Wipes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 18.81 Billion |

| Market Size (2031) | USD 21.54 Billion |

| Growth Rate (2026 - 2031) | 2.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wipes Market Analysis by Mordor Intelligence

The Wipes Market was valued at USD 18.31 billion in 2025 and is projected to grow from USD 18.81 billion in 2026 to USD 21.54 billion by 2031, registering a CAGR of 2.75% during the forecast period (2026-2031). This growth is driven by increased awareness of hygiene and sanitation, a rising preference for portable and time-efficient cleaning solutions, and the widespread use of wipes in personal care, surface cleaning, and professional sanitation. The industry is also shifting toward higher-performance and safer formulations, with innovations focusing on enhanced substrate strength and softness, skin-friendly formulations for sensitive users, and improved functional attributes such as antibacterial properties, odor control, and multi-surface applicability. Additionally, sustainability concerns are reshaping the market, driving the adoption of biodegradable, compostable, and plastic-free materials.

Key Report Takeaways

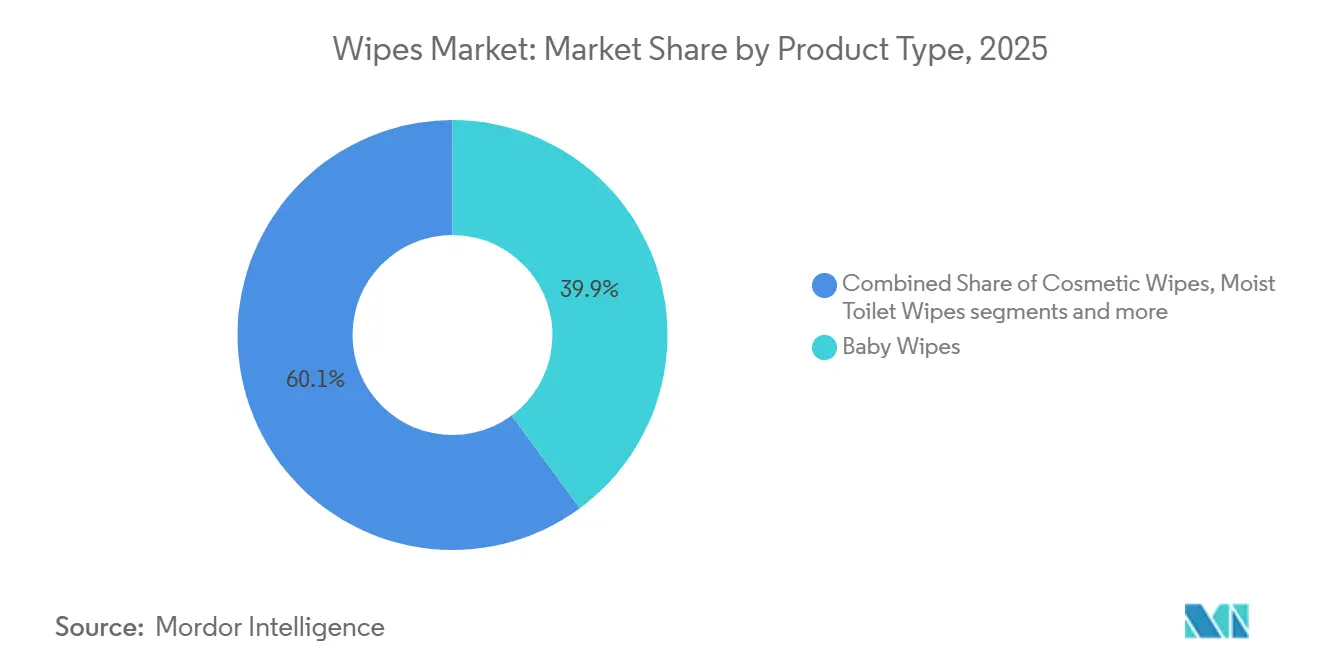

- By product type, baby wipes led with 39.86% of 2025 revenue, while moist toilet wipes posted the highest projected 2.83% CAGR to 2031.

- By ingredient, conventional formulations held 68.01% share of the 2025 global wipes market size, but natural and organic variants are projected to expand at a 2.96% CAGR through 2031.

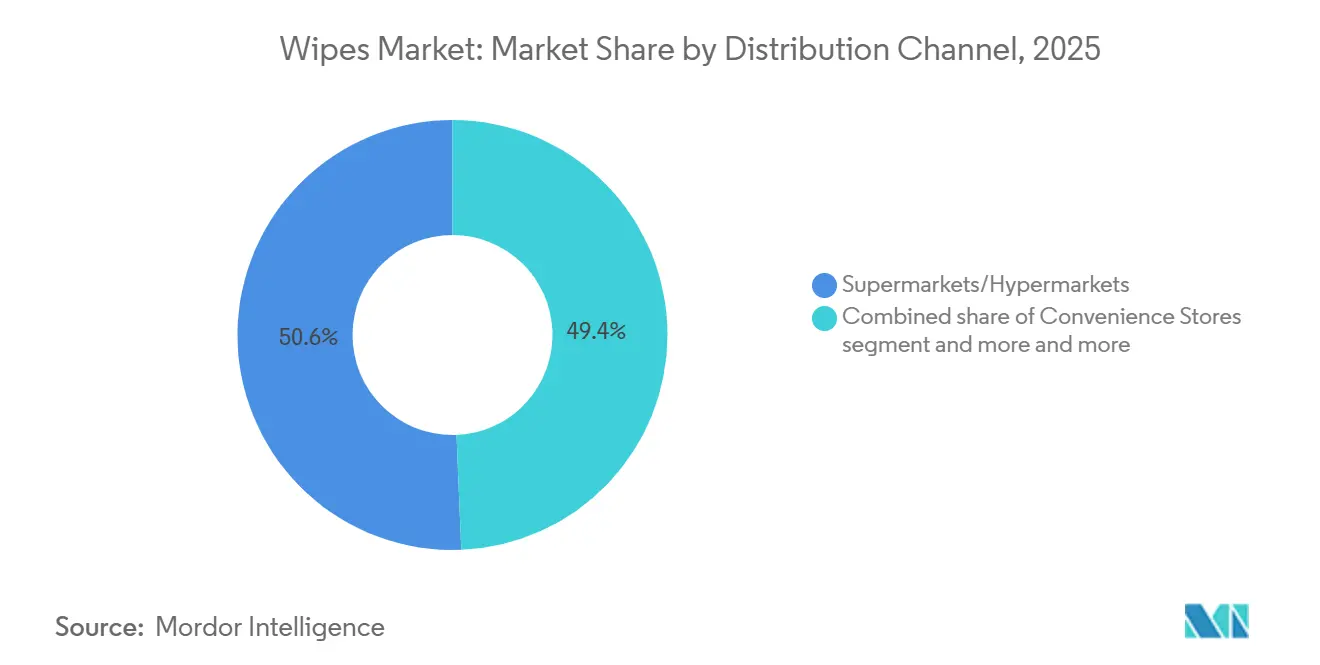

- By distribution channel, supermarkets and hypermarkets captured 50.65% of the global wipes market share in 2025, whereas online retail is advancing at a 3.34% CAGR over 2026-2031.

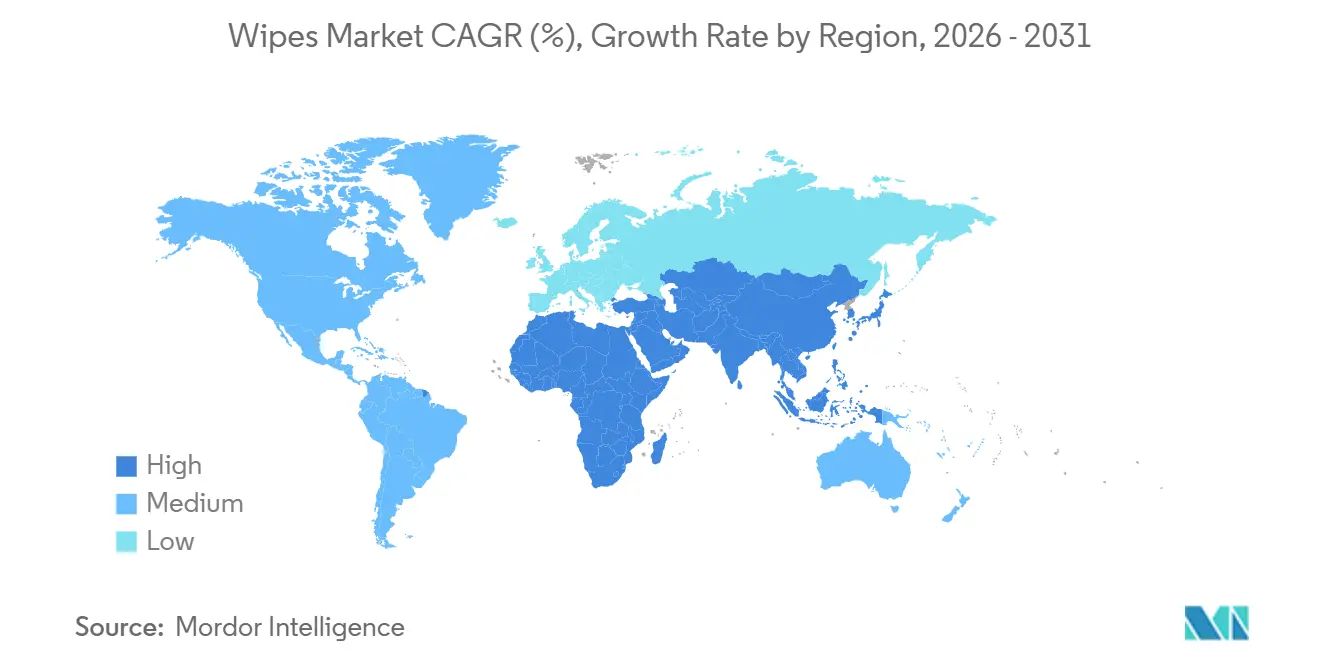

- By geography, North America commanded 40.19% revenue share in 2025, while Asia-Pacific is set to record the fastest 3.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wipes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hygiene and sanitation awareness | +0.8% | Global, with elevated intensity in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Product innovation and advanced formulations | +0.6% | North America and Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Rising female workforce is driving the market growth | +0.5% | Asia-Pacific core, Latin America emerging | Long term (≥ 4 years) |

| Shift toward sustainable and eco‑friendly solutions | +0.4% | Europe and North America regulatory-led, Asia-Pacific consumer-driven | Medium term (2-4 years) |

| Branding, marketing and product awareness | +0.3% | Global, digital-first in North America and Europe | Short term (≤ 2 years) |

| Increasing preference for skin‑friendly and dermatologically tested formulations | +0.2% | North America and Europe, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising hygiene and sanitation awareness

Increasing awareness of hygiene and sanitation has become a key driver of the global wipes market, significantly influencing consumer behavior and institutional hygiene practices worldwide. Greater emphasis on personal cleanliness, surface disinfection, and germ prevention, accelerated by global public health events and reinforced by ongoing awareness campaigns, has made the use of wipes a routine part of daily life. Consumers now perceive wipes as a primary preventive hygiene solution rather than an occasional convenience product, leading to increased usage across baby care, personal hygiene, household cleaning, and on-the-go applications. Similarly, institutional environments such as hospitals, clinics, schools, offices, hospitality venues, and public transportation systems have strengthened sanitation protocols, incorporating disinfectant and cleaning wipes into their standard procedures. The portability and single-use nature of wipes meet heightened hygiene standards by reducing cross-contamination risks compared to reusable cleaning tools. Additionally, growing awareness of skin-safe hygiene has driven demand for dermatologically tested, alcohol-free, and sensitive-skin formulations, particularly among families with infants and elderly individuals.

Product innovation and advanced formulations

Product innovation and advanced formulations are key growth drivers in the global wipes market, as manufacturers focus on enhancing performance, skin safety, and sensory appeal to meet increasing consumer expectations. As wipes evolve from basic cleaning products to skin-contact hygiene solutions, advancements in substrate technology, lotion chemistry, and product design have become critical for competitive differentiation. Companies are prioritizing the development of softer and stronger nonwoven fibers, improved absorbency, pH-balanced and minimal-ingredient formulations, and dermatologically tested solutions to address concerns related to skin irritation, sensitivity, and safety for daily use, particularly in baby and personal care segments. Advanced formulations also support multifunctionality, enabling wipes to provide cleansing, moisturizing, and protective benefits in a single product, thereby increasing usage frequency and enhancing value perception. For example, in September 2025, WaterWipes introduced a new line of stronger, softer wipes specifically designed for sensitive skin. This updated range featured an embossed pattern made from finer, softer fibers, improving both cleansing efficiency and comfort while reinforcing the brand’s positioning for sensitive skin.

Rising female workforce is driving the market growth

The increasing participation of women in the workforce is significantly contributing to the growth of the global wipes market by influencing household routines, childcare practices, and hygiene product preferences. As more women engage in full-time and part-time employment, the demand for time-efficient and convenient solutions in daily care and cleaning activities has risen. Working women, particularly mothers, are increasingly adopting wipes as convenient, ready-to-use hygiene solutions for baby care, personal hygiene, household cleaning, and on-the-go needs. This reduces reliance on more time-consuming alternatives such as cloth cleaning and repeated water use. Consequently, this shift has led to higher consumption frequency and sustained demand for wipes across various product categories. Additionally, the growing female workforce is driving demand for multipurpose and travel-friendly formats, bulk packaging, and subscription-based purchasing options, which cater to busy schedules and predictable replenishment requirements. This trend is supported by labor participation data. According to the Bureau of Labor Statistics, the female employment rate reached 55.2% in 2024, underscoring the influence of working women on consumption patterns [1]Source: Bureau of Labor Statistics, "Employment rate of women in the United States", bls.gov.

Shift toward sustainable and eco‑friendly solutions

The growing emphasis on sustainable and eco-friendly solutions is driving significant growth in the global wipes market. Consumers, regulators, and retailers are increasingly prioritizing environmental responsibility alongside product performance. Concerns over plastic pollution, microplastics in waterways, and sewage blockages caused by conventional synthetic-fiber wipes have led to a rising demand for biodegradable, compostable, and plastic-free alternatives. This trend is particularly prominent in the baby wipes and personal care segments, where sustainability is associated with gentleness, purity, and long-term health safety. Manufacturers are addressing these concerns by redesigning substrates with cellulose- and plant-based fibers, reducing synthetic binders, and incorporating naturally derived, skin-conditioning ingredients that align with clean-label and eco-conscious preferences. For example, in July 2024, Kudos introduced compostable and biodegradable wipes made from sustainably harvested trees. These wipes are infused with skin-safe ingredients such as apple fruit extract and glycerin, providing a soft and gentle cleansing experience for babies while reinforcing their sustainability credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and sustainability issues | -0.4% | Europe and North America regulatory-led, global consumer | Medium term (2-4 years) |

| Regulatory restrictions and compliance burden | -0.2% | Europe core, North America and Asia-Pacific emerging | Long term (≥ 4 years) |

| Fluctuating raw material prices | -0.3% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Competition from alternative cleaning products | -0.2% | Global, digital-first in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental concerns and sustainability issues

Environmental concerns and sustainability challenges have emerged as a critical restraint on the global wipes market, particularly for conventional wet wipes made from synthetic fibers and non-biodegradable plastics. Growing awareness of plastic pollution, microplastic release, and wastewater system blockages caused by improper disposal of wipes has significantly heightened public scrutiny and diminished consumer confidence in traditional products. Municipal authorities and environmental organizations across various regions have repeatedly highlighted the substantial role of wipes in sewage clogging and fatberg formation, further intensifying negative consumer sentiment and driving stricter disposal practices. These sustainability concerns have resulted in escalating regulatory pressures, with governments enforcing more stringent labeling requirements, mandatory plastic-content disclosures, and outright bans on specific wipe formulations, thereby creating substantial compliance challenges for manufacturers.

Regulatory restrictions and compliance burden

Regulatory restrictions and compliance requirements pose significant challenges to the global wipes market, increasing complexity, costs, and operational risks across product development, manufacturing, labeling, and distribution. Governments and regulatory bodies are intensifying oversight on wipes due to concerns related to plastic content, flushability claims, chemical safety, and environmental impact. This forces manufacturers to navigate evolving and often fragmented regulatory frameworks across different regions. Regulations addressing cosmetic safety, biocidal claims, wastewater compatibility, and environmental labeling demand extensive testing, documentation, and third-party certification, thereby extending the time-to-market for new products. In regions such as Europe, stricter environmental legislation, particularly concerning plastic reduction and microplastic control, requires manufacturers to reformulate existing products or discontinue non-compliant lines entirely. Additionally, the need to align with sustainability goals and consumer demand for eco-friendly products further amplifies the pressure on manufacturers to innovate while adhering to regulatory standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Baby Wipes Anchor Revenue, Toilet Wipes Gain Share

Baby wipes are projected to account for 39.86% of total market revenue in 2025, reflecting their strong and sustained dominance. This growth is driven by their necessity for hygiene, frequent daily usage, and ongoing product innovation. Considered an essential caregiving product rather than a discretionary item, baby wipes maintain consistent demand among households with infants and toddlers. Their usage extends beyond diaper changes to general skin cleansing, hand and face wiping, and on-the-go hygiene, significantly increasing per-capita consumption. Additionally, heightened parental awareness regarding infant skin health has bolstered demand for gentle, hypoallergenic, alcohol-free, fragrance-free, and dermatologically tested formulations. These attributes position baby wipes as a safer alternative to water and cloth in various settings. Furthermore, the increasing availability of eco-friendly and biodegradable baby wipes has attracted environmentally conscious consumers, further driving market growth.

Moist toilet wipes are expected to grow at a CAGR of 2.83% through 2031, driven by changing hygiene habits, product repositioning, and increasing adoption beyond traditional toilet paper usage. Consumers are associating moist toilet wipes with enhanced personal cleanliness, comfort, and skin care, particularly for sensitive skin, elderly users, and individuals with medical or mobility-related needs. Compared to dry toilet paper, moist wipes are perceived as more effective for thorough cleansing, encouraging a gradual shift toward combined usage rather than complete substitution. Product innovation has been critical in sustaining growth, with manufacturers introducing flushable variants, biodegradable substrates, pH-balanced formulations, and alcohol- and fragrance-free options to address skin sensitivity and environmental concerns. Additionally, the growing emphasis on sustainable and environmentally friendly products has led to the development of compostable and plastic-free moist wipes, appealing to eco-conscious consumers and supporting long-term market expansion.

By Ingredient: Conventional Formulations Dominate, Natural Variants Accelerate

Conventional formulations are projected to account for 68.01% of the total market share in 2025, underscoring their continued dominance. This is attributed to established consumer trust, cost-effective performance, and broad functional reliability across various end-use segments. Typically formulated with standard preservatives, surfactants, fragrances, and antimicrobial agents, conventional wipes offer proven efficacy in cleaning, sanitization, and skin cleansing. These attributes make them the preferred choice for mass-market applications, including baby care, household cleaning, personal hygiene, and institutional use. Their long shelf life, strong microbial protection, and consistent performance under diverse storage and climatic conditions support large-scale distribution across retail, healthcare, hospitality, and commercial cleaning channels.

Natural and organic wipes are expected to grow at a CAGR of 2.96% through 2031, driven by a structural shift in consumer priorities toward ingredient transparency, skin safety, and environmental responsibility. This trend is particularly evident in the baby care and personal hygiene segments. Parents and health-conscious consumers are increasingly avoiding synthetic preservatives, alcohol, parabens, and artificial fragrances due to concerns about skin irritation, allergies, and long-term exposure. This has created sustained demand for wipes formulated with plant-based fibers, minimal ingredients, and gentle cleansing agents. For example, in November 2025, Popees Baby Care launched premium organic bamboo wipes. These wipes are formulated with pure water derived from 100% organic bamboo and are free from alcohol and added fragrances. The product features 60 GSM ultra-soft wipes that are dermatologically tested, addressing parental concerns about skin safety, dryness, and irritation.

By Distribution Channel: E-Commerce Outpaces Brick-and-Mortar

Supermarkets and hypermarkets are projected to account for 50.65% of the total distribution share in 2025, highlighting their role as the primary purchase channel for everyday hygiene products. This dominance is attributed to high product visibility, a broad assortment of offerings, and the consumer trust associated with organized retail formats. These outlets function as one-stop destinations where wipes are strategically placed across various aisles, including baby care, personal hygiene, household cleaning, and healthcare, promoting impulse purchases and cross-category buying. The ability to physically compare brands, formulations, pack sizes, and price points enhances consumer confidence, particularly in sensitive categories such as baby and personal care wipes. Additionally, these retail formats support high-volume sales through bulk packs, value bundles, and multi-pack promotions, aligning with the frequent and repeat-purchase nature of wipes.

Online retail channels, expanding at a CAGR of 3.34% through 2031 and outpacing brick-and-mortar formats by a full percentage point, are becoming a significant growth driver for the global wipes market. This growth is fueled by changing consumer purchasing behavior, the convenience of digital platforms, and evolving retail ecosystems. Consumers increasingly prefer online platforms for purchasing wipes due to the ease of repeat ordering, access to a wider product assortment, and detailed product information, particularly for sensitive categories such as baby wipes, natural formulations, and specialty hygiene wipes. The rapid expansion of digital commerce infrastructure further supports this trend. For example, according to the United States Census Bureau, e-commerce sales reached USD 310.3 billion in Q3 2025, underscoring the scale and normalization of online purchasing behavior [2]Source: United States Census Bureau, "Quarterly Retail E-Commerce Sales", census.gov. Additionally, targeted digital promotions, personalized recommendations, and influencer-driven marketing on e-commerce platforms are enhancing brand discovery and conversion rates for wipes.

Geography Analysis

North America holding 40.19% of the global wipes market revenue in 2025 reflects the region’s mature consumption patterns, strong hygiene culture, and deep penetration of wipes across baby care, personal hygiene, household cleaning, and healthcare applications. High awareness of infection prevention, routine use of disinfectant and personal wipes, and strong institutional demand from hospitals, long-term care facilities, offices, and hospitality sectors underpin sustained volumes. The region also benefits from brand-led innovation, premium product adoption, and widespread availability across supermarkets, pharmacies, and online platforms. Consumers in North America are early adopters of value-added features such as dermatologically tested formulations, sensitive-skin variants, and multipurpose wipes, supporting higher average selling prices and reinforcing the region’s revenue leadership.

In contrast, Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of 3.81% through 2031, driven by rapid urbanization, expanding middle-class populations, and accelerating development of e-commerce infrastructure. Urban lifestyles and longer commuting times are increasing demand for on-the-go hygiene solutions, while rising health awareness is supporting the adoption of baby wipes, personal care wipes, and household disinfectant wipes across both metropolitan and tier-2 cities. The region is also seeing strong momentum from digital-first retail models, with online marketplaces and quick-commerce platforms improving product accessibility and repeat purchasing. Local manufacturers and multinational brands are actively tailoring formulations, pack sizes, and pricing strategies to suit diverse climatic conditions, skin sensitivities, and cultural hygiene practices, enabling the Asia-Pacific to outperform other regions in growth momentum.

Europe, meanwhile, is playing a pivotal role in reshaping global wipes standards through regulatory leadership, particularly around sustainability and plastic reduction. Environmental concerns related to microplastics, wastewater blockages, and non-biodegradable substrates have prompted stricter oversight of wipe composition and labeling. This regulatory direction is influencing not only regional product portfolios but also global formulation strategies, as multinational brands seek harmonization across markets. For instance, in November 2025, the Department of Agriculture, Environment and Rural Affairs (DAERA) announced new regulations prohibiting the sale and supply of wet wipes containing plastic, with limited exemptions for business-to-business supply and medical use [3]Source: Department of Agriculture, Environment and Rural Affairs (DAERA), "New rules to ban sale and supply of plastic wet wipes being introduced", daera-ni.gov.uk. Such measures are accelerating innovation in plastic-free, biodegradable, and cellulose-based wipes, positioning Europe as a global benchmark for environmentally responsible wipes manufacturing and compliance.

Competitive Landscape

The global wipes market demonstrates moderate consolidation, with a mix of large multinational corporations and numerous regional and niche manufacturers. Prominent companies such as Procter & Gamble Company, Kimberly-Clark Corporation, Essity AB, Diamond Wipes International Inc., and Unilever PLC hold strong market positions. These firms leverage extensive brand portfolios, global distribution networks, and robust manufacturing capabilities. High brand trust, particularly in baby care, personal hygiene, and household wipes, enables these companies to secure significant shelf space in supermarkets, pharmacies, and online platforms. Their scale provides cost efficiencies, consistent product quality, and the ability to rapidly introduce innovations across multiple regions, creating competitive barriers for smaller market entrants.

Despite the dominance of major players, opportunities exist in specific niches, particularly in flushable wipes formats and institutional channels. Increasing regulatory scrutiny regarding plastic content and sewage compatibility has driven demand for genuinely flushable, fiber-based wipes that comply with wastewater safety standards, an area where many current products face credibility issues. Additionally, institutional demand from healthcare facilities, offices, hospitality venues, and industrial workplaces is growing due to stricter hygiene protocols and professional cleaning standards. This segment prioritizes large-volume packs, contract-based supply arrangements, and performance-oriented formulations, offering growth potential for both established companies and specialized manufacturers capable of meeting compliance and performance requirements. Regional players and private-label brands are increasingly targeting these niches to differentiate themselves from mass-market consumer products.

Technological innovation is a critical factor influencing product performance and sustainability in the wipes market. Leading companies are investing in advancements in nonwoven substrate technology, including biodegradable fibers, plastic-free materials, and higher GSM fabrics that enhance softness, strength, and absorbency. Innovations in lotion chemistry, such as pH-balanced formulations, reduced preservative systems, and skin-barrier-supporting ingredients, are improving safety and efficacy, particularly for baby and sensitive-skin applications. Furthermore, packaging innovations, including improved resealability, tubeless dispensing, and smart labeling, are enhancing shelf life and user convenience. As environmental regulations become stricter and consumer expectations rise, the ability to integrate technology-driven sustainability, performance, and compliance is increasingly shaping market leadership and long-term competitiveness in the global wipes market.

Wipes Industry Leaders

-

Procter & Gamble Company

-

Kimberly-Clark Corporation

-

Essity AB

-

Diamond Wipes International Inc.

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: WaterWipes has launched its most durable wipe to date. The new WaterWipes are noticeably thicker and softer, providing an effective clean while being gentle on sensitive skin. The wipes also feature a refreshed design with an embossed WaterWipes pattern made from softer, finer fibers.

- January 2025: Panacea Biotec's wholly-owned subsidiary, Panacea Biotec Pharma Limited, has introduced baby diapers and wipes under the brand name NikoMom. These products are described as hypoallergenic, toxin-free, and dermatologically and pediatrician-tested.

- May 2024: Medicare Hygiene introduced eco-friendly wet wipes, marking its diversification into the cosmetics segment. Earthika Wet Wipes are made from ethically sourced, eco-friendly materials, aiming to provide users with instant freshness and confidence.

- May 2024: Wipemate introduced its premium-quality wipes across the United States and other operational regions. The product range includes beauty wipes, pet wipes, and other home care wipes, all of which are 100% compostable.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global wipes market as the value generated from single-use non-woven or fabric substrates pre-impregnated or dry, sold for personal care, household, industrial, and institutional cleaning or hygiene purposes. They include baby, cosmetic, moist toilet, surface, disinfectant, and other specialty wipes and are tracked at the first commercial sale price.

Scope exclusion: Industrial shop towels and bulk roll wipers sold purely as raw non-woven material are kept outside the model.

Segmentation Overview

-

By Product Type

- Baby Wipes

- Cosmetic Wipes

- Moist Toilet Wipes

- Home Care Wipes

- Others

-

By Ingredient

- Conventional

- Natural/Organic

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribtution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed manufacturers, contract converters, packaging suppliers, retail buyers, and infection-control specialists across North America, Europe, Asia-Pacific, and the Middle East. These conversations validated average selling prices, substrate mix shifts, biodegradable uptake rates, and channel inventory norms, closing information gaps left by desk research.

Desk Research

We began with public statistics from sources such as the US Census Bureau trade data, Eurostat PRODCOM, China Customs, and Japan's METI shipment surveys, which help size export-import flows and domestic output of non-woven hygiene articles. Industry association briefs from INDA, EDANA, and the World of Wipes conference proceedings provided unit penetration clues, while company 10-Ks and select press releases clarified segment revenue splits and pricing moves. In addition, paid intelligence from D&B Hoovers, Dow Jones Factiva, and Questel patents offered supplier financials, news sentiment, and technology adoption indicators. National health agencies, waste-management regulations, and peer-reviewed journals on micro-plastics informed ingredient trend variables. The list above is illustrative; many other open and subscription sources were mined to build, cross-check, and enrich our evidence base.

Market-Sizing & Forecasting

A top-down demand pool anchored on national household counts, birth rates, healthcare bed days, and food-service outlets was created, then balanced with selective bottom-up supplier roll-ups to test plausibility. Key variables like per-capita wipe consumption, average pack size, substrate cost inflation, retail-private-label share, regulatory phase-outs, and e-commerce penetration drive our Excel-based model. A multivariate regression with scenario analysis projects values to 2030; missing micro-data are bridged through regional proxies agreed upon during expert calls.

Data Validation & Update Cycle

Outputs undergo variance checks against shipment trends and commodity price movements, followed by a two-step analyst peer review. The report is refreshed each year, with interim tweaks when material events such as raw-material shocks or major legislation occur.

Why Our Wipes Market Baseline Commands Reliability

Published figures often diverge because firms pick different product mixes, price bases, and refresh cadences. Our disciplined scoping, variable selection, and annual update ensure users receive a balanced view rather than an optimistic or overly narrow snapshot.

Key gap drivers include: some publishers counting only personal-care wipes, others blending industrial shop towels; a few models apply aggressive premium-price assumptions, while others freeze exchange rates; still others extend forecasts without verifying regulatory cut-off dates that erode plastic-based volume.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.73 B (2025) | Mordor Intelligence | - |

| USD 4.86 B (2024) | Regional Consultancy A | Excludes household and industrial wipes; uses factory-gate prices only |

| USD 22.90 B (2024) | Global Consultancy A | Mixes wet and dry rolls, counts multi-use shop towels, limited currency normalization |

Taken together, the comparison shows that Mordor's carefully delimited scope and annual ground-truthing provide a dependable midpoint that decision-makers can replicate and audit with limited effort.

Key Questions Answered in the Report

What is the current value of the global wipes market?

The global wipes market was valued at USD 18.81 billion in 2026.

Which product segment is growing fastest?

Moist toilet wipes are advancing at a 2.83% CAGR between 2026 and 2031.

How fast is online retail growing within wipes distribution?

Online channels are forecasted to experience sustained growth, achieving a projected CAGR of 3.34% during 2026-2031.

Which region shows the quickest growth?

Asia-Pacific leads with a 3.81% CAGR during 2026-2031, driven by urbanization and digital commerce expansion.

Page last updated on: