 2025; hybrid architectures are forecast to expand at a 15.2% CAGR through 2031.

- By component, software captured 55% of the telecom ERP market share in 2025, while services are advancing at a 17.8% CAGR through 2031.

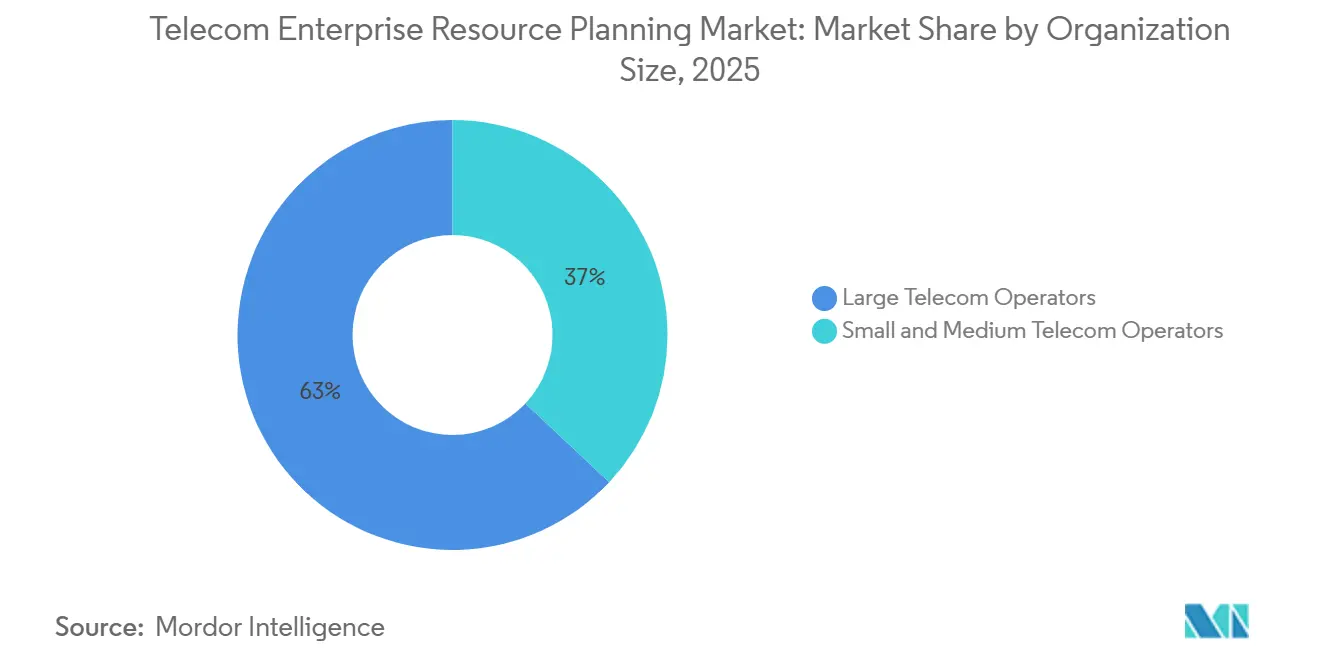

- By organization size, large operators held 63% of the telecom ERP market in 2025, and small and medium operators are projected to expand at a 14.4% CAGR between 2026 and 2031.

- By function, finance and accounting accounted for 28% of the telecom ERP market in 2025, and AI-enabled network management is projected to record the highest CAGR at 21% through 2031.

- By geography, Asia-Pacific dominated with 34% revenue share in 2025; the Middle East is set to grow at a 13.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telecom Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Networks Among CSPs | +3.2% | Global – early momentum in North America, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Push Toward Operational Expenditure Reduction Via Automation | +2.8% | Global – Asia-Pacific and South America | Short term (≤ 2 years) |

| Rising Adoption of Cloud-Native BSS/OSS Stacks in Tier-1 Operators | +2.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Integration of AI-Driven Predictive Analytics Within ERP Suites | +1.9% | Global – led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Mandates for Real-Time Revenue Assurance and Auditability | +0.6% | Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Growing Demand for End-to-End Network Visibility Across Multi-Vendor Environments | +0.3% | Global – Open RAN rollouts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of 5G Networks Among CSPs

Standalone 5G cores require real-time billing, dynamic cost allocation, and orchestration across partner clouds, functions that legacy ERP stacks cannot handle. MTN South Africa’s 2025 rollout exposed these gaps, prompting the carrier to adopt a cloud-native suite that integrates finance, inventory, and network analytics. Operators in Oman and Indonesia echoed this pivot, reducing activation windows from weeks to hours through API-based ERP workflows. 5G’s latency and slicing capabilities also unlock vertical enterprise services that demand granular SLA pricing, intensifying the shift toward modular ERP with embedded catalog and revenue-assurance engines. Hybrid deployments now outpace market growth because they retain on-premise billing governance while cloudifying analytics that optimize slice monetization.

Push Toward Operational Expenditure Reduction Via Automation

Stagnant ARPU and tower-lease inflation leave operators little room for manual processes. Reliance Jio cut operating costs by 30% in 2024 by automating procurement, inventory reconciliation, and vendor payments within a unified ERP fabric. Ericsson shaved 30% off project budgets after moving to SAP S/4HANA, confirming that cloud ERP compresses both implementation time and consultant fees.[1]Ericsson AB, “Rethinking ERP With SAP S/4HANA,” TM Forum, tmforum.org Regulatory frameworks like GDPR further demand automated audit trails, turning compliance from a cost center into a board-level driver. Small and medium carriers, once hampered by capital constraints, are therefore adopting SaaS ERP at almost 1.5 times the overall market CAGR.

Rising Adoption Of Cloud-Native BSS/OSS Stacks In Tier-1 Operators

Tier-1 operators seek API-driven modularity for Open RAN and dynamic spectrum sharing. Freedom Mobile shifted to a cloud-based BSS stack in 2024, launching new products in days rather than quarters.[2]Freedom Mobile, “Cloud-Native BSS Success Story,” TM Forum, tmforum.org Odido’s 2025 migration eliminated 40% of its IT footprint and pushed uptime to 99.99%, underscoring reliability gains that challenge traditional on-premise assumptions. As network-as-a-service strategies spread, hybrid ERP offers the best of both worlds, control over subscriber data and elastic scaling for analytics, which explains its double-digit outperformance.

Integration Of AI-Driven Predictive Analytics Within ERP Suites

GSMA’s Open Telco AI framework standardizes how machine learning models plug into finance, supply chain, and network modules. Early adopters report 15%- 25% reductions in revenue leakage and faster fault remediation, freeing up capital for further digital upgrades.[3]GSMA Intelligence, “Open Telco AI Framework,” GSMA, gsma.com AI now sifts through terabytes of CDRs, inventory logs, and energy metrics to spot anomalies long before humans can. Vendors without native AI risk obsolescence as carriers demand pre-trained telecom models that deliver value on day one.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Licensing Costs For Tier-3 Operators | -1.4% | Global – South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| Data Migration Complexities From Legacy OSS/BSS | -1.1% | Global – Europe and North America | Medium term (2-4 years) |

| Scarcity Of Telecom-Specific ERP Implementation Talent | -0.7% | Global – emerging markets | Medium term (2-4 years) |

| Concerns Over Data Sovereignty In Cross-Border Cloud Deployments | -0.5% | Europe, China, Middle East, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Licensing Costs For Tier-3 Operators

For a mid-size carrier, enterprise-grade ERP licenses can exceed USD 5 million, a figure that rivals tower builds and spectrum renewals. ARPU below USD 2 restricts credit headroom, delaying modernization projects in Africa and parts of Southeast Asia. SaaS pricing eases the pain but triggers concerns about vendor lock-in and exchange-rate volatility. This financial barrier reduces the projected CAGR by roughly 1.4 percentage points and skews vendor pipelines toward larger incumbents.

Data Migration Complexities From Legacy OSS/BSS

Decades-old billing and inventory data use proprietary schemas, making cleansing and mapping a herculean task. Up to half of a migration budget can be lost to data quality work, and misaligned records can cause customer overbilling that sparks churn. Operators therefore phase projects, retaining legacy cores while shifting peripheral functions first. Vendors that package automated migration accelerators will win share as they directly reduce this 1.1 percentage-point drag on growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Balance Control And Agility

Hybrid deployments captured a meaningful share of the telecom ERP market in 2025 and are poised to grow at a 15.2% CAGR through 2031. Operators keep subscriber data and critical billing on-premise while leveraging cloud elasticity for analytics, procurement, and HR. The approach also sidesteps sovereign data hurdles. Cloud models remain attractive, holding 46% telecom ERP market share in 2025, but pure-play cloud growth trails hybrid because mission-critical workloads still demand local control. The telecom ERP market size for hybrid solutions is expected to widen further as latency-sensitive edge applications proliferate.

Freedom Mobile’s cloud migration proved that a hybrid design can deliver 99.99% availability and 35% IT Opex savings. Similar blueprints are now deployed by Vodafone, Orange, and operators across the Gulf states. In China and Russia, strict data-residency clauses hold back public-cloud adoption, yet regulators signal eventual relaxation, which will funnel pent-up demand toward hybrid over the forecast window.

By Component: Services Outpace Software As Integration Complexity Rises

Software licenses generated 55% revenue in 2025, but services, from consulting to managed operations, are scaling faster at 17.8% CAGR. The telecom ERP market for services is expanding as carriers outsource scarce skills in data migration, AI model tuning, and API governance. Ericsson’s SAP program saved 30% not on licensing but on automated migration, underscoring where value accrues.[4]Ericsson AB, “Implementation Cost Savings After SAP Migration,” TM Forum, tmforum.org

System integrators such as IBM, Accenture, and Amdocs are packaging fixed-price bundles that guarantee cut-over timelines, a proposition resonating with CFOs fatigued by open-ended IT budgets. As AI modules permeate network management, demand for data-scientist-as-a-service further tilts wallet share toward services. Consequently, the telecom ERP market share of services is projected to expand steadily, even as software retains its foundational role.

By Organization Size: Small And Medium Operators Accelerate Cloud Adoption

Large carriers commanded 63% market share in 2025, yet small and medium operators are expanding at 14.4% CAGR through 2031, outstripping the broader telecom ERP market. SaaS models eliminate hefty capital outlays, letting tier-2 players leapfrog directly to cloud-native stacks. Pre-configured templates from Oracle NetSuite and Microsoft Dynamics compress go-live from years to months, critical for operators chasing first-mover advantage in underserved rural markets.

Reliance Jio’s automation-led 30% cost cut reverberated across emerging markets, proving that lean teams can harness enterprise-grade capabilities without bespoke customization. As venture-backed mobile-virtual-network operators proliferate, the telecom ERP market size generated by this cohort will keep swelling, challenging the historical dominance of incumbents.

By Function: AI-Enabled Network Management Leads Functional Growth

Finance modules remain the revenue bedrock, with a 28% share in 2025, but AI-enabled network management is on track for a 21% CAGR. GSMA’s framework unlocks plug-and-play predictive models that slash outage minutes and energy bills. With 5G slicing and edge nodes multiplying the number of configuration variables, automated orchestration is no longer optional.

CRM and procurement follow closely, buoyed by digital customer-experience strategies and persistent chipset shortages. Human resources and static inventory modules lag as outsourcing and virtualization marginalize their strategic impact. Vendors embedding pre-trained AI directly into network management stand to capture premium renewals, cementing their hold on the fastest-growing functional pocket of the telecom ERP market.

Geography Analysis

Asia-Pacific held 34% revenue in 2025, fueled by India’s rapid 5G monetization and China’s multi-billion-dollar virtualization programs. Reliance Jio’s ERP-driven 30% OpEx drop spurred Bharti Airtel and Vodafone Idea to initiate similar projects. Japan and South Korea, having modernized during 4G cycles, now focus on AI overlay modules that optimize spectrum, subtly shifting wallet share from core finance to network analytics. As local regulators ease cross-border data hurdles, hybrid ERP adoption will keep pace with rising edge-compute traffic.

The Middle East is the fastest-growing region, with a 13.6% CAGR. Saudi Arabia’s Vision 2030 mandates and the United Arab Emirates’ smart-city agendas require real-time billing, IoT integration, and elastic provisioning. STC and Etisalat pivoted to cloud-native ERP to secure those capabilities, and the Gulf Cooperation Council’s efforts to harmonize data laws further accelerate momentum. Turkey and Israel follow suit, leveraging ERP modernization to differentiate enterprise service portfolios in a crowded mobile landscape.

North America and Europe remain sizable but mature. AT&T’s USD 14 billion network plan and Verizon’s spectrum investments allocate meaningful funds to ERP for procurement and inventory automation. In Europe, GDPR compels real-time revenue assurance, nudging operators toward ERP suites with embedded compliance workflows. Growth therefore tilts toward module-level upgrades rather than greenfield replacements. South America and Africa progress more slowly, yet SaaS models that offer pay-as-you-grow pricing begin to unlock latent demand among cash-strapped carriers.

Competitive Landscape

The field demonstrates a moderate level of concentration. At the higher end of the market, SAP, Oracle, and Microsoft dominate, offering telecom-specific modules that seamlessly integrate critical functions such as finance, supply chain, and network data management. Amdocs, Ericsson, and Nokia maintain a strong presence in the BSS/OSS segment by incorporating advanced AI analytics into their solutions and aligning their offerings with the TM Forum’s Open Digital Architecture, which has emerged as a key standard for procurement decisions.

On the other hand, smaller competitors like Comarch and Tecnotree focus on tier-2 accounts by delivering pre-configured, cloud-based bundles designed to enable rapid deployments within 6 months. Although technological maturity remains a significant factor, the depth and quality of service offerings often play a decisive role in securing contracts.

IBM’s aggressive acquisition strategy in telecom consulting, along with Accenture’s expansion of its communications practice, highlights a concerted effort to capture a larger share of the implementation revenue market. The GSMA’s AI framework has standardized the API landscape, compelling vendors to differentiate themselves through innovative machine-learning models and robust, certified partner ecosystems. While price competition continues to exert pressure, the scarcity of skilled telecom ERP professionals allows service divisions to sustain healthy double-digit profit margins.

Telecom Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Telefonaktiebolaget LM Ericsson

Nokia Corporation

Amdocs Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: GSMA launched the Open Telco AI framework, enabling standardized machine-learning integration across BSS and OSS flows. Early adopters cite 15%-25% lower revenue leakage.

- November 2025: Odido finalized its cloud-native ERP migration, trimming IT footprint by 40% and boosting uptime to 99.99%.

- January 2025: Ericsson completed its SAP S/4HANA rollout, reducing project expenses by 30% and cutting timelines by 40%.

- October 2024: Reliance Jio reported a 30% operating-cost reduction after automating procurement and payments through ERP.

Global Telecom Enterprise Resource Planning Market Report Scope

The Telecom ERP market refers to the ecosystem of specialized enterprise software solutions and associated services that manage, integrate, and optimize business and operational processes for telecommunications service providers.

The Telecom ERP Market Report is Segmented by Deployment Model (On-Premise, Cloud, and Hybrid), Component (Software and Services), Organization Size (Small and Medium Telecom Operators and Large Telecom Operators), Function (Finance and Accounting, Human Resources, and Other Functions), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Software |

| Services |

| Small and Medium Telecom Operators |

| Large Telecom Operators |

| Finance and Accounting |

| Human Resources |

| Supply Chain and Procurement |

| Customer Relationship Management |

| Network Management |

| Inventory Management |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Component | Software | |

| Services | ||

| By Organization Size | Small and Medium Telecom Operators | |

| Large Telecom Operators | ||

| By Function | Finance and Accounting | |

| Human Resources | ||

| Supply Chain and Procurement | ||

| Customer Relationship Management | ||

| Network Management | ||

| Inventory Management | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected revenue for telecom ERP solutions in 2031?

The market is forecast to reach USD 6.86 billion by 2031, growing at an 11.25% CAGR from 2026-2031.

Which deployment model is expanding the fastest?

Hybrid architectures are advancing at a 15.2% CAGR because they balance on-premise billing control with cloud analytics flexibility.

Which region shows the highest growth momentum?

The Middle East leads with a 13.6% CAGR through 2031 as Vision 2030 projects and smart-city initiatives demand cloud-native ERP.

Why are services revenues outpacing software in telecom ERP?

Integration complexity, AI model tuning, and scarce telecom expertise are driving carriers to outsource, pushing services growth to 17.8% CAGR.

Which functional module is growing most rapidly?

AI-enabled network management modules top the list at a 21% CAGR as operators automate fault detection and capacity planning.

How fragmented is vendor competition?

Moderate consolidation exists; the top five vendors hold roughly 60% share, yielding a concentration score of 6.

Page last updated on: