Tax Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

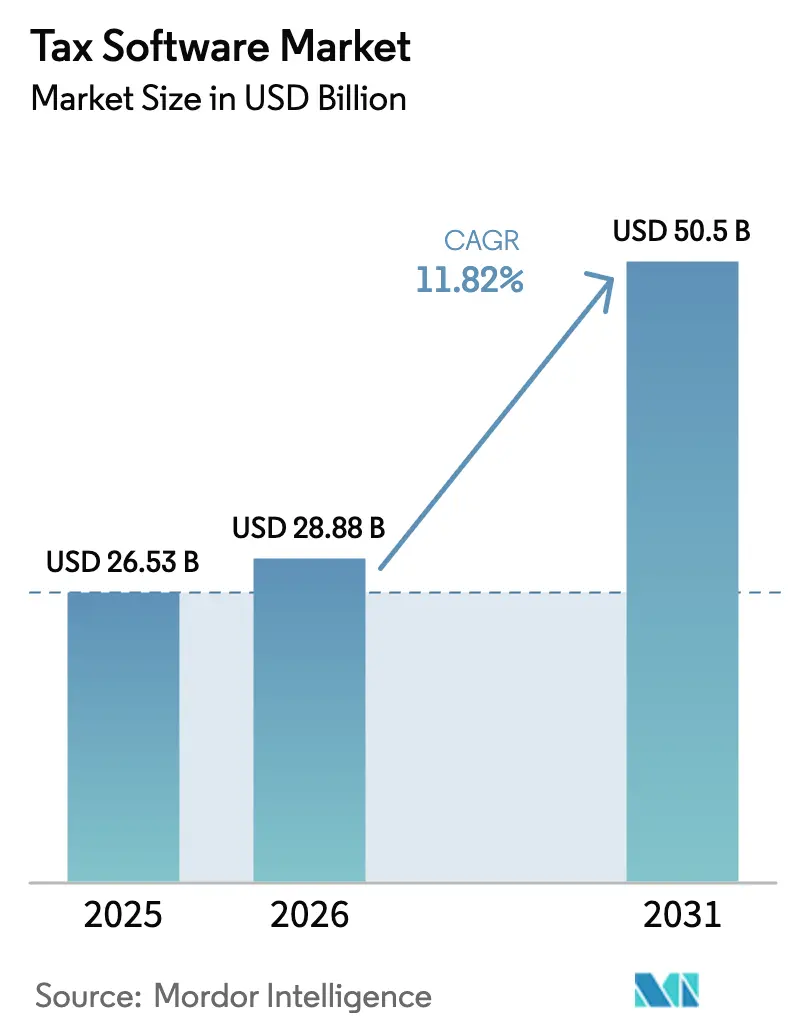

| Market Size (2026) | USD 28.88 Billion |

| Market Size (2031) | USD 50.5 Billion |

| Growth Rate (2026 - 2031) | 11.82% CAGR |

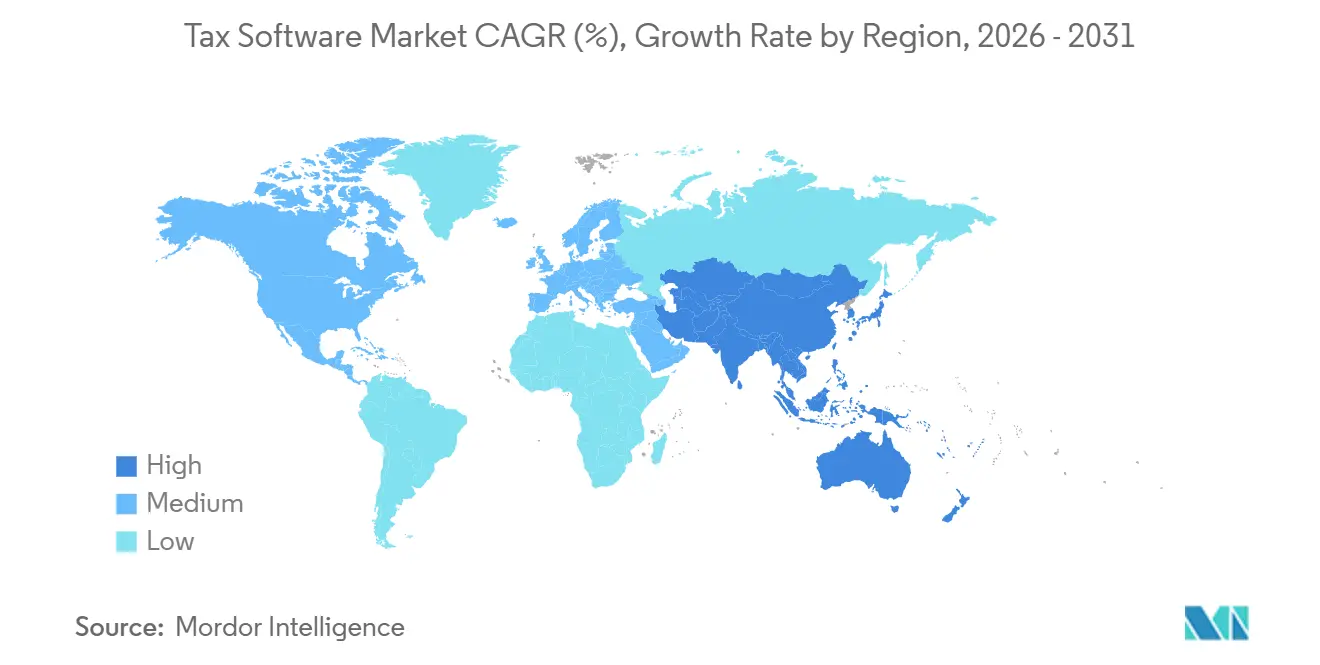

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

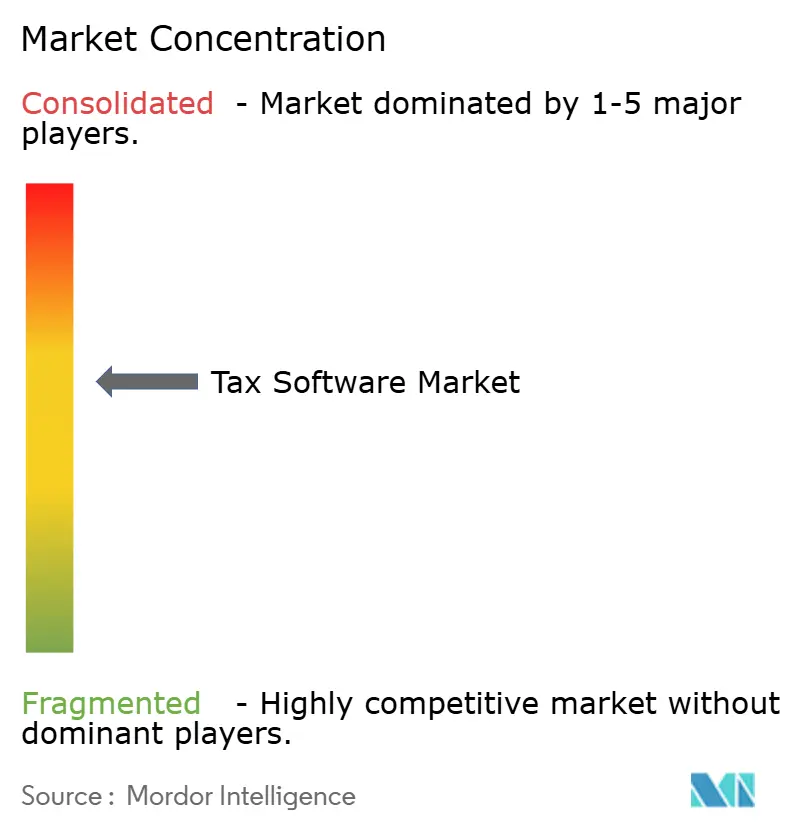

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tax Software Market Analysis by Mordor Intelligence

The tax software market size was valued at USD 26.53 billion in 2025 and estimated to grow from USD 28.88 billion in 2026 to reach USD 50.50 billion by 2031, at a CAGR of 11.82% during the forecast period (2026-2031). Demand is shifting from periodic, form-based compliance to always-on, API-connected workflows that sit inside enterprise resource-planning and payment systems. Cloud deployment already dominates because real-time invoice reporting frameworks, introduced across Europe and Asia-Pacific, cannot be met by legacy architectures. Artificial-intelligence modules now draft memos, classify transactions and predict audit risk, reducing preparation cycles and widening adoption among resource-constrained small businesses. Vendor competition therefore hinges on the depth of AI automation, the breadth of localized rule content, and the scale economies that come from multi-tenant hosting.

Key Report Takeaways

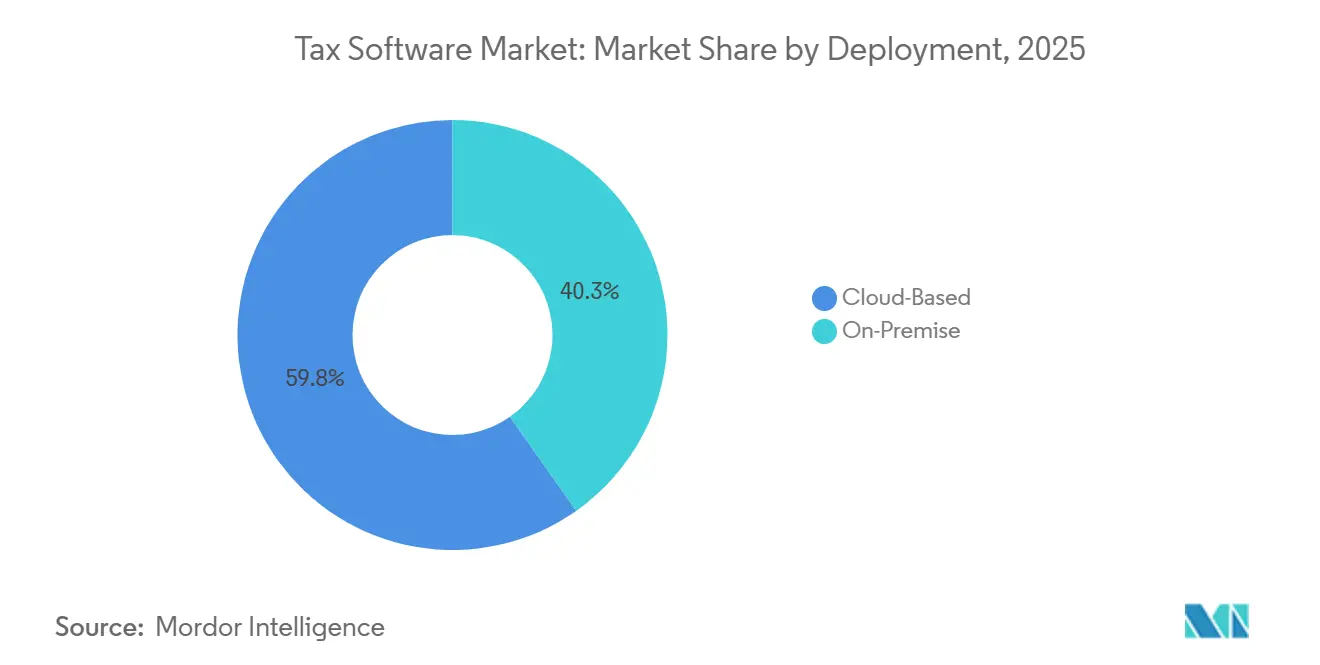

- By deployment, cloud captured 59.75% of 2025 revenue while on-premise lags; cloud is projected to expand at a 13.61% CAGR through 2031.

- By enterprise size, large enterprises held 55.53% share in 2025, whereas small and medium enterprises are forecast to grow at a 9.90% CAGR as low-cost SaaS tiers proliferate.

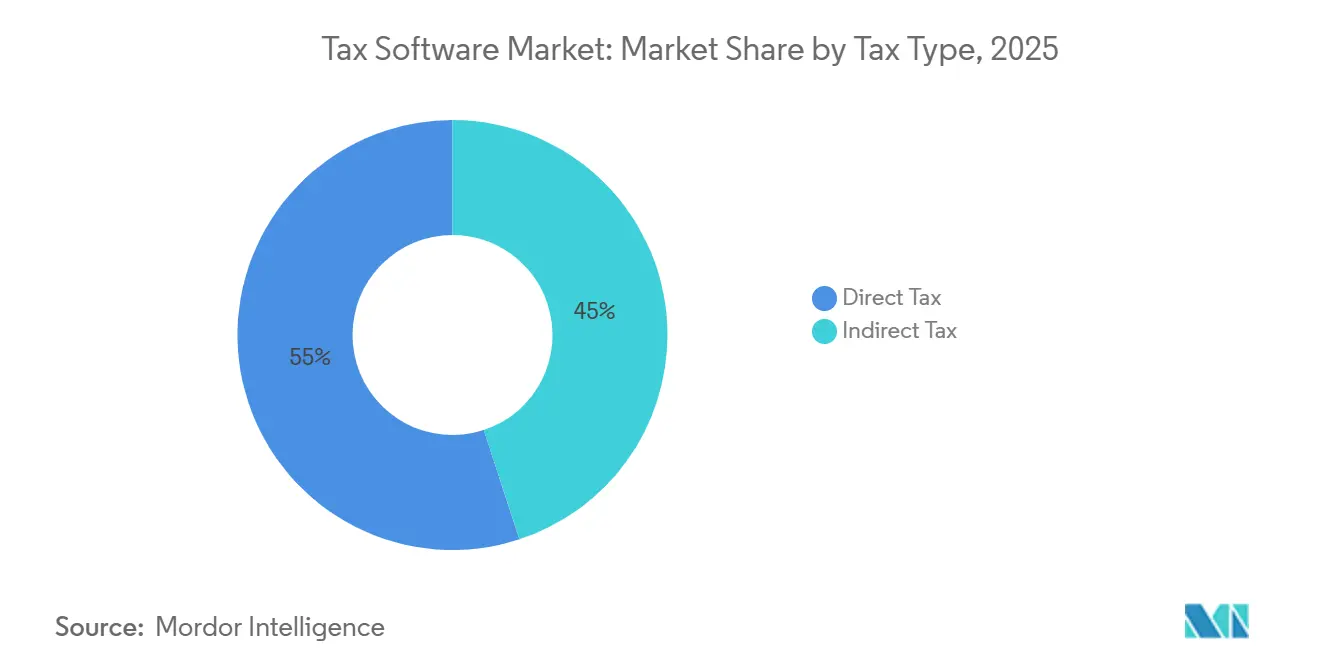

- By tax type, direct tax software led with 55.04% of 2025 spending, yet indirect tax offerings are expected to advance at a 14.80% CAGR to 2031.

- By end-user, individuals accounted for 17.53% of 2025 revenue, while small businesses are set to rise at a 13.70% CAGR on the back of e-invoicing mandates.

- By geography, North America held 37.95% of 2025 revenue and Asia-Pacific is anticipated to post a 15.64% CAGR, making it the fastest-growing region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tax Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Native SaaS Tax Engines | +3.5% | Global, with North America and Europe leading; rapid uptake in Asia-Pacific urban centers | Medium term (2-4 years) |

| Shift Toward Real-Time Digital Tax Reporting (e-Invoicing and SAF-T Mandates) | +2.8% | Europe (France, Germany, Poland), Asia-Pacific (India, China, South Korea), Latin America (Brazil, Mexico) | Short term (≤ 2 years) |

| Expansion of E-Commerce Creating Complex Cross-Border Indirect-Tax Needs | +2.2% | Global, with concentration in Europe (OSS/IOSS), North America (marketplace facilitator laws), Asia-Pacific (GST harmonization) | Medium term (2-4 years) |

| Integration of AI-Driven Error Detection and Predictive Audit Flags | +1.8% | North America and Europe early adopters; Asia-Pacific following in 2027-2028 | Long term (≥ 4 years) |

| Government APIs for Pre-Filled Returns (OECD "Tax Admin 3.0" Vision) | +0.9% | OECD member states, select Asia-Pacific nations (Singapore, South Korea, Australia) | Long term (≥ 4 years) |

| ESG-Linked Tax Transparency and Country-by-Country Reporting Demand | +0.6% | Europe (public CbCR for €750M+ firms), North America (IRS Form 8975), multinational enterprises globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud-Native SaaS Tax Engines

Cloud-native architectures decouple tax logic from enterprise resource cores, allowing vendors to push legal updates within hours rather than quarterly cycles. A January 2026 launch embedded micro-services that ingest legislative feeds and auto-generate calculation scripts, cutting configuration work from weeks to days.[1]Thomson Reuters, “ONESOURCE AI Launch,” Thomson Reuters, THOMSONREUTERS.COM Subscription economics replace capital purchase with predictable operating spend, and multi-tenant hosting averages 60-70% gross margins that on-premise rivals struggle to match. Real-time invoice rules in France for September 2026 and Germany for January 2027 effectively force SaaS connectivity for mid-market and enterprise taxpayers.[2]European Commission, “ViDA and E-Invoicing Timelines,” EC, EC.EUROPA.EU The result is an expanding installed base, especially among small businesses that cannot fund a dedicated IT stack.

Shift Toward Real-Time Digital Tax Reporting (e-Invoicing and SAF-T Mandates)

Governments now close value-added tax gaps by linking supplier and buyer invoices within seconds of issuance. Poland’s SAF-T JPK_V7M file set, refined through 2025, trimmed its VAT gap by 12 percentage points. India lowered the goods-and-services-tax e-invoice threshold to INR 5 crore (USD 0.60 million) in 2023 and extended a 30-day reporting limit to firms above INR 10 crore (USD 1.20 million) in 2025. Brazil’s 2026 reform merged five indirect levies into three and mandated a nationwide e-invoice, with over 1 280 municipalities already connected. Saudi Arabia logged 8.2 billion e-invoices in 2025 after its second implementation phase. These timelines compress vendor roadmaps, ensuring that cloud platforms replace desktop tools across compliant enterprises.

Expansion of E-Commerce Creating Complex Cross-Border Indirect-Tax Needs

Digital merchants face 170-plus VAT and GST regimes, each with rate tables, thresholds and filing portals. A European seller must apply destination-based VAT under the One-Stop Shop or the Import One-Stop Shop. United Kingdom legislation in October 2024 shifted liability to marketplaces, driving large platforms to embed automated rate engines. Economic-nexus thresholds diverge- USD 100,000 in several U.S. states, AUD 75,000 (USD 48.000) in Australia, and province-specific tests in Canada.[3]PwC Indirect-Tax Team, “Economic Nexus Thresholds,” PwC, PWC.COM Plugins from Avalara and Vertex now process millions of daily transactions, an approach that netted more than USD 500 million combined subscription revenue in 2025.

Integration of AI-Driven Error Detection and Predictive Audit Flags

Generative models have moved tax software from passive calculators to proactive advisors. An agentic workflow launched in January 2026 scans contractor invoices, flags missing W-9 forms, and drafts IRS-compliant 1099 filings without manual review. Machine-learning modules that predict which line items will attract examiner scrutiny reduced settlement costs for early adopters by 20-30%. Optical-character-recognition accuracy tops 95% for structured invoices, and auto-reconciliation reaches 98% match rates when bank-feed APIs are present. Regulatory standards for AI-generated records remain under discussion, but productivity gains are already influencing buying criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented, Frequently Changing Local Tax Codes in Emerging Economies | -1.5% | Latin America (Brazil, Argentina), Africa (Nigeria, Kenya), Southeast Asia (Indonesia, Vietnam) | Short term (≤ 2 years) |

| Cyber-Security and Data-Sovereignty Concerns in Multi-Tenant Environments | -1.2% | Europe (GDPR enforcement), China (data-localization laws), Middle East (regulatory uncertainty) | Medium term (2-4 years) |

| High Switching Costs from Legacy On-Premise Systems | -0.8% | North America and Europe large enterprises with customized ERP integrations | Medium term (2-4 years) |

| Shortage of Domain-Skilled Developers for Tax Rule Engines | -0.5% | Global, with acute pressure in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented, Frequently Changing Local Tax Codes in Emerging Economies

Post-reform, Brazil assigns rate-setting powers to 27 states and more than 5 500 municipalities, forcing vendors to maintain content continuously, which inflates localization costs.[4]SAP Localization Hub, “Brazil Indirect-Tax Reform,” SAP, SAP.COM Argentina’s provincial gross-receipts taxes publish amendments only through non-machine-readable gazettes, delaying software updates. Nigeria stalled its nationwide e-invoice rollout in 2025, leaving developers uncertain over final schemas. Each deviation pushes small enterprises back to manual filings, slowing the penetration of tax software in high-growth regions.

Cyber-Security and Data-Sovereignty Concerns in Multi-Tenant Environments

Sensitive income and payroll files make tax platforms an attractive target: the average data breach now costs USD 4.88 million and takes 292 days to detect. General Data Protection Regulation enforcement in Europe levied more than EUR 2 billion (USD 2.12 billion) of fines in 2025 for inadequate safeguards. China prohibits cross-border transfers of tax records without explicit authorization, compelling global vendors to host in-country and exposing source code to regulatory review. These realities deter risk-averse enterprises and add 15-20% to infrastructure expense as platforms pursue SOC 2 and ISO 27001 certificates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates Amid API Mandates

Cloud solutions accounted for 59.75% of 2025 revenue, representing the largest tax software market share within deployment models, and remain on pace for a 13.61% CAGR to 2031 as governments replace web-form portals with API-only gateways. The tax software market size for on-premise installations continues to grow more slowly because certified platforms are now the sole conduit for French and German e-invoices. Organizations value elastic compute that scales during quarterly closes without permanent capital outlay, while subscription models align vendor income with customer retention.

Hybrid approaches persist in defense, utilities, and finance, where data-sovereignty rules block public-cloud use; vendors offer containerized engines that reconcile locally yet transmit filings through secure endpoints. However, feature parity is sliding toward cloud releases first, leaving on-premise users to wait months for AI modules, collaborative dashboards, and micro-service rule updates. Industry consensus expects on-premise tax engines to narrow to niche, high-security workloads before the end of the decade.

By Enterprise Size: SMEs Drive Volume Growth Through Affordable SaaS Tiers

Large enterprises delivered 55.53% of 2025 revenue, reflecting high seat counts and multi-entity licenses, but small and medium enterprises lead future unit growth. Entry-level bundles priced below USD 50 per month now automate bookkeeping, payroll and GST filing, erasing the need for hired preparers among freelancers and micro-shops. The tax software market size for SMEs benefits from subsidy programs such as India’s GSTN vouchers, which offset first-year subscription costs.

SME adoption reduces illegal cash economy activity, expanding the overall addressable tax software market. Meanwhile, enterprise customers seek deeper integrations with SAP, Oracle and Microsoft Dynamics to keep complex transfer-pricing and Pillar Two calculations inside the finance stack. ONESOURCE AI and Vertex O Series differentiate on agentic natural-language queries and certified security attestations, attributes that sustain premium margins even as SaaS pricing compresses.

By Tax Type: Indirect Tax Surges on Cross-Border Complexity

Direct tax platforms held 55.04% of 2025 spending, the leading tax software market share by tax category, but the indirect tax software market is expanding faster, projected to grow at a 14.80% CAGR. Real-time rate lookups, marketplace-facilitator rules, and import-VAT thresholds together create mathematical layers beyond the reach of spreadsheet methods.

Platform providers responded with microservices that perform nexus determination, capture exchange rates, and map line items down to the SKU level. Continuous government rule releases mean that rate tables for more than 170 jurisdictions update daily, an operational tempo only achievable in cloud environments. As a result, indirect tax features command premium subscription tiers even among micro-merchants.

By End-User: Small Businesses Outpace Individuals as Complexity Rises

Individuals generated 17.53% of 2025 revenue but confront free-file alliances and expanding government pre-fill services that erode basic-return fees. Conversely, small businesses experience double-digit compliance events each month, from invoice issuance to payroll accruals, driving a 13.70% CAGR that outpaces every other user segment.

Vendors now embed freelancer APIs, point-of-sale connectors, and payment-provider data streams, automating Schedule C, Form 1099, and e-invoicing in one workflow. Accounting practices of two to ten staff adopt collaborative suites, lifting revenue per employee by up to 70%. Enterprise taxpayers still anchor high-margin consulting, but volume growth belongs to the digital micro-business.

Geography Analysis

North America accounted for 37.95% of 2025 revenue, driven by the USD 4 trillion federal tax collection ecosystem, yet growth trails the global average as cloud penetration nears maturity. The Internal Revenue Service's pilot of API-based wage imports and a broadened Free File program reduce consumer software fees but unlock advisory opportunities for vendors able to monetize scenario planning. Canada’s automatic data retrieval for simple filers follows the same pattern, trimming entry-level demand while sustaining enterprise indirect-tax spending linked to cross-border sales.

Asia-Pacific is the fastest-moving region, set to post a 15.64% CAGR as mandatory e-invoicing rolls across India, China, South Korea, and the ASEAN bloc. India’s 30-day invoice-report rule added more than two million registrants in 2025, and China’s Golden Tax System Phase IV now cross-references VAT, customs, and social-insurance data in real time. Japan’s Peppol pilot among ministries creates a blueprint for B2G adoption, while Australia’s Single Touch Payroll Phase 3 increases the volume of pre-filled individual returns by 60%. Vendors localize quickly through low-code rule builders and joint ventures with domestic fintechs.

Europe presents a mixed picture, mature markets such as the United Kingdom, Germany and France already exhibit high cloud penetration, yet fresh mandates like Germany’s January 2027 ViDA requirement foment a replacement cycle. Eastern and Southern members accelerate SAF-T deployments after Poland cut its VAT gap through near-real-time invoice matching. South America gains momentum on the back of Brazil’s January 2026 indirect-tax consolidation, which compels enterprises to adopt certified software across 1,280 municipalities. Middle East and Africa remain fragmented, though Saudi Arabia processed 8.2 billion e-invoices in 2025 and the United Arab Emirates launched a pilot covering 300 large taxpayers.

Competitive Landscape

The tax software market shows moderate concentration; the five leading vendors command roughly half the combined share, leaving room for specialists and regional challengers. Incumbents leverage brand equity and decades-long client relationships but now race to embed generative AI copilots across their suites. One provider filed a patent for a natural-language interface in January 2026, signaling a coming battle over intellectual property in AI-driven workflows.

Strategic spend on foundation-model partnerships already exceeds USD 100 million per year for the top consumer-focused platform, which integrates conversational guidance, audit-risk scoring, and deduction suggestions across its tax, accounting, and payroll lines. Regional specialists differentiate through hyper-local rule content and offline-capable mobile apps aimed at informal traders without persistent connectivity.

White-space niches include microenterprises in emerging economies, cross-border freelancers, and mid-sized accounting practices seeking an all-in-one client collaboration platform. Vendors use low-code configurators to localize in under four weeks, bypassing years of traditional development. Security attestations-SOC 2, ISO 27001 and data-residency options-have become table stakes, adding 15-20% to infrastructure spend but unlocking deals in regulated industries.

Tax Software Industry Leaders

Intuit Inc.

Wolters Kluwer N.V.

Thomson Reuters Corporation

Sage Group plc

H&R Block Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Xendoo acquired Botkeeper to embed automated transaction categorization and accelerate month-end close cycles for 10 000 small-business clients.

- February 2026: SAP rolled out Brazil’s Nota Fiscal Eletrônica 4.0 schema within its S/4HANA suite ahead of the January 2026 indirect-tax reform cutover.

- January 2026: Thomson Reuters introduced ONESOURCE AI, a large-language-model assistant that drafts memos, classifies transactions and generates audit documentation.

- January 2026: Zenwork launched Tax1099, an agentic platform that automates contractor reporting with 95% field-level accuracy.

Global Tax Software Market Report Scope

The Tax Software Market is the industry focused on developing, deploying, and using software solutions to assist individuals, businesses, and organizations in managing tax-related processes. These processes include tax preparation, filing, compliance, and reporting.

The Tax Software Market Report is Segmented by Deployment (Cloud-Based and On-Premise), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Tax Type (Direct Tax and Indirect Tax), End-User (Individuals, Small Businesses, Large Enterprises, Accounting and Tax Firms, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Direct Tax |

| Indirect Tax |

| Individuals |

| Small Businesses |

| Large Enterprises |

| Accounting and Tax Firms |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment | Cloud-Based | ||

| On-Premise | |||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Tax Type | Direct Tax | ||

| Indirect Tax | |||

| By End-User | Individuals | ||

| Small Businesses | |||

| Large Enterprises | |||

| Accounting and Tax Firms | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the tax software market expected to grow through 2031?

It is projected to expand from USD 28.88 billion in 2026 to USD 50.50 billion by 2031, reflecting an 11.82% CAGR.

Why are cloud-based platforms overtaking on-premise tax engines?

Real-time reporting mandates and API-only filing portals require continuous connectivity and rapid rule updates that legacy architectures cannot deliver.

Which region will add the most new spending by 2031?

Asia-Pacific leads, with a forecast 15.64% CAGR fueled by mandatory e-invoice rollouts in India, China and Southeast Asia.

What segment offers the highest growth opportunity?

Indirect tax software, used for VAT and GST compliance, is forecast to rise at a 14.80% CAGR as cross-border e-commerce proliferates.

How are vendors differentiating products in 2026?

Providers embed generative-AI assistants, low-code rule builders and certified security controls to automate research, classification and filing tasks.

Page last updated on: