Wet Wipes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

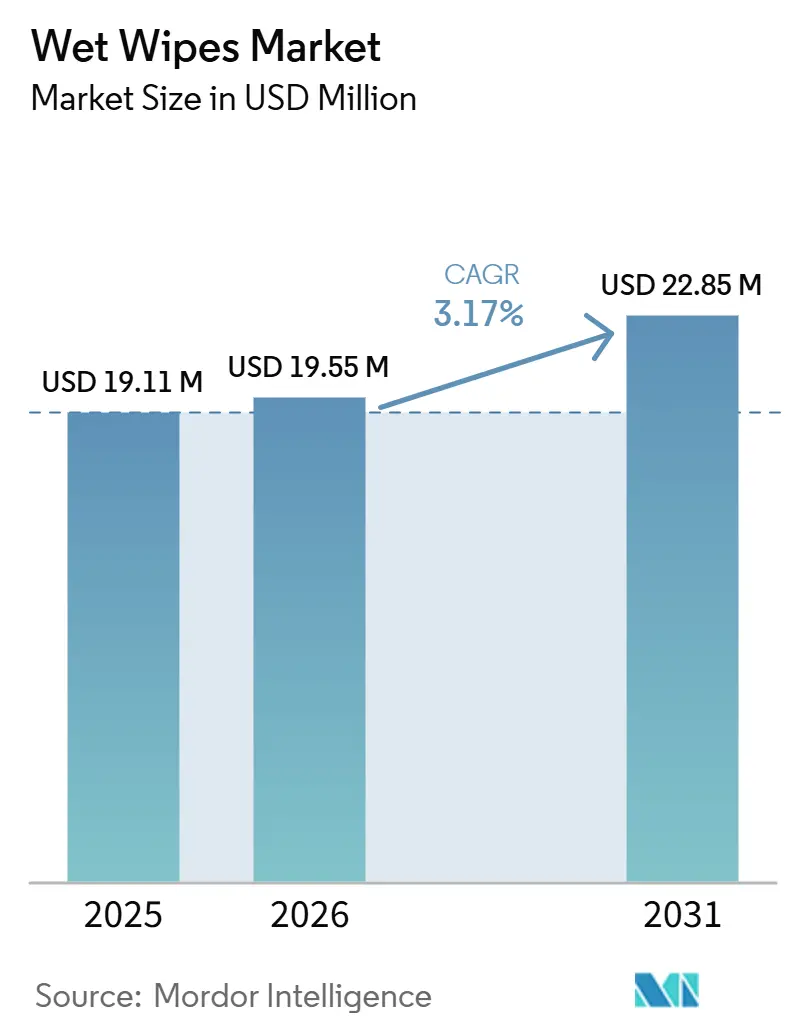

| Market Size (2026) | USD 19.55 Million |

| Market Size (2031) | USD 22.85 Million |

| Growth Rate (2026 - 2031) | 3.17% CAGR |

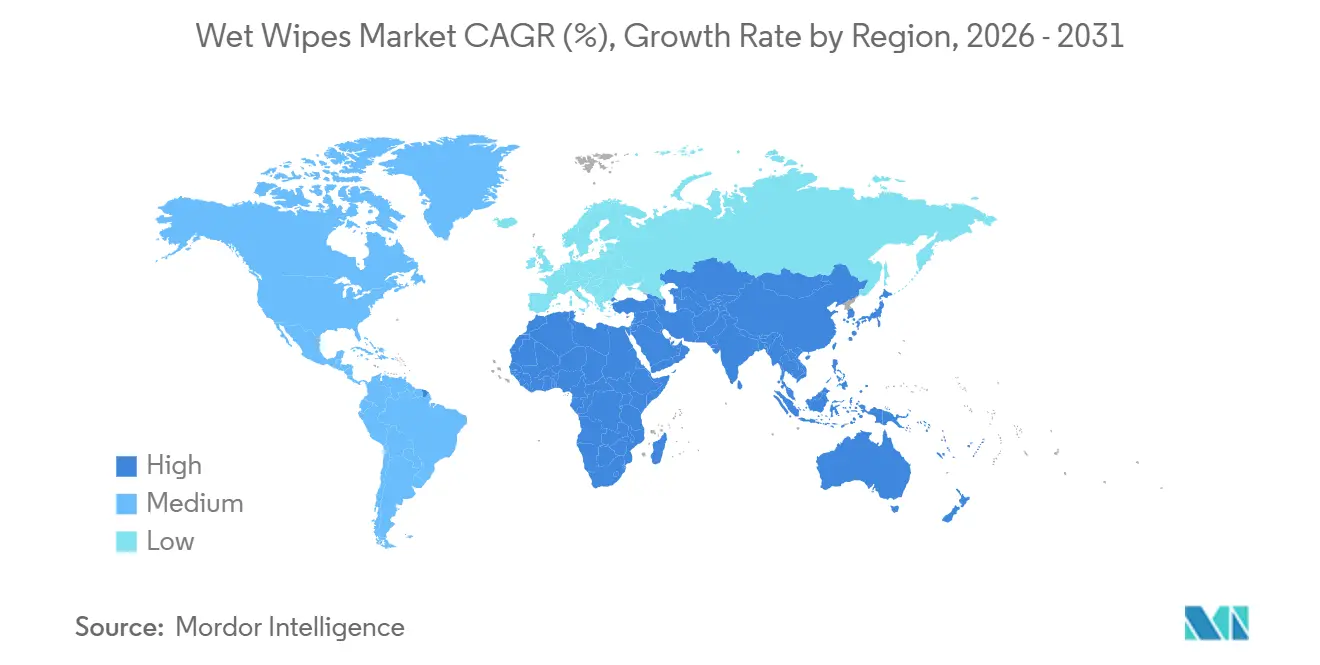

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wet Wipes Market Analysis by Mordor Intelligence

The wet wipes market size was valued at USD 19.11 million in 2025 and is estimated to grow from USD 19.55 million in 2026 to reach USD 22.85 million by 2031, at a CAGR of 3.17% from 2026 to 2031. This growth is driven by government restrictions on plastic substrates, increasing adoption of waterless hygiene practices due to water scarcity, and the expansion of digital retail, which enhances access to premium biodegradable products. While personal care wipes dominate the market, pet wipes are also gaining traction among Gen Z consumers who prioritize pet grooming and treat animals as family. Regulatory deadlines in the United Kingdom and European Union are accelerating reformulation efforts, while labeling mandates in North America are pushing manufacturers toward plant-based fibers. In water-stressed regions across the Asia-Pacific and the Middle East, single-use hygiene formats are becoming more prevalent due to limited access to piped water, thereby shifting the geographic focus of the wet wipes market. Competitive intensity remains moderate, creating opportunities for niche brands offering flushable, compostable, or plant-based alternatives that comply with stricter regulations.

Key Report Takeaways

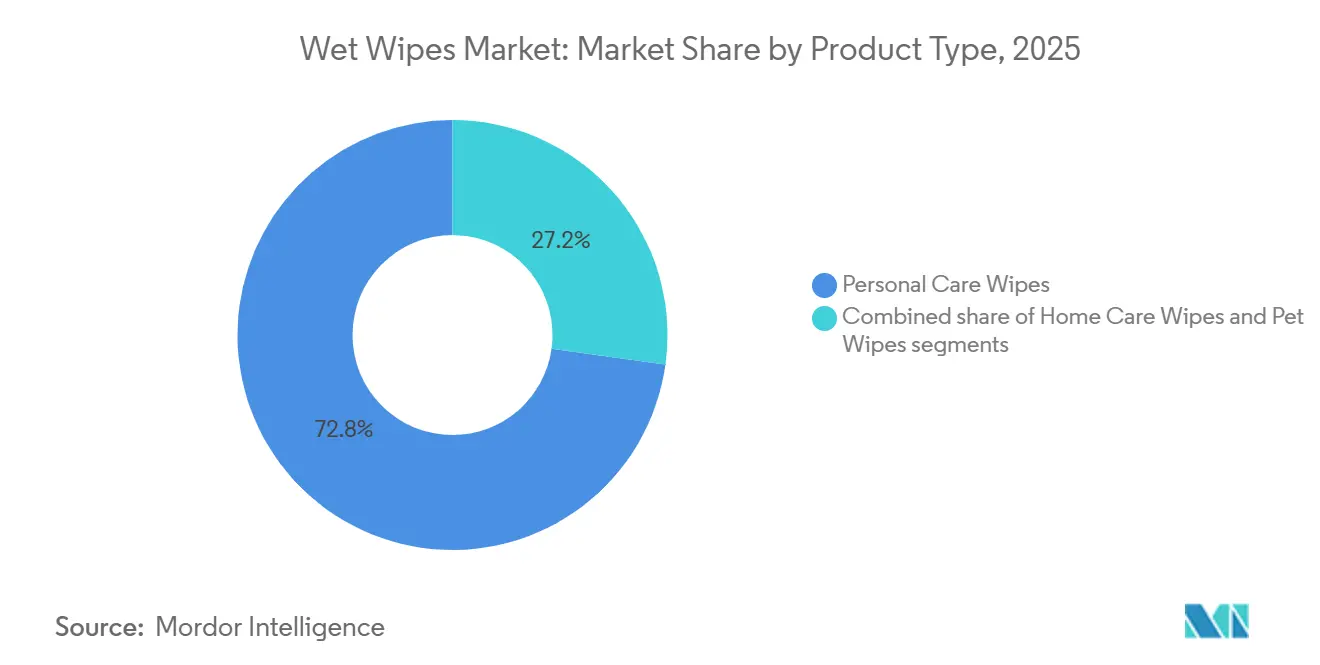

- By product type, personal care wipes led with 72.81% of the wet wipes market share in 2025, while pet wipes are projected to post a 4.02% CAGR between 2026 and 2031.

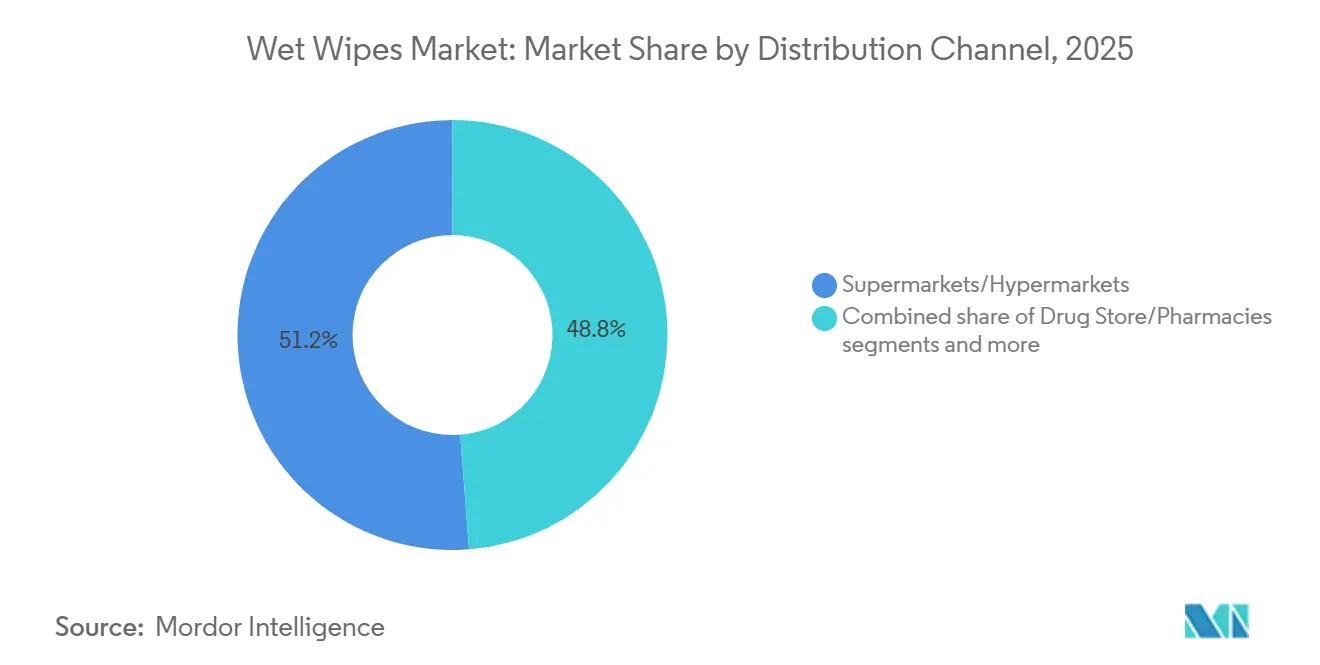

- By distribution channel, supermarkets and hypermarkets accounted for 51.23% of the 2025 value, whereas online retail is forecasted to expand at a 3.56% CAGR during 2026-2031.

- By geography, North America captured 36.09% of 2025 revenue; Asia-Pacific is forecast to expand at a 3.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wet Wipes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hygiene and sanitation consciousness | +0.6% | Global, with stronger gains in Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising marketing and advertisement initiatives | +0.4% | North America and Europe | Short term (≤ 2 years) |

| Growth in travel and outdoor activities | +0.5% | Global, led by Asia-Pacific and Middle East | Medium term (2-4 years) |

| Premiumization and biodegradable substrates | +0.7% | North America and Europe, driven by regulatory mandates and consumer willingness to pay for sustainability claims | Long term (≥ 4 years) |

| Water-scarcity driven adoption in emerging hot-climate regions | +0.3% | Middle East, Africa, and water-stressed basins in Asia-Pacific (e.g., parts of India, Indonesia) | Long term (≥ 4 years) |

| Workplace wellness mandates boosting institutional demand | +0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising hygiene and sanitation consciousness

Households and institutions without a reliable water supply increasingly rely on disposable wipes for everyday cleaning, driving demand in densely populated urban areas across the Asia-Pacific and the Middle East. The growing emphasis on hygiene, coupled with convenience, has made wet wipes a staple in these regions. Public-sector procurement standards that prioritize biodegradable substrates are becoming more prevalent in school, transit, and healthcare tenders, signaling sustained volume growth for suppliers that meet these criteria. Additionally, workplace wellness mandates, such as Ontario’s 2025 washroom cleaning rule, are further boosting institutional bulk orders [1]Source: Ontario Ministry of Labour, "Occupational Health and Safety Act - Washroom Cleaning Mandates," ontario.ca. The wet wipes market continues to benefit from employers integrating surface disinfecting wipes into safety protocols and consumers maintaining pandemic-era hygiene practices. Brands that can demonstrate both germ-kill efficacy and environmental safety are gaining a competitive edge, particularly as regulatory scrutiny intensifies. Furthermore, advancements in product innovation, such as flushable and compostable wipes, are addressing environmental concerns while expanding the market's appeal.

Growth in travel and outdoor activities

International arrivals grew 4% to 1.52 billion in 2025, with Asia-Pacific up 6% and Africa up 8% [2]Source: UN Tourism Analytics Unit, “International Tourist Arrivals Up 4% in 2025 Reflecting Strong Travel Demand Around the World,” unwto.org. These trends are driving the demand for travel-size antibacterial wipes, particularly in airports, hotels, and convenience stores. The growing trend of pet-friendly travel is also contributing to this demand, as the majority of U.S. pet owners now vacation with their pets, creating a need for specialized products such as paw and ear wipes. Additionally, the rising popularity of outdoor recreation activities, including hiking, camping, and music festivals, has normalized the use of carry-along hygiene kits. This shift is fueling incremental sales across both personal care and surface disinfectant subsegments. The wet wipes market is capitalizing on these trends by offering innovative solutions such as resealable packs and multi-unit bundles that cater to specific consumer needs. These products are designed to comply with airline liquid restrictions and campsite disposal regulations, making them more convenient for travelers.

Premiumization and biodegradable substrates

Regulatory deadlines across the United Kingdom, Scotland, Wales, and Northern Ireland are set to ban plastic-containing wipes between December 2026 and August 2027, effectively driving the adoption of plant-based alternatives. This shift has prompted manufacturers to innovate rapidly. For instance, CloroxPro EcoClean launched in January 2025, featuring 100% plant fibers, while Ecolab introduced the first plastic-free hospital-grade wipe in July 2024. Additionally, advancements in production processes, such as closed-loop water recycling, have enabled manufacturers to reduce freshwater usage, mitigating risks in regions prone to water scarcity. The wet wipes market is also witnessing diversification into premium segments. Cosmetic and intimate wipes now incorporate ingredients like vitamin E and hyaluronic acid, appealing to consumers seeking skincare solutions beyond traditional bottled cleansers. Furthermore, the market is experiencing a trend toward premiumization, with brands introducing high-quality, value-added products to cater to discerning consumers. The growing demand for biodegradable, eco-friendly options is also reshaping the industry as consumers increasingly prioritize sustainability.

Rising marketing and advertisement initiatives

Premium labels are increasingly positioning wipes as lifestyle essentials through influencer campaigns and direct-to-consumer subscription models, effectively bypassing traditional shelf-space competition. These strategies leverage dynamic social-media targeting to engage niche consumer groups, including new parents, pet owners, travelers, and festival-goers, who prioritize portability and specialized ingredients. Sustainability messaging has become a cornerstone of advertising efforts, as approximately 3 billion disposable nappies and wipes are discarded into UK landfills annually. Brands are addressing this issue by promoting FSC (Forest Stewardship Council)-certified fibers, biodegradable materials, and compostable packaging. Additionally, the wet wipes market is shifting from a focus on commodity pricing to value-added segmentation, emphasizing traceable supply chains, innovative product formulations, and credible eco-friendly claims to meet evolving consumer demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns over plastic-based wipes | -0.5% | Global, with acute regulatory enforcement in United Kingdom and European Union | Short term (≤ 2 years) |

| Rising availability of alternatives | -0.3% | North America and Europe | Medium term (2-4 years) |

| High cost per use compared to traditional cleaning methods like soap and water | -0.2% | Price-sensitive markets in Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Frequent use may cause skin irritation or allergies in sensitive individuals | -0.1% | Global, affecting baby wipes and intimate wipes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental concerns over plastic-based wipes

Sewer blockages caused by non-flushable wipes cost UK utilities approximately USD 250 million annually, intensifying political and regulatory pressure for bans. Additionally, microplastic pollution has placed brands under increased scrutiny from NGOs and exposed retailers to potential reputational risks. Flushability regulations under the European Single-Use Plastics Directive now mandate clear labeling and impose extended producer responsibility fees, further squeezing margins for non-compliant products [3]Source: European Commission Staff, “Single-Use Plastics Directive,” europa.eu. In response, leading players in the wet wipes market are investing in innovative solutions, such as water-dispersible binders like polyvinyl alcohol and carboxymethyl cellulose, which disintegrate efficiently in wastewater systems. Companies are focusing on developing biodegradable and compostable alternatives to align with evolving consumer preferences and stricter environmental standards, ensuring long-term sustainability and market competitiveness.

Rising availability of alternatives

Reusable cloth wipes and bidet attachments are gaining traction among eco-conscious consumers in the United States and Western Europe, dampening the growth of disposable products in the baby and toilet tissue subsegments. Elevated bidet sales, which surged during the pandemic, continue as consumers recognize their potential for long-term cost savings, improved hygiene, and reduced waste. Additionally, growing awareness of environmental sustainability has led to a shift in consumer preferences toward reusable, eco-friendly alternatives. While institutional adoption is slower due to stringent infection-control regulations, pilot programs in Scandinavian schools demonstrate that logistical challenges can be addressed effectively. Manufacturers are now focusing on specialized formulations, such as hypoallergenic, fragrance-free, or disinfecting options, which provide unique benefits that reusable alternatives cannot easily replicate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominates, Pet Wipes Surge

Personal care wipes accounted for 72.81% of the revenue in 2025, driven by the widespread use of baby, cosmetic, and hand-and-body wipes as essential hygiene products across various demographics. The personal care segment is expected to maintain steady growth, while pet wipes are projected to be the fastest-growing category, with an annual growth rate of 4.02% through 2031. The increasing adoption of pets, particularly among Gen Z couples, and the convenience of subscription delivery models are fueling this growth. Pet wipes now feature innovative products such as antibacterial paw pads and deodorizing formulas that comply with airline carry-on regulations and hotel pet policies, further enhancing their appeal. Within the personal care segment, manufacturers are focusing on innovation to meet evolving consumer preferences and regulatory requirements. Skin-friendly preservatives and plant-based sheets are being incorporated to align with new flushability standards.

Baby wipes, while facing margin pressures from private-label competitors, continue to maintain consumer trust by emphasizing dermatologically tested claims and hypoallergenic formulations. Cosmetic wipes are increasingly incorporating advanced ingredients such as micellar water and vitamin C, catering to beauty-conscious consumers seeking quick, effective skincare solutions. These innovations are helping brands differentiate themselves in a competitive market. Home care wipes, although facing competition from reusable microfiber cloths, remain a staple in institutional settings due to their effectiveness in disinfecting and maintaining hygiene. The demand for disinfecting formats is particularly strong in healthcare facilities, schools, and offices, where hygiene standards are critical. Additionally, the growing awareness of hygiene and cleanliness among consumers has led to increased adoption of home care wipes for everyday cleaning tasks. Manufacturers are also exploring sustainable options, such as biodegradable materials, to address environmental concerns and appeal to eco-conscious consumers.

By Distribution Channel: E-Commerce Gains, Supermarkets Hold Ground

Supermarkets and hypermarkets retained a dominant 51.23% share in 2025, driven by in-store promotions that encourage impulse purchases. These retail formats continue to attract consumers because they offer a wide variety of products under one roof, including exclusive deals and discounts on bulk purchases. However, online retail is projected to grow at a 3.56% CAGR between 2026 and 2031, as auto-replenishment programs and subscription models gain traction, particularly for baby, cosmetic, and pet wipes. The convenience of doorstep delivery and the ability to compare products online are key factors driving this shift. The wet wipes market share is expected to gradually shift toward e-commerce as digital platforms lower entry barriers for start-ups, promoting eco-friendly, sustainable products.

Drug stores remain a trusted channel for sensitive and specialized products, such as intimate and medical-grade wipes, where pharmacist recommendations play a significant role in influencing consumer decisions. These stores are particularly favored for products requiring a higher degree of trust and quality assurance. Convenience stores, on the other hand, cater to on-the-go consumers seeking travel-size or single-use wipes. However, their market share is expected to remain relatively flat as consumers increasingly consolidate their shopping trips at larger retail formats or opt for online subscriptions. Regulatory developments, such as the UK pharmacy exemptions for medical wipes following the 2027 plastic ban, highlight how channel dynamics are evolving under product-specific regulations.

Geography Analysis

In 2025, North America accounted for 36.09% of the wet wipes market revenue, driven by high per-capita usage and extensive institutional procurement across schools, offices, and healthcare systems. State-level flushability labeling requirements in regions like California and Washington have added cost and complexity for manufacturers. However, the potential federal passage of the WIPPES Act could standardize these regulations. Corporate wellness initiatives continue to fuel demand for surface wipes in office environments, while the growing penetration of e-commerce accelerates the market share of private-label products. In Canada, regulatory trends closely follow those in the United States, while Mexico benefits from a rising middle class that supports the premiumization of wet wipes.

The Asia-Pacific region is expected to register the highest growth rate, with a projected CAGR of 3.64% from 2026 to 2031. Urbanization, inconsistent water supply, and the expansion of smartphone-driven retail channels are key factors driving this growth. China leads the region in volume, primarily through baby-wipe purchases, while India and Indonesia are experiencing double-digit value growth in natural-ingredient cosmetic wipes. E-commerce platforms enable domestic start-ups to bypass traditional retail barriers. Additionally, initiatives like Unicharm’s dry-clean diaper recycling program highlight how local manufacturers are leveraging water conservation as a competitive advantage.

Europe faces increasing regulatory pressures under the Single-Use Plastics Directive, with national bans on plastic-based wipes set to take effect in December 2026 in Wales and by August 2027 in Scotland. Germany’s Blue Angel certification amplifies the demand for fiber transparency, while Scandinavian retailers are delisting non-certified products. In the Middle East and Africa, the market is expanding from a smaller base, supported by a rebound in tourism surpassing previous levels and rising per-capita wipe usage due to drought conditions. In South America, market growth is concentrated in Brazil, Argentina, and Colombia, although currency volatility poses challenges for premium-priced products.

Competitive Landscape

The wet wipes market exhibits moderate concentration, with a few multinational consumer goods companies, including Kimberly-Clark, Procter & Gamble, Reckitt Benckiser, Johnson & Johnson, Unilever, and Clorox, alongside regional specialists such as Essity, Hengan, Unicharm, Nice-Pak, and emerging sustainability-focused brands like The Honest Company, WaterWipes, and Biom. Kimberly-Clark's USD 48.7 billion acquisition of Kenvue, announced in November 2025 and expected to close in the second half of 2026, is anticipated to consolidate personal care portfolios and likely drive pricing discipline as the combined entity rationalizes SKUs and leverages procurement scale.

Patent filings indicate a competitive race to develop water-dispersible substrates using polyvinyl alcohol and carboxymethyl cellulose binders to meet flushability standards. Smaller challengers such as Biom, WaterWipes, and Harper Hygienics are differentiating themselves through quat-free actives, 100% cotton sheets, and transparent supply chains. Institutional buyers increasingly favor suppliers that can validate ESG metrics, making technologies like water-saving closed-loop manufacturing a procurement advantage. Emerging opportunities are evident in institutional channels such as schools, transit hubs, and corporate campuses, where procurement cycles prioritize suppliers demonstrating compliance with occupational health and safety regulations.

Technology serves as a competitive advantage: closed-loop water recycling in manufacturing reduces freshwater consumption by up to 40%, mitigating operational risks in water-stressed regions and supporting ESG narratives that appeal to institutional buyers and retail partners. Smaller entrants like Biom (quat-free, plant-based disinfecting wipes launched in March 2026) and Harper Hygienics (Cleanic Naturals 100% cotton biodegradable wipes launched in February 2025) are carving out niches by targeting healthcare, food service, and eco-conscious consumers willing to pay premiums for safer chemistries and certified sustainable substrates.

Wet Wipes Industry Leaders

-

The Clorox Company

-

Reckitt Benckiser Group PLC

-

Johnson & Johnson

-

Procter & Gamble

-

Kimberly-Clark

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Biom launched quat-free, plant-based disinfecting wipes targeting healthcare and food-service operators seeking safer active ingredients and reduced chemical residues. The product addresses growing regulatory and consumer scrutiny of quaternary ammonium compounds, which have been linked to respiratory irritation and antimicrobial resistance.

- November 2025: Kimberly-Clark announced the acquisition of Kenvue for USD 48.7 billion, a transformative deal expected to close in the second half of 2026 that will consolidate personal-care brands, expand geographic reach, and create procurement and distribution synergies.

- November 2025: The UK Department for Environment, Food & Rural Affairs signed into law the Environmental Protection (Wet Wipes Containing Plastic) (England) Regulations 2025, banning the supply and sale of plastic-containing wet wipes from May 2027. The legislation follows a public consultation in which 95% of respondents supported the ban and is aligned with parallel measures in Scotland, Wales, and Northern Ireland, creating a unified UK regulatory framework that will force manufacturers to reformulate or exit the market.

Global Wet Wipes Market Report Scope

The wet wipes market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into personal care wipes, home care wipes, and pet wipes. By distribution channels, the market has been segmented into supermarkets/hypermarkets, drug stores/pharmacies, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Personal Care Wipes |

| Home Care Wipes |

| Pet Wipes |

| Supermarkets/Hypermarkets |

| Drug Stores/Pharmacies |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Personal Care Wipes | |

| Home Care Wipes | ||

| Pet Wipes | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Drug Stores/Pharmacies | ||

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the wet wipes market?

The wet wipes market size reached USD 19.55 million in 2026 and is on course for USD 22.85 million by 2031.

Which product category is growing the fastest?

Pet wipes are projected to post a 4.02% CAGR from 2026-2031 due to rising pet-care routines among Gen Z owners.

Which region will add the most incremental demand by 2031?

Asia-Pacific, forecast at a 3.64% CAGR, will contribute the largest volume jump because urban populations lack reliable water infrastructure.

What channels are expanding the quickest?

Online retail is growing at a 3.56% CAGR as auto-replenishment subscriptions capture recurring purchases.

Page last updated on: