Government Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

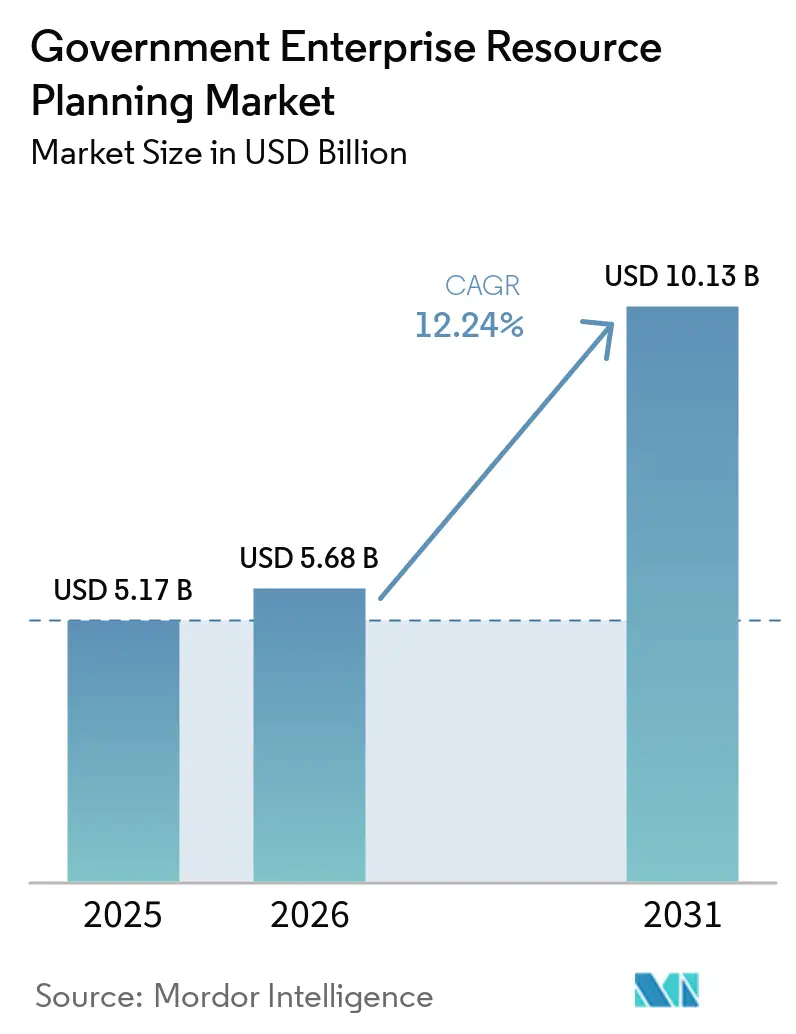

| Market Size (2026) | USD 5.68 Billion |

| Market Size (2031) | USD 10.13 Billion |

| Growth Rate (2026 - 2031) | 12.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Government Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Government ERP market size is expected to increase from USD 5.17 billion in 2025 to USD 5.68 billion in 2026 and reach USD 10.13 billion by 2031, growing at a CAGR of 12.24% over 2026-2031. Accelerated adoption of integrated platforms is displacing fragmented legacy systems as agencies seek a single source of truth for financial, human capital, procurement, and grant management. Cloud deployment remains the entry point for many smaller entities, yet the shift toward hybrid architectures is reshaping vendor roadmaps because sovereignty mandates force sensitive ledgers to stay on-premises while analytics and collaboration tools live in the cloud. Modules that expose real-time dashboards to legislators and citizens are now viewed as essential, moving ERP from back-office recordkeeping to front-office accountability. Vendors that embed AI for predictive budgeting and automated compliance are widening their competitive moat, while professional-services partners capture rising demand for configuration, migration, and training.

Key Report Takeaways

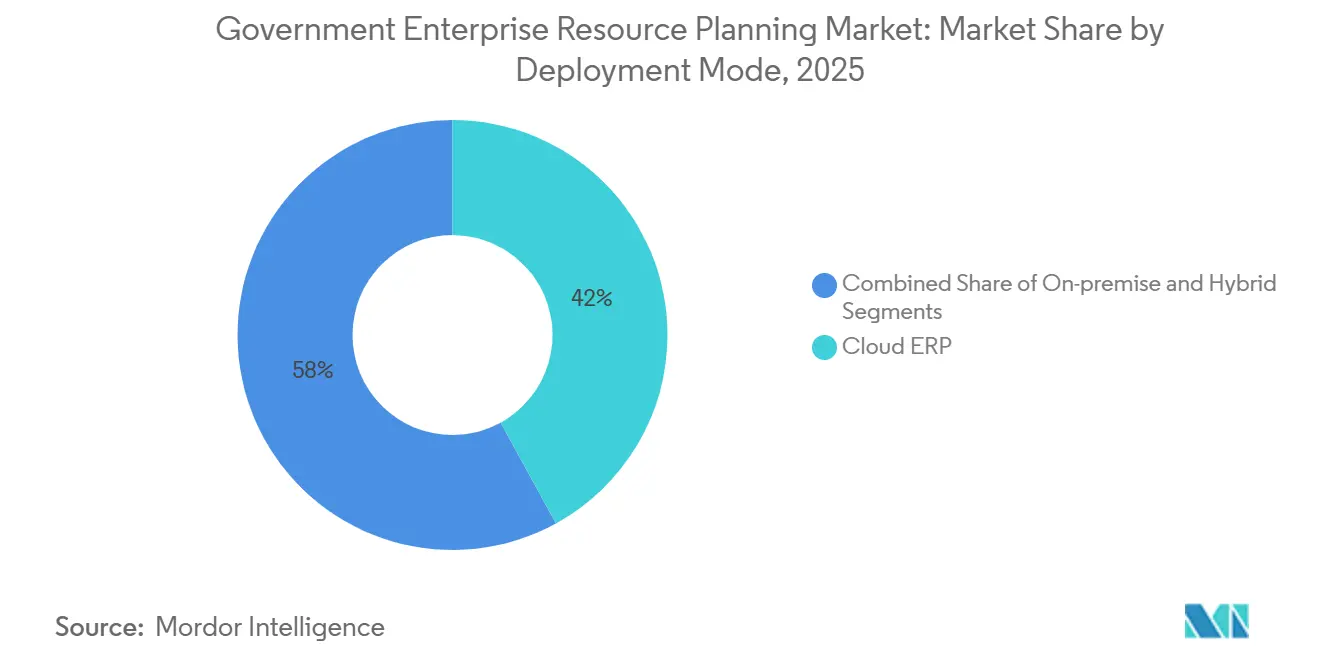

- Cloud ERP held 42% of the government ERP market share in 2025, and hybrid ERP is projected to expand at a 14.80% CAGR to 2031.

- Financial management accounted for 34% of the government ERP market in 2025, while grant management is forecast to grow at a 15.20% CAGR through 2031.

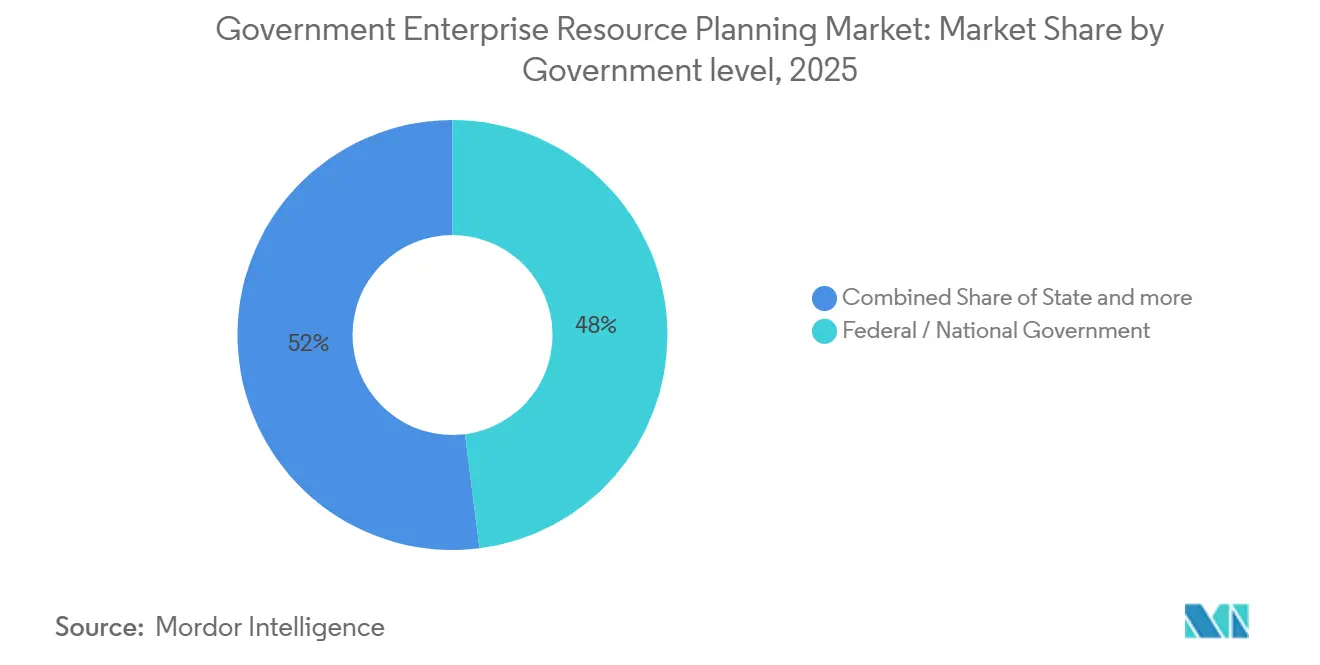

- Federal and national agencies accounted for 48% of 2025 spending, and local governments are advancing at a 12.10% CAGR through 2031.

- Software captured 70% of 2025 component revenue, but services are on track to rise at a 13.70% CAGR across the forecast window.

- North America led with 37% of 2025 revenue, and Asia-Pacific registers the fastest 12.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Government Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Mandates in Government | +3.2% | Global, concentrated in North America, Europe and Asia-Pacific | Medium term (2-4 years) |

| Cost Savings from Cloud Migration | +2.8% | North America and Europe lead, Asia-Pacific and Middle East accelerating | Short term (≤ 2 years) |

| Need for Enhanced Transparency and Accountability | +2.1% | Global, high intensity where stimulus funds flow | Medium term (2-4 years) |

| Integration of AI and Analytics for Decision Support | +1.9% | North America and Europe early adopters, Asia-Pacific emerging | Long term (≥ 4 years) |

| Zero-Trust Security Requirements Driving ERP Upgrades | +1.5% | North America, Europe and Australia | Medium term (2-4 years) |

| Stimulus-Funded Green Ledger Tracking for Sustainability Reporting | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Mandates In Government

Mandatory cloud-first directives are making decades-old mainframes prime candidates for replacement. Oklahoma’s 2026-2028 plan requires every agency to adopt cloud architectures by fiscal 2028, and Tennessee earmarked USD 47 million for legacy ERP retirement in FY2026.[1]Oklahoma Office of Management and Enterprise Services, “IT Strategic Plan 2026-2028,” ok.gov Vermont is consolidating 14 disparate ledgers, mirroring dozens of U.S. states where COBOL retirements outpace hiring pipelines. Australia shortened procurement lead times from 36 to 12 months by launching a pre-qualified vendor panel in February 2026, unlocking backlogged projects.[2]Australian Digital Transformation Agency, “A New Approach to Enterprise Resource Planning for the APS,” dta.gov.au Because these mandates couple deadlines with audit penalties, budget allocations are ring-fenced, ensuring consistent demand even where internal IT capacity is thin.

Cost Savings From Cloud Migration

Financial models show 30-40% lower five-year total cost of ownership versus on-premises, making cloud attractive for budget-pressed treasuries. The United Kingdom partnered with Rackspace Technology and Rubrik in 2025 to build a sovereign cloud that meets data-residency rules without sacrificing hyperscale elasticity. SAP introduced a France-hosted sovereign cloud in 2025 that satisfies European privacy laws while preserving global support. Rhode Island selected Workday after calculating that subscription fees would be 35% lower than maintaining its legacy PeopleSoft stack. Savings free funds to develop citizen-facing portals, enhancing satisfaction scores, and cutting call-center costs.

Need For Enhanced Transparency And Accountability

Trillions in stimulus and infrastructure funds require real-time audit trails. HHS GrantsSolutions processes more than USD 100 billion annually, enforcing 2 CFR 200 compliance and publishing performance dashboards. REI Systems’ GovGrants adds AI risk scoring, which reduced improper payments by 12% in pilots. Miami publishes budget-versus-actual dashboards through Oracle OPAL, a transparency metric tracked by bond-rating agencies. As citizens gain self-service insight, ERP value propositions shift from internal bookkeeping to public accountability.

Integration Of AI And Analytics For Decision Support

Predictive modules now inform procurement, budgeting, and workforce planning. Atlanta uses Oracle OPAL to forecast cash-flow gaps and optimize bond issuances. Tyler Technologies’ Resident AI Assistant fielded 17,000 monthly queries in Indiana, slicing call-center loads by 40%. Workday disclosed that 75% of new government contracts include AI products. Deltek’s GovWin IQ now drafts proposal outlines in minutes, compressing bid cycles for vendors. As AI becomes table-stakes, agencies redeploy staff from transactional tasks to analytical roles, justifying premium subscriptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy Government Procurement Cycles | -1.8% | Global, acute at federal and state levels | Short term (≤ 2 years) |

| Data Security and Sovereignty Concerns | -1.3% | Europe, Asia-Pacific and Middle East | Medium term (2-4 years) |

| Shortage of Public-Sector ERP Skillsets | -0.7% | Global, most severe in local governments | Long term (≥ 4 years) |

| Political Turnover Disrupting Long-Term Projects | -0.5% | Emerging and politically volatile regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Government Procurement Cycles

Award schedules of 24-48 months erode modernization business cases. The U.S. Department of Defense cancelled the CIO-SP4 vehicle in 2025, forcing agencies to re-compete IT services and adding up to 18 months to timelines. Union County, North Carolina, expects no vendor decision until late 2026, following a two-stage RFP issued in 2025. The U.K. Public Accounts Committee reported capability gaps that fuel overruns and delay go-lives. Such inertia favors incumbents and dissuades new entrants, slowing overall market momentum.

Data Security And Sovereignty Concerns

Localization laws compel vendors to deploy in-country data centers, raising costs and complexity. India’s Digital Personal Data Protection Act, Vietnam’s PDP Law and Singapore’s MAS guidelines mandate residency and stringent key management. Australia’s CPS 230 ties cloud adoption to strict operational resilience tests. In November 2025, France and Germany formed a sovereign AI ERP consortium with Mistral AI and SAP to avoid U.S. hyperscalers. Contract clauses that demand customer-controlled encryption and audit rights extend deployment schedules and inflate total cost of ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Configurations Reconcile Sovereignty And Scalability

Hybrid ERP is advancing at a 14.80% CAGR, the fastest among deployment modes, because agencies can partition sensitive ledgers on-premises while exploiting cloud elasticity for analytics. Cloud ERP held 42% of the government ERP market size in 2025, driven by municipalities that lack data-center infrastructure. Washington State’s USD 518 million One Washington program illustrates the approach, hosting payroll on state servers and procurement on Microsoft Azure Government. SAP’s France sovereign cloud shows that similar models satisfy European Schrems II rulings. Orchestration complexity once discouraged hybrid rollouts, but vendors now embed low-latency connectors that keep sub-ledgers synchronized. As air-gapped government cloud regions proliferate, on-premises deployments decline except in defense and revenue agencies bound by high-security baselines.

Vendor consolidation is accelerating because only providers with dual codebases can win large solicitations. Rhode Island’s Workday contract contains repatriation options if privacy regulations tighten, proof that even cloud-first buyers want exit flexibility. Australia’s 2026 policy makes hybrid the default for federal departments, pushing hyperscalers to partner with local data-center operators. North American agencies benefit from 12 newly FedRAMP-authorized platforms that reduce assessment costs. The competitive lens has shifted from pure functionality to architectural optionality, rewarding suppliers that deliver seamless workload mobility across environments.

By Module: Grant Management Surges On Stimulus Tracking Mandates

Grant management is forecast to grow at a 15.20% CAGR through 2031, eclipsing every other functional pillar as agencies administer escalating stimulus and infrastructure disbursements. Financial management retained 34% of the government ERP market share in 2025, anchoring core ledgers, yet replacement demand has plateaued. HHS Grantsolutions handles more than USD 100 billion annually, setting the compliance bar for indirect-cost validation and performance audits. REI Systems’ AI scoring cuts improper payments before awards are issued, and vendors such as OpenGov and GrantWorks added milestone-based disbursement features in 2025. Transparency mandates propel citizen portals that let applicants track award status without staff intervention.

Human-capital modules ride a separate wave of demand as baby-boomer retirements squeeze public-sector recruiting pipelines. Procurement suites integrate e-invoicing mandates that France, Belgium, and Poland phase in by 2026, making PEPPOL compatibility non-negotiable. Asset-management modules are gaining traction in cities that maintain roads, water systems, and public buildings, as predictive maintenance lowers lifecycle costs. Citizen-service portals and case-management tools are blending into core ERP as vendors bundle capabilities, expanding the addressable government ERP market size without requiring separate procurement.

By Government Level: Municipal Digitization Outpaces Federal Modernization

Local governments are advancing at a 12.10% CAGR, the fastest tier of the government ERP market, because citizens increasingly demand digital permitting, licensing, and budget transparency. Federal bodies still commanded 48% of 2025 spend, buoyed by mega-projects such as the U.K. Home Office SAP S/4HANA migration and the U.S. Department of Veterans Affairs ERP solicitation. Miami’s adoption of Oracle OPAL shows bond rating agencies now consider dashboard transparency. Liège integrated Microsoft Dynamics 365 with its PEPPOL gateway ahead of Belgium’s 2026 rule. Melton City Council in Australia unified finance, assets, and citizen services on TechnologyOne Ci Anywhere, eliminating synchronization headaches.

State and provincial projects balance scale and agility. One Washington swaps 40-year-old COBOL code for a hybrid stack, while Florida’s Project PALM and South Dakota’s Project BISON stretch to 2027. Federal buying cycles lengthen when contract vehicles collapse, as seen with CIO-SP4. Municipalities, by contrast, can implement pre-configured templates within a year, lowering total cost by 20-30% and expanding the practical government ERP market.

By Component: Services Surge As Agencies Outsource Implementation Complexity

Services are projected to grow at a 13.70% CAGR, outpacing software, as agencies lack internal ERP architects. Software generated 70% of 2025 revenue, but consumption-based pricing now bundles managed services into multi-year contracts. Union County’s RFP seeks consultants for vendor selection through change management, a pattern echoed nationwide. Major advisories hired former CIOs and FedRAMP specialists to guide the design of role-based access control and data-migration testing.

Implementation remains the largest sub-segment, covering legacy data extraction and user-acceptance. Managed services grow faster as agencies offload patching and performance monitoring to vendors. The U.S. Treasury Bureau of Engraving and Printing shifted to an Oracle-managed cloud contract, retaining configuration control while outsourcing infrastructure. Consulting evolves toward target-operating-model design and KPI definition. Training earns fresh attention after Indiana cut call-center traffic by 40% using Tyler’s Resident AI Assistant, proving that adoption, not just go-live, drives return on investment.

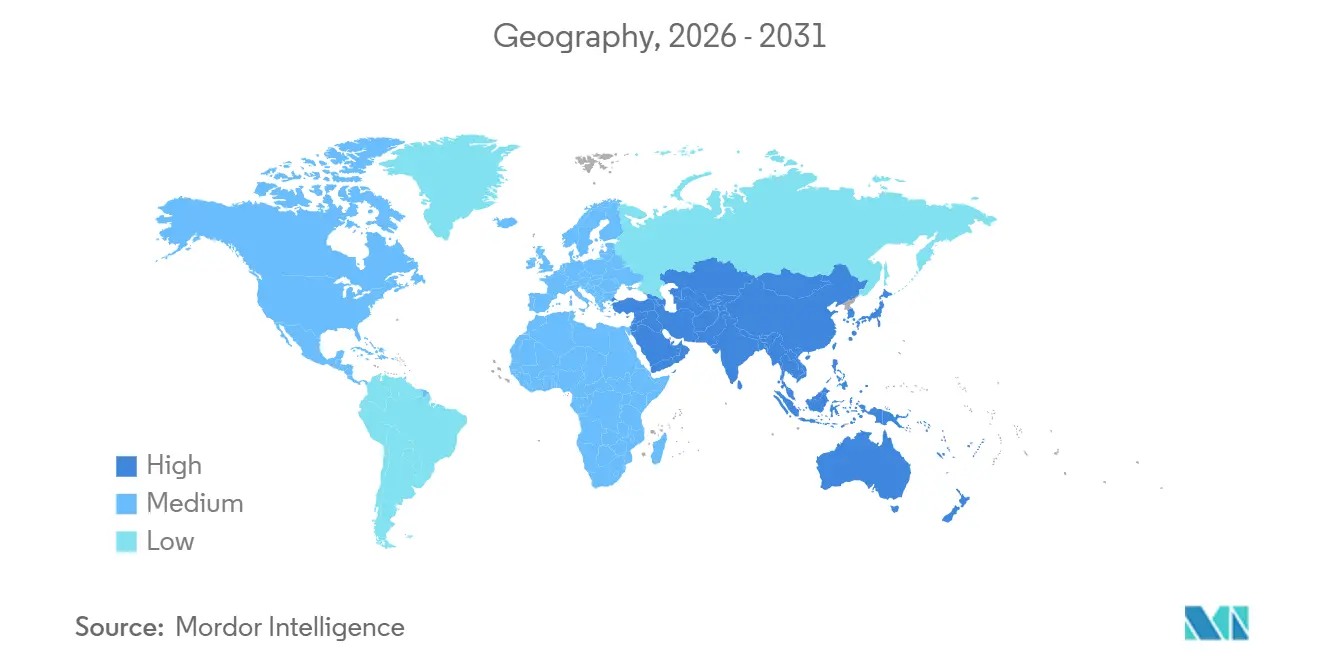

Geography Analysis

North America led the government ERP market with a 37% revenue share in 2025, as the Technology Modernization Fund funded federal upgrades and states such as Washington committed USD 518 million to replace 40-year-old systems. Municipal deployments, such as Miami’s Oracle OPAL roll-out, underscore how transparent dashboards enhance credit ratings. Canada’s Digital Adoption Program issued CAD 15,000 (USD 11,700) grants and CAD 100,000 (USD 78,000) loans to accelerate cloud migration for small governments. FedRAMP added 12 authorized platforms in 2025, slashing security assessment costs and widening supplier pools.

Asia-Pacific exhibits the fastest 12.80% CAGR through 2031, driven by India’s Digital India 2.0 roadmap, China’s unifying Government Service Platform, and Australia’s vendor panel that cuts procurement to 12 months. Sovereignty laws require in-country hosting, spurring local data-center investment by global vendors. Thailand and Malaysia issue guidelines modeled on Australia’s CPS 230, anticipating similar resilience tests. Municipal digitization in Indonesia and the Philippines is expanding the addressable government ERP market, where broadband penetration exceeds 70%.

Europe balances opportunity with regulatory friction. Schrems II, GDPR and country-specific e-invoicing mandates push agencies toward sovereign clouds. France and Germany formed a consortium with Mistral AI and SAP to deploy AI-ready ERP starting 2026, excluding U.S. hyperscalers. Belgium enforced PEPPOL compliance in January 2026, and Poland’s KSeF system entered phased go-live in February 2026, compelling ERP vendors to integrate national gateways. The U.K. completed its Home Office migration yet the National Audit Office warns savings remain elusive without stronger vendor governance.

Competitive Landscape

The market is moderately concentrated, with the top 10 players holding around half of the market share. Tyler Technologies, Oracle, SAP, Microsoft, and Workday dominate North American and European bids because their platforms already possess FedRAMP or ISO 27001 credentials. Tyler bought For The Record for USD 212.5 million in February 2026, adding AI court transcription that deepens its justice vertical. [3]Tyler Technologies, “For The Record Acquisition,” sec.gov Workday created a “Workday Government” unit in 2025 and then secured the U.K. Matrix cluster contract, valued at GBP 144.3 million (USD 183 million). [4]Workday Inc., “UK Matrix Cluster ERP Contract Win,” workday.com OpenGov, valued at USD 1.8 billion, purchased Ignatius in February 2025 and partnered with NEOGOV in March 2026, targeting cities that need bundled HR-finance suites.

Mid-tier vendors carve niches: Deltek serves project-based federal contractors, Accela leads permitting systems, and TechnologyOne dominates Australian councils. Low-code platforms like Appian win extension projects that avoid lock-in, while open-source Axelor appeals to budget-constrained municipalities. AI integration is now a must-have: Workday reports 75% of new public-sector contracts bundle AI. Vendors lacking roadmaps risk displacement as agencies evaluate platforms on productivity gains rather than module checklists.

White-space lies in grant-lifecycle automation and hybrid-orchestration tooling. Agencies still reconcile billions in spreadsheets, offering fertile ground for specialized providers. Meanwhile, consolidation accelerates because only companies with deep compliance investments can afford multi-year FedRAMP authorizations. Expect further MandA as vendors chase end-to-end portfolios that span budgeting, citizen portals and AI-driven insights.

Government Enterprise Resource Planning Industry Leaders

Oracle Corporation

SAP SE

Tyler Technologies, Inc.

Microsoft Corporation

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tyler Technologies announced a USD 1 billion share-repurchase program, citing strong government pipeline.

- March 2026: OpenGov partnered with NEOGOV to link workforce and financial analytics for municipalities.

- February 2026: Tyler Technologies acquired For The Record for USD 212.5 million, adding AI court transcription to its justice suite.

- February 2026: Defense Logistics Agency selected Icertis Contract Intelligence for SAP-integrated procurement workflows.

Global Government Enterprise Resource Planning Market Report Scope

The Government Enterprise Resource Planning (ERP) market refers to the ecosystem of software platforms and associated services designed to support the planning, management, and execution of administrative, financial, and operational functions across public-sector entities.

The Government Enterprise Resource Planning Report is Segmented by Deployment Mode (On-Premises ERP, Cloud ERP, Hybrid ERP), Module (Financial Management, Human Capital Management, Procurement and Supply Chain, Asset and Infrastructure Management, Grant Management, Other Modules), Government Level (Federal/National, State/Provincial, Local/Municipal), Component (Software, Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa).

| On-Premises ERP |

| Cloud ERP |

| Hybrid ERP |

| Financial Management |

| Human Capital Management |

| Procurement and Supply Chain |

| Asset and Infrastructure Management |

| Grant Management |

| Other Modules |

| Federal / National Government |

| State / Provincial Government |

| Local / Municipal Government |

| Software |

| Services |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Mode | On-Premises ERP | |

| Cloud ERP | ||

| Hybrid ERP | ||

| By Module | Financial Management | |

| Human Capital Management | ||

| Procurement and Supply Chain | ||

| Asset and Infrastructure Management | ||

| Grant Management | ||

| Other Modules | ||

| By Government Level | Federal / National Government | |

| State / Provincial Government | ||

| Local / Municipal Government | ||

| By Component | Software | |

| Services | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the government ERP market be by 2031?

It is projected to reach USD 10.13 billion by 2031, reflecting a 12.24% CAGR from 2026.

Which deployment model is growing fastest among public agencies?

Hybrid ERP configurations are advancing at a 14.80% CAGR because they balance data sovereignty with cloud scalability.

Why are grant-management modules gaining traction?

Stimulus and infrastructure programs demand real-time fund tracking, pushing grant-management modules to a forecast 15.20% CAGR.

Which region shows the quickest growth in government ERP adoption?

Asia-Pacific leads with a 12.80% CAGR through 2031, driven by national digitization roadmaps in India, China and Australia.

What factors restrain rapid ERP modernization in government?

Lengthy procurement cycles and data-sovereignty mandates extend implementation timelines and raise total cost of ownership.

How concentrated is vendor competition?

The top 10 vendors hold 44.6% of revenue, indicating moderate concentration and potential for further consolidation.

Page last updated on: