Enterprise Resource Planning Upgrade And Migration Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.97 Billion |

| Market Size (2031) | USD 10.04 Billion |

| Growth Rate (2026 - 2031) | 10.98% CAGR |

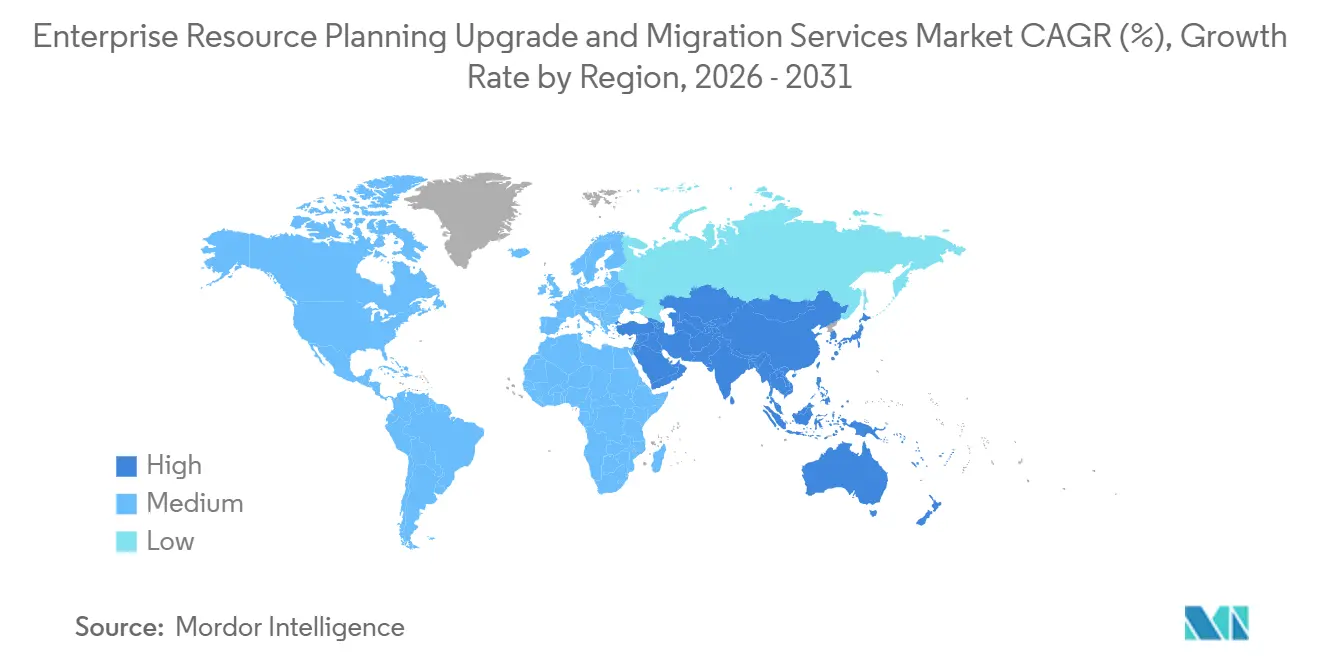

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Resource Planning Upgrade And Migration Services Market Analysis by Mordor Intelligence

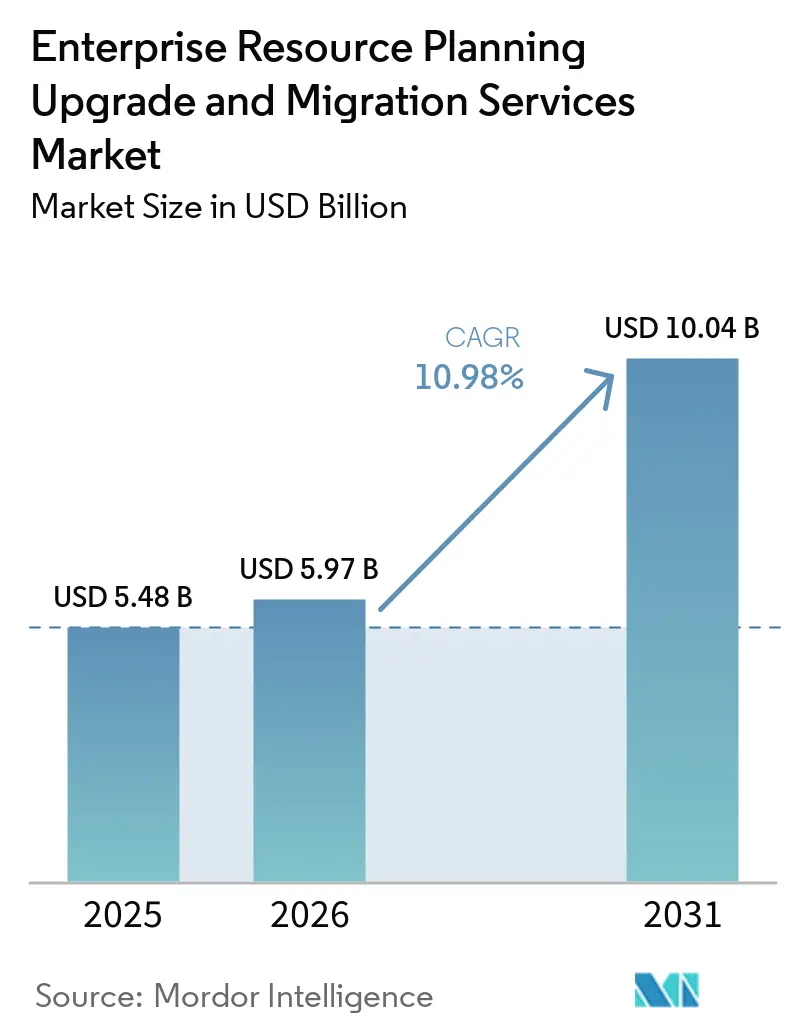

The ERP upgrade and migration services market size is projected to be USD 5.48 billion in 2025, USD 5.97 billion in 2026, and reach USD 10.04 billion by 2031, growing at a CAGR of 10.98% from 2026 to 2031. Enterprises that postponed modernization during the pandemic are now compressing multi-year road maps into 18-to-24-month programs as vendor end-of-support deadlines converge, pushing demand for rapid cloud migrations. Cloud deployments already dominate, vendors are packaging industry-specific templates to shrink customization effort, and low-code migration toolkits are lowering the skills barrier. Heightened regulatory focus on data residency, together with sizable vendor infrastructure investments across Asia-Pacific, is widening the addressable base of regulated industries. Consolidation among global system integrators and boutique specialists is creating one-stop shops that promise lower execution risk and faster time-to-value for large transformation mandates.

Key Report Takeaways

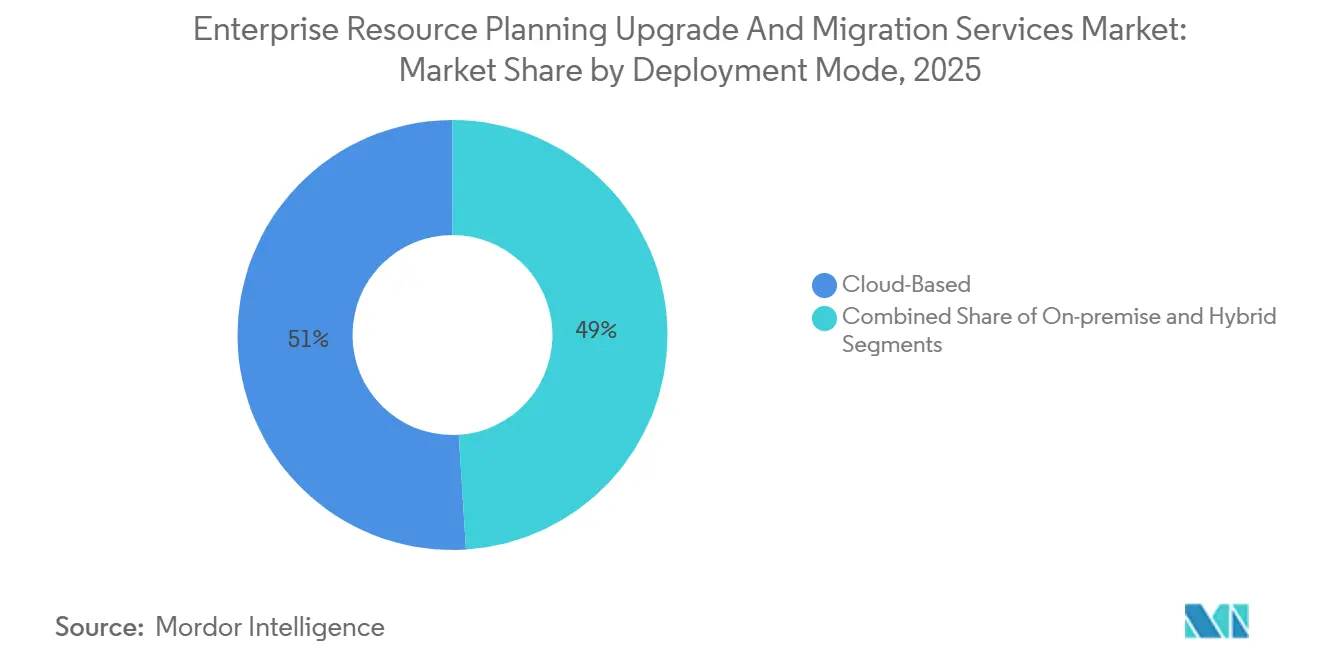

- By deployment model, cloud captured 51% of ERP upgrade and migration services market share in 2025 and is projected to advance at an 18.4% CAGR through 2031.

- By organization size, large enterprises accounted for 62% of 2025 revenue, while small and medium enterprises are forecast to expand at a 15.2% CAGR through 2031.

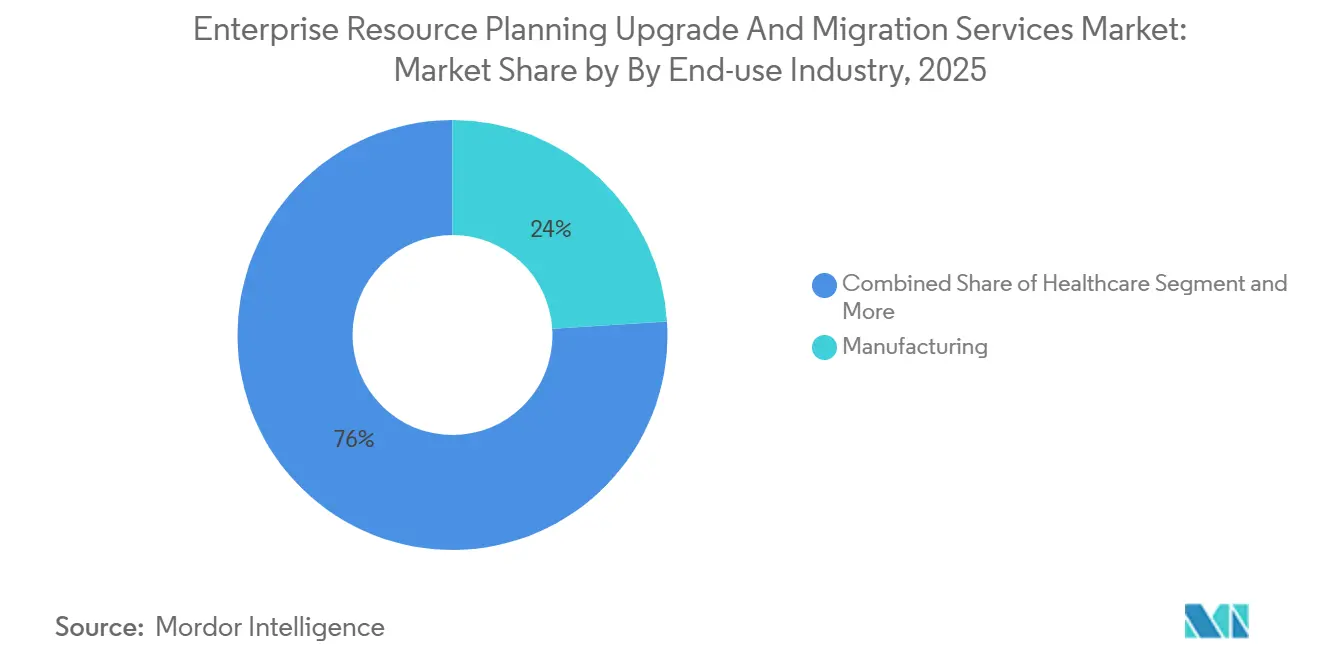

- By industry vertical, manufacturing led with 24% of 2025 revenue, whereas healthcare is expected to post the fastest 14.7% CAGR during 2026-2031.

- By geography, North America accounted for 34.5% of 2025 revenue, yet Asia-Pacific is on track to record a 13.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Resource Planning Upgrade And Migration Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Post-Pandemic Digital Resilience | +2.8% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Accelerated Shift to Cloud-First ERP Architectures | +3.5% | Global, Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Vendor-Induced End-of-Support Deadlines | +2.1% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Increasing Adoption of Industry-Specific Templates | +1.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Availability of Low-Code Migration Toolkits | +0.9% | Global, higher uptake in developed markets | Medium term (2-4 years) |

| Growing Near-Zero-Downtime Methodologies | +0.3% | Global, prioritized by 24 / 7 BFSI and e-commerce operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Post-Pandemic Digital Resilience

Organizations that endured supply-chain shocks and prolonged remote work between 2020 and 2023 concluded that on-premises ERP lacked the elasticity required for rapid reconfiguration. The imperative for resilience is accelerating cloud uptake, with 70.4% of deployments already cloud-based by 2024.[1]SAP SE, “SAP ECC Support, What You Need to Know,” SAP Community, sap.com Manufacturing firms are embedding IoT sensors in S/4HANA to predict maintenance needs, while retailers use real-time stock analytics to cut stockouts by 20-30%.[2]Epicor, “Kinetic 2025 Release IoT Integration,” Epicor, epicor.com Financial institutions are shifting liquidity dashboards to cloud-native cores that integrate seamlessly with payment gateways. North America and Europe lead adoption, yet Asia-Pacific is closing the gap as government incentive programs offset infrastructure costs.

Accelerated Shift to Cloud-First ERP Architectures

Cloud ERP’s five-year total cost of ownership is 30-40% lower than comparable on-premises estates when hardware refreshes, database licenses, and internal labor are factored in.[3]Oracle Corporation, “What Is ERP?,” Oracle, oracle.com SME enthusiasm is high, 70% prefer cloud solutions, and platforms such as Odoo added 13,000 clients per month in 2025.[4]Odoo SA, “Odoo Experience 2025 Highlights,” Odoo, odoo.com Hybrid designs persist in risk-averse sectors but mainly serve as transition architectures. Asia-Pacific momentum is underpinned by a USD 8 billion Oracle data-center buildout in Japan that guarantees sub-10-millisecond latency for domestic users. Data-sovereignty statutes like GDPR and PDPL make in-country cloud zones a prerequisite for regulated workloads, reinforcing the long-term shift.

Vendor-Induced End-of-Support Deadlines

SAP will end mainstream support for ECC on 31 December 2027, yet only about 25% of installations had migrated by 2024. The looming cut-off presses enterprises to avoid security, compatibility, and feature deficits. Oracle’s phased retirement of E-Business Suite nudges customers toward Fusion Cloud, sometimes with fee incentives. A mid-sized S/4HANA migration can cost USD 150,000-USD 750,000, whereas global conversions may exceed USD 50 million. System integrators respond with fixed-price accelerators that trim timelines to under 12 months.

Increasing Adoption of Industry-Specific ERP Templates

Pre-configured templates such as SAP Model Company for discrete manufacturing and Oracle Industry Cloud for banking shave 40-60% off build times. Templates ship with best-practice workflows, manufacturing kits include ISO-aligned quality checkpoints, while healthcare blueprints align admission flows with HIPAA transaction sets. Infor CloudSuite editions extend the model with tax, language, and regulatory logic for 40 countries. Uptake is strongest in North America and Europe, but is spreading as Indian and Japanese integrators localize templates for GST and electronic invoicing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for Upgrades | -1.8% | Global, acute in cost-sensitive SME and emerging markets | Short term (≤ 2 years) |

| Shortage of Certified ERP Migration Specialists | -1.2% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Security Concerns in Hybrid and Multi-Cloud Deployments | -0.7% | Global, heightened in regulated industries | Long term (≥ 4 years) |

| Integration Complexities with Legacy Customizations | -0.9% | Global, concentrated in long-tenure ERP estates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for Large-Scale Upgrades

Project budgets remain front-loaded: midsized migrations cost USD 150,000-USD 750,000 and enterprise programs can exceed USD 50 million. Hidden overruns in data quality and custom code can inflate totals by 30%. SMEs mitigate shock with phased rollouts or modular cloud suites starting below USD 50,000. Currency volatility and limited financing options in Africa and South America further constrain uptake. Compliance add-ons—GDPR hosting, HIPAA controls—consume an extra 10-15% of budgets.

Shortage of Certified ERP Migration Specialists

Seventy percent of enterprises report difficulty hiring SAP-certified talent, and senior vacancies remain open for over 60 days. Korn Ferry warns of 85 million unfilled tech roles globally by 2030. Salary premiums of 15-25% are common, driving integrators to shift routine tasks to India and Eastern Europe while keeping process-redesign roles onshore. Government programs such as Singapore’s SkillsFuture co-fund certifications, yet demand continues to outstrip supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Architectures Reshape Total Cost Equations

Cloud deployments captured 51% of the ERP upgrade and migration services market share in 2025, and this segment is advancing at a 18.4% CAGR through 2031, making it the structural growth engine of the ERP upgrade and migration services market. Subscription pricing removes data-center capital outlays, and quarterly vendor releases replace costly version-upgrade projects, shifting spend toward value-added extensions. SMEs embrace pure-cloud suites that go live within six months, while large enterprises often start with infrastructure-as-a-service “lift and shift” moves before refactoring to cloud-native designs.

Hybrid models bridge risk-averse organizations to the cloud, keeping finance cores on-premises while offloading analytics or HCM modules. This dual-state architecture complicates data synchronization and raises support costs by 10-15%, but remains preferable to disruptive rip-and-replace tactics. On-premises estates now represent legacy holdouts in sectors such as defense and critical infrastructure, where latency or sovereignty overrides economics. The ERP upgrade and migration services market continues to reward vendors that provide zero-downtime migration tooling and automated regression testing that protect production uptime during cutovers.

By Organization Size: SMEs Close the Capability Gap

Large enterprises accounted for 62% of 2025 revenue, yet SME adoption is growing faster at a 15.2% CAGR, progressively lifting the overall ERP upgrade and migration services market. Pay-as-you-go cloud suites priced from USD 50 per user per month remove historical budget barriers, enabling SMEs to deploy real-time consolidation, demand planning, and embedded analytics once reserved for billion-dollar companies. Low-code builders such as SAP Build and Microsoft Power Platform empower business users to tailor workflows without scarce ABAP or PL/SQL talent, trimming maintenance costs by 30-40%.

Conversely, multinational corporations value global support, deep vertical functionality, and multi-currency consolidation, steering them toward SAP S/4HANA, Oracle Fusion Cloud, or Microsoft Dynamics 365 Finance. Their migrations span dozens of entities, require phased rollouts, and often exceed USD 10 million in budget. Despite different entry points, both cohorts converge on a need for continuous innovation, driving managed-services contracts that bundle upgrades with evergreen optimization. The bifurcated demand profile underpins sustained growth across the ERP upgrade and migration services market.

By Industry Vertical: Manufacturing Leads, Healthcare Accelerates

Manufacturing contributed 24% of 2025 revenue, the largest slice of the ERP upgrade and migration services market size, reflecting early ERP penetration and current Industry 4.0 modernization. Factories integrate IoT telemetry with S/4HANA for predictive maintenance, improving overall equipment effectiveness. Digital twins and machine learning for demand forecasting are increasingly bundled into migration scopes to justify investment.

Healthcare, growing at a 14.7% CAGR, is racing to modernize billing, electronic health records, and regulatory reporting workflows mandated by HIPAA and emerging interoperability rules. Cloud-native templates shorten deployment and embed compliance checks such as 21 CFR Part 11 electronic signatures. Banking, retail, government, telecom, and energy thereafter round out demand, each with niche functional requirements, from Basel III liquidity dashboards to omnichannel inventory sync, keeping service providers busy across multiple value chains.

Geography Analysis

North America retained 34.5% of 2025 revenue thanks to the world’s densest population of legacy SAP and Oracle estates and a mature consulting ecosystem. Growth is propelled by the approaching 2027 SAP ECC deadline, reshoring initiatives in manufacturing, and healthcare consolidation. Canada and Mexico add incremental demand tied to USMCA supply chains, particularly in automotive and agribusiness.

Asia-Pacific is the fastest-growing region at 13.9% CAGR through 2031, driven by Digital India, Made in China 2025, and Japan’s Digital Garden City Nation funding that subsidizes municipal cloud ERP upgrades. Oracle’s USD 8 billion infrastructure pledge in Japan and SAP partnerships with NTT Data and Fujitsu ensure local data residency, a prerequisite under Japan’s privacy statutes. Although state-owned Chinese firms often select domestic vendors for sovereignty reasons, multinationals rely on SAP and Oracle for harmonized global processes.

Europe’s trajectory is shaped by GDPR, MiFID II, and medical-device regulations that favor compliance-ready templates. Germany leads spend among Mittelstand manufacturers, followed by the United Kingdom and France. The Middle East, led by Saudi Arabia and the United Arab Emirates, channels oil-diversification funds into large-scale ERP modernization; PDPL data-localization rules stimulate local cloud zones. Africa and South America, though smaller, are leapfrogging on-premises stages by adopting mobile-first cloud ERP in fintech and agriculture, aided by improving broadband coverage and competitive hyperscale pricing.

Competitive Landscape

The top 10 providers account for arounf half of aggregate revenue, indicating moderate concentration in the ERP upgrade and migration services market. Accenture, IBM, Deloitte, and Capgemini leverage strategy through operational skill sets, proprietary migration accelerators, and multi-year managed services deals valued at up to USD 100 million. Indian firms TCS, Infosys, Wipro, and Cognizant compete on blended onsite-offshore staffing, delivering 30-40% cost savings relative to Western peers. Vendor-captive units from SAP, Oracle, and Infor attract clients seeking single-throat-to-choke accountability but typically command premium rates.

Consolidation is accelerating: Capgemini acquired Syniti and Cloud4C in 2024, while AttivoERP acquired Acuity in March 2026 to deepen its NetSuite and Dynamics 365 skills. Private-equity interest is high in regional specialists that own repeatable data-migration tooling or near-zero-downtime cutover scripts. Technology shifts are also redistributing value; automated migration platforms from Syniti and Precisely cut manual data mapping by up to 70%, pushing integrators to emphasize advisory and change-management services.

White-space opportunities persist in mid-market Asia-Pacific and South America where deal sizes of USD 0.5-2 million are too small for global majors yet too complex for local boutiques. Low-code, template-driven delivery lowers entry barriers for challengers. Meanwhile, talent scarcity has integrators investing heavily in certification academies and AI-assisted code remediation tools to sustain margins.

Enterprise Resource Planning Upgrade And Migration Services Industry Leaders

Accenture plc

IBM Corporation

Deloitte Touche Tohmatsu Limited

Capgemini SE

Cognizant Technology Solutions Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AttivoERP acquired Acuity, adding 50 consultants and banking expertise to its North American practice.

- March 2026: UiPath and Deloitte unveiled Agentic ERP, an AI automation layer that executes routine SAP and Oracle transactions autonomously.

- November 2025: TCS won a five-year managed-services contract to migrate a global telecom operator to SAP S/4HANA Cloud.

- October 2025: Tamilnad Mercantile Bank completed a 10-month Oracle Fusion Cloud migration that cut month-end close from seven to two days.

Global Enterprise Resource Planning Upgrade And Migration Services Market Report Scope

The ERP Upgrade and Migration Services market comprises specialized services that enable organizations to modernize, transition, and optimize their existing Enterprise Resource Planning (ERP) systems by upgrading legacy systems or migrating to new platforms, architectures, or deployment environments.

The ERP Upgrade and Migration Services Market Report is Segmented by Deployment Model (On-Premises, Cloud-Based, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (Manufacturing, BFSI, Retail, Healthcare, Government, IT and Telecom, Energy, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are in Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-Commerce |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Information Technology and Telecom |

| Government and Public Sector |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Mode | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-Use Industry | Manufacturing | |

| Retail and E-Commerce | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare | ||

| Information Technology and Telecom | ||

| Government and Public Sector | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the ERP Upgrade and Migration Services market by 2031?

The market is forecast to reach USD 10.04 billion by 2031 growing at a CAGR of 10.98% during the forecast period of 2026-2031..

How large is the ERP upgrade and migration services market in 2026?

The ERP upgrade and migration services market size stands at USD 5.97 billion in 2026.

Which region is expected to grow the fastest through 2031?

Asia-Pacific, expanding at a 13.9% CAGR, is the fastest-growing geography.

Why are small and medium enterprises adopting cloud ERP rapidly?

Subscription pricing, low-code configuration, and template-based deployments reduce capital outlay and time-to-value for SMEs.

What are the biggest challenges in large-scale ERP migrations?

High upfront costs, a shortage of certified specialists, and complex legacy customizations pose the greatest hurdles.

Which deployment model dominates current spending?

Cloud deployments lead with 51% of 2025 revenue and continue to outpace on-premises and hybrid alternatives.

Page last updated on: