Diaper Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 73.71 Billion |

| Market Size (2031) | USD 99.43 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

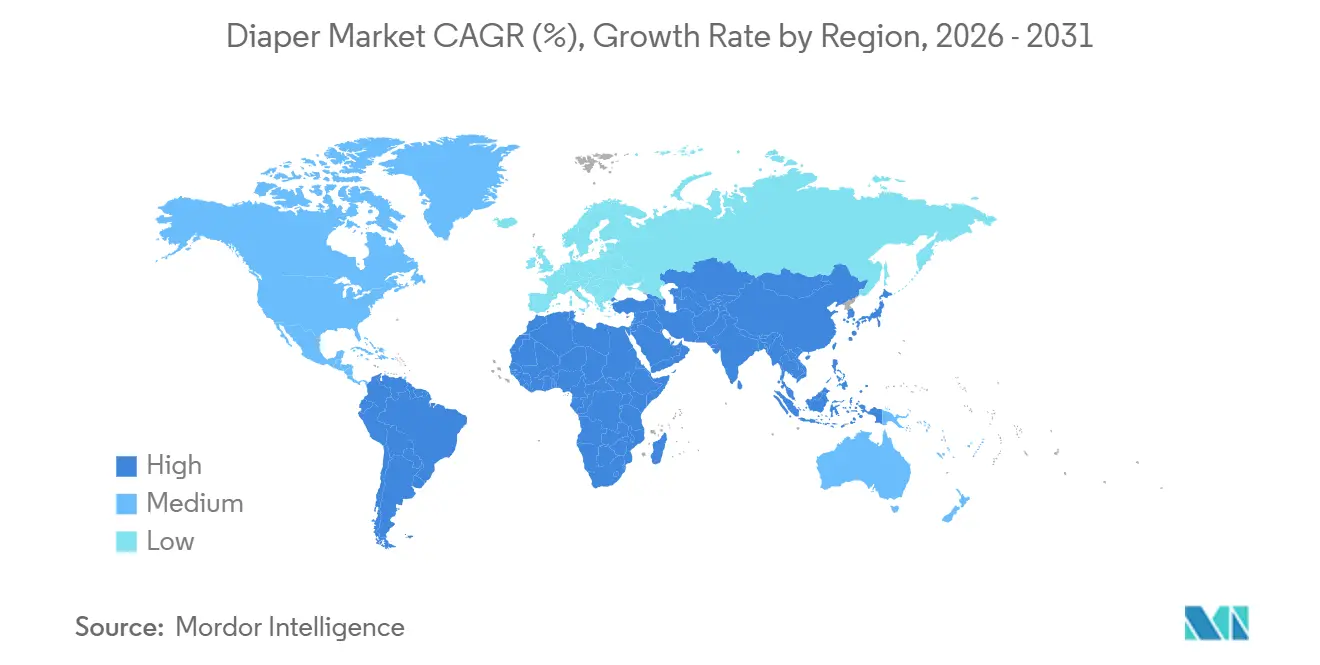

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

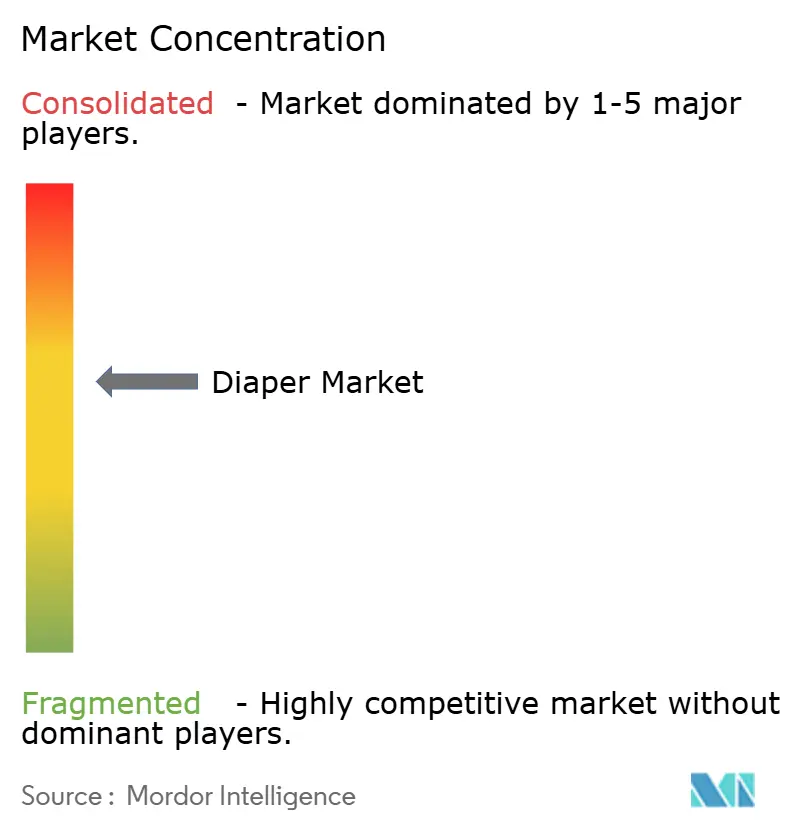

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diaper Market Analysis by Mordor Intelligence

The diaper market size is expected to increase from USD 70.13 billion in 2025 to USD 73.71 billion in 2026 and reach USD 99.43 billion by 2031, growing at a CAGR of 6.17% over 2026-2031.Demand is shifting from infant care products to adult incontinence solutions due to aging global populations and declining birth rates, particularly in China and Japan. Manufacturers are allocating research and development budgets toward high-performance super-absorbent polymers and breathable nonwovens to maintain premium pricing, despite fluctuations in raw material costs. Sustainability regulations in Europe and several United States states are accelerating the adoption of bio-based materials. Additionally, e-commerce subscription models are strengthening brand loyalty and minimizing the risk of stock shortages. While competitive intensity remains moderate, with the top five suppliers dominating shelf space, direct-to-consumer brands are challenging this position through targeted online marketing and quicker product innovation cycles.

Key Report Takeaways

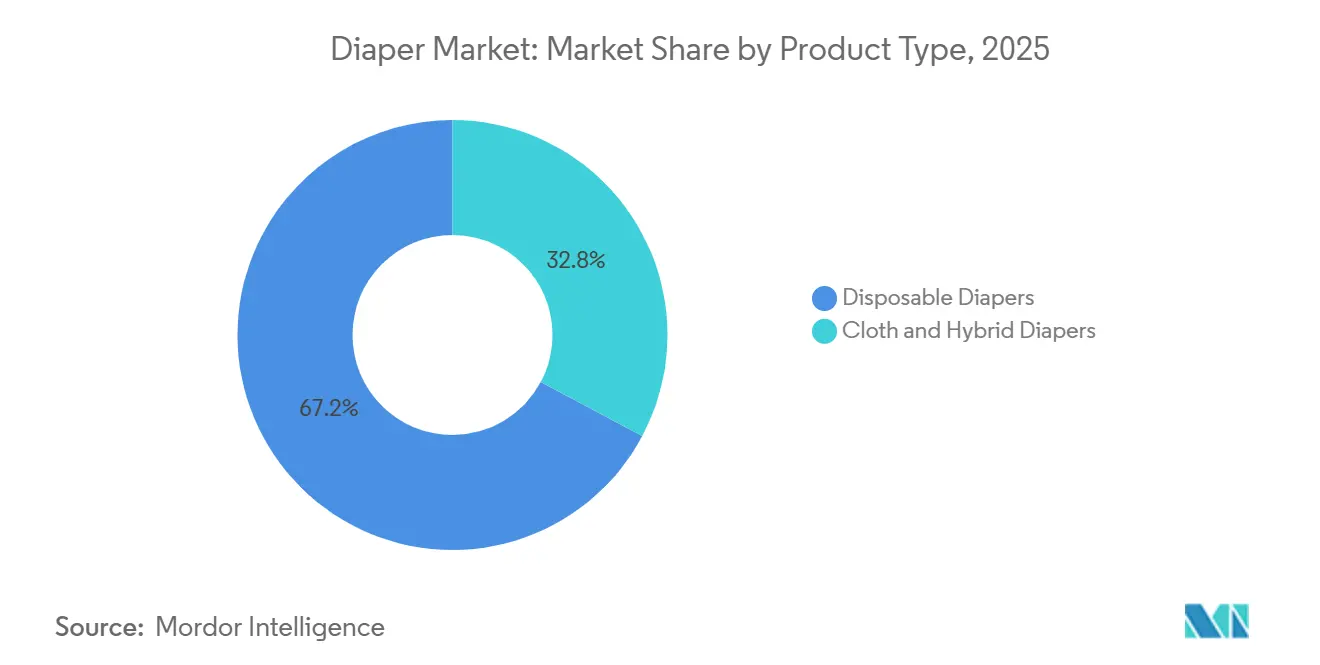

- By product type, disposable diapers led with 67.21% of Diaper market share in 2025, whereas cloth and hybrid formats are forecast to post a 7.52% CAGR to 2031.

- By age group, the adult segment accounted for 45.83% of 2025 volume and is projected to rise at a 7.21% CAGR through 2031.

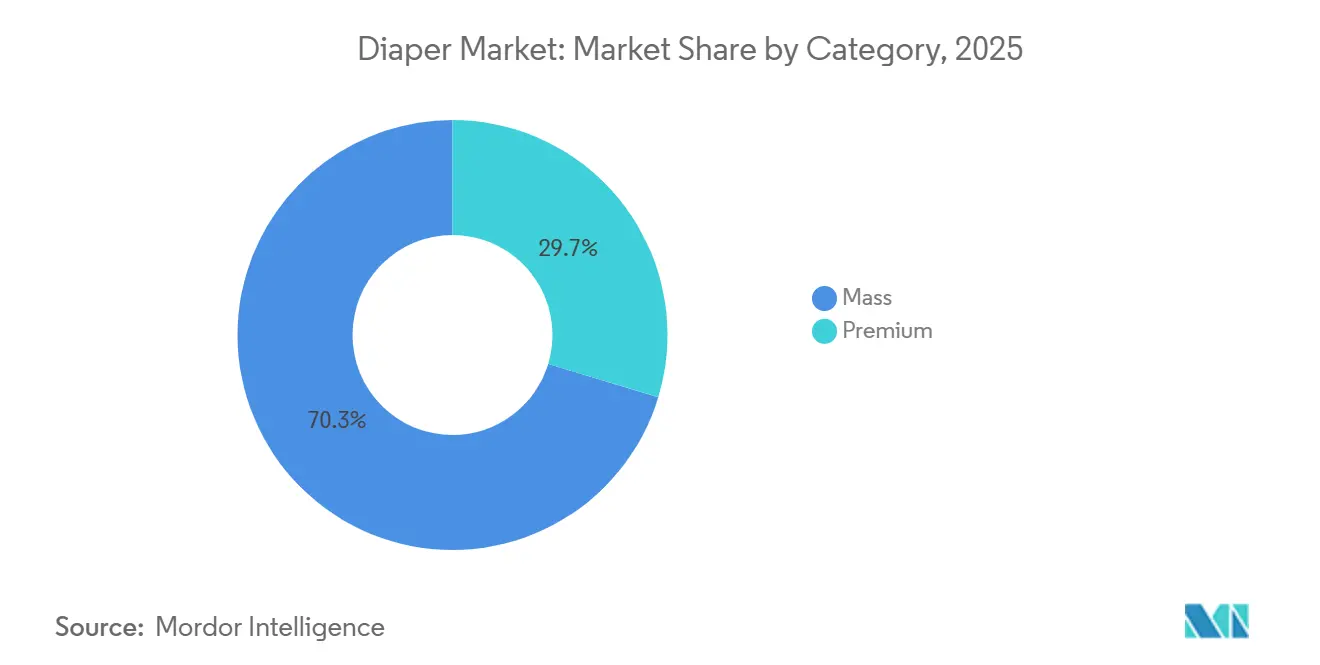

- By category, mass products held 70.32% of the Diaper market size in 2025, yet the premium tier is on track for a 7.12% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets retained 33.32% share in 2025, while alternative outlets, including direct-to-consumer subscriptions, are expected to expand at 6.81% annually.

- By geography, Asia-Pacific generated 40.12% of 2025 revenue and remains the growth engine, but the Middle East and Africa region shows the fastest trajectory at a 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diaper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of adult incontinence due to aging populations and longer life expectancy | +1.8% | Global, concentrated in Japan, Germany, United States, China | Long term (≥ 4 years) |

| Increasing awareness of infant hygiene and skin health among parents | +1.2% | Asia-Pacific core, spillover to Middle East and Africa, Latin America | Medium term (2-4 years) |

| Technological advancements in superabsorbent polymers for better leakage protection | +0.9% | Global, led by North America and Europe R&D hubs | Medium term (2-4 years) |

| Growing demand for eco-friendly and biodegradable diaper options | +0.7% | North America and Europe, early adoption in urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of e-commerce and subscription services for easy access | +0.6% | Global, strongest in India, Southeast Asia, Brazil | Short term (≤ 2 years) |

| Innovations in skin-friendly, hypoallergenic materials to prevent rashes | +0.5% | Global, premium segments in North America, Europe, urban China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of adult incontinence due to aging populations and longer life expectancy

Adult incontinence has shifted from being a niche issue to a significant concern in the broader market, influencing product development strategies. In the United States, millions of adults are affected by bladder conditions, with prevalence rates higher among women compared to men. In Germany, the overall incontinence rate has shown an increase, with a higher prevalence among females than males. In China, the elderly population shows even more pronounced trends, with a significant percentage of women and men over the age of 65 experiencing incontinence. The population aged 60 and above in China represents a substantial portion of the total population. In Japan, a significant milestone was reached when adult diaper demand surpassed that of baby diapers, leading at least one major manufacturer to discontinue infant diaper production and shift focus to elderly care products. In the coming decades, the United States is projected to have a growing population of adults aged 65 and older. With increasing life expectancy, these individuals are expected to spend more years managing chronic conditions. This demographic shift is driving manufacturers to develop discreet, high-capacity products with odor-control features, catering to active seniors who prioritize mobility and independence.

Increasing awareness of infant hygiene and skin health among parents

Parental concerns about diaper rash and skin irritation have increased, driven by the influence of digital platforms that amplify peer reviews and dermatological research. Diapers containing shea butter-based emollients have shown measurable reductions in erythema, highlighting the effectiveness of plant-derived barrier creams integrated into nonwoven layers. In September, Sam's Club introduced its Member's Mark Premium Diaper, emphasizing a hypoallergenic construction free from lotions, parabens, and fragrances, along with sustainably sourced pulp. This product appeals to millennial and Generation Z parents who carefully examine ingredient lists. In India, where urbanization has been steadily increasing and middle-class households are expected to grow significantly in the coming years, parents are increasingly shifting from cloth to disposable diapers and from economy to premium options as disposable incomes rise. Digital commerce platforms such as Meesho, which reported a large number of annual transacting users in fiscal year 2025, with a significant portion of these users from non-metropolitan regions, are expanding access to branded hygiene products in Tier 2 and Tier 3 cities, where traditional retail penetration remains limited. This transition from unbranded to branded consumption represents a structural shift rather than a cyclical trend, ensuring sustained volume growth even as birth rates stabilize or decline in urban areas.

Technological advancements in superabsorbent polymers for better leakage protection

Innovation in superabsorbent polymers is focusing on two key areas: performance enhancement and sustainability. In February 2025, BASF introduced HySorb B 6610 ZeroPCF, a zero-carbon-footprint superabsorbent polymer manufactured using renewable electricity and bio-based acrylic acid. This product achieves absorption capacities comparable to traditional petroleum-derived polymers, according to a BASF press release. Similarly, Ontex developed bioSAP, a partially bio-based polymer that reduces the carbon footprint significantly while maintaining high absorption ratios suitable for overnight protection. Additionally, cellulose-based hydrogels synthesized with citric acid and glycerol demonstrated notable absorption capacities in synthetic urine. However, their commercial viability is limited due to cost and scalability challenges. The strategic implication is that established players with significant research and development resources can protect margins through proprietary formulations. In contrast, smaller competitors lacking expertise in polymer development may face difficulties in differentiating their products based on performance. These smaller players could lose market share to private-label brands or direct-to-consumer companies that emphasize transparency and sustainability narratives over absorption performance metrics.

Growing demand for eco-friendly and biodegradable diaper options

Regulatory pressure and consumer activism are driving the transition toward biodegradable materials. The European Union's Single-Use Plastics Directive targets wet wipes and sanitary items, while Regulation 2023/2055 restricts microplastics in consumer products, requiring manufacturers to reformulate adhesives and nonwoven layers [1]Source: European Union, “Single-Use Plastics Directive,” eur-lex.europa.eu. Additionally, the European Union Packaging Regulation 2025/40 mandates 30 percent to 35 percent recycled content in plastic packaging by 2030, necessitating significant investments in reverse logistics and material separation technologies. In the United States, New York has enacted an ingredient labeling law effective December 2025, and Oregon expanded its Toxic-Free Kids Act in January 2025. Both regulations require brands to disclose chemical compositions and phase out substances of concern. Similarly, France introduced extended producer responsibility for single-use sanitary textiles in January 2025, transferring disposal costs to manufacturers and encouraging designs that prioritize recyclability, as noted by the French Ministry of Ecological Transition [2]Source: French Environmental Ministry, “Extended Producer Responsibility for Sanitary Textiles,” ecologie.gouv.fr. These regulatory developments favor vertically integrated companies such as Procter and Gamble and Kimberly-Clark, which are better positioned to absorb compliance costs and utilize their scale to source certified bio-based pulp and polymers. In contrast, smaller brands face challenges such as margin compression or potential market exit unless they establish partnerships with specialty material suppliers or adopt premium positioning to justify higher retail prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns over non-biodegradable plastic waste in landfills | -0.8% | Global, acute in Europe and coastal Asia-Pacific cities | Long term (≥ 4 years) |

| Stringent regulations on material safety and waste disposal | -0.6% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Low awareness of diaper benefits in rural or traditional areas | -0.4% | Sub-Saharan Africa, rural India, interior Latin America | Long term (≥ 4 years) |

| Dependency on imported raw materials affecting supply reliability | -0.5% | Global, acute in regions without domestic SAP production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental concerns over non-biodegradable plastic waste in landfills

Disposable diapers make up a small but notable portion of municipal solid waste in developed economies. Their long decomposition periods have become a significant concern for environmental advocacy groups and municipal waste management authorities. The European Union's Single-Use Plastics Directive specifically addresses sanitary items, prompting member states to explore extended producer responsibility (EPR) schemes that transfer disposal costs to manufacturers. For example, France introduced extended producer responsibility for single-use sanitary textiles in January 2025, requiring brands to finance collection and recycling infrastructure. In coastal cities across the Asia-Pacific region, where landfill capacity is limited and incineration raises air quality concerns, municipal governments are implementing landfill taxes and waste-reduction mandates. These policies increase the overall cost of ownership for disposable products. At the same time, consumer attitudes are changing. Surveys conducted in North America and Europe show that many parents, particularly millennials and Generation Z, feel guilt over diaper waste and are actively exploring biodegradable or cloth alternatives. This shift in sentiment is leading to market share declines for conventional disposable diapers, especially in premium segments where environmentally conscious consumers are more prevalent. Brands that do not implement credible sustainability initiatives, supported by third-party certifications such as the Cradle to Cradle standard or the United States Department of Agriculture BioPreferred label, risk losing market share. Niche competitors and private-label products marketed as environmentally sustainable are gaining traction among consumers who prioritize environmentally friendly options. For instance, the United States Department of Agriculture (USDA) BioPreferred label is increasingly recognized as a marker of sustainability, influencing purchasing decisions in favor of certified products.

Stringent regulations on material safety and waste disposal

Regulatory complexity is increasing across jurisdictions, leading to fragmented compliance requirements and higher market entry costs. The European Union's (EU) microplastics restriction, Regulation 2023/2055, limits the use of intentionally added microplastics in consumer products, necessitating the reformulation of adhesives and nonwoven layers. Additionally, the EU Packaging Regulation 2025/40 requires 30% to 35% recycled content in plastic packaging by 2030, which will demand substantial investment in reverse logistics and material separation technologies. In the United States, New York's ingredient labeling law, effective December 2025, and Oregon's expansion of the Toxic-Free Kids Act in January 2025, require brands to disclose chemical compositions and eliminate substances of concern [3]Source: Oregon Legislature, “Toxic-Free Kids Act Expansion,” oregonlegislature.gov. These regulations place a disproportionate burden on smaller manufacturers and regional players, who often lack the legal and technical resources to manage multi-jurisdictional compliance. In contrast, larger companies such as Procter and Gamble, Kimberly-Clark, and Unicharm can distribute compliance costs across global operations and use their scale to secure favorable terms with certified material suppliers. This creates a barrier to entry that consolidates market share among established players. The strategic risk lies in regulatory fragmentation potentially delaying product launches and innovation cycles, as brands must ensure formulations meet evolving standards in each major market before proceeding with production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Dominate but Hybrids Gain Traction

Disposable diapers accounted for 67.21% of the market in 2025, highlighting their strong presence in urban households where convenience and performance take precedence over environmental concerns. Cloth and hybrid diapers, although starting from a smaller market base, are projected to grow at an annual rate of 7.52% through 2031, marking the fastest growth among product types. This growth is driven by environmentally conscious parents and institutional childcare centers seeking alternatives to petroleum-based superabsorbent polymers. In February 2025, BASF introduced HySorb B 6610 ZeroPCF, a zero-carbon-footprint superabsorbent polymer made using renewable electricity and bio-based acrylic acid, indicating that established players are investing in sustainable formulations to maintain their share in the disposable diaper market.

Similarly, Ontex's bio-based superabsorbent polymer (bioSAP), which offers a 15% to 25% reduction in carbon footprint, demonstrates that incorporating partial bio-based content can help bridge the performance gap between conventional and fully biodegradable options. The key challenge remains whether disposable diapers can adapt quickly enough to meet regulatory requirements and consumer expectations or if hybrid diapers will secure a lasting position among affluent, environmentally conscious consumers.

By Age Group: Adult Segment Outpaces Baby Despite Smaller Base

In the United States, approximately 100 million adults are affected by bladder conditions, with a prevalence of 14% among men and 51% among women, according to the National Association for Continence. In Germany, the overall incontinence rate was reported at 14.7% in 2025, increasing to 17.8% among females, as noted in a peer-reviewed epidemiology study. These statistics highlight that adult incontinence has transitioned from being a niche issue to a widespread concern, influencing product development strategies.

Manufacturers are addressing this shift by focusing on discreet, high-capacity designs and odor-control technologies that cater to active seniors who prioritize mobility. Procter and Gamble's Pampers Preemie Extra Extra Small (XXS), introduced in November 2025, is designed for premature infants weighing less than 500 grams. This product not only meets a specific medical need but also reflects the brand's strategy to further segment the baby care market.

By Category: Mass Leads but Premium Grows Faster

Mass-market products accounted for 70.32% of the market in 2025, highlighting the price sensitivity of the majority of consumers. However, the premium category is projected to grow at an annual rate of 7.12% through 2031, driven by affluent urban households seeking hypoallergenic materials, transparent sourcing, and enhanced product performance. Procter and Gamble's Pampers AMORE, introduced in March 2026 with cashmere-soft materials, targets this segment and has contributed to the brand's double-digit growth and a three-percentage-point market share increase in Greater China, where organic sales rose by 20% in the latest quarter.

Coterie, a direct-to-consumer brand positioned at twice the price of traditional brands, reported revenues exceeding USD 200 million and a year-on-year growth of 60% before being acquired by Mammoth Brands for over USD 1 billion in October 2025. Sam's Club's Member's Mark Premium Diaper, launched in September 2025, reflects the trend of premiumization even among warehouse clubs, offering hypoallergenic construction free from lotions, parabens, and fragrances, along with sustainably sourced pulp.

By Distribution Channel: Supermarkets Hold Share but Alternative Channels Surge

Supermarkets and hypermarkets are projected to account for 33.32% of the market in 2025, underscoring their established role in weekly household shopping. However, other distribution channels, including direct-to-consumer subscriptions, pharmacy chains, and specialty baby stores, are expected to grow at an annual rate of 6.81% through 2031. With the increasing penetration of e-commerce and a growing emphasis on convenience, Amazon's third-party seller services generated over USD 156 billion in 2024, while its subscription services segment exceeded USD 44 billion. This reflects the platform's ability to secure recurring revenue through automatic replenishment models, as outlined in Amazon's annual 10-K filing. Same-day delivery now spans thousands of ZIP codes across the United States, reducing barriers for bulk diaper purchases and enabling parents to avoid stockpiling, according to Amazon corporate disclosures. In India, Meesho's fiscal 2025 user base of nearly 199 million, including approximately 174 million users from non-metro regions, highlights the potential of application-based retail in areas where traditional supermarkets and hypermarkets have limited presence.

Geography Analysis

In 2025, the Asia-Pacific region led the market, accounting for 40.12% of the total share. This dominance was driven by Unicharm's strong presence in India, where the company operates three factories and holds a significant market share, second only to Procter & Gamble. Unicharm's third factory in Gujarat, a Japanese Yen (JPY) 20 billion investment announced in February 2025, is expected to boost production capacity by 30% and create approximately 1,000 jobs. In China, despite a decline in births from 14.7 million in 2019 to 7.92 million in 2025, the market remains critical due to premiumization. Procter & Gamble's Pampers Prestige line, featuring silk fibers, achieved double-digit growth and a three-percentage-point market share increase, with Greater China organic sales rising by 20% in the latest quarter. In Japan, a demographic shift in 2024, where adult diaper demand surpassed baby diaper volumes, led at least one major manufacturer to cease infant diaper production and refocus on elderly care products.

The Middle East and Africa region is projected to grow at the fastest rate globally, with a compound annual growth rate (CAGR) of 7.08% through 2031. This growth is fueled by accelerating urbanization in countries such as Nigeria, Egypt, and Saudi Arabia, along with improvements in healthcare infrastructure. Unicharm's joint venture with Toyota Tsusho in Kenya, announced in June 2025 and named Sofy East Africa Limited, aims to produce baby care and feminine care products. This move reflects the company's confidence in the region's long-term potential.

Other regions, such as North America and Europe, face challenges from stagnant birth rates but benefit from premiumization trends. Kimberly-Clark's USD 2 billion investment over five years in North American manufacturing, including an approximately USD 800 million facility in Warren, Ohio, focuses on producing next-generation Huggies with automated waistbands and quilted protection, emphasizing a shift toward higher-margin products. In South America, the market remains fragmented, with local players competing on price and incumbents facing challenges from currency volatility and import dependency. For instance, Brazil's Cost, Insurance, and Freight (CIF) Santos superabsorbent polymer prices rose to USD 1,450 to USD 1,470 per metric ton in the third quarter of 2025, an 11.46% increase, highlighting the region's susceptibility to global supply chain disruptions. However, urbanization and rising disposable incomes in countries like Colombia, Chile, and Peru are creating opportunities for premium products. Global brands face the strategic challenge of balancing the need for local manufacturing to mitigate currency risks against the high capital requirements of establishing greenfield facilities in markets with uncertain regulatory environments and infrastructure limitations.

Competitive Landscape

The diaper market presents a moderately consolidated structure, with the top five players, Procter and Gamble, Kimberly-Clark, Unicharm, Essity, and Kao, dominating significant shelf space. However, these companies face increasing competition from direct-to-consumer brands and regional specialists. Kimberly-Clark's acquisition of Kenvue for USD 48.7 billion, announced in November 2025 and expected to close in the second half of 2026, is set to create a combined entity with approximately USD 32 billion in revenue and USD 2.1 billion in anticipated synergies. This move is expected to further consolidate the North American market while enabling cross-selling opportunities across baby care, skin health, and oral care product categories, as per Kimberly-Clark investor communications.

Procter and Gamble is focusing on premiumization, exemplified by the launch of Pampers AMORE in March 2026, featuring cashmere-soft materials and achieving double-digit growth in Greater China. Unicharm is aggressively expanding in emerging markets, with a Japanese Yen (JPY) 20 billion investment in a third factory in Gujarat, India, inaugurated in February 2025, and the formation of a joint venture in Kenya in June 2025 to produce baby care and feminine care products. Kao is leveraging strategic partnerships to enter new markets, including a distribution agreement with Magicwave in Vietnam in 2026 to expand its Merries brand, which highlights breathable technology with 5 billion air vents.

Opportunities for growth exist in areas such as adult incontinence products for active seniors, biodegradable materials that meet regulatory requirements without compromising performance, and subscription models that ensure recurring revenue. Direct-to-consumer brands like Coterie illustrate the potential of premium positioning. Mammoth Brands acquired Coterie for over USD 1 billion in October 2025 after the brand reported revenue exceeding USD 200 million and year-on-year growth of 60%. Coterie's success demonstrates that affluent urban households are willing to pay a premium, double the price of legacy brands, for hypoallergenic materials and transparent sourcing practices.

Diaper Industry Leaders

Procter & Gamble Co.

Kimberly-Clark Corp.

Unicharm Corp.

Essity AB

Kao Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hiro Technologies introduced MycoDigestible diapers, utilizing fungi to accelerate the breakdown of organic materials, thereby significantly reducing degradation times. This development targets environmental challenges linked to traditional diaper waste.

- May 2025: Kimberly-Clark has announced a USD 2 billion expansion of its manufacturing operations in North America. This includes an investment of USD 800 million in a new diaper manufacturing facility in Warren, Ohio. Furthermore, the company is upgrading its operations in South Carolina, which is expected to create 900 new skilled jobs.

- December 2024: Unicharm and Toyota Tsusho have initiated local production of sanitary products, including pads and diapers, in Kenya. This effort seeks to meet the increasing demand for affordable and accessible hygiene products in the region, supporting better public health and hygiene standards.

- September 2024: Doms Industries has acquired a 51.77% stake in Uniclan Healthcare for USD 54.88 million, obtaining a controlling interest in the company. This acquisition includes the ownership of the Wowper diaper brand, enhancing Doms Industries' presence in the healthcare and personal care market.

Global Diaper Market Report Scope

The diaper market includes disposable and reusable absorbent products designed for both babies and adults to address urine and fecal incontinence. Key factors driving the market are the increasing awareness of hygiene, the growing aging population, and the rising preference for convenience-oriented lifestyles across the globe. The market is segmented based on product type into disposable diapers, cloth diapers, and hybrid diapers; by age group into baby diapers and adult diapers; by category into premium and mass products; and by distribution channel into supermarkets and hypermarkets, pharmacies and drugstores, online retail, and other distribution channels. Additionally, the market is analyzed geographically across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Disposable Diapers |

| Cloth and Hybrid Diapers |

| Baby Diaper |

| Adult Diaper |

| Premium |

| Mass |

| Supermarkets and Hypermarkets |

| Pharmacies and Drugstores |

| Online Retail/E-commerce |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Disposable Diapers | |

| Cloth and Hybrid Diapers | ||

| By Age Group | Baby Diaper | |

| Adult Diaper | ||

| By Category | Premium | |

| Mass | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Pharmacies and Drugstores | ||

| Online Retail/E-commerce | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Diaper market by 2031?

The Diaper market size is forecast to reach USD 99.4 billion by 2031.

Which product type is growing the fastest?

Cloth and hybrid formats are expected to post a 7.52% CAGR from 2026 to 2031 as eco-conscious buyers seek lower-waste solutions.

Why is adult diaper demand outpacing baby diaper demand?

Aging populations and longer life expectancy are boosting adult incontinence prevalence, leading to a 7.21% CAGR for the adult segment through 2031.

How are regulations influencing diaper design?

European and U.S. rules on recycled content and microplastics are driving manufacturers to adopt bio-based super-absorbent polymers and recyclable packaging.

Which region shows the fastest revenue growth?

The Middle East and Africa region is projected to expand at a 7.08% CAGR to 2031 due to rapid urbanization and improving healthcare infrastructure.

Page last updated on: