Special Effects (SFX) Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.67 Billion |

| Market Size (2030) | USD 4.15 Billion |

| Growth Rate (2025 - 2030) | 9.22% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

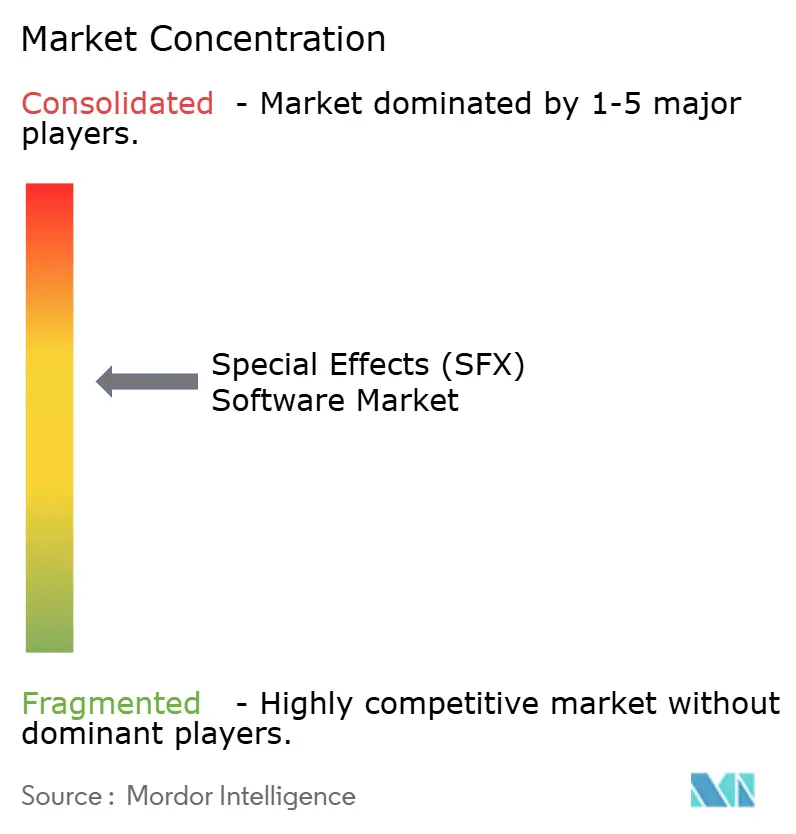

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Special Effects (SFX) Software Market Analysis by Mordor Intelligence

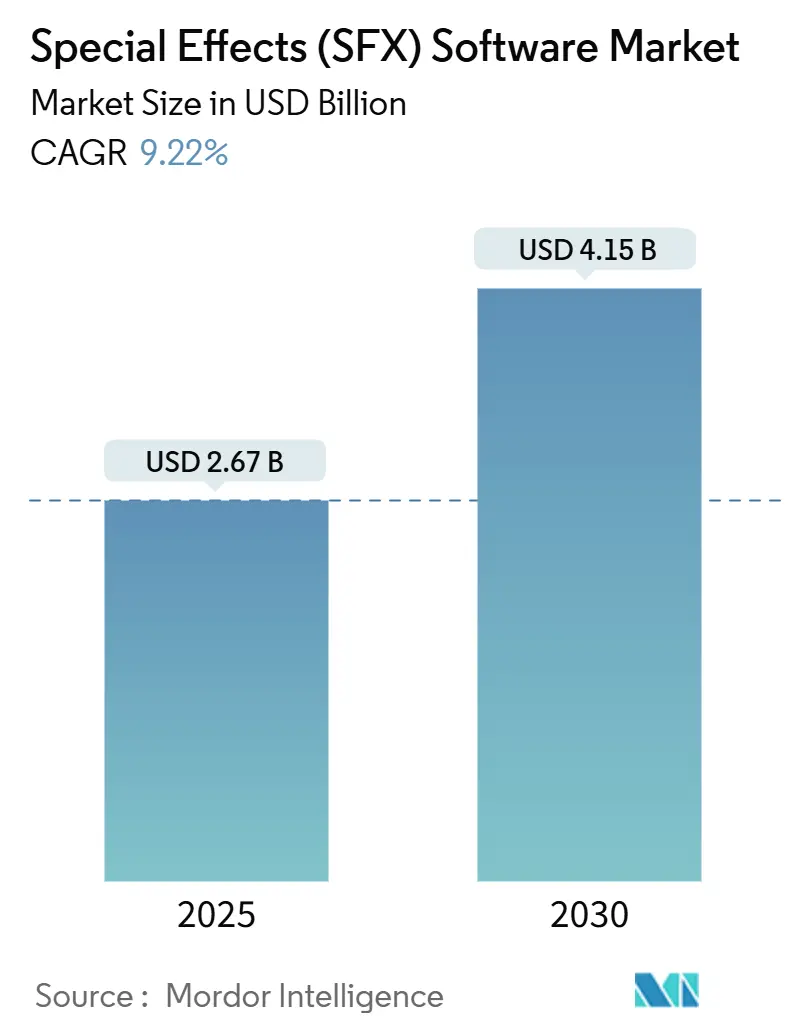

The special effects software market size stands at USD 2.67 billion in 2025 and is projected to reach USD 4.15 billion by 2030, expanding at a 9.22% CAGR. Strong streaming-platform spending, swift cloud-rendering adoption, GPU performance leaps, and broader access to professional-grade toolkits are reshaping competitive dynamics. Intensifying demand for cinematic-quality visuals in episodic content drives recurring upgrades of 3D modeling, compositing, and real-time rendering suites. Studios are shifting away from fixed on-premise render farms toward elastic cloud pipelines that curb capital outlays while supporting peak workloads. Government production incentives continue to tilt location decisions, spreading VFX spending across a wider set of regional hubs. In parallel, AI-driven automation is lowering the effort needed for rote tasks such as rotoscoping, freeing artists for creative work even as a shortage of senior technical directors persists.

Key Report Takeaways

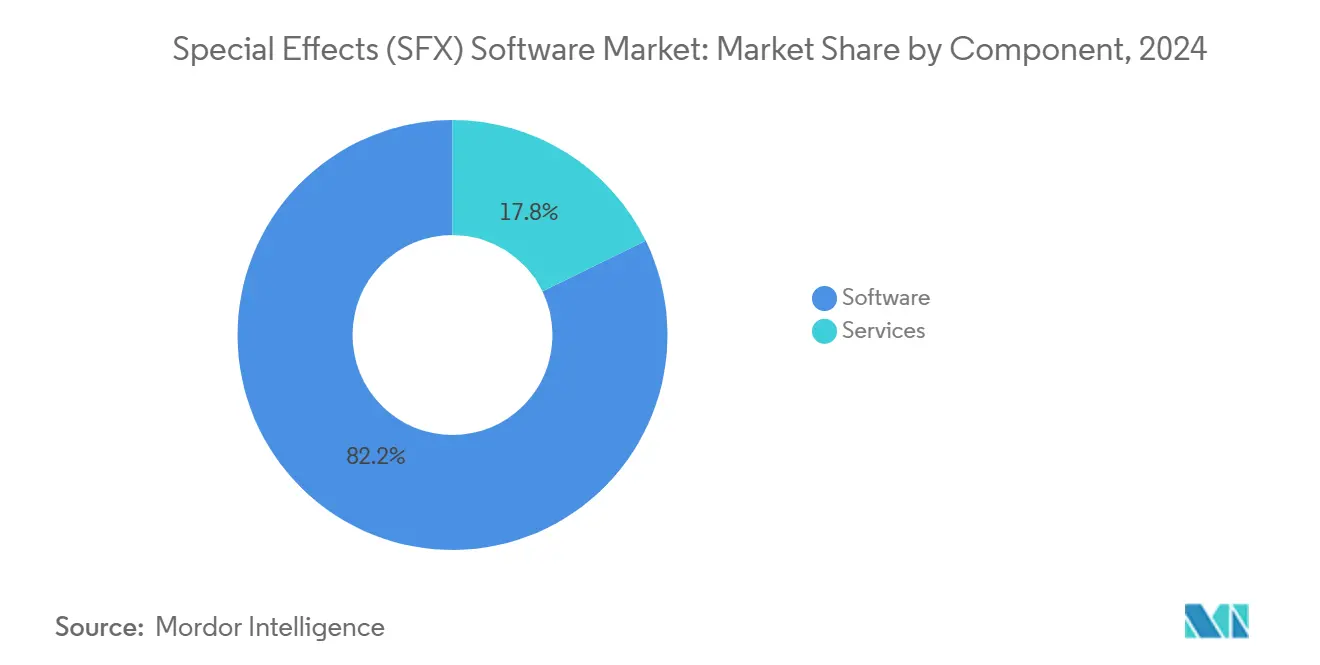

- By component, software accounted for 82.22% of the special effects software market share in 2024, whereas services will grow at a 10.44% CAGR to 2030.

- By deployment model, on-premise held 67.44% of the special effects software market size in 2024, while cloud is advancing at 11.24% CAGR through 2030.

- By application, movies captured 44.66% revenue share in 2024; gaming is projected to expand at an 11.65% CAGR to 2030.

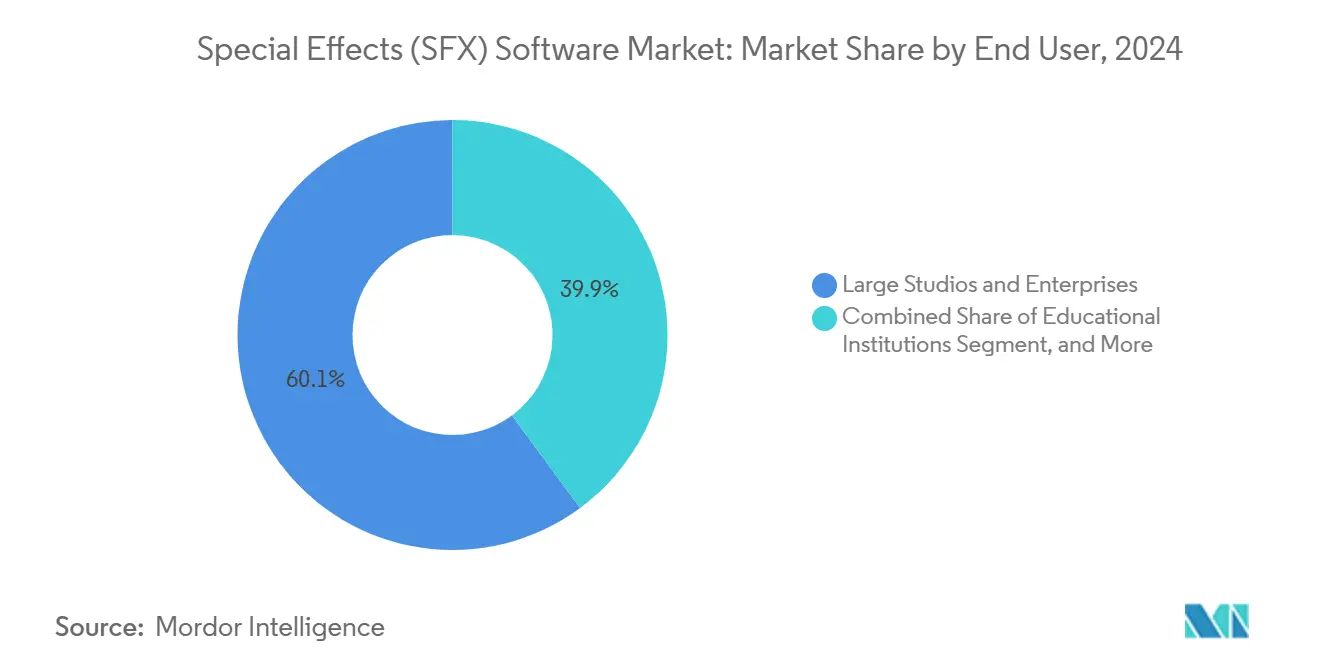

- By end user, large studios commanded 60.12% of spending in 2024, but small and medium studios plus freelancers are rising at a 10.62% CAGR over the forecast period.

- By technology, compositing led with 31.78% of the special effects software market share in 2024, yet real-time rendering is set to grow at 10.24% CAGR to 2030.

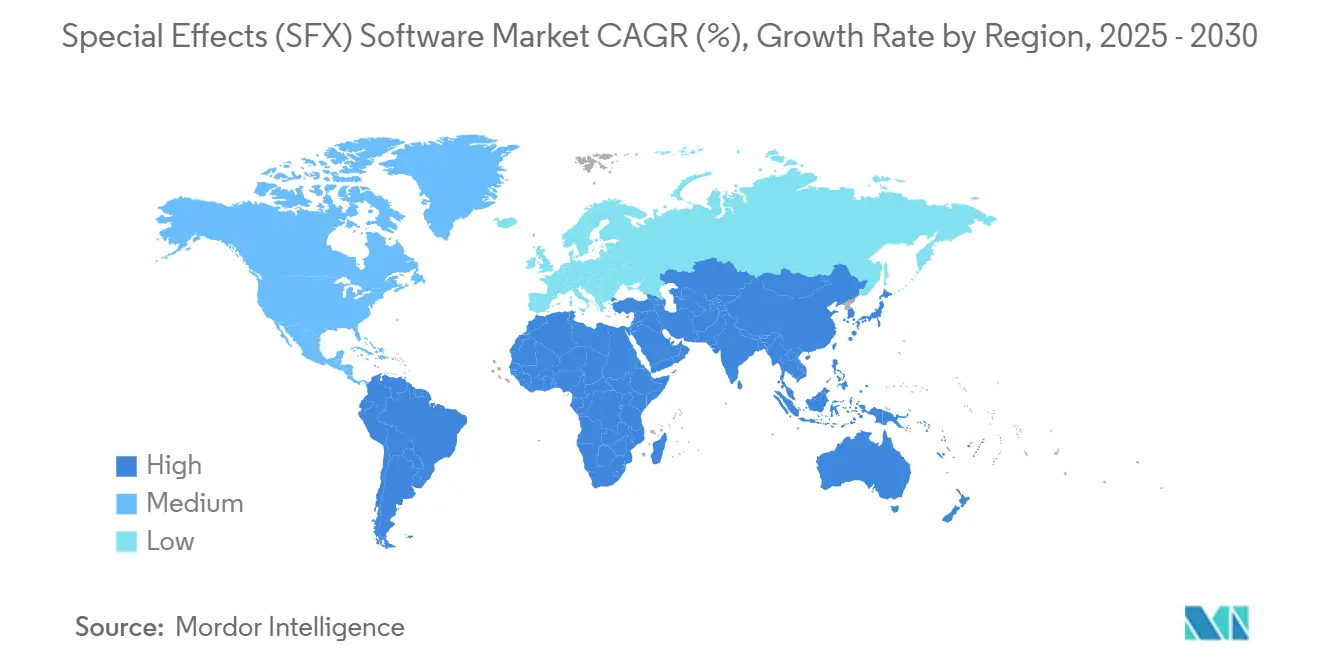

- By geography, North America held 37.88% share of the special effects software market size in 2024 and is forecast to register the fastest regional CAGR at 11.89% through 2030.

Global Special Effects (SFX) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for High-Quality VFX Content Across Streaming Platforms | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cost Efficiency and Scalability of Cloud-Based Rendering Pipelines | +1.8% | Global, early adoption in North America and APAC | Short term (≤ 2 years) |

| Advances in GPU Acceleration and Real-Time Rendering Engines | +1.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government Tax Incentives for Film Production in Key Markets | +1.3% | Regional, focused on Australia, UK, Canada, US states | Long term (≥ 4 years) |

| Standardization on Red Hat Enterprise Linux 9.x Boosting Ecosystem Compatibility | +0.9% | Global, enterprise-focused adoption | Long term (≥ 4 years) |

| OpenUSD and OpenFX Adoption Accelerating Plug-In Interoperability | +0.7% | Global, studio-driven implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Streaming Demand for High-Quality VFX

Streaming platforms continue to escalate original-content budgets, spurring steady ordering of series and films that match theatrical production values. Multi-season contracts require consistent visual-quality benchmarks, compelling studios to standardize on advanced compositing, simulation, and real-time rendering suites. Localization mandates issued by regional services in Asia Pacific and Latin America broaden the customer base for multilanguage toolchains and remote-collaboration services. The upgrade cadence for major software releases accelerates as production schedules compress, giving vendors recurring subscription revenue streams.

Cloud-Based Rendering Cost Efficiency

Variable-cost rendering on hyperscale infrastructure delivers 30-60% savings versus maintaining idle local compute clusters during off-peak periods, according to production tests published by Microsoft Azure. Automated resource scheduling and cost-analytics dashboards now ship natively in most flagship render-farm managers, easing adoption at small studios that lack dedicated systems staff. Hybrid deployments keep pre-visualization data in secure local storage while bursting large final-frame jobs to cloud GPU instances, striking a balance between security and elasticity.

Advances in GPU Acceleration and Real-Time Engines

NVIDIA RTX Ada Lovelace cards deliver up to 5 times prior-generation ray-tracing performance, cutting render times and lowering per-shot budgets. Unreal Engine 5’s Nanite virtualized geometry and Lumen global illumination allow directors to judge near-final shots live on set, shifting decision-making to earlier production phases. Competing hardware from AMD and Intel broadens component choice and sustains price-performance pressure, while open standards such as Vulkan preserve cross-platform compatibility across Linux and Windows pipelines.

Government Tax Incentives for Film Production

Australia’s Producer Offset of up to 40% for qualifying local expenditure, the United Kingdom’s 25% Film Tax Relief, and similar credits in Canada and several U.S. states directly stipulate enhanced percentages for VFX and post-production work, driving siting decisions toward those jurisdictions.[1]Screen Australia, “Producer Offset and Location Incentive Guidelines 2025,” screenaustralia.gov.auUpdated guidelines in 2025 added virtual-production stages and real-time rendering costs to eligible spend categories, catalyzing fresh investment in LED volume facilities that rely heavily on advanced software suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Licensing and Hardware Costs for Professional SFX Suites | -1.4% | Global, particularly affecting SME studios | Short term (≤ 2 years) |

| Acute Shortage of Skilled VFX Artists and Technical Directors | -1.9% | Global, most severe in North America and Europe | Long term (≥ 4 years) |

| Project Budget Volatility From Unpredictable Cloud Compute Billing | -0.8% | Global, cloud-adopting regions | Medium term (2-4 years) |

| IP Security Concerns During Cross-Border Remote Collaboration | -0.6% | Global, regulatory compliance focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Licensing and Hardware Costs for Professional SFX Suites

Flagship enterprise bundles can exceed USD 200 000 annually per seat once mandatory plugins and support contracts are included, while workstation-class GPUs fetch USD 5 000–15 000 each. Replacement cycles average 3–4 years to remain compatible with current drivers and real-time features. Although subscription models lower upfront spend, multi-year total cost often rises. Cloud rendering shifts capital outlay to operational expense yet introduces new budget-variability risks when last-minute revisions trigger unplanned compute spikes.[2]Foundry Visionmongers, “Cloud Cost Prediction Challenges in VFX Production,” foundry.com

Acute Shortage of Skilled VFX Talent

Screen Ireland’s 2024 skills audit found every surveyed studio requiring six to twelve months of on-the-job training before graduates reach baseline productivity. Senior technical director vacancies frequently remain open for more than eight months, delaying project starts or forcing expensive outsourcing. Wage inflation in primary hubs such as Vancouver and London exceeds 10% per annum, widening the affordability gap for emerging vendors. Accelerated online-course offerings help, yet curriculum often trails software-release cycles, limiting immediate impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expansion Accelerates Software Dominance

Software retained 82.22% of 2024 revenue because core creative functions modeling, animation, compositing, rendering require perpetual licensing or subscriptions for every project seat. Services, however, are climbing at a 10.44% CAGR as studios outsource pipeline integration, cloud orchestration, and security compliance. Vendors differentiate by bundling managed rendering, custom plugin development, and workflow consulting to reduce time-to-first-pixel. This services momentum underscores a structural pivot: rather than hiring full-time DevOps specialists, studios favor just-in-time expertise aligned to project cycles. As managed offerings grow, the special effects software market size for services is set to narrow the gap with software by decade-end.

The rise in services correlates with increased pipeline complexity. Multi-format deliveries (4K HDR, VR180, 8K master files) multiply integration points, spurring demand for certified consultants who resolve version-control issues across open formats such as USD and OpenFX. Cloud cost-governance audits and zero-trust security assessments now constitute routine line items. Collectively, these dynamics reinforce the symbiotic relationship between software innovation and service proficiency in the special effects software market.

By Deployment Model: Cloud Momentum Challenges On-Premise Preference

Despite ongoing security and latency benefits, on-premise environments still captured 67.44% of 2024 spending. Custom render farms remain essential for early-phase previz iterations where immediate feedback outweighs the economics of cloud burst capacity. Yet cloud instances priced per GPU-hour are advancing at an 11.24% CAGR, the fastest among all delivery modes, as baseline bandwidth improves and dedicated remote-desktop codecs minimize interactive lag. Studios in emerging hubs bypass cap-ex entirely, spinning up encrypted workstations inside hyperscale regions rather than importing high-end servers.

Hybrid architectures now predominate among top-tier studios: asset management and shot layout remain behind the firewall, whereas final-frame 4K renders burst to cloud nodes with temporal suspensions to eliminate egress fees. Cost-simulation tools inside leading pipeline suites estimate per-sequence compute demand, helping producers lock budgets before green-lighting. Consequently, cloud pipelines are moving from experimental to mainstream, fundamentally enlarging the special effects software market size attached to consumption-based render orchestration.

By Application: Movies Hold Revenue Lead While Gaming Posts Fastest Growth

Movies represented 44.66% of 2024 revenue as streamers funnel blockbuster budgets into direct-to-platform features that rival theatrical releases in scope. Post-production houses anchor their tool investments around academy-awarded compositing and simulation pipelines calibrated for DCI-P3 color spaces and Dolby Vision mastering. However, gaming revenue is growing at an 11.65% CAGR, fueled by convergence between real-time engines and high-fidelity cinematics. Advanced particle systems, ray-traced reflections, and photogrammetry workflows formerly reserved for film now power AAA titles, shortening pipeline divergence and encouraging joint licensing deals.

Television episodic series, especially premium limited runs, maintain a healthy middle ground, leveraging cloud burst render because weekly air dates leave no room for onsite queue backlogs. Advertisers increasingly commission CG-heavy brand activations and virtual product launches, feeding micro-licensing of specialized plugins. Other niches medical visualization, architecture, and education, though modest, give vendors alternate entry paths into conservative verticals, diversifying the revenue mix in the special effects software market.

By End User: SME Studios and Freelancers Erode Enterprise Exclusivity

Large studios commanded 60.12% of 2024 spend, yet their share gradually ebbs as cloud software tiers normalize professional-grade features for independent artists. Subscription models that scale seat counts monthly match freelance work rhythms, letting boutique facilities bid on shots previously monopolized by major vendors. Community asset libraries inside leading engines distribute ready-to-animate rigs or photoreal scans, shortening ramp-up for small teams.

Educational institutions, once limited to student licenses, now purchase enterprise-level subscriptions to mirror industry toolchains. Screen Ireland’s curriculum overhaul mandates USD-compliant workflows to ensure graduate portability across studios. This fosters earlier proficiency, indirectly addressing the talent shortage restraint. Over the forecast period, compounded SME adoption lifts their contribution to the special effects software market size, while enterprises focus spending on AI-powered pipeline accelerators and proprietary toolsets.

By Technology: Real-Time Rendering Shifts Center of Gravity

Compositing commands 31.78% of revenue because every project ends with multi-layer image integration. Yet real-time rendering and virtual-production suites outpace all other technologies at 10.24% CAGR on growing LED volume installs. In-camera visual effects relying on Unreal Engine or Unity achieve near-final pixel on set, slashing post budgets and reducing revision cycles.

3D modeling and animation tools remain indispensable, but AI-driven procedural generation trims manual asset-creation hours. Simulation FX packages integrate GPU-accelerated fluid and destruction solvers that compute frames in minutes, not hours, shrinking overnight render windows. AI-enhanced assistants clone brush-strokes, auto-track masks, and denoise volumetric passes, propelling sustained upgrades across vendor roadmaps. These cross-currents make technology choice a moving target, sustaining license churn and enlarging the special effects software market.

Geography Analysis

North America captured 37.88% of 2024 revenue on the strength of Hollywood studios, Silicon Valley GPU suppliers, and public cloud hyperscalers headquartered in the United States. Canada’s 17% federal post-production credit plus provincial top-ups entice cross-border productions, while new LED stages in Vancouver, Toronto, and Atlanta anchor local ecosystems. Mexico secures Spanish-language commissions from global streamers, benefiting from reduced labor costs and proximity to U.S. creative leads. The special effects software market size in North America is therefore expanding even from an already high base, reflected in its 11.89% forecast CAGR.

Asia Pacific is the fastest-evolving production geography. India’s animation, visual effects, gaming, and comics segment is set to climb from USD 3 billion in 2025 to USD 26 billion by 2030, creating large addressable demand for mid-tier licenses.[3] Asian Development Bank, “India AVGC Sector Growth 2025-2030,” adb.org . China’s box-office resurgence and Beijing’s guidelines that at least 70% of blockbuster VFX be produced domestically accelerate the adoption of home-grown pipelines interoperable with global USD standards. Japan, South Korea, and Australia round out a tri-pole of innovation in stylized animation, virtual production, and incentive-driven live-action features. Southeast Asian hubs such as Thailand and Vietnam leverage competitive labor rates and improved connectivity to win overflow rotoscoping and match-move work.

Europe preserves consistent growth anchored by longstanding creative industries in the United Kingdom, France, and Germany. Post-Brexit customs paperwork initially disrupted cross-channel asset transfers, but standardized USD plus secure VPN tunnels now streamline hand-offs. The European Union’s strict GDPR rules drive demand for on-premise or EU-resident cloud regions, sustaining local data-center builds and specialized compliance services. Smaller nations—Ireland, Czech Republic, Spain—capitalize on targeted rebates ranging from 25–32% to capture boutique projects and remote service contracts. Meanwhile, the Middle East and Africa, though nascent, show promise: UAE Media City hosts regionally focused VFX startups, and South Africa’s Cape Town benefits from 25% national film incentives on spend denominated in ZAR (USD values applied using SARB average 2024 rate).

Competitive Landscape

Market concentration sits in a mid-range band: the top five vendors control roughly 55-60% of global license and subscription revenue, reflecting moderate consolidation yet leaving meaningful share for specialized entrants. Adobe, Autodesk, Foundry, and Maxon each maintain broad ecosystems covering modeling, animation, compositing, and rendering, leveraging deep integration plug-ins and developer SDKs. Epic Games and Unity Technologies disrupt through real-time engines licensed on revenue-share or seat-based terms, attracting studios embracing virtual production.

Recent strategic moves cluster around AI and cloud. Autodesk’s USD 400 million purchase of Wonder Dynamics injects machine-learning character automation into Maya and 3ds Max portfolios. NVIDIA’s Omniverse Cloud transforms its hardware advantage into a platform business offering subscription collaboration spaces and on-demand RTX rendering. Foundry’s partnership with Microsoft Azure streamlines Nuke-in-browser sessions that shorten workstation boot times and enable secure remote dailies.

Niche providers succeed by owning critical workflow nodes—Chaos’ V-Ray for unbiased photoreal rendering, SideFX’s Houdini for procedural simulations, and Boris FX for specialized plug-ins. Patent filings logged at USPTO for neural render and AI denoising techniques point to continued performance leaps over the forecast period. Open-source initiatives, notably Pixar’s USD components released under Apache 2.0, temper vendor lock-in and invite community innovation. As AI democratizes rote compositing, vendors pivot toward value-added managed services and proprietary acceleration frameworks to preserve margin.

Special Effects (SFX) Software Industry Leaders

Adobe Inc.

Autodesk Inc.

Side Effects Software Inc.

The Foundry Visionmongers Ltd.

Blackmagic Design Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Autodesk completed the USD 400 million acquisition of Wonder Dynamics, integrating AI-powered character animation into flagship toolsets.

- September 2025: NVIDIA launched Omniverse Cloud with integrated RTX rendering and USD-based collaboration services.

- August 2025: Epic Games released Unreal Engine 5.5, adding native OpenUSD workflows and real-time ray-tracing upgrades for virtual production stages.

- July 2025: Adobe unveiled Creative Cloud AI Suite, automating rotoscoping, object removal, and content-aware fill across After Effects and Premiere Pro.

Global Special Effects (SFX) Software Market Report Scope

| Software |

| Services |

| On-Premise |

| Cloud |

| Movies |

| Television |

| Gaming |

| Advertising |

| Other Applications |

| Large Studios and Enterprises |

| Small and Medium Studios and Freelancers |

| Educational Institutions |

| 3D Modeling and Animation |

| Compositing |

| Simulation FX |

| Real-Time Rendering and Virtual Production |

| AI-Enhanced Tools |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| By Application | Movies | |

| Television | ||

| Gaming | ||

| Advertising | ||

| Other Applications | ||

| By End User | Large Studios and Enterprises | |

| Small and Medium Studios and Freelancers | ||

| Educational Institutions | ||

| By Technology | 3D Modeling and Animation | |

| Compositing | ||

| Simulation FX | ||

| Real-Time Rendering and Virtual Production | ||

| AI-Enhanced Tools | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the special effects software market?

The market is valued at USD 2.67 billion in 2025.

How fast is the special effects software market growing?

It is projected to expand at a 9.22% CAGR, reaching USD 4.15 billion by 2030.

Which application area is registering the highest growth?

Gaming revenues are climbing the fastest with an 11.65% CAGR.

Why are studios adopting cloud rendering?

Cloud pipelines cut 30-60% of infrastructure costs by replacing idle on-premise hardware with elastic, pay-as-you-go GPU capacity.

Which region leads global adoption?

North America holds the largest share and also posts the highest forecast growth at 11.89% CAGR.

What is the main challenge facing VFX studios today?

A severe shortage of experienced artists and technical directors extends project timelines and inflates wage costs.

Page last updated on: