Menstrual Cup Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

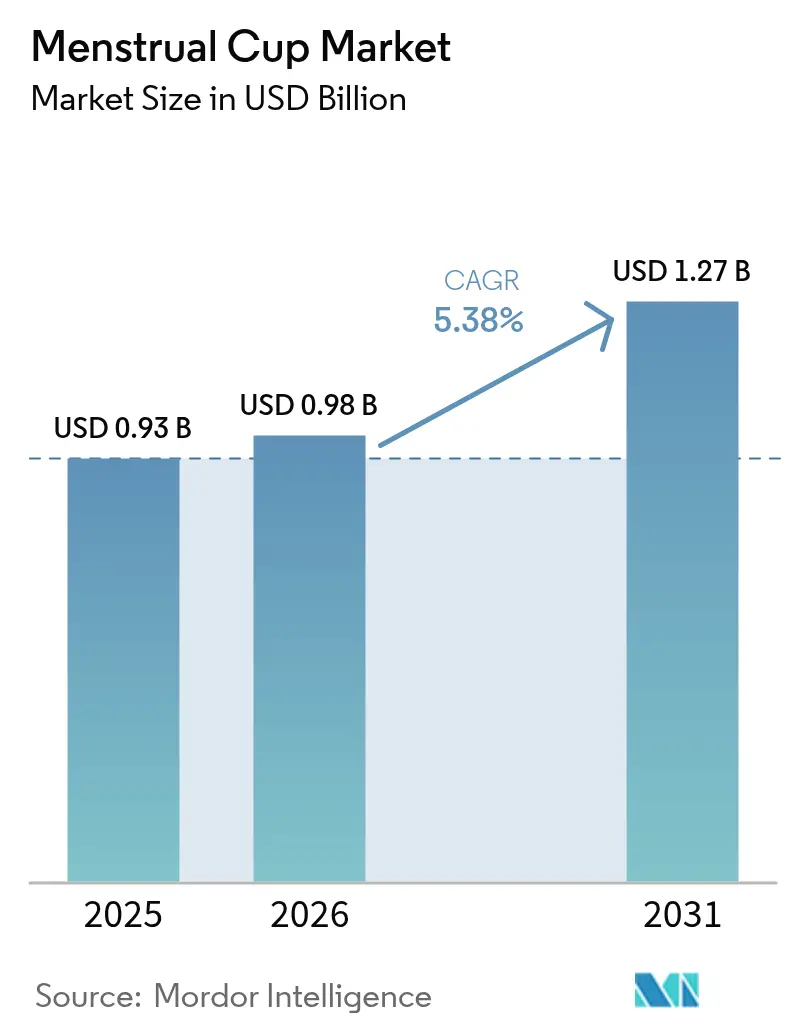

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Menstrual Cup Market Analysis by Mordor Intelligence

The menstrual cup market size is expected to grow from USD 0.93 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.27 billion by 2031 at 5.38% CAGR over 2026-2031.

Robust momentum comes from a sweeping consumer shift toward reusability, cost savings, and reduced waste. Across regions, sustainability credentials outweigh convenience, supported by data showing a 90% carbon-footprint drop versus tampons. Governments further boost demand through period-poverty schemes, while e-commerce removes access hurdles and supplies detailed educational content. Intensifying material innovation, especially thermoplastic elastomer (TPE), widens product choice, and North America’s early adoption underpins steady baseline demand even as Asia-Pacific leads incremental growth. Collectively, these factors position the menstrual cups market for durable expansion through the decade.

Key Report Takeaways

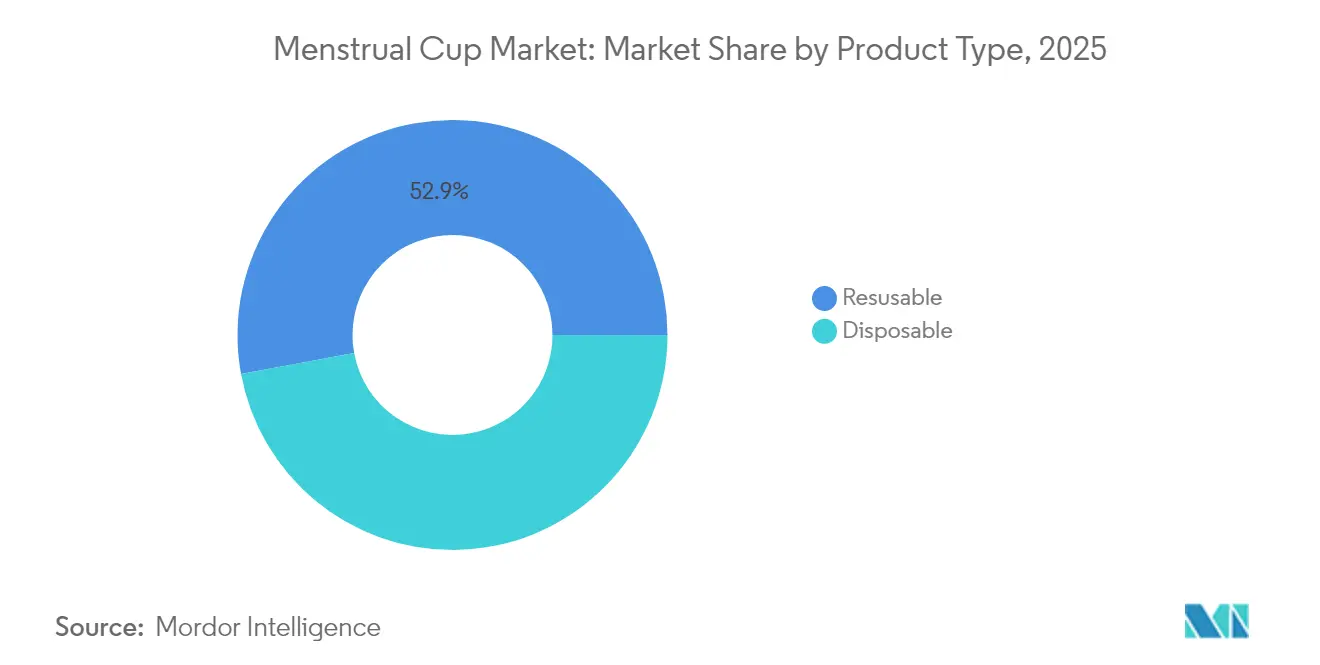

- By product type, reusable variants held 52.90% of menstrual cups market share in 2025, whereas disposable cups posted the quickest 6.83% CAGR to 2031.

- By material, medical-grade silicone led with 70.10% revenue share in 2025; TPE is forecast to expand at a 7.21% CAGR through 2031.

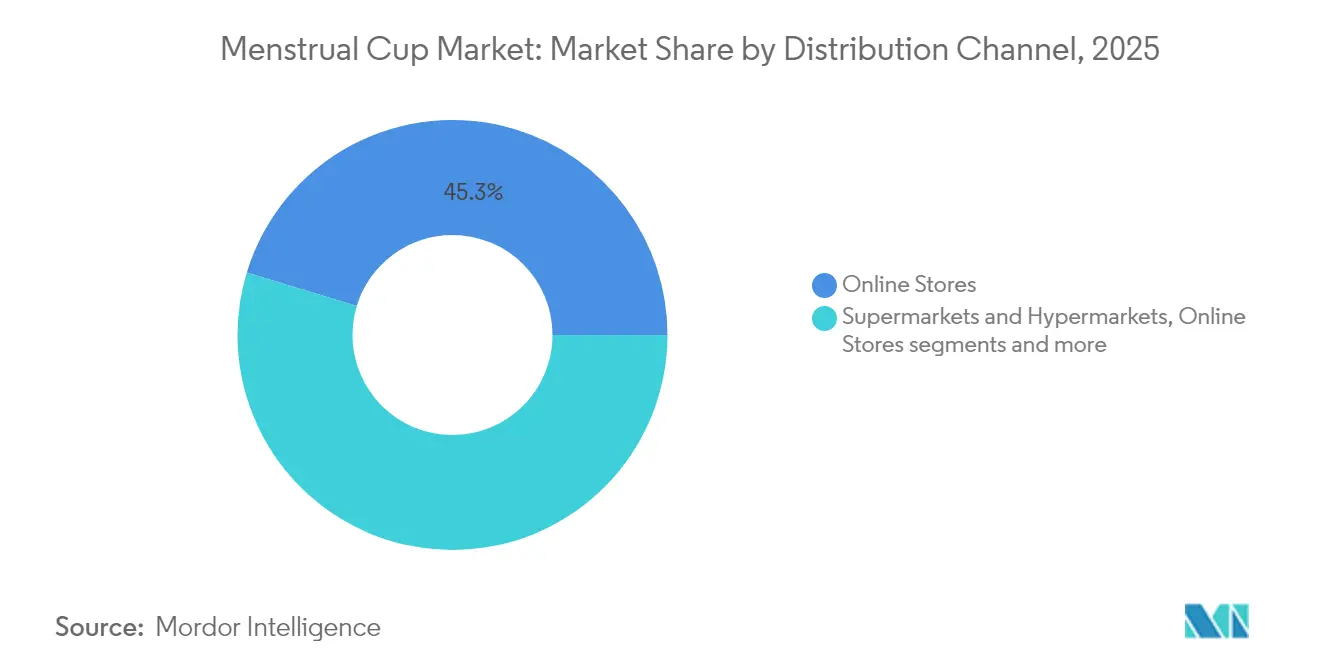

- By distribution channel, online stores accounted for 45.30% of the menstrual cups market size in 2025 and are advancing at an 8.05% CAGR.

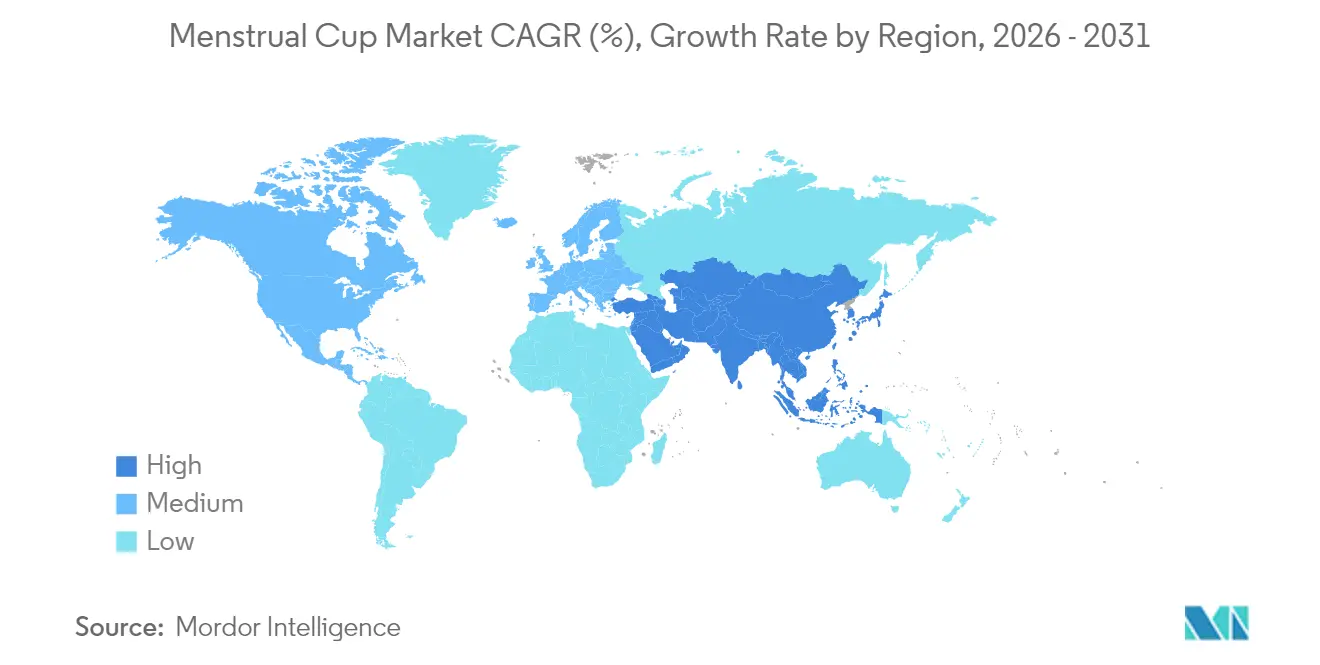

- By geography, North America commanded 38.40% share in 2025, while Asia-Pacific is projected to grow at a 8.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Menstrual Cup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in sustainability-driven consumer behaviour | +1.2% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Long-term cost advantage versus disposables | +0.9% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Expanding e-commerce & DTC fulfilment models | +0.8% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Government "period-poverty" schemes distributing free cups | +0.6% | EU, North America, select APAC markets | Medium term (2-4 years) |

| Medical-grade TPE enabling hypoallergenic, ultra-thin cups | +0.4% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Social-media influencer advocacy among Gen-Z | +0.3% | Global, strongest in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Sustainability-Driven Consumer Behaviour

Multiple life-cycle studies in France, India, and the United States confirm that one cup offsets its embodied emissions within a month of use, amplifying environmental value across a 10-year lifespan. Each unit removes roughly 2,500 tampons from landfill streams. Gen-Z and millennial cohorts actively reward brands with visible climate commitments, reshaping category messaging across the menstrual cups market. Waste-reduction statistics, such as Scotland’s annual disposal of 427.5 million single-use period items, sharpen consumer resolve[1]Source: Zero Waste Scotland, “Trial Period,” zerowastescotland.org.uk . The alignment of ecological values and personal health preference sustains demand and encourages repeat purchases.

Long-Term Cost Advantage Versus Disposables

One cup can replace close to 3,250 tampons over 10 years, offering compelling household savings that outweigh higher entry price. Cost messaging resonates in price-sensitive economies and is amplified when linked to accessibility initiatives, as shown in Japan, Indonesia, and France where cost information proved a stronger influence than health claims. Subsidy programs cut first-purchase barriers; for instance, Peterborough City Council sells Mooncups at GBP 5 (USD 6.25) compared with the regular GBP 20 (USD 25), driving trial rates. This financial edge becomes more pronounced as inflation lifts the ongoing price of disposables, reinforcing the menstrual cups market growth narrative.

Expanding E-Commerce & DTC Fulfilment Models

Online channels provide privacy and detailed tutorials that demystify sizing, insertion, and care routines, explaining why they now hold 44.90% channel share with an 8.26% CAGR. Direct-to-consumer storefronts foster community and offer subscription accessories such as sterilizers, which increase lifetime value. Forum Brands’ purchase of Lola validates investor appetite for digital-native period-care assets. For small entrants, e-commerce lowers geographic entry costs and accelerates brand visibility, expanding the menstrual cups market both horizontally and vertically.

Government “Period-Poverty” Schemes Distributing Free Cups

Public programs normalize cup use and reach demographics otherwise unable or unwilling to pay. Catalonia’s pharmacy initiative distributes reusable products to 2.5 million people, illustrating rapid scale potential. Wales earmarked GBP 3.25 million to supply 90-100% eco-friendly period products by 2027, embedding reusables in public discourse. Canada’s CAD 29.8 million Menstrual Equity Fund extends the model across 400 sites [2]Source: Government of Canada, “Menstrual Equity Fund Pilot,” canada.ca . The resulting product trials generate peer advocacy, further enlarging the menstrual cups market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural stigma & low awareness in emerging economies | -1.1% | APAC emerging markets, MEA, parts of South America | Long term (≥ 4 years) |

| Steep learning curve for first-time users | -0.7% | Global, particularly first-time user segments | Medium term (2-4 years) |

| Lack of product standards → counterfeit/low-quality cups | -0.5% | Emerging markets, online marketplaces | Medium term (2-4 years) |

| Water-scarcity challenges for cleaning & sterilising cups | -0.3% | Sub-Saharan Africa, parts of APAC, arid regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cultural Stigma & Low Awareness in Emerging Economies

Taboos surrounding menstruation hinder open discussion and product experimentation. A Nepalese study found worries about virginity loss to be a major barrier among schoolgirls NCBI. In South Korea, only 1.6% of women aged 18-45 have adopted cups despite rising health concerns with disposables OPHRP. Effective outreach therefore hinges on culturally sensitive education delivered by trusted community figures. Without this groundwork, the menstrual cups market penetration stalls and counterfeit products proliferate, undermining user confidence.

Steep Learning Curve for First-Time Users

Insertion challenges, leakage, and discomfort cause early abandonment: an Australian survey reported a 54% leakage rate on first use with 25% experiencing pain. Success improves after several cycles, yet many new users quit before reaching that milestone. Brands now bundle sizing quizzes, animated tutorials, and customer support to shorten the adjustment period. Technological advances such as Sunny’s FDA-cleared applicator cup signal further relief. Overcoming this hurdle is pivotal for sustained growth of the menstrual cups market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reusable Dominance Drives Innovation

Reusable models owned 52.90% of menstrual cups market share in 2025 while advancing at a 6.41% CAGR. Lower lifetime cost and strong eco-benefits position them as the default choice in most regions. Single-use cups satisfy niche travel and low-water contexts but conflict with the core sustainability narrative powering overall demand. Material research amplifies reusable value: Virginia Tech scientists demonstrated alginate-glycerol gels that solidify menstrual fluid, which could reduce leakage without undermining reusability Gizmodo. Should such features commercialize, reusable leadership will widen as form factors become easier to manage during heavy flow.

Market education highlights cleaning simplicity with compact sterilizers, and community testimonials reassure first-time users. Government agencies increasingly prefer reusable products for public procurement, cementing their primacy in the menstrual cups market. Yet manufacturers still monitor single-use formats for humanitarian aid or disaster scenarios where sterilization remains difficult. Balanced portfolios allow firms to hedge against regional water scarcity, keeping the menstrual cups industry resilient across diverse operating environments.

By Material: Silicone Leadership Faces TPE Innovation

Medical-grade silicone accounted for 70.10% of 2025 revenue, buoyed by decades of clinical acceptance and durable supply chains. The segment embeds the menstrual cups market size for premium users who trust its biocompatibility and 10-year life. However, TPE’s 7.21% CAGR illustrates appetite for softer, hypoallergenic options. KRAIBURG TPE’s THERMOLAST M extends usable life to 12 years and resolves heavy-metal concerns, providing new competitive ground KRAIBURG TPE.

Silicone will remain dominant because of extensive regulatory clearances, but firms gradually introduce blended portfolios that accommodate consumers sensitive to stiffness or latex cross-allergy. Ongoing R&D seeks to equal silicone’s resilience while boosting comfort, an approach that diversifies revenue without destabilizing existing production. Strategic sourcing from FDA-compliant suppliers preserves brand integrity as counterfeit risk rises in the menstrual cups market.

By Distribution Channel: Digital Transformation Accelerates

Online outlets generated 45.30% of the menstrual cups market size in 2025 and are growing at 8.05% CAGR as shoppers favor the discretion, product depth, and peer reviews offered by e-commerce. Digital storefronts optimize search visibility and funnel traffic to brand-hosted tutorial libraries, which lower the steep learning curve. DIVA International’s impact program leverages these channels to distribute 75,000 cups alongside social-impact storytelling

Pharmacies still con fer professional credibility, and supermarkets sustain impulse purchases, but both face lower growth trajectories. Specialty feminine-care shops curate high-end assortments and in-person fitting advice, cushioning their premium pricing. Direct-to-consumer models foster subscriptions for cleaning tablets or lubricant gels, unlocking repeat revenue and high-margin kits. The shift tilts bargaining power toward brands that master digital literacy and retention metrics, a defining feature of the evolving menstrual cups market.

Geography Analysis

North America retained 38.40% revenue share in 2025 due to high awareness, favorable regulation, and mature e-commerce logistics. Canada’s CAD 29.8 million Menstrual Equity Fund raises adoption further by normalizing cups across public settings Government of Canada. Penetration is already high among younger cohorts, so future growth hinges on technological upgrades and value-added accessories rather than first-time conversions.

Asia-Pacific is the growth engine, demonstrating a 8.85% CAGR to 2031. Rising disposable incomes, improved menstrual-health literacy, and wide-scale public projects such as India’s Thinkal distribution of 1 million units underscore latent demand. South Korea’s low 1.6% usage rate indicates vast runway once social barriers are addressed. Companies tailor marketing to local norms and partner with NGOs for village-level workshops, steadily enlarging the menstrual cups market. Europe sustains growth via strict waste mandates and publicly funded product schemes. Catalonia’s pharmacy rollout to 2.5 million residents exemplifies swift mainstreaming. Wales’ target of 90-100% eco-friendly period products reinforces regional leadership. Meanwhile, South America and the Middle East & Africa hold untapped potential, but addressable demand is constrained by cultural stigma and water infrastructure limitations. Producers invest in localized translations, lower-price SKUs, and community demonstrations to lay groundwork for future menstrual cups market expansion.

Competitive Landscape

The menstrual cups market is moderately fragmented, with established leaders—DIVA, Mooncup, Lunette—holding brand equity built over nearly two decades. These incumbents emphasize certifications such as B Corp status and FDA 510(k) clearances to reassure safety-conscious consumers. Mid-sized challengers differentiate through material science: Sunny secured FDA clearance for an applicator-equipped design that mimics tampon familiarity.

R&D alliances with universities accelerate next-generation prototypes, including Virginia Tech’s blood-solidifying biomaterial that promises leak mitigation without disposables. Strategic acquisitions, such as Forum Brands buying Lola, signal growing interest from consumer-product aggregators. At the same time, Lune Group’s bankruptcy in 2024 highlights scale pressures for niche players whose unit economics cannot absorb rising digital advertising costs.

Leading firms double down on impact marketing, distributing free cups in under-served communities, which both advances social mission and seeds future demand. Material suppliers like KRAIBURG TPE position themselves as enablers of product diversification, partnering with manufacturers to prototype softer, hypoallergenic lines. Overall, competitive intensity centers on comfort innovations, influencer credibility, and omnichannel reach, shaping the forward trajectory of the menstrual cups market.

Menstrual Cup Industry Leaders

Diva International Inc.

Mooncup Ltd

Me Luna GmbH

Lena Cup LLC

The Flex Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Wales allocated GBP 3.25 million for free period products across schools and communities, aiming for 90-100% eco-friendly options by 2027.

- December 2024: Bettii Pod raised GBP 400,000 to advance public-toilet washing solutions for menstrual cups

- July 2024: Saalt reported tripled sales following tampon safety studies, illustrating demand spikes tied to health news

Global Menstrual Cup Market Report Scope

As per the scope of the report, a menstrual cup is a small, flexible, funnel-shaped feminine hygiene product made of rubber, silicone, or elastomer. Its objective is to collect menstrual fluid during menstruation.

The menstrual cup market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into disposable and reusable. By distribution channel, the market is segmented into online stores and offline stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in value (USD) for the above segments.

| Reusable Menstrual Cups |

| Disposable/Single-use Menstrual Cups |

| Medical-grade Silicone |

| Natural Rubber (Latex) |

| Thermoplastic Elastomer (TPE) |

| Pharmacies & Retail Stores |

| Supermarkets & Hypermarkets |

| Online Stores (Company DTC, Marketplaces) |

| Specialty Feminine-Care Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Reusable Menstrual Cups | |

| Disposable/Single-use Menstrual Cups | ||

| By Material | Medical-grade Silicone | |

| Natural Rubber (Latex) | ||

| Thermoplastic Elastomer (TPE) | ||

| By Distribution Channel | Pharmacies & Retail Stores | |

| Supermarkets & Hypermarkets | ||

| Online Stores (Company DTC, Marketplaces) | ||

| Specialty Feminine-Care Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the menstrual cups market?

The market was valued at USD 0.98 billion in 2026 and is projected to reach USD 1.27 billion by 2031.

Which product type dominates sales?

Reusable cups captured 52.90% of global revenue in 2025.

Why are online channels growing so quickly?

They combine privacy, detailed education, and direct-to-consumer support, lifting online share to 45.30% in 2025 with an 8.05% CAGR outlook.

What regions show the strongest future growth?

Asia-Pacific leads with a forecast 8.85% CAGR thanks to rising income and government hygiene campaigns.

Page last updated on: