Tampon Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

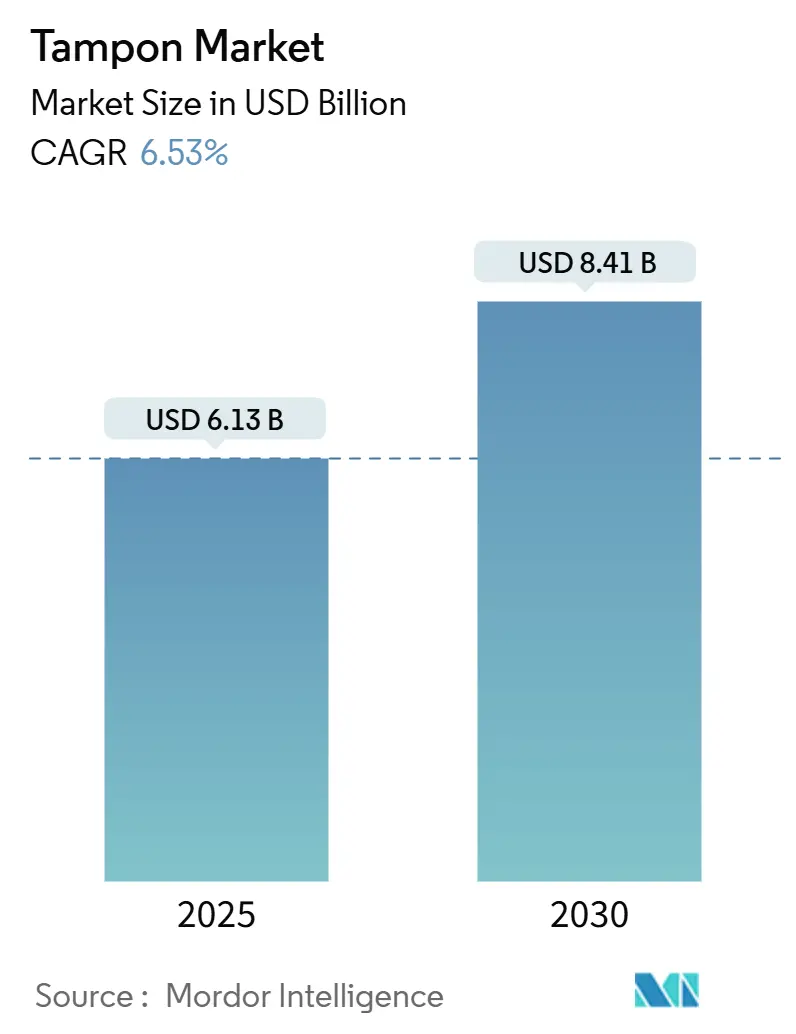

| Market Size (2025) | USD 6.13 Billion |

| Market Size (2030) | USD 8.41 Billion |

| Growth Rate (2025 - 2030) | 6.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tampon Market Analysis by Mordor Intelligence

The Tampon Market size is estimated at USD 6.13 billion in 2025, and is expected to reach USD 8.41 billion by 2030, at a CAGR of 6.53% during the forecast period (2025-2030).

This outlook reflects a maturing industry that must counter headwinds from fast-rising substitutes while capitalizing on growing female workforce participation, expanding e-commerce channels, and stronger regulatory support, such as tax eliminations. Product safety controversies, most notably heavy-metal findings highlighted by the United States Food and Drug Administration, have accelerated consumer migration toward organic cotton lines and forced manufacturers to invest in stringent testing protocols. Intensifying competition from period underwear and menstrual cups has pushed brands to differentiate through design innovations such as Sequel’s spiral construction, the first fundamental tampon redesign in eight decades. Regionally, North America maintains pricing power on the back of premium positioning, whereas Asia-Pacific delivers the fastest volume gains because awareness programs are pushing first-time adoption rates higher.

Key Report Takeaways

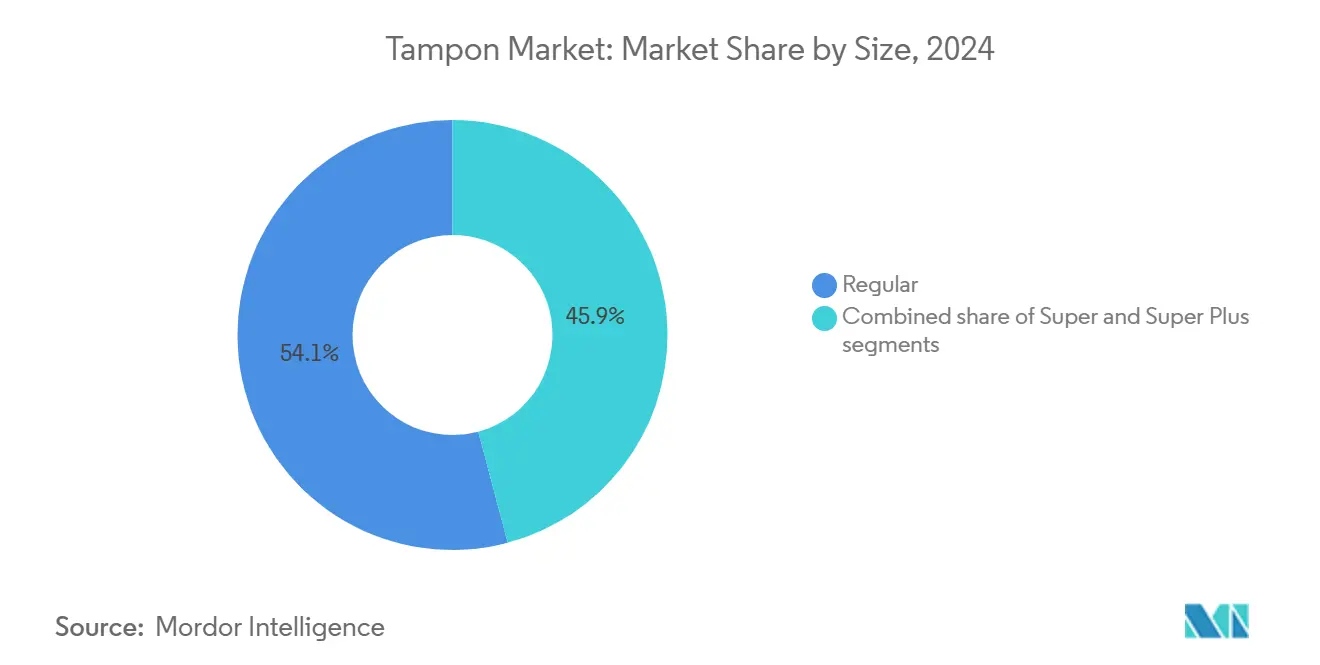

- By size/absorbency, regular captured 54.13% of the tampon market share in 2024, while super plus is projected to expand at a 7.59% CAGR through 2030.

- By product type, applicator variants held 61.37% revenue share of the tampon market in 2024; non-applicator units are advancing at an 8.13% CAGR to 2030.

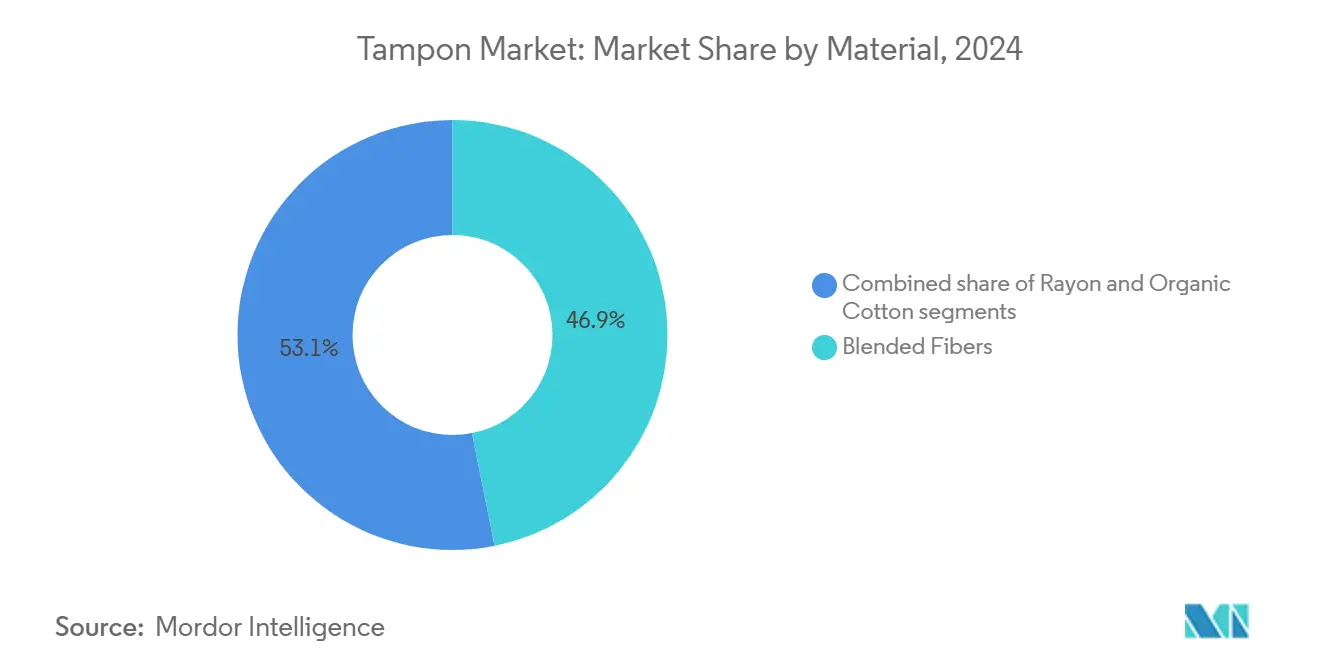

- By material, blended fibers accounted for 46.87% share of the tampon market size in 2024, whereas organic cotton is forecast to grow at 8.19% CAGR.

- By distribution channel, supermarkets/hypermarkets commanded 41.67% of the tampon market size in 2024; online retail exhibits the fastest growth at 8.59% CAGR.

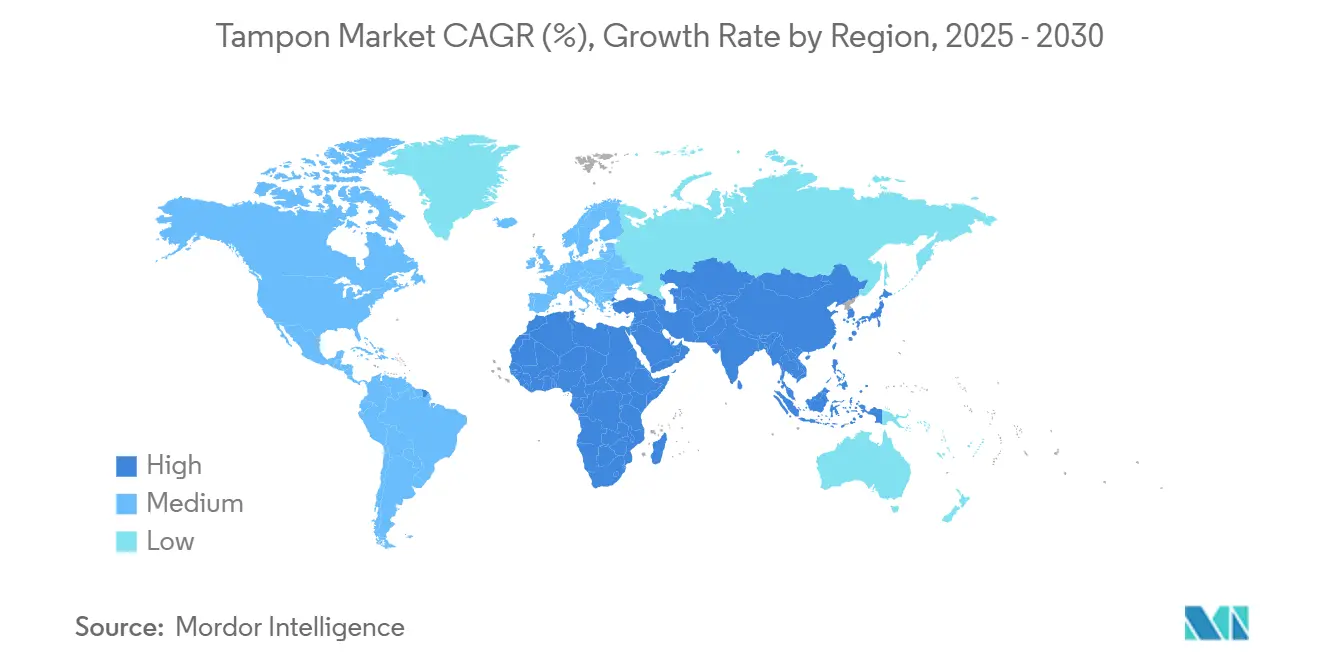

- By geography, North America led with 37.43% tampon market share in 2024; Asia-Pacific records the highest projected CAGR at 9.23% through 2030.

Global Tampon Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising female workforce participation | +1.2% | Global, with strongest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Growing awareness of menstrual hygiene | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Product innovations in organic and bio-based tampons | +0.9% | North America and EU, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| E-commerce subscription models gaining traction | +0.7% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Elimination/reduction of tampon taxes in key regions | +0.5% | North America, Europe, with emerging momentum in Asia-Pacific | Short term (≤ 2 years) |

| Strong Marketing and Brand Innovation | +0.4% | Global, with premium positioning in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Female Workforce Participation

Rising female workforce participation continues to drive tampon demand by increasing the need for mobility-friendly and convenience-oriented menstrual hygiene solutions. In the United States, the female labor force participation rate stood at 57.0% as of June 2025, underscoring a sustained trend of women engaging in professional roles that demand discreet and reliable menstrual care [1]Source: U.S. Bureau of Labor Statistics, "Labor Force Participation Rate - Women", bls.gov. Working women, especially in urban settings and leadership positions, prioritize products that align with active lifestyles, favoring applicator tampons despite their higher cost. In parallel, workplace policies such as menstrual leave in countries like India and Japan are helping destigmatize menstruation, boosting product acceptance and supporting long-term category growth across developed and emerging markets alike.

Growing Awareness of Menstrual Hygiene

In developed markets, where tampons are both readily available and socially accepted, awareness initiatives surrounding menstrual hygiene are increasingly influencing tampon adoption patterns. In the U.S., initiatives such as the Menstrual Equity for All Act and state-backed distribution programs in schools have played pivotal roles in normalizing tampon use. By providing free access and comprehensive education on menstruation, these programs have made significant strides. In the UK, the Period Product Scheme mirrors this approach, offering free tampons in educational institutions. This not only diminishes stigma but also fosters early adoption among young women. Such initiatives bolster familiarity and regular tampon use, especially among active and working demographics. To further amplify tampon acceptance and ensure sustained growth in this segment, a blend of school programs, digital outreach, and training for healthcare providers is essential across various regions.

Product Innovations in Organic and Bio-based Tampons

Innovations in organic and bio-based tampons are addressing consumer health and environmental concerns. Sequel’s FDA-approved spiral tampon, for instance, boosts leak protection and athletic performance. Meanwhile, Viv offers tampons made from 100% certified organic cotton, ensuring they're free from harmful chemicals and heavy metals. Biodegradable options are on the rise: German startup Vyld has introduced seaweed-based tampons sans applicators, and Italy’s Corman S.p.A. is crafting compostable applicators from agricultural byproducts. These advancements underscore a surging demand for sustainable, chemical-free menstrual products, emphasizing safety, comfort, and eco-friendliness. As consumers increasingly gravitate towards these effective and environmentally responsible alternatives, the organic tampon segment is poised for robust growth.

E-commerce Subscription Models Gaining Traction

Subscription models are transforming tampon purchases, shifting consumers from reactive buying to proactive replenishment. This change increases customer lifetime value and reduces acquisition costs. LOLA’s acquisition by Forum Brands highlights the importance of subscription-based organic tampon businesses. Direct-to-consumer models bypass retail markups, offering 15–25% savings while maintaining a premium image. Using data analytics, subscription services optimize deliveries and product choices, improving retention through personalized experiences. This approach appeals to younger consumers valuing convenience and discretion. The U.S. Census Bureau reports e-commerce sales accounted for 16.2% of total retail sales in Q1 2025, emphasizing the growing role of digital channels in purchasing [2]Source: U. S. Census Bureau, "Quarterly Retail E-Commerce Sales", census.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxic Shock Syndrome (TSS) concerns | -0.8% | Global, with heightened awareness in developed markets | Long term (≥ 4 years) |

| Environmental disposal and plastic-waste debates | -0.6% | Europe and North America, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Cultural Taboos and Social Stigma | -1.1% | Asia-Pacific, Middle East and Africa, and Latin America rural areas | Long term (≥ 4 years) |

| Competition from menstrual cups and period underwear | -1.4% | Global, led by environmentally conscious demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxic Shock Syndrome (TSS) Concerns

Toxic Shock Syndrome (TSS) concerns significantly restrain the tampon market. Recent FDA investigations revealed heavy metal contamination, including lead, in tampons from major brands, sparking class-action lawsuits against companies like Procter & Gamble and Kimberly-Clark. While the FDA found no immediate safety risks, it emphasized that no lead exposure is safe. Social media has amplified these findings, driving consumers toward alternative menstrual products. Legal rulings suggest federal preemption may not shield manufacturers from design defect lawsuits, increasing liability. TSS and contamination concerns hinder market growth while highlighting brands prioritizing transparency and safety testing.

Competition from Menstrual Cups and Period Underwear

As alternative menstrual products gain popularity, the tampon market finds itself under pressure. Solutions like menstrual cups and period un derwear are becoming preferred choices, thanks to their environmental advantages, durability, and cost savings over time. Institutional backing for these alternatives is evident, highlighted by initiatives like India's Thinkal project, which successfully distributed over a million menstrual cups in South India. With consumers becoming more informed about ownership costs and waste reduction, there's been a noticeable dip in repeat tampon purchases. In response, major players like Kimberly-Clark are acquiring reusable brands, underscoring both the segment's validation and the looming threat of market cannibalization. As eco-friendly choices gain mainstream acceptance, the tampon industry is challenged to either carve out a unique identity or pivot its approach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size/Absorbency: Regular Dominates Daily Use

In 2024, regular absorbency tampons captured a 54.13% share of the market, underscoring their adaptability to diverse flow intensities and a consumer inclination towards moderate protection. Their leading position is bolstered by being the go-to choice for newcomers and those desiring a blend of comfort and absorption. Meanwhile, Super Plus variants are on a rapid ascent, boasting a 7.59% CAGR through 2030, fueled by their adoption in active lifestyles and overnight applications. This trend underscores a consumer's readiness to invest more for heightened protection during peak activity or extended use.

Super absorbency products cater to those who find regular options lacking but deem Super Plus too much for everyday use. Light absorbency tampons, on the other hand, target specific needs, such as the tail end of menstrual cycles or users with consistently lighter flows. This segmentation highlights a growing consumer discernment, with many aligning absorbency choices to particular scenarios rather than settling for a one-size-fits-all approach. Sequel, recognizing this trend, has channeled its engineering prowess into the Super Plus segment, unveiling a spiral design technology aimed at alleviating leakage concerns, a primary driver pushing consumers towards higher absorbency.

By Product Type: Applicators Maintain Convenience Premium

In 2024, applicator tampons command a 61.37% market share, driven by a consumer preference for hygienic insertion and user-friendliness, especially among younger and first-time users. Marketers highlight discretion and cleanliness, positioning applicators as the premium choice, even with their higher manufacturing costs. Meanwhile, non-applicator tampons are set to grow at an 8.13% CAGR through 2030, fueled by budget-minded consumers and eco-conscious advocates aiming to cut down on plastic waste. This uptick signals a maturing market, with users becoming more adept at digital insertion methods and placing sustainability above mere convenience.

In regions with limited menstrual education, the applicator's edge remains strong. Its insertion mechanism alleviates user anxiety and simplifies the process. Conversely, digital tampons are making headway in Europe, where eco-awareness trumps convenience. This shift is bolstered by campaigns spotlighting proper insertion techniques. Notably, a surge in patent activity around collapsible applicator designs indicates manufacturers' recognition of the need to harmonize convenience with environmental considerations. Price sensitivity is playing a pivotal role in product selection. Non-applicator variants, boasting a 15-20% cost advantage, are increasingly favored by budget-conscious consumers grappling with inflation across essential goods.

By Material: Blended Fibers Balance Performance and Cost

In 2024, blended fiber tampons command a 46.87% market share, leveraging cotton-rayon combinations to enhance absorption and manufacturing efficiency. This segment's dominance is rooted in decades of material science advancements, enabling manufacturers to fine-tune absorbency while navigating raw material cost fluctuations. Meanwhile, organic cotton is on a rapid ascent, projected to grow at an 8.19% CAGR through 2030, as consumers increasingly favor natural materials over synthetics due to safety concerns.

Rayon-based products cater to budget-conscious consumers, delivering satisfactory performance at reduced manufacturing costs. However, their growth is hampered by lingering concerns over synthetic materials, especially in light of studies linking them to heavy metal contamination. Despite challenges in the supply chain, consumers are willing to pay a premium of 20-30% for certified organic materials, underscoring the enduring allure of organic cotton. In a nod to the industry's shifting priorities, Kimberly-Clark has pledged to be "Natural Forest Free" by 2030, highlighting a broader recognition of sustainability's importance. Yet, the landscape is fraught with challenges: supply chain disruptions stemming from EU deforestation regulations jeopardize material availability, posing a potential hurdle for the organic segment's growth while simultaneously opening doors for alternative fiber sources.

By Distribution Channel: Online Retail Disrupts Traditional Patterns

In 2024, supermarkets/hypermarkets command a 41.67% market share, capitalizing on established consumer shopping habits and impulse buying. However, they grapple with competition from digital platforms that emphasize convenience and discretion. Traditional retail still holds an edge, offering immediate product access and the chance to inspect packaging pre-purchase. This is especially crucial for first-time buyers who seek educational insights. Meanwhile, online retail is on a growth trajectory, expanding at an 8.59% CAGR through 2030. This surge is largely fueled by the rising adoption of subscription models and the emergence of direct-to-consumer brands, which sidestep traditional retail markups.

Pharmacies and drug stores cater to niche needs, providing professional consultations and strategically positioning medical devices. This appeals to health-conscious consumers who prioritize expert advice. These outlets benefit from their proximity to healthcare services and their ability to stock products tailored for specific medical conditions. Other distribution avenues, such as convenience stores and vending machines, cater to urgent purchase needs and ensure accessibility in educational settings. The evolution of these channels mirrors the broader transformation in retail. Successful brands are now embracing omnichannel strategies, blending online ease with offline experiences. A testament to this shift is LOLA's acquisition by Amazon aggregator Forum Brands, underscoring the growing significance of direct-to-consumer capabilities in today's retail arena.

Geography Analysis

In 2024, North America holds a 37.43% market share, driven by mature distribution networks, premium product positioning, and consumer education normalizing tampon use. Regulatory moves, like Texas's tampon tax removal in September 2023, and menstrual equity laws in 27 states and Washington, D.C., as of 2025, reduce period poverty and boost school attendance [3]Source: Alliance for Period Supplies, "Period Products in Schools", allianceforperiodsupplies.org. Market saturation shifts focus to premium segments, with organic and applicator variants sustaining revenue growth despite volume constraints. Procter & Gamble's Baby, Feminine & Family Care segment, including Tampax, earned USD 15.3 billion in 2024, offsetting volume declines with pricing strategies. Competition remains intense, with established players countering direct-to-consumer entrants and managing safety-related lawsuits.

Asia-Pacific, the fastest-growing region, is projected to grow at a 9.23% CAGR through 2030, driven by awareness campaigns, rising female workforce participation, and urbanization. Japan's aging population and hygiene culture support premium product adoption, with Unicharm leveraging pricing and innovation. Cultural barriers persist in rural areas, but government and corporate initiatives are improving acceptance. The region attracts global investment, with companies adapting products to local preferences and expanding distribution to underserved markets.

Europe's stringent environmental regulations and strong consumer preference for sustainable products drive the organic cotton segment. The UK's VAT removal on tampons lowers cost barriers, highlighting regulatory support for menstrual health. EU deforestation regulations challenge supply chains, risking shortages but spurring innovation in alternative fibers. Environmental awareness boosts demand for organic and biodegradable products, with consumers paying sustainability premiums above global averages. Regulatory harmonization across EU member states simplifies market entry and sets high safety and environmental standards, influencing global product development. In South America and the Middle East and Africa (MEA), a growing urban middle class and rising menstrual health awareness create opportunities. However, cultural taboos and limited tampon access necessitate education campaigns and affordable innovations for gradual market growth.

Competitive Landscape

The tampon market remains highly consolidated, with Procter & Gamble, Kimberly-Clark, and Edgewell Personal Care collectively dominating global market share. However, competition from direct-to-consumer (DTC) brands and alternative menstrual products, like period underwear and menstrual cups, is rising. Premium organic tampon brands are gaining traction, and sustainability-driven consumers are seeking alternatives. Kimberly-Clark entered the reusable segment with its Thinx acquisition, while Procter & Gamble focuses on innovation, advertising, and market defense. Sequel’s FDA-approved spiral tampon, with 12 patents and 6 pending, marks the first major engineering shift in over 80 years, signaling a surge in patent activity and design innovation.

Personalized and subscription-based models are emerging, as seen in LOLA’s acquisition by Forum Brands, highlighting the potential of DTC platforms. These platforms cut retail markups, enhance convenience, and build loyalty through tailored offerings and discreet deliveries. Major players are advancing packaging and supply chain technologies, including smart packaging, inventory tracking, and blockchain authentication, to improve efficiency and counter counterfeits. Meanwhile, smaller disruptors gain trust by prioritizing ingredient transparency, sustainable sourcing, and values-driven branding, areas where traditional manufacturers face scrutiny and legal challenges over safety disclosures.

This shifting landscape reflects broader trends in consumer goods, where traditional advantages in scale and retail distribution are waning. Leading tampon manufacturers grapple with the challenge of defending their core portfolios while exploring growth in adjacent categories that risk cannibalizing existing revenues. Their success hinges on aligning with evolving consumer priorities around health, transparency, and sustainability, without compromising profitability. Meanwhile, the nimbleness of newer entrants positions them to seize this shift, potentially reshaping competitive standards in a market long dominated by a select few.

Tampon Industry Leaders

-

Procter & Gamble Co.

-

Kimberly-Clark Corp.

-

Edgewell Personal Care Co.

-

Essity AB

-

Unicharm Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stayfree has launched Stayfree Tampons, combining o.b.'s tampon technology with its strong brand presence in India to expand period protection options for Indian women.

- February 2025: Berlin-based startup Vyld has unveiled Kelpon, the globe's inaugural certified seaweed-based tampon, ensuring safety and microbiome compatibility. Kelpon is making its debut in Germany via collaborations with local partners.

- January 2024: Forum Brands acquired LOLA, an organic period care brand with a direct-to-consumer subscription model and 100% organic cotton tampons. This acquisition by the Amazon aggregator highlights the strategic value of subscription-based feminine care businesses and consolidation trends in the direct-to-consumer market.

Global Tampon Market Report Scope

| Regular |

| Super |

| Super Plus |

| Applicator Tampons |

| Non-Applicator (Digital) Tampons |

| Rayon |

| Blended Fibers |

| Organic Cotton |

| Supermarkets/Hypermarkets |

| Pharmacies and Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Size/Absorbency | Regular | |

| Super | ||

| Super Plus | ||

| By Product Type | Applicator Tampons | |

| Non-Applicator (Digital) Tampons | ||

| By Material | Rayon | |

| Blended Fibers | ||

| Organic Cotton | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies and Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the tampon market’s 6.53% CAGR to 2030?

Rising female workforce participation, government-led hygiene campaigns, and product upgrades such as organic cotton lines collectively sustain demand even as reusable substitutes gain ground.

How significant is the safety controversy surrounding heavy metals?

FDA investigations and related lawsuits have increased scrutiny, prompting brands to publish third-party test results and invest in cleaner supply chains, though the overall market growth projection remains intact.

Which region offers the strongest incremental opportunity for tampon makers?

Asia-Pacific posts a 9.23% CAGR as awareness programs expand, disposable incomes rise, and retail distribution deepens, leaving a wide runway for first-time adoption.

Why are subscription services important to future growth?

Subscriptions deliver predictable revenue, personalized shipment cycles, and cost savings for consumers, helping online channels outpace brick-and-mortar at an 8.59% CAGR.

How are incumbents responding to surging demand for eco-friendly solutions?

Leading companies are ramping up organic cotton capacity, exploring biodegradable applicators, acquiring reusable-product brands, and pledging forest-free sourcing to align with buyers’ sustainability expectations.

Page last updated on: