ERP With Embedded Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

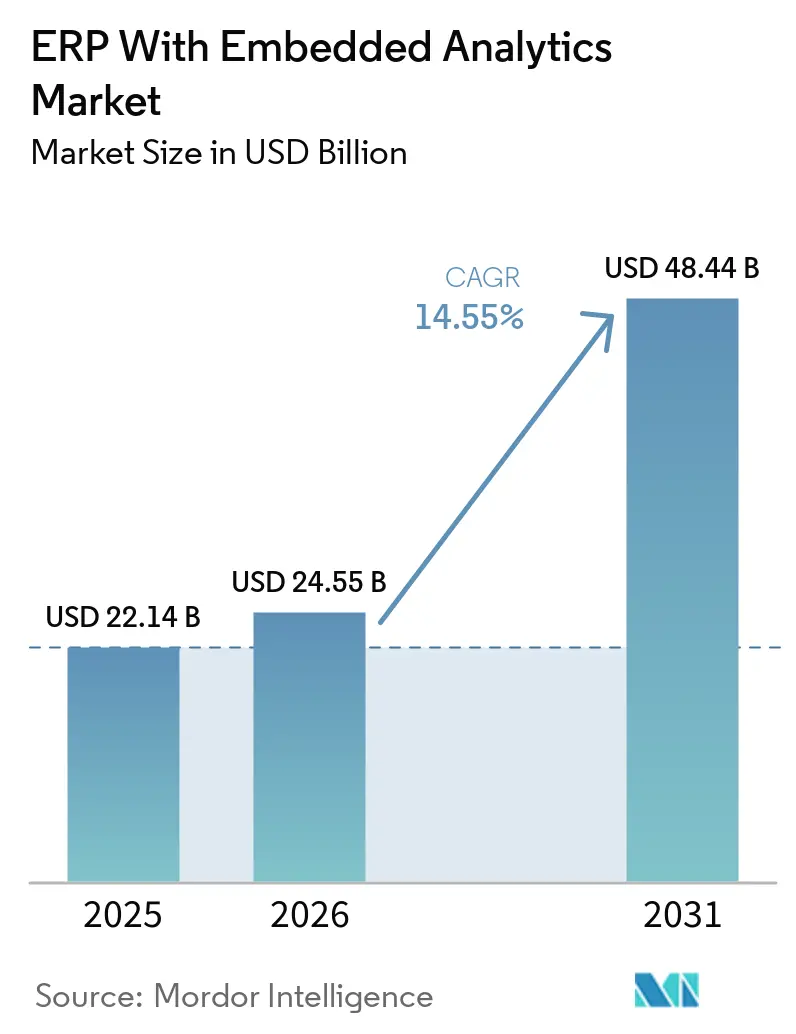

| Market Size (2026) | USD 24.55 Billion |

| Market Size (2031) | USD 48.44 Billion |

| Growth Rate (2026 - 2031) | 14.55% CAGR |

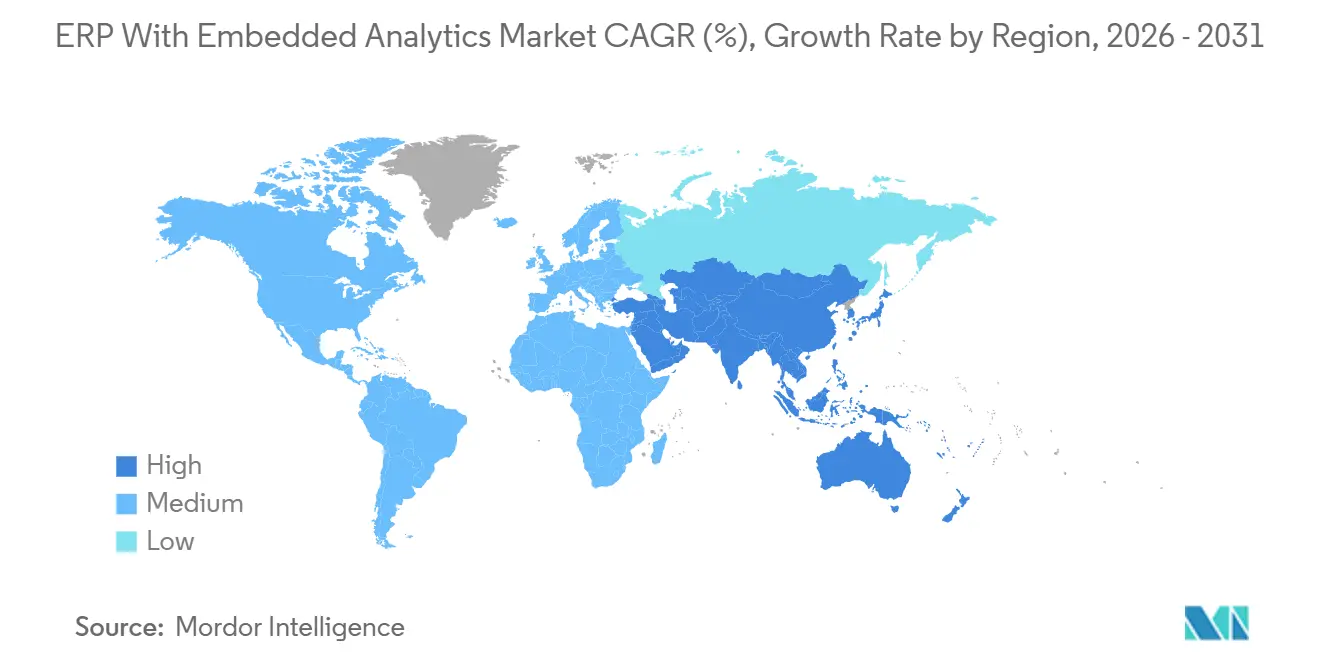

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

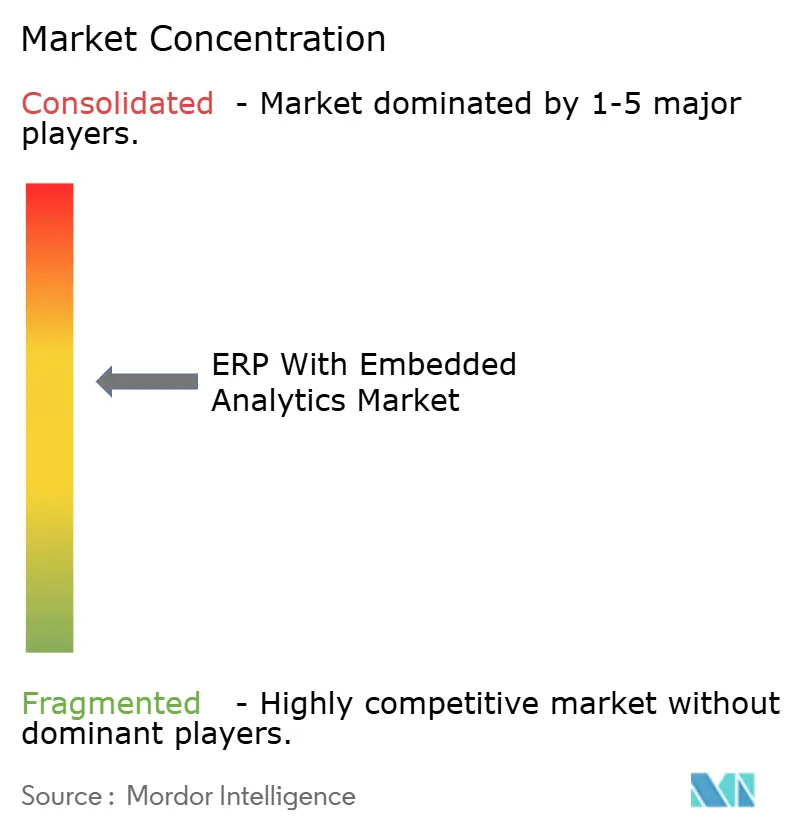

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ERP With Embedded Analytics Market Analysis by Mordor Intelligence

The ERP with Embedded Analytics market size is expected to increase from USD 24.55 billion in 2026 to USD 48.44 billion by 2031, growing at a CAGR of 14.55% over 2026-2031. In 2025, the value stood at USD 22.14 billion, confirming rapid scale-up as enterprises replace detached business-intelligence layers with in-workflow analytics that cut decision latency from days to minutes. Heightened demand for real-time process optimization, swift migration toward cloud architectures, and expanding availability of generative-AI copilots are intensifying vendor rivalry and shrinking product-differentiation windows. Enterprises increasingly prefer packaged analytics templates that compress roll-outs from a year to a single quarter, even as buyers in regulated sectors pursue hybrid models to protect sensitive data. Meanwhile, open API-first ecosystems are nurturing a partner marketplace of niche algorithm providers, accelerating time-to-value for line-of-business users and further fueling the ERP with Embedded Analytics market.

Key Report Takeaways

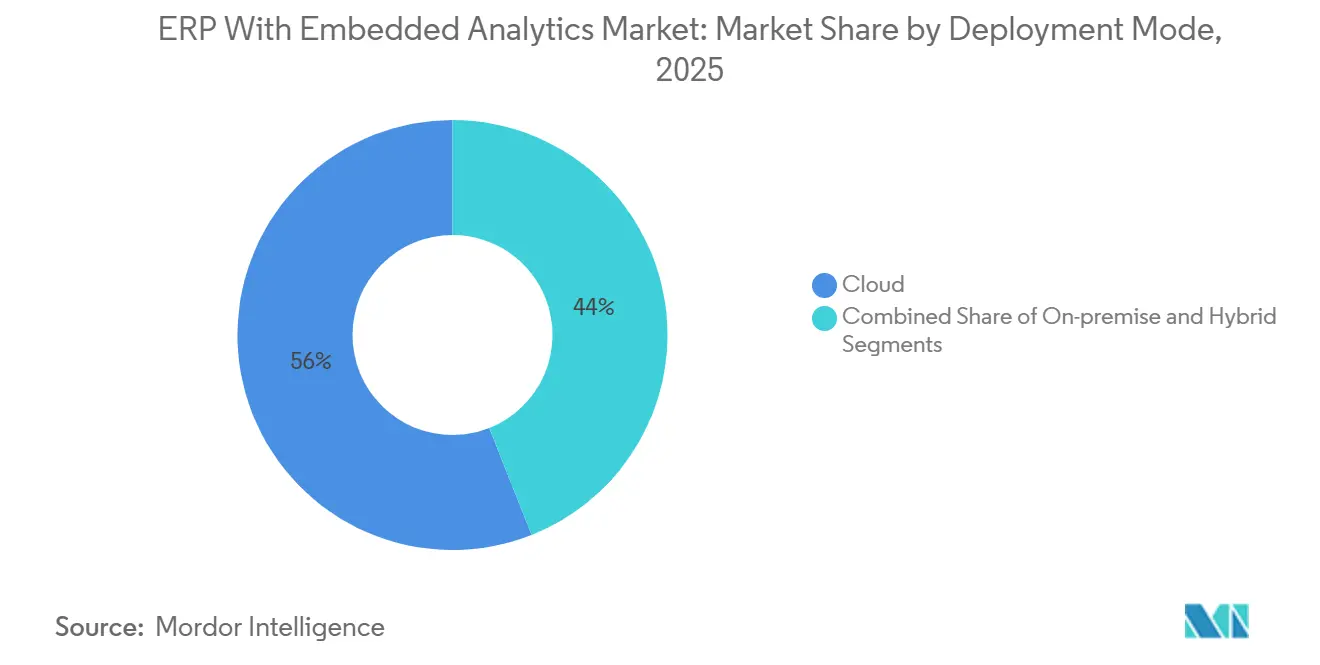

- By deployment mode, cloud held 56% revenue share in 2025, while hybrid architectures are forecast to expand at an 18.00% CAGR through 2031.

- By component, software licenses accounted for 68% of 2025 revenue, whereas implementation and integration services are projected to rise at a 15.50% CAGR to 2031.

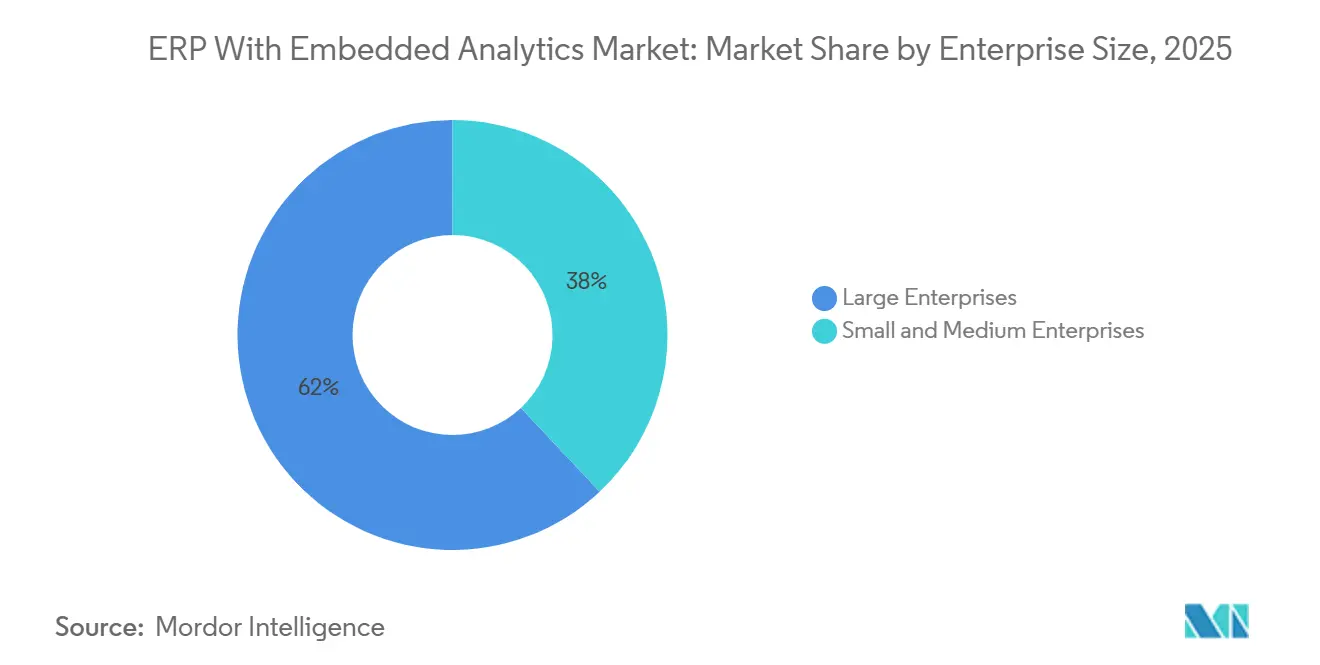

- By enterprise size, large enterprises commanded 62% revenue share in 2025; small and medium enterprises are expected to post a 17.20% CAGR between 2026 and 2031.

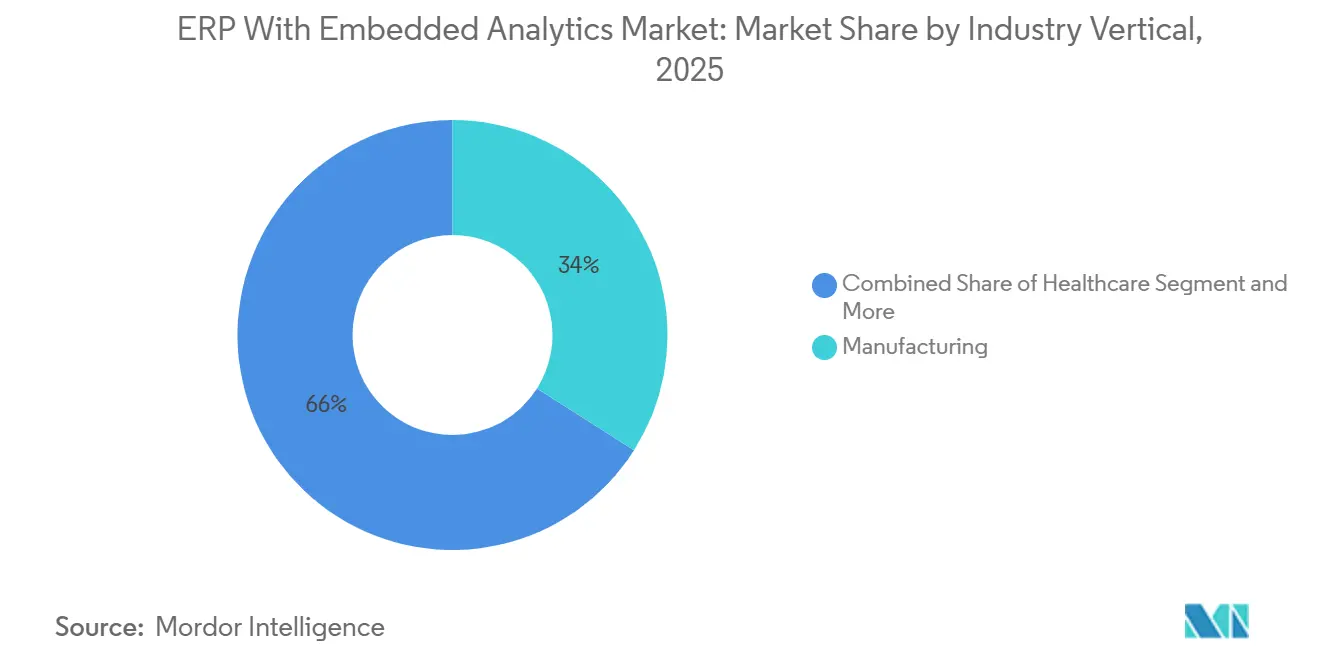

- By industry vertical, manufacturing led with 34% revenue contribution in 2025, yet healthcare is on track for a 16.80% CAGR to 2031.

- By geography, North America captured 37% of the revenue share in 2025, but Asia-Pacific is poised to record a 13.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ERP With Embedded Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Cloud ERP Adoption Among Enterprises | +3.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Demand for Real-Time Data and Predictive Insights to Optimize Operations | +2.8% | Global, particularly Asia-Pacific and North America manufacturing hubs | Short term (≤ 2 years) |

| Integration of AI, ML and IoT Driving Embedded Analytics Capabilities | +2.5% | Global, led by North America and Asia-Pacific technology corridors | Medium term (2-4 years) |

| Shift Toward ESG and Sustainability Reporting Embedded into ERP Analytics | +1.9% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rise of Two-Tier ERP Architectures Requiring Unified Analytics | +1.6% | Global, early adoption in multinational enterprises | Medium term (2-4 years) |

| Generative AI Accelerating ERP Data Migration and Analytics Model Creation | +2.1% | North America and Europe early adopters, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Cloud ERP Adoption Among Enterprises

Cloud penetration exceeded 70% of mid-market and large-enterprise installations in 2025. Average infrastructure cost fell 30% relative to on-premise, unlocking budget for advanced analytics talent while centralized data lakes enabled cross-functional dashboards. Subscription pricing converted multi-million-dollar upfront licenses into predictable annual operating expenses, bolstering uptake among organizations with constrained capital budgets. Despite latency sensitivities in transaction-intensive verticals, secure API gateways and regional data centers are easing compliance with GDPR and China’s PIPL. The net result is sustained momentum that enlarges the ERP with Embedded Analytics market footprint

Demand for Real-Time Data and Predictive Insights to Optimize Operations

Manufacturers are increasingly using IoT telemetry to predict equipment failures up to 72 hours in advance, reducing unplanned downtime by 40%.[1]Siemens, “IoT Integration in Manufacturing ERP Systems,” SIEMENS.COM Source: SAP, “Joule Agentic AI Capabilities,” SAP.COM Similarly, retailers and pharmaceutical companies are experiencing significant operational improvements, including faster replenishment cycles and reduced timelines for clinical-trial submissions. These advancements underscore the scalable, transformative value of embedded analytics across industries.

Integration of AI, ML and IoT Driving Embedded Analytics Capabilities

IoT-driven digital twins have significantly enhanced operational efficiency by enabling the simulation of supply shocks within hours, a process that previously required weeks. This advancement allows businesses to respond more swiftly to disruptions, ensuring better supply chain resilience. Additionally, natural-language queries are democratizing access to these technologies, empowering non-technical staff to leverage insights without requiring specialized expertise. Furthermore, edge computing processes data closer to its source, reducing bandwidth costs by 60% and enabling advanced analytics in facilities with intermittent connectivity, thereby expanding the reach of data-driven decision-making.

Shift Toward ESG and Sustainability Reporting Embedded Into ERP Analytics

Europe’s Corporate Sustainability Reporting Directive compels 50,000 firms to disclose emissions, spurring demand for built-in carbon ledgers that calculate supplier-level intensities.[2]European Commission, “Corporate Sustainability Reporting Directive,” EC.EUROPA.EU SAP’s Sustainability Control Tower already helps manufacturers trim footprints by up to 25%. Parallel SEC proposals in the United States and rising investor scrutiny are accelerating global adoption, cementing ESG analytics as a core differentiator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security and Privacy Concerns in Cloud ERP Deployments | -1.8% | Global, acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Implementation Complexity and Cost Overruns | -1.5% | Global, affecting mid-market enterprises | Medium term (2-4 years) |

| Shortage of Skilled Data Engineers for Embedded Analytics | -1.2% | Global, severe in emerging markets | Long term (≥ 4 years) |

| Vendor Lock-In Risks Limiting Analytics Flexibility | -0.9% | Global, in multi-vendor IT landscapes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns in Cloud ERP Deployments

High-profile breaches exposed 1.2 billion records across finance and healthcare during 2024, prompting 43% of enterprises to pause migrations pending stronger controls.[3]IBM Security, “Cloud Security Threat Landscape Report,” IBM.COM Multi-million-euro GDPR fines and data-localization laws are forcing region-specific instances that fragment analytics. Zero-trust architectures, immutable backups, and in-country data centers are now table stakes, but collectively raise subscription spend by up to 18%.

Implementation Complexity and Cost Overruns

Legacy integrations account for nearly half of project timelines, creating significant delays in project execution. Furthermore, resistance to change management processes and the challenges associated with data-quality remediation often postpone the go-live phase by several quarters, impacting overall project efficiency. To address these challenges, vendors are increasingly offering bundled industry accelerators designed to minimize the need for extensive customization. However, despite these strategic measures, service costs remain elevated, which continues to constrain growth momentum in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architectures Reconcile Sovereignty and Scale

Hybrid approaches, though smaller today, are projected to grow 18.00% annually, reflecting regulated enterprises that must keep sensitive assets on-premise. Banking players keep transaction ledgers locally for Basel III reporting while pushing operational analytics to the public cloud, an arrangement that trims infrastructure spending by 22%. In healthcare, HIPAA drives similar splits between clinical and non-clinical workloads.[4]U.S. Department of Health and Human Services, “HIPAA Compliance Guidelines,” HHS.GOV Edge computing augments these designs by processing sensor feeds at the factory floor before forwarding aggregated insights to central clouds, eliminating latency complaints and expanding the ERP's market appeal with Embedded Analytics.

Generative-AI training on proprietary data also favors hybrid topologies, with on-premises GPU clusters safeguarding intellectual property during model training while inference runs in elastically scaled cloud environments. Disaster-recovery imperatives reinforce the model, enabling failover from on-premises primaries to cloud replicas within minutes, ensuring uninterrupted analytics. API management complexity remains a stumbling block, so vendors now bundle managed gateways, typically priced at a 10-15% premium over base subscriptions.

By Component: Services Surge as Analytics Complexity Outpaces Packaged Software

Software still accounts for 68% of revenue, yet the fastest-growing segment will be implementation and integration services, with a 15.50% CAGR. Enterprises grapple with mainframe extraction, data-quality cleansing, and bespoke model development, funneling 30-40% of total budgets into system integrators. Migration specialists command USD 200-350 per hour, underscoring the scarcity of skills. Training and support lines are swelling because democratized analytics now touch sales, HR, and operations teams, adding sizable curriculum costs.

Managed services offerings that assume responsibility for updates, security, and tuning are emerging, typically 15-25% of license value. Custom algorithm development for vertical nuances. such as clinical-trial outcome prediction or asset-portfolio stress testing, creates fresh service revenue that rivals product income. As a result, the ERP with Embedded Analytics market is tilting toward service-led value capture.

By Enterprise Size: SMEs Leapfrog Legacy Constraints Through Cloud-Native Analytics

Large organizations retained 62% of 2025 revenue, while small and medium enterprises will be the fastest risers, with a 17.20% CAGR. Cloud-native platforms with pre-configured dashboards reduce roll-out to 90 days, enabling firms with annual revenue near USD 5 million to adopt enterprise-grade predictive tools once limited to Fortune-500 budgets. Subscription delivery eliminates the need for dedicated infrastructure staff, allowing SMEs to focus resources on data-driven growth initiatives.

Medium-size multinationals increasingly deploy two-tier strategies, using cloud ERP for subsidiaries while the headquarters maintains legacy systems, which in turn creates hunger for unified analytics across disparate instances. Price competition is driving user fees below USD 100 per month, lowering entry barriers and expanding the ERP with Embedded Analytics market size for this cohort.

By Function: HR Analytics Ascend as Workforce Planning Eclipses Headcount Tracking

Finance and accounting modules remain the anchor, with a 23% share, owing to statutory compliance requirements. Automated reconciliation shortened the month-end close from 10 to three days and freed finance staff for high-value variance analysis. Real-time profitability dashboards are enabling daily SKU-level margin decisions, accelerating resource reallocation.

Human-resources analytics grow fastest at 14.28% CAGR by predicting attrition with 78% accuracy, guiding targeted retention offers that save significantly per avoided departure. Skills-gap modeling steers training budgets toward strategic competencies, boosting on-time project delivery. Diversity dashboards surface inequities and mitigate litigation risk, while predictive labor models optimize workforce allocation in volatile demand environments, broadening the ERP with Embedded Analytics market opportunity.

By Industry Vertical: Healthcare Acceleration Outpaces Manufacturing Maturity

Manufacturing held 34% of 2025 revenue due to decades-long ERP entrenchment. IoT-driven digital twins now simulate supply disruptions within hours, cutting stoppages. Pharmaceutical plants that integrate trial data with shop-floor execution shave 6 to 9 months off regulatory submissions, reaping first-mover premiums.

Healthcare, growing at 16.80% CAGR, merges revenue-cycle and clinical-outcome data to curb per-patient spend, directly influencing reimbursement under value-based care schemes. Hospitals seek unified views across EHRs, procurement, and staffing, while strict privacy mandates drive demand for on-premises or hybrid deployments. Collectively, these forces expand the market share of the ERP with Embedded Analytics market for healthcare providers.

Geography Analysis

North America accounted for 37% of 2025 sales, buoyed by early generative AI adoption and deep cloud infrastructure. The United States captured almost three-quarters of regional turnover, aided by venture-capital-backed vendors that supply API-first products to mid-market buyers. Canada channeled federal digital budgets into bilingual cloud ERP roll-outs across agencies, while Mexico’s nearshoring wave compelled suppliers to adopt real-time visibility tools demanded by U.S. automotive OEMs.

Asia-Pacific is the fastest-growing region, with a 13.50% CAGR. China’s industrial digitization subsidies added 120,000 cloud ERP tenants in 2025, many of them small manufacturers navigating stringent data localization edicts. India’s production-linked incentive programs hinge on traceability, accelerating uptake among electronics and pharmaceutical exporters. Japan and South Korea embed IoT analytics into legacy systems to cut energy use by up to 22%, enhancing regional ERP adoption amid the Embedded Analytics market growth trajectory.

Europe held 28% share in 2025, with Germany’s Mittelstand upgrading platforms to satisfy ESG reporting, and the United Kingdom installing trade-compliance analytics to shave customs bottlenecks by up to 40%. South America earmarked USD 8 billion for public-sector ERP transformations, Brazil leading the charge by migrating 45 agencies to cloud suites. The Middle East funnels smart-city budgets into unified analytics that span utilities and transport, and Africa leverages mobile interfaces to circumvent desktop limitations, completing the global picture.

Competitive Landscape

The ERP with Embedded Analytics market is moderately concentrated. SAP, Oracle, and Microsoft embed generative-AI copilots that automate tasks such as variance investigations and supply-chain exception handling, stiffening switching costs even as open-source alternatives gain low-end traction. SAP’s Joule answered 2 million natural-language queries daily by late 2025, while Oracle patented autonomous anomaly-detection algorithms that self-tune without admin input.

Workday and Acumatica target mid-market displacements with pre-built industry accelerators, cutting deployment timelines from a year to three months and offering pricing 25-35% below incumbents. Odoo harnesses community-contributed modules to waive license fees for firms with sub-USD 50 million in revenue, capturing around 15% of that tier and proving disruptive at the low end. Technology differentiation is shifting toward agentic architectures that autonomously execute multi-step workflows, slashing processing costs by up to 60% and accelerating job completion to near-real-time.

Patent activity underscores the arms race: total embedded-analytics filings advanced 43% year over year in 2025, with SAP adding 22 patents for natural-language SQL generation and Oracle securing 18 patents focused on autonomous database tuning. Strategic acquisitions, such as Oracle’s purchase of Cerner and IFS’s buyout of Copperleaf, fuse domain data with core ERP workflows to deliver unified patient or asset analytics, tightening ecosystem control and expanding total addressable reach.

ERP With Embedded Analytics Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

The Sage Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Oracle finalized its USD 28.3 billion Cerner acquisition, merging EHR data with Fusion Cloud ERP to deliver unified clinical and financial analytics.

- January 2026: Microsoft extended Azure OpenAI Service into Dynamics 365, accelerating financial statement creation and demand forecasting, and helping early adopters close books 35% faster.

- January 2026: AP rolled out Joule Agentic AI across all S/4HANA Cloud modules, automating invoice reconciliation and variance investigation while integrating with Microsoft Teams and Slack for conversational access.

- November 2025: Infor and AWS committed USD 500 million to co-develop industry-specific cloud suites embedding predictive maintenance and dynamic pricing.

Global ERP With Embedded Analytics Market Report Scope

The ERP with Embedded Analytics market refers to the ecosystem of enterprise software solutions and associated services that integrate advanced analytics capabilities directly within Enterprise Resource Planning (ERP) systems, enabling real-time data analysis, reporting, and decision-making within core business workflows.

The ERP with Embedded Analytics Market Report is Segmented by Deployment Mode (Cloud, On-Premise, Hybrid), Component (Software, Implementation and Integration Services, Training and Support Services), Enterprise Size (Small, Medium, Large), Function (Finance and Accounting, Supply Chain, HR, Production Planning, CRM, Other), Industry Vertical (Manufacturing, BFSI, Healthcare, Retail, Government, IT and Telecom, Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Software |

| Implementation and Integration Services |

| Training and Support Services |

| Small Enterprises (1-99 Employees) |

| Medium Enterprises (100-999 Employees) |

| Large Enterprises (1,000+ Employees) |

| Manufacturing |

| Banking, Financial Services and Insurance |

| Healthcare |

| Retail and E-commerce |

| Government |

| IT and Telecom |

| Other Industry Verticals |

| Finance and Accounting |

| Supply Chain and Inventory Management |

| Human Resources |

| Production Planning and Scheduling |

| Customer Relationship Management |

| Other Functions |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Component | Software | |

| Implementation and Integration Services | ||

| Training and Support Services | ||

| By Enterprise Size | Small Enterprises (1-99 Employees) | |

| Medium Enterprises (100-999 Employees) | ||

| Large Enterprises (1,000+ Employees) | ||

| By Industry Vertical | Manufacturing | |

| Banking, Financial Services and Insurance | ||

| Healthcare | ||

| Retail and E-commerce | ||

| Government | ||

| IT and Telecom | ||

| Other Industry Verticals | ||

| By Function | Finance and Accounting | |

| Supply Chain and Inventory Management | ||

| Human Resources | ||

| Production Planning and Scheduling | ||

| Customer Relationship Management | ||

| Other Functions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the ERP with Embedded Analytics market projected to grow?

It is forecast to expand from USD 24.55 billion in 2026 to USD 48.44 billion by 2031, reflecting a 14.55% CAGR.

Which deployment model is expected to rise the quickest?

Hybrid architectures combining on-premise and cloud components are set to grow at an 18.00% CAGR as firms balance data sovereignty with scalability.

What is the biggest restraint for new ERP with Embedded Analytics projects?

Data security and privacy concerns remain the chief barrier, trimming the forecast CAGR by an estimated 1.8%.

Which enterprise segment is fueling the next wave of demand?

Small and medium enterprises will grow at a 17.20% CAGR thanks to subscription pricing and pre-configured analytics templates.

Why are services revenue outpacing software growth?

Complex data migration, customization and training requirements are driving a 15.50% CAGR in implementation and integration services.

Which region will post the fastest growth through 2031?

Asia-Pacific is projected to lead with a 13.50% CAGR, underpinned by government digitization mandates and Industry 4.0 investments.

Page last updated on: