Market Overview

| Study Period | 2021 - 2031 |

|---|---|

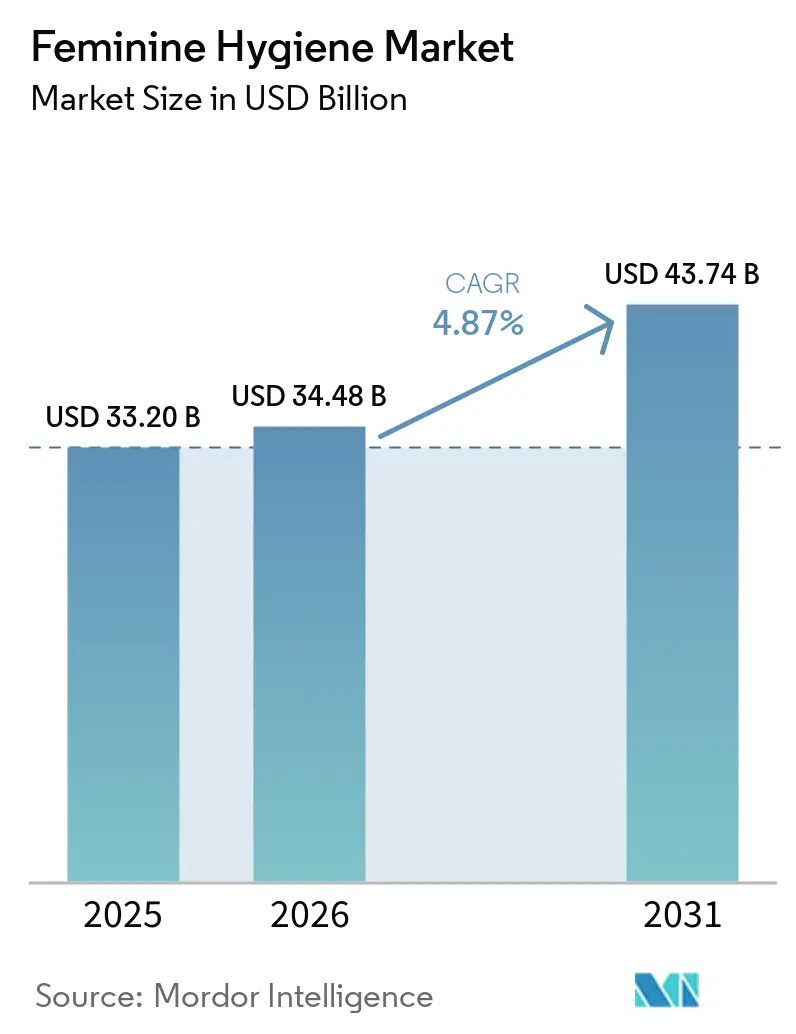

| Market Size (2026) | USD 34.48 Billion |

| Market Size (2031) | USD 43.74 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

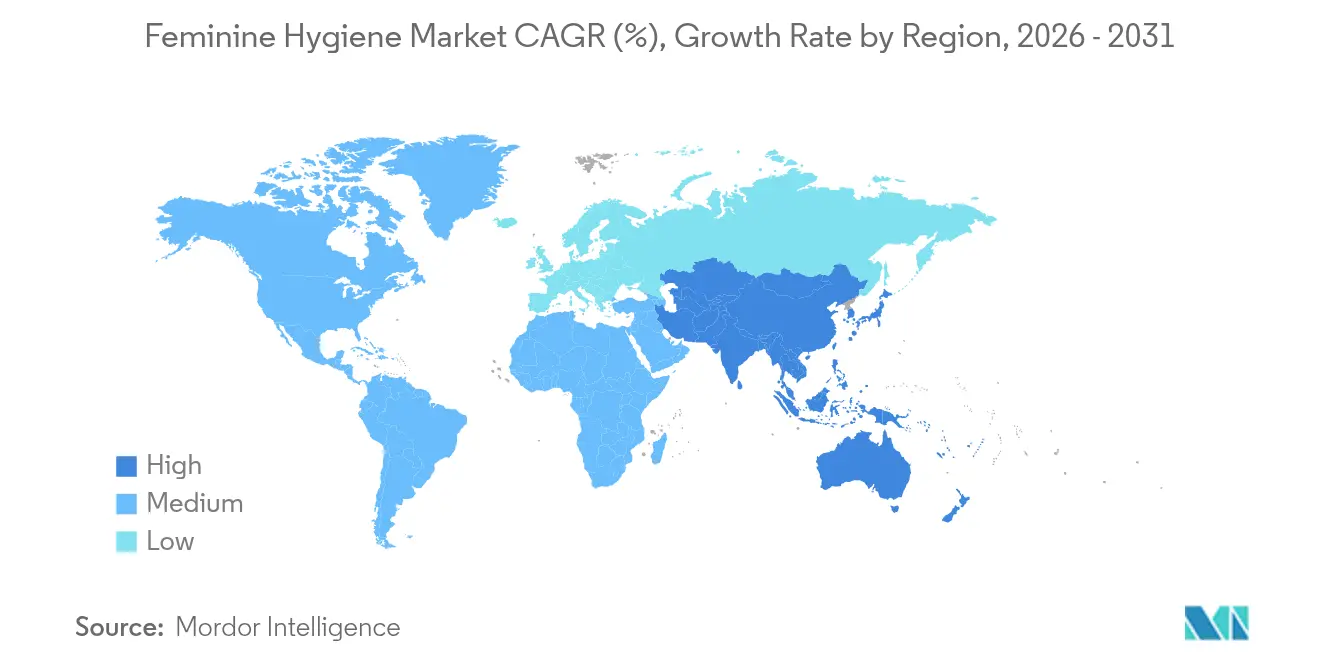

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Feminine Hygiene Market Analysis by Mordor Intelligence

The feminine hygiene market size was valued at USD 33.20 billion in 2025 and estimated to grow from USD 34.48 billion in 2026 to reach USD 43.74 billion by 2031, at a CAGR of 4.87% during the forecast period (2026-2031). Heightened consumer interest in sustainable materials, widening institutional procurement mandated by menstrual equity laws, and rapid e-commerce adoption underpin this growth trajectory. North America remains the revenue leader, yet Asia-Pacific delivers the fastest incremental volumes as access programs and cultural acceptance converge with rising disposable income. Besides, disposable sanitary pads retain the largest individual category share, although reusable menstrual cups record the highest growth as value-minded and eco-conscious shoppers pivot toward long-life options. Additionally, channel dynamics continue to shift: pharmacy chains still dominate sales, but online platforms record the most robust traffic gains as discreet doorstep delivery and subscription replenishment appeal to digital-first consumers.

Key Report Takeaways

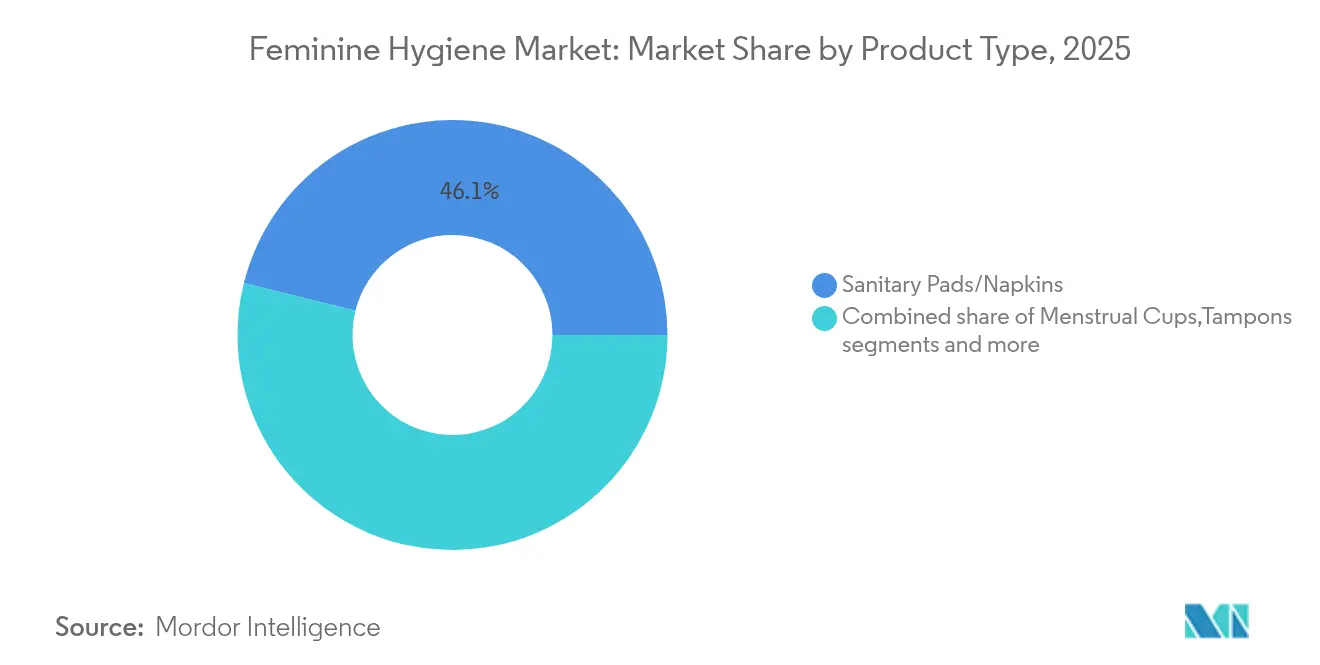

- By product type, sanitary pads held 46.12% revenue share in 2025, while menstrual cups are forecast to expand at a 7.07% CAGR through 2031.

- By product category, disposable items captured 78.12% of the feminine hygiene market share in 2025, whereas reusable alternatives are projected to advance at a 7.41% CAGR.

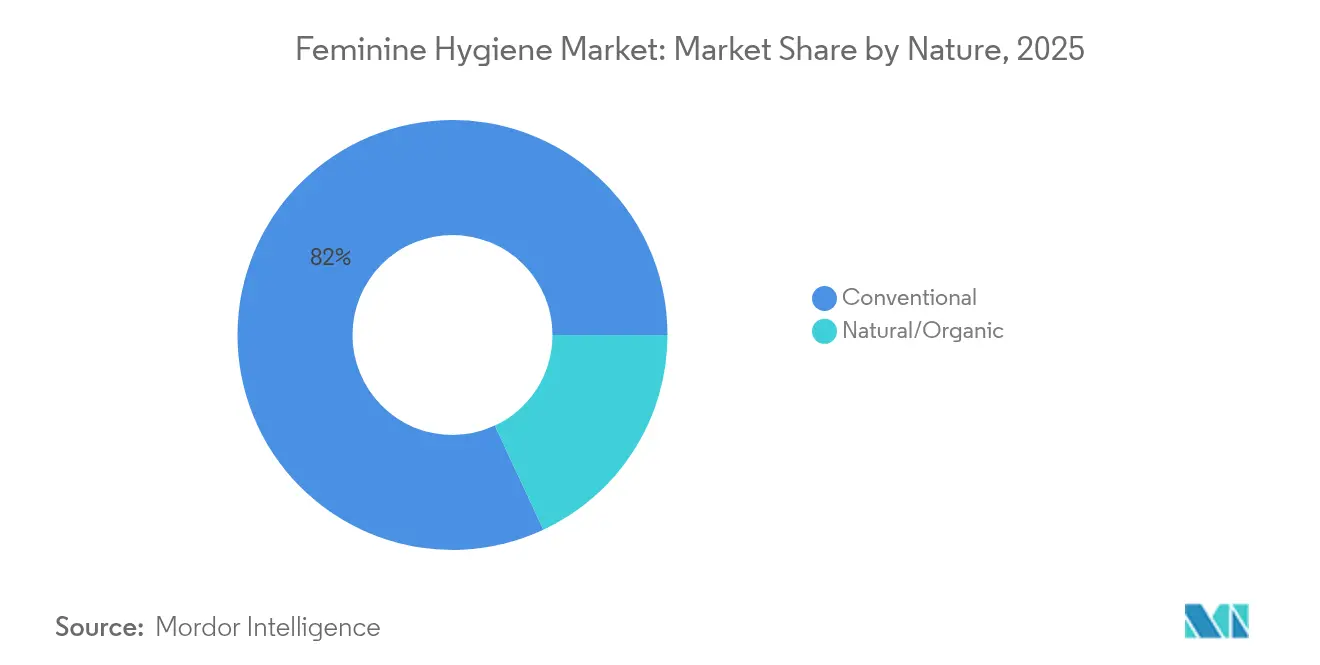

- By nature, conventional products accounted for 81.95% of the feminine hygiene market size in 2025, while natural/organic offerings are growing at a 7.6% CAGR.

- By distribution channel, pharmacy and drug stores led with 38.35% share in 2025; online retail stores posted the highest forecast CAGR at 6.79%.

- By geography, North America contributed 36.60% of 2025 revenue, whereas Asia-Pacific is projected to record a 6.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feminine Hygiene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness and education about feminine hygiene and health | +1.2% | Global, with stronger impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Increasing governmental and NGO initiatives promoting feminine hygiene awareness in developing regions | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Influence of social media diversifying product discovery | +0.6% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Growing demand for sustainable and biodegradable products | +1.0% | North America and European Union, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Stricter mandates for ingredient disclosure and product labeling | +0.4% | North America and European Union regulatory frameworks | Short term (≤ 2 years) |

| Menstrual-equity mandates (free products in public spaces) | +0.7% | North America leading, expanding to European Union and select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising awareness and education about feminine hygiene and health

Educational initiatives and awareness programs are driving increased adoption of feminine hygiene products across markets. According to the United Nations International Children's Emergency Fund (UNICEF) and World Health Organization (WHO) Progress on Drinking Water, Sanitation and Hygiene in Schools 2015-2023 report, only 39% of schools provide menstrual health education. This figure varies significantly between primary schools (34%) and secondary schools in Central and Southern Asia (84%), indicating that younger girls often lack essential knowledge during the onset of menstruation [1]Source: World Health Organization, "Progress on Drinking Water, Sanitation and Hygiene in Schools 2015-2023 ", who.int. Government programs in developing markets are addressing this gap by implementing educational initiatives that improve school attendance and reduce urogenital infections through better hygiene practices. The inclusion of menstrual health in national education curricula has increased the demand for safe hygiene products over traditional alternatives like cloth rags, particularly in regions where cultural taboos have limited open discussion. Moreover, digital health platforms are expanding the reach of menstrual health education to remote and underserved communities through culturally appropriate content. This has created a network effect where educated individuals become advocates within their communities, leading to changes in consumer behavior and increased adoption of modern hygiene products. Major manufacturers such as Procter & Gamble's Always and Kenvu's Stayfree are supporting these educational initiatives through school-based campaigns and awareness programs. These efforts simultaneously advance menstrual health education and strengthen their market presence in developing regions. The combination of education, policy implementation, and corporate initiatives is transforming menstrual health awareness and contributing to market growth.

Increasing governmental and NGO initiatives promoting feminine hygiene awareness in developing regions

The feminine hygiene products market is experiencing transformation through government and NGO initiatives that position menstrual health as a public health and gender equity priority. Policy measures, such as free menstrual product programs implemented across 27 U.S. states and Washington, D.C., in January 2025, according to the Alliance for Period Supplies, have created significant institutional procurement channels that ensure consistent product demand [2]Source: Alliance for Period Supplies, "Period Products in Schools", allianceforperiodsupplies.org. International development organizations integrate menstrual hygiene management into health and education programs, creating sustainable funding streams for product distribution in underserved areas. These programs often support locally manufactured products, strengthening regional suppliers and improving supply chain stability. The recognition of menstrual equity as a human rights issue has led to legislation affecting healthcare, workplace policies, and public facility requirements. This market expansion reflects broader social efforts to normalize menstruation, address cultural stigmas, and improve access to feminine hygiene products. Companies like Kotex participating in these initiatives gain enhanced institutional and public market access. These government and NGO programs create market opportunities, strengthen menstrual health's position in public policy, and support market growth through improved product accessibility, education, and empowerment.

Influence of social media diversifying product discovery

The widespread adoption of digital and social media platforms enables direct-to-consumer brands to compete with established companies through targeted content and community engagement. Social media campaigns help normalize discussions about menstruation, increasing consumer awareness and introducing alternative products like menstrual cups and period underwear. These platforms provide the educational support needed for product adoption. Product reviews and testimonials on TikTok and Instagram allow brands to validate new products quickly without substantial traditional advertising investments. Influencer collaborations effectively reach younger consumers who prioritize authentic experiences and peer recommendations. This broader access to product information has increased the adoption of specialized and premium products previously available only through limited retail channels. Companies like Sirona Hygiene have implemented social media campaigns such as #PeriodsHiTohHai to address stigma and misconceptions. These campaigns encourage consumers to share experiences and product images, increasing both engagement and sales. Social media's interactive approach is influencing consumer purchasing decisions by building trust, providing education, and supporting menstrual awareness, contributing to market expansion and growth.

Growing demand for sustainable and biodegradable products due to environmental concerns and shifting consumer preferences

Rising environmental consciousness is driving product innovation toward sustainable and biodegradable solutions, as consumers pay increasing attention to the lifecycle impact of disposable menstrual products that can persist in landfills for centuries. The market has responded with innovations such as compostable sanitary pads manufactured from bamboo fiber and organic cotton, maintaining performance while reducing environmental impact. Research developments have introduced hydrogel-based products that offer high absorption capabilities and decompose naturally in composting conditions. In institutional markets, environmental impact assessments now influence procurement decisions, reflecting broader corporate sustainability initiatives. While sustainable options often command higher prices, consumers demonstrate willingness to invest in them, particularly in reusable products like menstrual cups and period underwear that offer long-term cost benefits. The Apple Women's Health Study in 2023 reported that 19% of U.S. participants used internal menstrual cups, and another 19% used period underwear, indicating growing adoption of eco-friendly alternatives alongside conventional products [3]Source: Harvard T.H. Chan School of Public Health, "Apple Women’s Health Study", hsph.harvard.edu. Moreover, companies like Saathi have introduced banana fiber-based biodegradable pads, combining environmental sustainability with agricultural development. The increasing preference for sustainable products continues to create market opportunities worldwide, supported by environmental consciousness, product innovation, and changing consumer behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulation and scrutiny over personal care ingredients and claims | -0.3% | North America and European Union, expanding globally | Short term (≤ 2 years) |

| Environmental concerns regarding non-biodegradable wipes contributing to pollution and landfill issues | -0.2% | Global, with stronger regulatory response in European Union | Medium term (2-4 years) |

| Cultural taboos and stigma surrounding menstruation | -0.4% | Asia-Pacific, Middle East and Africa, and South America rural markets | Long term (≥ 4 years) |

| Upward pricing pressure and product affordability | -0.5% | Global, with stronger impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing regulation and scrutiny over personal care ingredients and claims

Increasing regulatory oversight and scrutiny regarding personal care ingredients and product claims significantly impacts manufacturers and product developers, with smaller companies facing heightened compliance burdens. The Food and Drug Administration (FDA) 2024 investigation into metal contamination in tampons, following a study that identified lead and arsenic in products across the U.S. and Europe, indicates potential future restrictions that may require product reformulation and supply chain modifications. The intensified regulatory framework has increased development costs and product launch timelines, benefiting companies with established compliance systems. While the FDA's classification of tampons as medical devices currently limits ingredient disclosure requirements, congressional and advocacy pressure is mounting for enhanced transparency and safety protocols. These regulatory changes influence product development strategies, particularly for established brands like Tampax, which must maintain consumer trust while adhering to evolving safety standards. Companies with comprehensive safety testing, supply chain monitoring, and quality control systems are better positioned to address these regulatory challenges, enhancing their market position. The increased regulatory oversight, while challenging, contributes to improved product safety and consumer confidence in the industry.

Environmental concerns regarding non-biodegradable wipes contributing to pollution and landfill issues

The increasing environmental impact of non-biodegradable wipes and applicators has raised concerns due to their contribution to plastic pollution and waste management challenges. The European Union's Deforestation Regulation (EUDR) implementation, aimed at ensuring timber traceability and reducing deforestation, is transforming supply chains for wood-based materials like fluff pulp. This regulation impacts major producers such as Procter & Gamble and Kimberly-Clark by affecting the supply of essential raw materials. The regulatory environment and increased consumer awareness of environmental impacts from disposable products are driving demand for biodegradable alternatives. However, these alternatives face challenges, including higher production costs and performance variations. The industry is experiencing supply chain pressures, as evidenced by the closure of International Paper's Georgetown facility, which represents approximately 5% of U.S. pulp production. In response, manufacturers are developing new materials and superabsorbent polymers to enhance product efficiency while meeting regulatory requirements. These developments require significant investment in research and development, along with consumer education initiatives. Companies like Saathi are addressing market demands by producing biodegradable pads using local raw materials, demonstrating the viable integration of environmental sustainability with market requirements. The market continues to evolve as regulatory requirements and environmental considerations influence consumer purchasing decisions, necessitating sustainable product development across the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cups Drive Premium Innovation

The competitive landscape is transforming, with reusable alternatives gaining traction due to their superior long-term value propositions. Menstrual cups, for instance, are projected to grow at a 7.07% CAGR despite holding a smaller market share. In 2025, sanitary pads are expected to maintain a dominant 46.12% market share, supported by entrenched consumer habits and continuous advancements in materials and absorbency technologies. Innovations such as AI-powered smart sanitary pads are redefining traditional products by integrating health monitoring capabilities, offering added value beyond basic functionality. Conversely, tampons are experiencing declining popularity in certain regions. In the UK, sales have dropped as consumers shift toward menstrual cups and period underwear, driven by health and environmental concerns.

Emerging categories are bridging the gap between disposable and reusable options. Period panties and panty liners provide convenience while reducing environmental impact compared to traditional products. Growing awareness of pH balance and intimate health is driving demand for feminine wipes and intimate washes, although these products face increasing regulatory scrutiny over ingredient safety. Market diversification is evident in the "others" category, which includes intimate moisturizers and cleaning products, as brands expand their portfolios to encompass comprehensive intimate care solutions. The FDA's approval of innovative applications, such as Qvin's menstrual blood testing for health monitoring, highlights the convergence of feminine hygiene and digital health technologies. This development signals the creation of new product categories that extend beyond traditional absorption-focused solutions.

By Product Category: Reusable Gains Despite Disposable Dominance

In 2025, consumer preferences for convenience are reflected in the 78.12% market share held by disposable products. However, reusable alternatives are gaining traction, achieving a robust 7.41% CAGR growth. This growth is driven by increasing sustainability concerns and the appeal of long-term cost savings. Technological advancements in materials science, such as antimicrobial fabrics and improved absorption capabilities, have addressed historical performance issues in the reusable segment. Additionally, consumer education initiatives are critical, as proper care and maintenance directly influence product longevity and user satisfaction. Inflationary pressures further strengthen the economic case for reusable products, as rising tampon prices make the higher upfront costs of cups and period underwear more attractive.

Manufacturers of disposable products are responding to sustainability demands by incorporating biodegradable materials and reducing packaging, aiming to balance environmental concerns with market retention. Institutions, particularly schools and public facilities adhering to menstrual equity mandates, favor disposable products due to hygiene protocols and maintenance requirements. Subscription models are emerging as a hybrid solution, combining the convenience of disposables with reduced packaging waste and predictable costs. Competitive dynamics are intensifying as reusable brands expand into retail channels traditionally dominated by disposables, prompting established manufacturers to develop dual-category strategies to remain competitive.

By Nature: Organic Momentum Challenges Conventional Leadership

Natural and organic products are experiencing robust growth, with a 7.6% CAGR, driven by increasing consumer demand for ingredient transparency and concerns over synthetic materials in intimate products. In 2025, conventional products retain a commanding 81.95% market share, supported by established supply chains, cost efficiencies, and proven performance attributes that meet the needs of mainstream consumers. Regulatory changes mandating enhanced ingredient disclosures are driving growth in the organic segment, enabling consumers to make more informed purchasing decisions. As production scales improve, the premium pricing of organic alternatives is becoming less of a barrier, with health considerations increasingly outweighing cost concerns for consumers.

Regulatory frameworks are significantly influencing this market. For example, MoCRA's requirements for ingredient transparency and safety substantiation are creating competitive advantages for brands that have prioritized clean formulations. Manufacturers are leveraging vertical integration opportunities by developing organic cotton supply chains specifically for feminine hygiene applications, enabling better control over quality and costs. Conventional manufacturers are adopting hybrid strategies, introducing organic product lines within their existing portfolios to capture premium segment growth while maintaining their mass-market presence. However, the evolving certification landscape, with multiple organic and natural standards, presents both opportunities and challenges in effectively communicating value propositions to consumers.

By Distribution Channel: Digital Transformation Accelerates

Online retail stores exhibit substantial growth potential, with a projected 6.79% CAGR. This growth is driven by increasing consumer confidence in purchasing intimate products online and the operational efficiency of subscription-based delivery models. In 2025, pharmacy and drug stores are expected to retain a leading 38.35% market share, capitalizing on their established healthcare credibility and the ability to meet urgent consumer demands. The integration of quick commerce platforms with traditional retailers is reshaping channel dynamics. For example, DoorDash's partnerships with brands like Lola and Hims & Hers enable the rapid delivery of feminine hygiene products. Supermarkets and hypermarkets are under competitive pressure from specialized online retailers that offer an extensive product range and value-added educational content.

E-commerce platforms are instrumental in driving consumer adoption of alternative products, such as menstrual cups and organic options, which often require detailed product information and educational support. The direct-to-consumer model allows brands to strengthen customer relationships through subscription services and personalized recommendations informed by usage data. Furthermore, menstrual equity initiatives are expanding distribution opportunities, with convenience stores and workplace dispensers exploring placements in non-traditional locations. Channel strategies are increasingly adopting an omnichannel approach, where online platforms facilitate product discovery and education, while physical retail outlets provide immediate product access and trial opportunities.

Geography Analysis

North America holds the largest market share at approximately 36.60% as of 2025, supported by a well-established healthcare infrastructure and progressive menstrual equity policies that drive institutional demand, such as free product distribution programs in schools. The region’s market maturity is reflected in consumer preferences for premium and sustainable products, bolstered by the strong presence of leading brands like Kotex and Tampax. The differing growth rates between Asia-Pacific and North America underscore the varying market dynamics, with North America focusing on innovation and sustainability, while Asia-Pacific prioritizes expanding access to basic products and enhancing affordability.

In comparison, Asia-Pacific is positioned as the fastest-growing region in the global feminine hygiene market, with a projected CAGR of approximately 6.54% through 2031. This growth is driven by improving economic conditions, government initiatives to enhance menstrual hygiene access, and efforts to foster cultural acceptance, particularly in high-population markets like India and China. Increased investments in awareness campaigns and menstrual hygiene education are accelerating product adoption, while urbanization and rising disposable incomes are enabling consumers to access a broader range of premium and innovative offerings. Regional players such as Prakati, Saathi, Eco Femme, and Anandi are capitalizing on this trend by introducing biodegradable and reusable feminine hygiene products, catering to the growing demand for environmentally friendly and health-conscious solutions.

Europe demonstrates steady market growth, driven by stringent environmental regulations favoring sustainable feminine hygiene products and robust healthcare systems that recognize menstrual health as a public health priority. South America shows potential for accelerated growth, supported by regional consolidation and the expansion of private labels, such as those in Colombia, which are optimizing distribution networks and improving cost efficiency. In the Middle East and Africa, increasing governmental and NGO-led initiatives are advancing menstrual hygiene education; however, cultural barriers and economic constraints continue to limit market penetration. Additionally, diverse regional regulatory frameworks, including tax exemptions in some markets and restrictions in others, significantly impact accessibility and affordability, shaping the global feminine hygiene market landscape.

Competitive Landscape

The feminine hygiene market is moderately fragmented, with prominent multinational corporations such as Procter & Gamble, Kimberly-Clark, and Unicharm maintaining a dominant position. These companies utilize extensive distribution networks and strong brand equity to sustain their market leadership. However, these established players are facing increasing competition from agile, specialized direct-to-consumer brands and sustainability-focused entrants. For example, Rael, a direct-to-consumer brand, achieved the #1 bestseller position on Amazon for organic cotton pads. Similarly, in February 2025, Healthfab, which offered reusable period panties with an inbuilt absorbent layer, secured an INR 2 crore investment from Shark Tank India investors, highlighting the market potential for innovative, natural products that align with health- and eco-conscious consumer preferences.

Strategic consolidation is actively reshaping the competitive landscape. In 2024, Forum Brands acquired Lola, while Compass Diversified entered a partnership with The Honey Pot Company in a transaction valued at USD 380 million. These developments reflect investor confidence in the premium and natural feminine hygiene segments. Companies are focusing on portfolio expansion and capability enhancement to capitalize on the growing demand for premium, sustainable products. Additionally, investments in smart product development, AI-driven health monitoring, and digital health integration are enabling businesses to differentiate themselves, enhance personalization, and strengthen consumer engagement.

Supply chain optimization has become a critical focus area due to volatile raw material costs and stricter regulatory requirements. Companies like Kimberly-Clark are pursuing global research and development collaboration and streamlining value chains to mitigate an anticipated USD 300 million tariff impact in 2025. Regulatory frameworks, such as the FDA’s MoCRA legislation, provide compliance advantages to established players with robust quality systems, creating barriers for smaller competitors that lack the resources for facility registration and safety validation. This dynamic interplay of innovation, consolidation, regulatory pressures, and evolving consumer preferences continues to drive transformation and growth in the global feminine hygiene market.

Feminine Hygiene Industry Leaders

-

Kimberly-Clark Corporation

-

Procter & Gamble Company

-

Unicharm Corporation

-

Essity AB

-

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stayfree, a prominent women's menstrual hygiene brand in India, implemented a product portfolio expansion through the introduction of Stayfree Tampons by o.b. The product line integrated o.b.'s global expertise in tampon manufacturing with Stayfree's established market presence. The tampons were launched in two variants: Regular Flow, offered in packs of 10 and 20 units, and Super Flow, available in packs of 10 units.

- March 2025: Procter & Gamble introduced Always Pocket Flexfoam, a full-sized pad featuring Flexfoam technology that prevented leaks and bunching while maintaining comfort. The product came in a compact, resealable package designed for portability. The Always Pocket Flexfoam pad incorporated the company's Flexfoam technology to provide leak protection while being convenient to carry.

- January 2025: Lola, a female wellness brand, expanded its product portfolio with a postpartum care product line through its website and Walmart retail locations. The initial collection included stretch mark prevention cream, organic cotton postpartum pads, and perineal gel pads for both hot and cold therapy.

- January 2024: Danish femcare start-up Mewalii, founded by Simone Westergaard and Frederikke Dahl, introduced period pads made from Sero regenerative hemp fibers, eliminating the use of cotton.

Global Feminine Hygiene Market Report Scope

Feminine hygiene products are personal care products used during menstruation, vaginal discharge, and other bodily functions related to the vulva and vagina. The feminine hygiene market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into sanitary napkins/pads, tampons, menstrual cups, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, drug stores/pharmacies, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been provided on the basis of value (in USD).

By Product Type

| Sanitary Pads/Napkins |

| Tampons |

| Menstrual Cups |

| Period Panties |

| Panty Liners and Shields |

| Feminine Wipes and Intimate Washes |

| Others (Intimate moisturizers, Cleaning and deodorizing products) |

By Product Category

| Disposable Products |

| Reusable Products |

By Nature

| Conventional |

| Natural/Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Sanitary Pads/Napkins | |

| Tampons | ||

| Menstrual Cups | ||

| Period Panties | ||

| Panty Liners and Shields | ||

| Feminine Wipes and Intimate Washes | ||

| Others (Intimate moisturizers, Cleaning and deodorizing products) | ||

| By Product Category | Disposable Products | |

| Reusable Products | ||

| By Nature | Conventional | |

| Natural/Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the feminine hygiene market in 2026?

It reached USD 34.48 billion in 2026 and is forecast to climb to USD 43.74 billion by 2031.

Which region grows fastest through 2031?

Asia-Pacific leads with a projected 6.54% CAGR owing to rising income and public-sector access programs.

What product segment shows the highest growth?

Menstrual cups outpace others with a 7.07% CAGR as consumers embrace reusable options.

How are online sales channels performing?

Online retailers post the highest channel CAGR at 6.79%, driven by subscription convenience and discreet delivery.

Page last updated on: