Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

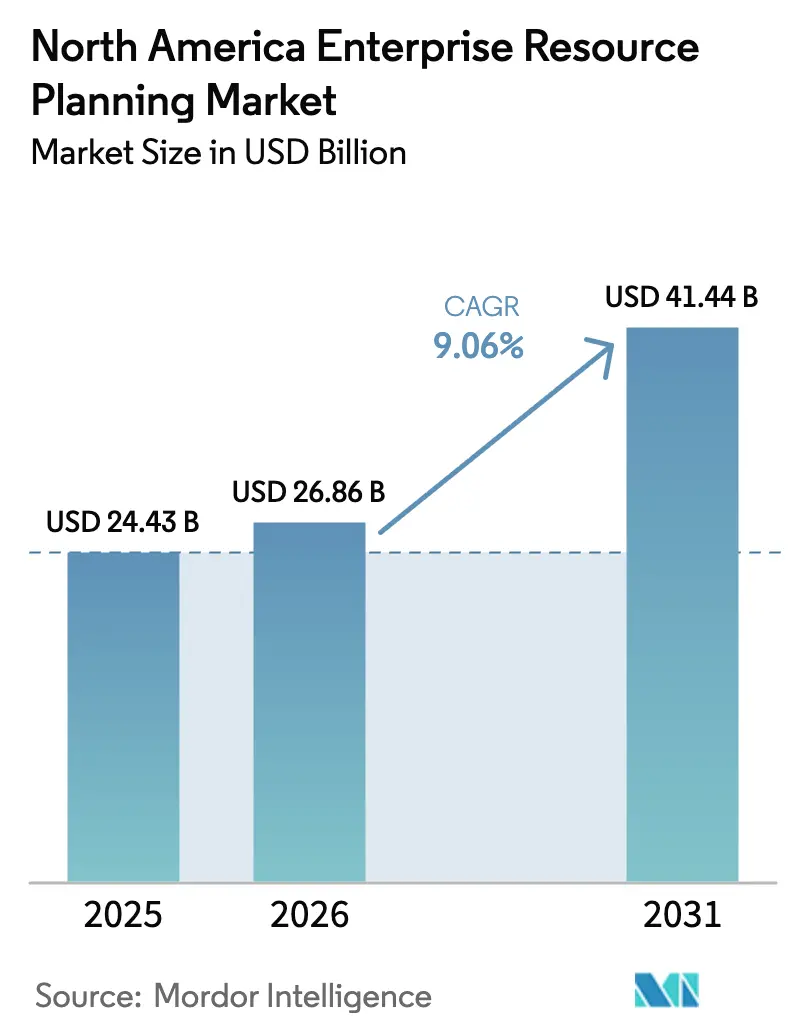

| Base Year Market Size (2025) | USD 24.43 Billion |

| Market Size (2026) | USD 26.86 Billion |

| Market Size (2031) | USD 41.44 Billion |

| Growth Rate (2026 - 2031) | 9.06% CAGR |

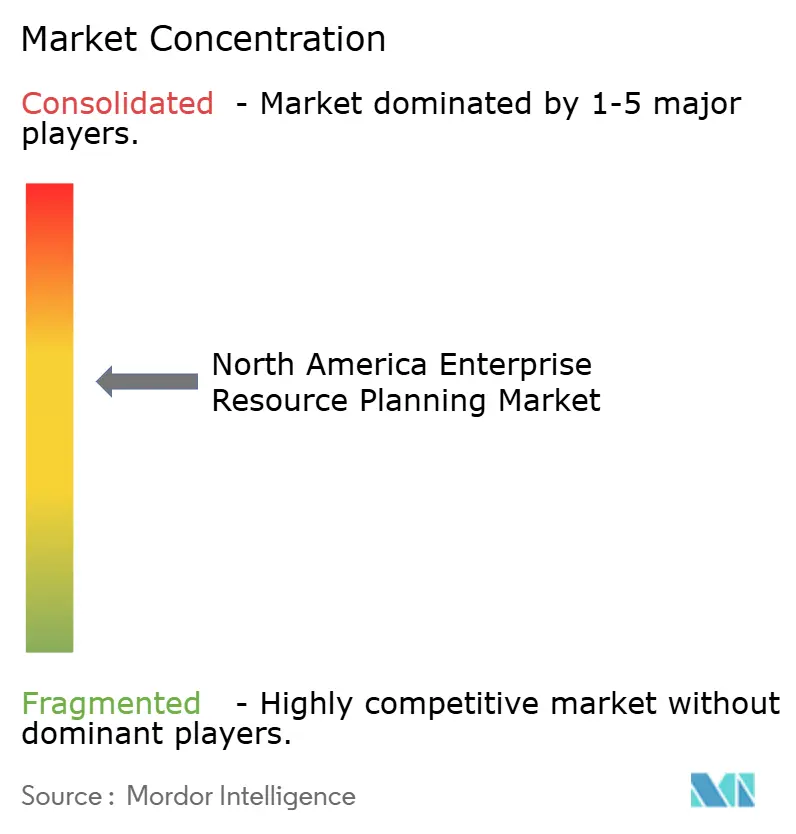

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Enterprise Resource Planning Market Analysis by Mordor Intelligence

The North America Enterprise Resource Planning Market size is expected to increase from USD 24.43 billion in 2025 to USD 26.86 billion in 2026 and reach USD 41.44 billion by 2031, growing at a CAGR of 9.06% over 2026-2031.

Cloud deployments command the largest slice of spending, while two-tier and edge configurations are rising fastest as manufacturers re-architect headquarters, plant, and subsidiary systems for real-time collaboration. Finance and accounting modules still generate the most revenue, yet supply-chain applications are drawing the strongest incremental demand as sensors, demand-sensing algorithms, and automation bridge shop-floor execution with corporate planning. Small and medium enterprises are closing the adoption gap thanks to modular subscription pricing that trims capital outlays, and nearshoring in Mexico is catalyzing bilingual, multi-currency rollouts that support both United States GAAP and Mexican fiscal reporting.

Key Report Takeaways

- By deployment model, cloud held 64.06% of the North America enterprise resource planning market share in 2025, the cloud segment is also expected to grow at the fastest rate of 9.45% CAGR through 2031.

- By business function, finance and accounting captured a 32.59% share in 2025, whereas supply-chain applications are expanding at a 10.61% CAGR to 2031.

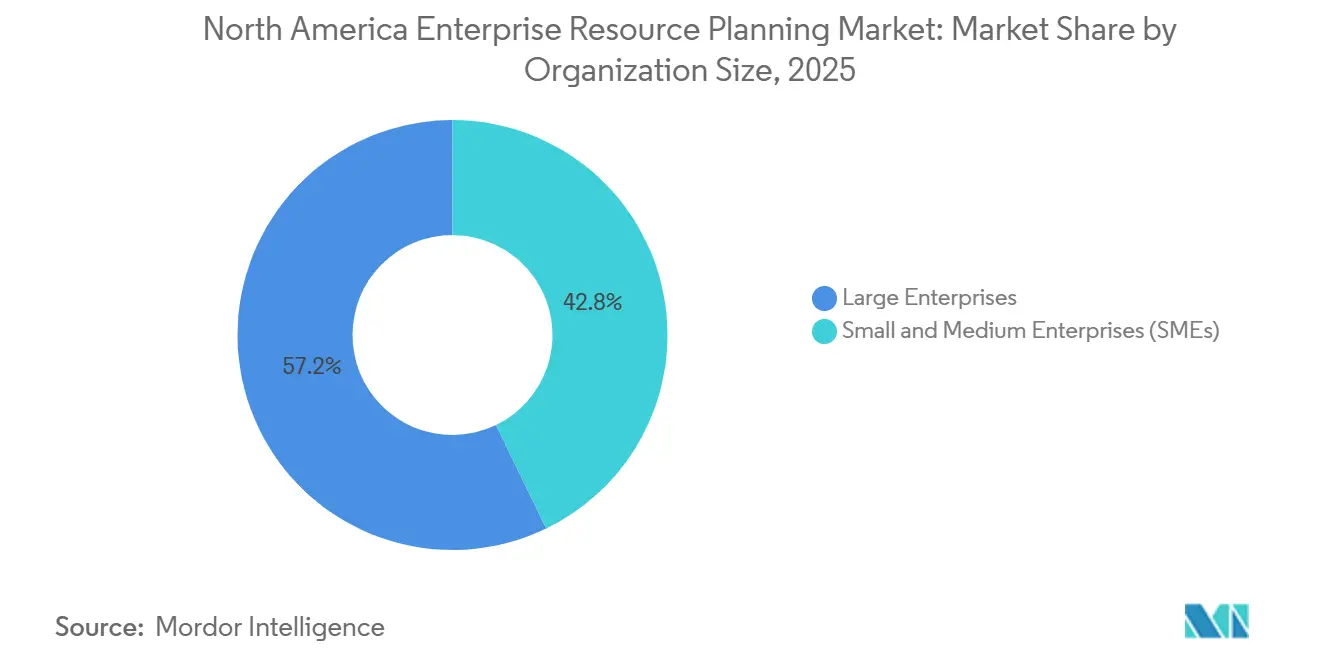

- By organization size, large enterprises accounted for 57.18% of the North America enterprise resource planning market size in 2025, but SMEs are growing at a 9.96% CAGR over the forecast period.

- By industry vertical, manufacturing led with 28.47% of revenue in 2025; retail and e-commerce is the fastest-growing vertical, with a 9.56% CAGR through 2031.

- By geography, the United States dominated with a 78.53% share in 2025; Mexico is forecast to post the highest country-level CAGR at 10.38% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Cloud-First ERP Deployment Models | +2.8% | United States and Canada, spillover to Mexico | Medium term (2-4 years) |

| Surge in AI-Embedded Analytics for Real-Time Decision-Making | +1.5% | The United States and Canada, early adoption in Mexico | Short term (≤ 2 years) |

| Two-Tier ERP Adoption to Harmonize HQ and Subsidiary Operations | +1.2% | United States parents with Mexico and Canada subsidiaries | Medium term (2-4 years) |

| Rising SMB Demand for Affordable, Modular SaaS Suites | +1.8% | The United States and Canada, emerging in Mexico | Short term (≤ 2 years) |

| ESG-Linked Reporting Mandates Accelerating System Upgrades | +0.9% | United States and Canada | Long term (≥ 4 years) |

| Edge/IoT Data Integration for Closed-Loop Operations | +0.7% | United States and Mexico corridors, Canada resource sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Cloud-First ERP Deployment Models

Subscription pricing, automated quarterly feature drops, and removal of capital infrastructure have elevated cloud suites to default status. SAP’s S/4HANA Cloud Public Edition added generative AI for invoice matching and demand forecasting, triggering 1,200 migrations in 2024. Oracle’s Fusion Cloud ERP AI agents replicate intercompany transactions and flag spend anomalies, slicing monthly close times by 30% in pilot users. Microsoft embedded Copilot into Dynamics 365 Finance to handle 40% of repetitive journal reviews, and Workday’s Sana acquisition integrates conversational AI across HCM flows. Manufacturers surveyed by Industry Week in late 2024 revealed that 90% planned cloud-based ERP upgrades within 24 months, up from 72% two years earlier.

Surge in AI-Embedded Analytics for Real-Time Decision-Making

Embedding machine-learning models into transactional workflows shifts ERP from static record-keeping to proactive insight-generation. An IBM study of 2,500 enterprises found that firms integrating AI models achieved 27% higher ERP ROI, reducing stockouts by 18% and excess inventory by 22%. SAP’s partnership with Snowflake lets automakers blend purchasing data with external chip lead-time signals to recalibrate production plans on the fly. Workday’s AI Gateway protects data residency while opening access to large language models, a dual imperative as privacy rules tighten. BCG warns that treating analytics as a bolt-on risks stale data extracts and eroded forecast accuracy.

Two-Tier ERP Adoption to Harmonize HQ and Subsidiary Operations

Multinationals add lightweight cloud instances to acquired plants rather than forcing heavy core templates, slashing post-merger integration cycles. NetSuite’s SuiteCloud now synchronizes bidirectionally with SAP and Oracle back ends, removing months of custom middleware.[1]NetSuite, “NetSuite Next 2025,” netsuite.com Acumatica’s 2024 review showed 38% of new North America customers were subsidiaries of Fortune 1000 parents seeking modern UX without disrupting headquarters payroll or statutory reporting. Gartner estimates that two-tier architectures reduce total cost of ownership by 25-35% compared with extending a monolith to every location.

Rising SMB Demand for Affordable, Modular SaaS Suites

Per-user monthly fees between USD 100 and USD 200 mean a 50-person distributor can deploy ERP for under USD 10,000 a year, an order of magnitude below historical license and hardware costs. Acumatica’s customer base grew 22% in 2024, with 60% of net-new logos having fewer than 250 employees. Sage Intacct subscriptions in North America rose 19% as professional services firms shifted away from spreadsheets. Open-source Odoo expanded its partner network to 180 implementers by March 2025, appealing to startups demanding customization without lock-in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-Front and Life-Cycle Costs of Implementation and Change-Management | -1.3% | The United States and Canada, moderate in Mexico | Short term (≤ 2 years) |

| Cyber-Security and Data-Sovereignty Concerns in Multitenant Clouds | -0.8% | United States and Canada, heightened regulation in the regulated sectors | Medium term (2-4 years) |

| Shortage of North America-Based ERP Talent and Project Bandwidth | -0.6% | The United States and Canada, emerging in Mexico | Short term (≤ 2 years) |

| Vendor Lock-In Risk Amid Shrinking On-Premise Support Windows | -0.4% | United States and Canada installed base | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-Front and Life-Cycle Costs of Implementation and Change-Management

Deloitte’s 2024 survey of 300 projects pegged the median five-year total cost at USD 2.7 million for mid-market rollouts, with 42% spent on change management and data cleansing. PwC found that 38% of projects were running 25% over budget and 29% were missing go-live dates, delaying product launches and revenue expansion. Ongoing subscription escalators can strain budgets as user counts grow, and vendors typically charge 18-22% for annual maintenance on perpetual licenses, forcing CFOs to weigh productivity gains against recurring spend.

Cyber-Security and Data-Sovereignty Concerns in Multitenant Clouds

The June 2024 Snowflake breach, which affected 165 organizations, and the February 2025 Veeam ransomware incident highlighted shared-infrastructure risks. Canadian banks must keep encryption keys onshore under OSFI rules, nudging deployments toward hybrid or sovereign-cloud instances. A 2024 EY poll showed 34% of enterprises pausing migrations until breach-liability clauses and residency guarantees are resolved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Edge Configurations Gain Traction

Edge and two-tier architectures are expanding at a 9.45% CAGR, the fastest pace among ERP architectures, as firms marry headquarters finance cores with lightweight plant-floor or subsidiary instances to handle local compliance, currencies, and low-latency shop-floor data. Cloud-native suites still held 41.11% of spending in 2025, indicating widespread confidence in vendor-managed infrastructure. Mobile-first ERP remains niche at roughly 12% penetration, favored by utilities and field-service fleets that need offline capture and GPS timestamping, while social and collaborative ERP has stalled because Teams and Slack connectors now provide comparable chat-based approval flows.

NetSuite’s 2025 bidirectional connectors slash integration weeks for acquisitions, and edge nodes in Mexican maquiladoras replicate downtime logs to United States cores overnight, preventing WAN congestion. ISO 27001 and SOC 2 certifications shape type selection in regulated pharma or aerospace plants, prompting on-premises edge nodes to preserve audit trails on-site. Vendors differ in their specialties: SAP and Oracle dominate cloud-native and two-tier solutions, whereas specialists such as ServiceMax excel in technician-focused mobile niches.

By Business Function: Supply-Chain Modules Outpace Finance

Supply-chain and operations software is growing at 10.61% annually, driven by the adoption of IoT sensors, demand-sensing algorithms, and supplier portals that compress order-to-cash cycles. Finance and accounting retain the largest slice at 32.59% of 2025 spending because every firm needs general ledger, payables, and statutory reports, yet incremental budgets now fund advanced planning and scheduling, warehouse management, and transportation optimization. Found that AI-driven demand forecasting reduced forecast error by up to 50%, freeing up working capital previously tied up in safety stock. Workday’s conversational AI streamlines benefits queries, demonstrating that HCM also benefits from embedded intelligence.

Traceability mandates in life sciences push manufacturing execution and quality modules higher, and convergence on a single database reduces reconciliation overhead compared with best-of-breed architectures. As cloud vendors infuse finance, operations, and HCM with predictive models and digital assistants, cross-functional workflows gain velocity. This dynamic drives new licenses and expansions, solidifying North America's enterprise resource planning market as the digital backbone for both front- and back-office processes.

By Deployment Model: Cloud Sustains Double-Digit Growth

Cloud accounted for 64.06% of 2025 spending and is rising at a 10.12% CAGR to 2031, driven by vendor deadlines to phase out mainstream on-premises support. SAP will limit S/4HANA on-premise mainstream maintenance to 2027, encouraging migrations with lower TCO and faster quarterly updates. Oracle offers Bring Your Own License credits for Fusion Cloud ERP, and Microsoft positions Azure Stack for regulated industries needing local residency.

The hybrid model combines on-prem financial cores with cloud talent, procurement, or analytics, satisfying compliance while securing AI upgrades. On-prem still appeals to defense contractors bound by ITAR and to hospitals that guard PHI under HIPAA. Hybrid and multi-cloud strategies will dominate as CIOs optimize latency, compliance, and cost. These models reinforce the trajectory of the North America enterprise resource planning market, ensuring cloud revenues scale while legacy cores wind down.

By Organization Size: SME Growth Outpaces Enterprise Adoption

SMEs are posting a 9.96% CAGR, eroding large-enterprise dominance, which stood at 57.18% in 2025. SaaS fees below USD 200 per user per month make enterprise-grade functionality attainable for 50-person distributors who once relied on spreadsheets. NetSuite and Odoo now serve installers with as few as 10 staff, while Sage Intacct’s 19% subscription growth in 2024 illustrates the momentum in the nonprofit and professional services sectors.[2]Sage, “Sage Intacct Cloud Financial Management,” sage.com Generational turnover also fuels demand; millennial founders expect mobile dashboards and self-service configuration.

Large enterprises remain top spenders, given thousands of seats and multi-year transformation programs that exceed USD 50 million, but SME velocity compels vendors to simplify onboarding and embed low-code tools that replace scarce consultants. The democratization of ERP means long-tail demand will steadily bolster the North America enterprise resource planning market, cushioning any cyclical pullback in mega-project spend.

By Industry Vertical: Healthcare Modernization Drives Acceleration

Manufacturing held a 28.47% share in 2025 thanks to automakers, aerospace primes, and machinery builders that need bill-of-material explosions and serial-level traceability. Retail and e-commerce, however, are growing at a 9.56% CAGR, as omnichannel logistics require real-time inventory management, returns handling, and last-mile coordination across stores and web fronts. BFSI relies on ERP for ASC 606 revenue recognition and regulatory filings, while government entities migrate to shared-service clouds under Canada’s Digital Ambition strategy.

IT and telecom providers integrate usage billing, and life-science firms leverage quality modules that meet the requirements of 21 CFR Part 820. Specialized editions, such as Epicor Kinetic for discrete manufacturing, sustain niche players while giants pursue broad suites. Vertical solutions tailored to compliance and workflow nuance deepen switching costs, anchoring the North America enterprise resource planning market share of established vendors and stoking demand for partner-built extensions.

Geography Analysis

The United States captured 78.53% of 2025 revenue, driven by Fortune 500 headquarters, dense partner ecosystems, and early AI adoption. Coastal tech hubs default to SaaS; meanwhile, SEC climate-disclosure rules under final review obligate public companies to report Scope 1-3 emissions, spurring upgrades to sustainability modules. Cyber incidents such as the Snowflake breach heighten due diligence, prompting some banks to adopt hybrid deployments.

Mexico delivers the fastest growth at 10.38% CAGR, buoyed by USD 74 billion in nearshoring pledges covering 174 projects in 2024. Two-tier architectures mesh United States cores with NetSuite or Acumatica in maquiladoras, easing local tax compliance while maintaining consolidated reporting. President Sheinbaum’s incentives for accelerated depreciation and training credits increase ERP penetration as firms monitor capital assets and skill matrices.

Canada aligns with the regional CAGR of 9.06%, propelled by Digital Ambition mandates and healthcare modernization. OSFI residency rules encourage sovereign-cloud or hybrid setups, especially for banks.[3]Government of Canada, “Digital Government Strategy,” canada.ca Ontario’s EV supply chain and Alberta’s resource projects deploy ERP for project accounting and joint-venture billing. Federal shared services consolidate HR and procurement, reinforcing cloud adoption across ministries.

Regulatory Landscape

ERP deployments in North America increasingly operate within cybersecurity, privacy, and digital-sovereignty compliance requirements, which shapes cloud-versus-hybrid decisions and vendor due diligence. In the United States, federal actions in 2025-2026 reinforced expectations around secure software and cryptography for systems used in regulated and public-sector contexts, including Federal Register updates in June 2026 aligned to FIPS standards (such as FIPS 140-3 for cryptographic modules and updates to the Digital Signature Standard under FIPS 186-5). Separately, a February 2026 bill (H.R. 7604) sought to restrict federal contracting with certain internationally owned software providers, which adds procurement risk considerations for ERP vendors and their supply chains serving US government buyers.

Canada is also tightening centralized governance and privacy requirements that affect ERP selection and hosting architecture. The Treasury Board of Canada Secretariat maintains an Interim Standard on Enterprise Resource Planning Solutions that steers federal institutions toward pre-approved ERP options under central oversight, limiting customization and raising entry barriers for new vendors in the federal market. In June 2026, the Government of Canada tabled Bill C-36 (Protecting Privacy and Consumer Data Act), which includes creation of a Data Protection Commission of Canada and introduces stronger enforcement levers (including penalties framed up to 5% of global revenue), while Canadian standards work on digital sovereignty, such as the 2026 second edition of CAN/DGSI 100-8, provides structure for assessing jurisdictional and residency risks relevant to multitenant cloud ERP.

Competitive Landscape

Moderate concentration prevails: SAP, Oracle, Microsoft, Workday, and Infor together hold roughly 60% of revenue. SAP links Datasphere with Google BigQuery, enabling live federation of transactional and supplier data for dynamic scheduling. Oracle’s AI agents trim month-end close by 30%, a lure for private-equity roll-ups. Microsoft’s Copilot reviews 40% of journals at mid-market adopters, while Workday’s Sana-driven chatbots reduce HR tickets in labor-constrained firms.

Specialists maintain beachheads. Epicor serves discrete manufacturers, Sage targets construction accounting, and Odoo leverages open-source to win over startups. NetSuite’s Next 2025 release tightens SAP and Oracle connectors, advancing its two-tier agenda. Talent scarcity shapes competition: Gartner forecasts that 75% of firms risk project delays due to a shortage of ERP consultants. Vendors answer with low-code and AI configuration assistants, such as SAP Build Code for Java and JavaScript extensions.

Cyber resilience and sovereignty differentiate offerings. Oracle partners with Palantir to serve defense customers within ITAR boundaries, and Microsoft’s Azure Stack supports Dynamics workloads on-premises. As vendors sunset on-prem support, migration incentives and partner certifications will decide share shifts. Overall, product innovation, consulting capacity, and vertical depth will determine winners in the North America enterprise resource planning market.

North America Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Workday, Inc.

Plex Systems Inc. (Rockwell Automation Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in regulated, cross-border, and audit-intensive operations, where ERP modernization has to combine cloud agility with provable controls, residency options, and faster integration. Mexico-linked two-tier rollouts tied to nearshoring (multi-currency, bilingual operations, and local statutory and tax reporting) continue to expand the implementation scope for vendors and partners that can synchronize subsidiary systems with US headquarters cores. In parallel, the Canadian market points to demand for sovereign-cloud and hybrid ERP patterns that fit OSFI-driven residency constraints in financial services and broader public-sector procurement guardrails such as the Treasury Board Interim Standard on ERP Solutions.

In terms of spend direction, buyers are shifting incremental budgets toward supply-chain and operations modules, alongside embedded AI intended to shorten cycle times and reduce manual close and reconciliation work. That pattern increases requirements for data-lineage, identity, and control frameworks inside ERP. Deployment activity in 2025-2026 reflects this shift, with Point B documenting a January 2025 program consolidating multiple ERP instances into a single platform for a global media and entertainment organization, and MPI Media Group reporting a February 2026 migration from Dynamics NAV 2009 to Dynamics 365 Business Central to modernize royalty processing and distribution workflows. As audit and security scrutiny remains elevated for shared infrastructure, advisory guidance such as Deloitte's 2025 focus on AI-automated controls in cloud ERP migrations supports an active services and tooling opportunity around SOX-ready control automation, access governance, and continuously monitored configurations.

Recent Industry Developments

- July 2026: Nokia finalized a multi-year agreement to migrate its ERP environment to SAP S/4HANA on Microsoft Azure under the RISE with SAP approach. The program indicates ongoing momentum for hyperscaler-aligned ERP transformations in North America, with vendor roadmaps and migration factories shaped around standardized cloud operating models and reference architectures.

- May 2026: inriver reported that its S/4HANA Cloud Connector achieved SAP certification as built with SAP Business Technology Platform (SAP BTP). The certification reinforces the partner extension ecosystem around S/4HANA Cloud, supporting ERP buyers that rely on certified integration components to reduce implementation risk and improve upgrade compatibility.

- November 2024: Workday completed its USD 1.1 billion acquisition of Sana to embed conversational AI into HCM workflows. Bringing generative AI into ERP-adjacent processes raises the competitive bar for experience-layer automation and self-service, particularly for labor-constrained enterprises looking to reduce HR ticket volumes through in-product assistants.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues earned from enterprise resource planning software and related platforms used to run core business processes across enterprises in North America, including licenses or subscriptions and the typical vendor-provided support tied to those platforms.

Scope exclusions: We exclude unrelated point solutions that do not function as ERP (such as standalone payroll, standalone CRM, or generic productivity tools) unless they are sold and deployed as part of an ERP suite.

Segmentation Overview

- By Type

- Cloud-Native Suite

- Mobile-First ERP

- Social / Collaborative ERP

- Two-Tier / Edge ERP

- By Business Function

- Finance And Accounting

- Supply-Chain And Operations

- Human Capital Management

- Customer Relationship And Commerce

- Manufacturing Execution And Quality

- By Deployment Model

- On-Premise

- Cloud

- By Organization Size

- Large Enterprises

- Small And Medium Enterprises (SMEs)

- By Industry Vertical

- Manufacturing

- Retail And E-Commerce

- BFSI

- Government And Public Sector

- IT And Telecom

- Healthcare And Life Sciences

- Others Industry Vertical

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public data that helps us map the demand pool and the rollout environment for ERP in North America. We typically reference sources such as the US Census Bureau and Statistics Canada for business counts and enterprise activity, the US Bureau of Labor Statistics for labor mix and wage inflation signals, and the US International Trade Commission for trade classifications that indicate technology and hardware movement linked to system upgrades.

We also use company filings, investor presentations, product documentation, and reputable press to understand pricing direction, deployment shifts, and partner ecosystem routes. Where needed, a paid subscription for company financials and intelligence and a paid patent database are used to confirm revenue direction and product focus without leaning on a single disclosure. These desk sources are illustrative only, and many additional public sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what is being bought, how deals are structured, and what customers actually deploy across the United States, Canada, and Mexico. We speak with ERP buyers, implementation partners, and product specialists so assumptions on adoption pace, cloud migration timing, and module expansion can be checked against real procurement and rollout patterns. When desk signals and interview inputs disagree, the assumptions are revisited and then re-tested with follow-up expert checks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | |

| Mid tier: 42% | Functional/Unit leaders: 28% | |

| Smaller Players: 20% | Managers: 58% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach once, where the regional software spend pool and ERP share are reconstructed using public enterprise indicators and then narrowed through deployment and buyer behavior. To keep the totals realistic, we corroborate them with selective bottom-up approximations, such as sampled subscription price ranges multiplied by likely user counts, plus channel checks on implementation throughput, which are then used to adjust outliers.

Inputs used in the model include enterprise counts by size band, cloud adoption direction, ERP replacement cycles for legacy systems, typical implementation timelines, and module add-on intensity in industries that run complex operations (manufacturing and distribution are good examples). Forecasting leans on scenario analysis, because ERP growth depends on a mix of macro budgets and timing of modernization programs, and the scenarios are aligned to what practitioners expect for cloud migration and project delays. Where a bottom-up check has gaps, we use conservative ranges and document why the midpoint was selected before it is rolled into the final total.

Data Validation & Update Cycle

Outputs are triangulated across independent signals, including software spending indicators, partner capacity signals, and adoption narratives collected in interviews. We run variance checks by country and deployment type, and when a result breaks expected patterns, the assumptions are reviewed and recalculated before sign-off.

The report is refreshed annually, and interim updates are made when material events can shift adoption or pricing. Before delivery, an analyst performs a fresh pass on key inputs and conversions so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's North America Enterprise Resource Planning Market Size Versus Other Published Estimates

Published market sizes for North America ERP can look different even when the topic name sounds the same, because the scope and the revenue line being counted is not always identical. Differences usually come from what is treated as ERP versus adjacent business apps, how cloud subscriptions are annualized, and whether implementation services are counted inside the headline value.

By tracking deployment mix shifts and refreshing country-level pricing and adoption inputs, Mordor Intelligence keeps the value tied to ERP software revenues and avoids pulling in loosely related enterprise applications that inflate totals. Gaps also show up when one estimate uses a 2024 base while another uses a 2025 base, or when currency timing and update cadence are not aligned to the same cut-off period.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.43 B (2025) | |

| Regional Consultancy A | USD 21.42 B (2024) | Uses a 2024 valuation year and provides limited clarity on how subscription run-rates and renewals are annualized, which can reduce the reported total versus a 2025 base with updated cloud mix assumptions. |

| Global Consultancy B | USD 28.98 B (2025) | Uses an ERP software scope that can be broader in practice, and the higher value is consistent with looser boundaries between ERP suites and adjacent enterprise applications, plus a different treatment of cloud revenue recognition timing. |

The spread in the table is mainly explained by year alignment and what gets counted inside the ERP boundary. When the scope is kept tight to ERP software revenues and the same pricing and adoption drivers are refreshed consistently, the final number becomes easier to trace and to replicate across North American countries.

Key Questions Answered in the Report

How large is the North America enterprise resource planning market in 2026?

It is valued at USD 26.86 billion and is forecast to grow at a 9.06% CAGR to reach USD 41.44 billion by 2031.

Which deployment model is growing fastest across North America?

Two-tier and edge ERP configurations expand at a 9.45% CAGR as firms overlay lightweight cloud instances on headquarters cores.

What business function commands the largest ERP spending today?

Finance and accounting account for 32.59% of 2025 spending, though supply-chain modules are expanding faster at a 10.61% CAGR.

Why is Mexico seeing rapid ERP adoption?

USD 74 billion of nearshoring projects and fiscal incentives for accelerated depreciation lift ERP demand to a 10.38% CAGR through 2031.

Which vendors dominate the competitive landscape?

SAP, Oracle, Microsoft, Workday, and Infor collectively control about 60% of North America revenue, with specialists like Epicor and Odoo active in niches.

What is the biggest restraint on ERP growth in the region?

Up-front implementation and change-management costs, which can exceed software fees by three to five times, continue to dampen some projects.

Page last updated on: