Toiletries Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

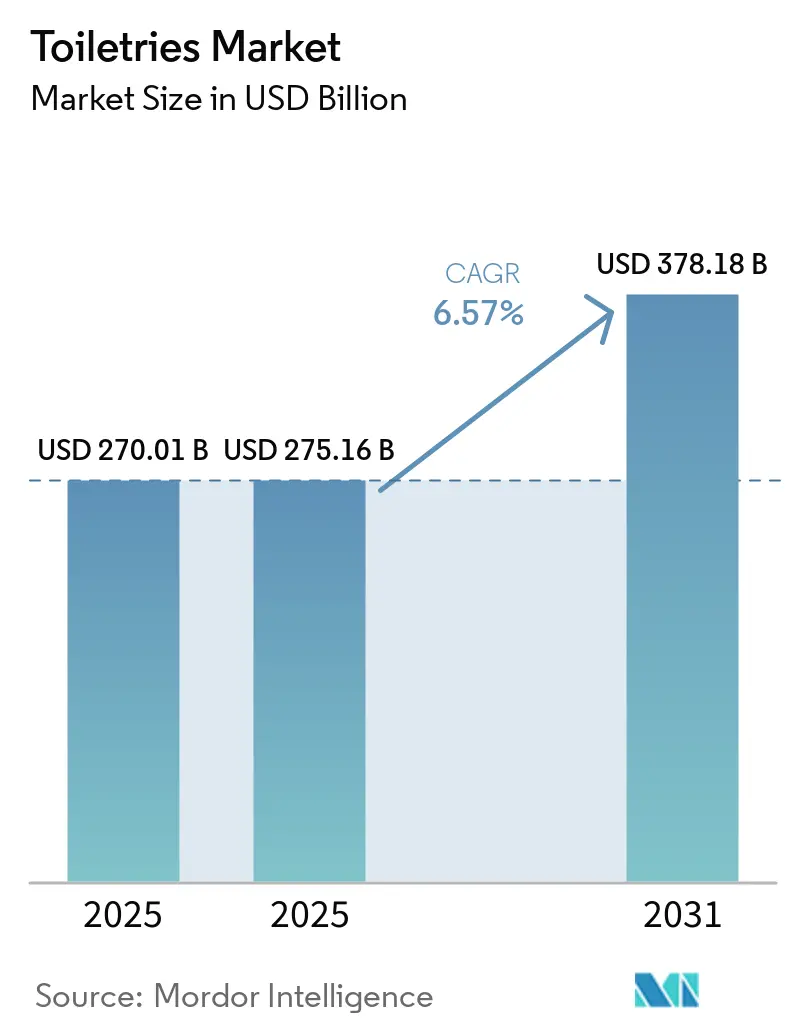

| Market Size (2025) | USD 275.16 Billion |

| Market Size (2031) | USD 378.18 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

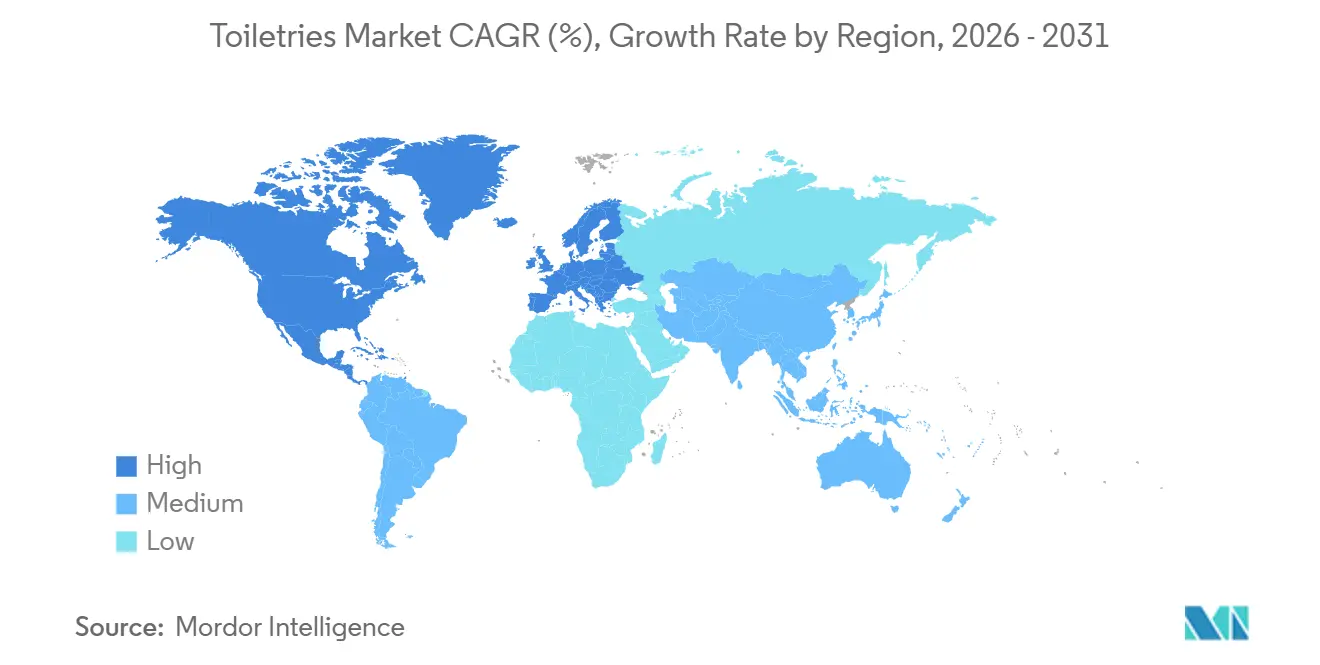

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Toiletries Market Analysis by Mordor Intelligence

The global toiletries market size is expected to grow from USD 270.01 billion in 2025 and USD 275.16 billion in 2026 to USD 378.18 billion by 2031, registering a CAGR of 6.57% between 2026 and 2031. Key growth drivers include ingredient-transparency mandates, stricter regulations on carcinogenic, mutagenic, and reprotoxic (CMR) substances, and the rise of algorithm-driven personalization platforms. These factors have replaced the pandemic-driven hygiene surge that characterized the 2020-2022 period. The retail landscape is increasingly shifting online, with direct-to-consumer (D2C) brands bypassing traditional shelf fees and leveraging first-party data to enable rapid product reformulations. Meanwhile, established multinational companies face higher compliance costs as they adapt products like soaps, shampoos, and deodorants to meet evolving regional regulations. Additionally, the adoption of refillable hardware, such as reusable pods and aluminum deodorant cases, is transforming sustainability from a marketing focus to a design requirement, driving up average selling prices in several premium micro-segments. The Asia-Pacific region leads in both scale and growth momentum, driven by Gen Z consumers in India and Indonesia who prioritize TikTok-endorsed, Halal-certified products as necessities rather than luxury items.

Key Report Takeaways

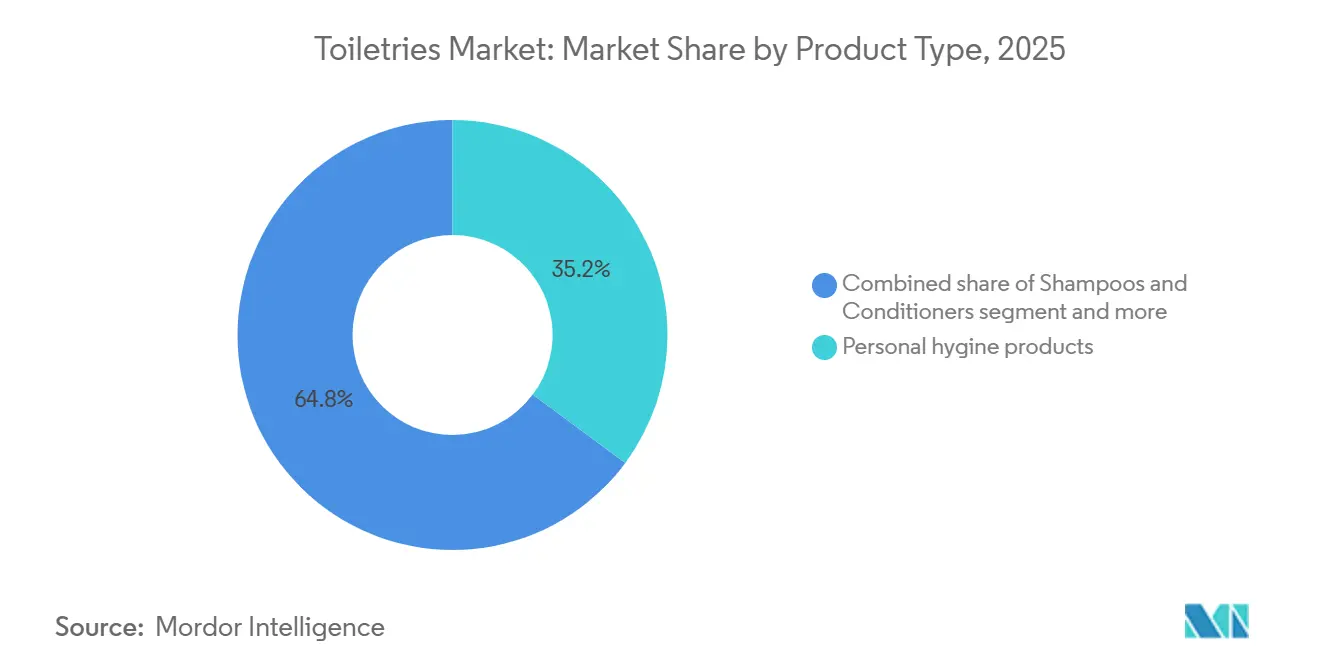

- By product type, personal hygiene items led with 35.1% revenue share in 2025, while shampoos and conditioners are advancing at a 6.88% CAGR through 2031.

- By category, mass offerings held 69.29% of the toiletries market share in 2025, yet the premium tier is growing faster at 7.45% CAGR to 2031.

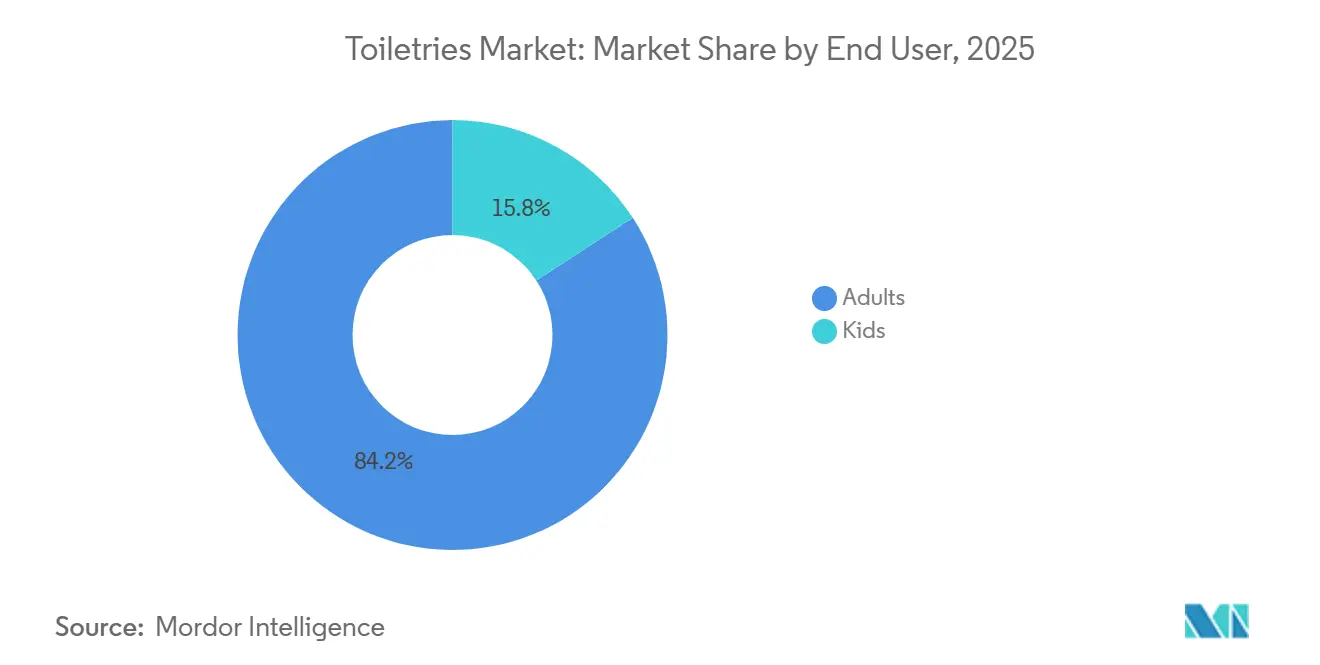

- By end user, adults accounted for 84.19% of sales in 2025, whereas products for kids are projected to expand at a 7.08% CAGR in the same horizon.

- By distribution channel, health and beauty specialists captured 38.20% of 2025 turnover; online retail, however, is scaling at an 7.89% CAGR on the back of rising digital adoption.

- By geography, Asia-Pacific commanded 37.40% of worldwide revenue in 2025 and is forecast to post the quickest regional CAGR of 6.81% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Toiletries Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing awareness about personal hygiene | +1.2% | Global, with a stronger impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Preference for natural and organic products | +0.9% | North America & Europe leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Innovations and launches in products | +0.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Rising demand for personalized and customized products | +0.7% | North America & Europe core, spill-over to urban Asia-Pacific | Medium term (2-4 years) |

| Recovery in the travel, tourism, and hospitality sectors | +0.6% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Growth in men’s grooming and baby care product adoption | +0.5% | Global, with accelerated growth in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing awareness about personal hygiene

Post-pandemic hygiene awareness has significantly influenced consumer behavior, supported by government health initiatives emphasizing personal cleanliness. The WHO's focus on hand hygiene and the CDC's updated guidelines on protective practices have driven consistent demand for antibacterial soaps, sanitizing wipes, and specialized cleansing products. This heightened awareness also extends to oral care, with the Chinese government's promotion of specialized oral care products contributing to growth in the children's oral care market. The trend is particularly pronounced in emerging markets, where increasing education levels and urbanization are establishing new hygiene standards. Additionally, digital health platforms and telemedicine consultations have enhanced awareness of the link between personal hygiene and overall health outcomes. Public health campaigns supported by governments in countries such as India and Brazil have institutionalized hygiene practices, fostering long-term behavioral changes and sustaining market demand beyond immediate health emergencies.

Preference for natural and organic products

Consumer preference for natural and organic toiletries is driving innovation and premium product development in the global market. Increasing awareness of skin health, sustainability, and ingredient transparency has led consumers to favor products made with plant-based ingredients, botanical extracts, essential oils, and chemical-free formulations. This trend has prompted manufacturers to reformulate products and invest in cleaner, safer, and environmentally responsible alternatives. Regulatory changes are further supporting this shift. For example, the European Union’s Regulation 2023/1545 requires the labeling of 56 fragrance allergens when concentrations exceed specified thresholds, enhancing transparency in personal care and toiletry products[1]Source: European Union, "Commission Regulation (EU) 2023/1545 of 26 July 2023 amending Regulation (EC) No 1223/2009 of the European Parliament and of the Council as regards labelling of fragrance allergens in cosmetic products", eur-lex.europa.eu. Similarly, the United Kingdom’s Regulation 2024/1334 imposes restrictions on fragrance allergens and certain UV filters, requiring full ingredient disclosure [2]Source: Legislation United Kingdom, "The Cosmetic Products (Restriction of Chemical Substances) (No. 2) Regulations 2024", legislation.gov.uk. These regulations have also encouraged brands to adopt certifications such as COSMOS and NATRUE to demonstrate compliance and build consumer trust. Consequently, the demand for certified natural and organic toiletries is growing, particularly among health-conscious and environmentally aware consumers seeking clean-label toiletries products.

Innovations and launches in products

Product innovation is increasingly focused on delivery systems and sensory differentiation rather than introducing novel active ingredients, reflecting the saturation of efficacy claims in mature categories. Shiseido's VOYAGER AI platform, launched in summer 2026, formulates suncare products customized to individual UV exposure patterns and skin phototypes. This platform utilizes machine learning to optimize SPF delivery and texture preferences. The Estée Lauder Companies' partnership with Exuud to develop smart fragrance expression platforms using SoliqaireTM technology highlights the integration of biotechnology with traditional cosmetics, enabling fragrance delivery without the use of heat or aerosols. Similarly, Amorepacific's patent for a manufacturing apparatus that facilitates rapid customization of skincare packs demonstrates how production technology is evolving to support mass customization. Innovation cycles are accelerating as brands adopt artificial intelligence for formulation optimization and consumer insights. Additionally, the integration of IoT sensors in packaging allows for real-time product monitoring and usage analytics, generating data streams that inform future product development and marketing strategies. These advancements share a common focus: addressing unmet needs in convenience, sustainability, and personalization, rather than incremental improvements in efficacy, reflecting a market where differentiation is driven by user experience and environmental impact.

Recovery in the travel, tourism, and hospitality sectors

International travel has surpassed pre-pandemic levels, with U.S. international visitor arrivals projected to reach 72.4 million in 2024, reflecting a 9.1% increase compared to 2023. This growth has directly driven demand for travel-sized toiletries and premium hotel amenities, as reported by the U.S. International Travel Volume. Hospitality chains are enhancing amenity offerings to improve guest experiences, creating opportunities for premium toiletries brands to secure bulk contracts. For example, in March 2024, Hotel Emporium collaborated with Kenneth Cole to supply premium, eco-friendly toiletries to Wyndham Destinations’ 854 Presidential Reserve Suites in locations including the U.S., St. Thomas, and Bali. Duty-free retail channels have also experienced a strong recovery, with travelers showing a greater inclination to purchase premium toiletries products during transit. Additionally, the recovery has accelerated the adoption of sustainable packaging in travel retail, driven by environmental initiatives from airports and airlines that influence product selection and supplier requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product imitations and counterfeiting | -0.8% | Global, particularly severe in Asia-Pacific and online channels | Medium term (2-4 years) |

| Environmental regulations increasing packaging costs | -0.6% | Europe and North America are leading, expanding globally | Long term (≥ 4 years) |

| High cost of premium and natural products | -0.5% | Global, with higher impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Pressure to replace performance-critical ingredients | -0.4% | Global, concentrated in regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product imitations and counterfeiting

Counterfeit toiletries products negatively impact brand equity, compromise consumer safety, and divert revenue from legitimate manufacturers, while enforcement efforts struggle to keep up with the rapid growth of digital distribution channels. In 2024, South Korea's customs authority initiated a permanent crackdown on counterfeit cosmetics, targeting fake K-beauty products sold via social media and cross-border e-commerce platforms. However, the volume of seizures highlights the persistence of counterfeit supply chains. Counterfeiting has become a significant issue in the toiletries sector, with the European Union Intellectual Property Office (EUIPO) reporting annual losses of EUR 3 billion for the cosmetics industry. This figure accounts for 4.8% of legitimate sales and has led to 32,000 job losses across the EU, according to the 2024 EUIPO Counterfeiting Report [3]Source: European Union Intellectual Property Office, "Economic impact of counterfeiting in the clothing, cosmetics, and toy sectors in the EU", euipo.europa.eu. Counterfeiting continues to hinder growth in the premium segment, as consumers in price-sensitive markets opt for counterfeit products that replicate packaging but offer inferior formulations, delaying the trust-building necessary for category expansion.

Environmental regulations increasing packaging costs

Extended producer responsibility (EPR) schemes and plastic reduction mandates are driving brands to redesign packaging structures, leading to increased upfront capital expenditures and higher per-unit costs. The European Union's Single-Use Plastics Directive, which will be fully enforced in 2024, prohibits certain plastic formats and requires member states to achieve a 90% collection rate for plastic bottles by 2029. This regulation compels brands to invest in deposit-return systems and adopt recyclable materials. Additionally, EPR laws are expanding across various states, obligating manufacturers to manage packaging waste throughout the product lifecycle. For instance, Minnesota has enacted comprehensive EPR legislation that impacts cosmetics packaging. The EU's Directive 2024/825 on misleading green claims requires pre-approval for environmental statements, increasing compliance costs and legal risks for brands making sustainability claims. These regulatory and market-driven changes are dividing the industry: large companies can distribute retooling costs across global operations, while smaller brands must either innovate to meet these constraints or exit markets with stringent packaging regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Hygiene Products Lead Market Evolution

Personal hygiene products accounted for 35.16% of the projected 2025 revenue, highlighting their significance as a key contributor to the global toiletries market size. These products, which include essential items such as soaps, deodorants, and sanitary products, form the foundation of the market due to their consistent demand and necessity in daily routines. Shampoos and conditioners, while currently smaller in market share, are expected to grow at a CAGR of 6.88%, driven by the increasing popularity of sulfate-free and probiotic formulations, particularly in emerging cities across Asia. This growth is further supported by rising consumer awareness of product ingredients and their impact on health and the environment.

Advancements in micellar technology and salon-grade formulations are contributing to higher per-unit prices, even in traditionally cost-sensitive markets, thereby increasing the market share of premium haircare brands. These innovations cater to a growing segment of consumers seeking professional-grade results at home, which has become a significant trend in the personal care industry. At the same time, commoditized categories such as toothpaste are shifting towards subscription-based electric toothbrushes to maintain profit margins. This shift reflects an effort to enhance customer retention and provide added value through convenience and advanced oral care solutions.

By Category: Premium Segment Drives Value Growth

The mass tier is projected to account for 69.29% of 2025 sales, driven by the widespread availability of products in supermarkets and convenience stores. This dominance is attributed to the affordability and accessibility of mass-tier products, which cater to a broad consumer base. In contrast, premium SKUs are expected to grow at a CAGR of 7.45%, supported by the increasing adoption of refillable pods and clinically validated serums. These innovations not only justify higher price points but also appeal to environmentally conscious and health-focused consumers, contributing to the expansion of the personal care products market at the premium end.

Multinational companies are developing premium sub-lines to maintain their shelf presence and compete in the evolving market landscape. These efforts are aimed at addressing the growing demand for high-quality, specialized products. Meanwhile, direct-to-consumer (D2C) challengers are leveraging influencer marketing channels to attract early adopters, particularly within affluent urban clusters. This strategy enables D2C brands to gain a foothold in the market, often at the expense of incumbents' market share in these high-value segments.

By End User: Kids Segment Emerges as Growth Driver

Adults account for 84.19% of consumption; however, kids' SKUs are growing at a CAGR of 7.08%, driven by millennial parents who increasingly prioritize skin-friendly wipes and fragrance-free lotions as essential healthcare products for their children. This growth highlights a shift in consumer behavior, with parents increasingly inclined to invest in products that ensure their children's safety and well-being, reflecting a growing demand for high-quality, non-toxic personal care items tailored for pediatric use.

Regulations mandating stricter testing for products intended for children under 3 create significant barriers to entry. These regulations require compliance with rigorous safety standards, including toxicology assessments, clinical trials, and certification processes, which can be both time-consuming and costly. Consequently, the future market share of toiltries is expected to become increasingly concentrated among established companies with advanced toxicology testing capabilities, robust research and development infrastructure, and the financial resources necessary to navigate these stringent regulatory requirements effectively.

By Distribution Channel: Online Retail Transforms Market Access

Health and beauty specialists accounted for 38.20% of sales in 2025, driven by in-store advisors who simplify ingredient information for consumers. These advisors play a crucial role in educating customers about product formulations, helping them make informed purchasing decisions. This personalized guidance has been a key factor in maintaining the dominance of health and beauty specialists in the market. However, e-commerce is expected to grow at the fastest rate, with a CAGR of 7.89%, supported by features such as one-step checkout on social media platforms and 15-minute delivery services in densely populated metropolitan areas. The convenience offered by these advancements is reshaping consumer behavior, making online shopping increasingly appealing.

Quick-commerce purchases are primarily focused on replenishment items, such as deodorant refills, which are frequently needed and benefit from the speed of delivery. On the other hand, premium skincare products continue to rely on in-store tactile experiences, as consumers often prefer to test and feel these products before committing to a purchase. This tactile interaction is particularly important for high-value items, where trust and sensory validation play a significant role. As a result, premium brands continue to adopt omnichannel strategies, combining the convenience of online platforms with the experiential benefits of physical stores to meet diverse consumer needs effectively.

Geography Analysis

Asia-Pacific accounts for 37.40% of the current revenue and is projected to strengthen its position with a region-leading CAGR of 6.81%. This growth is driven by multiple factors, including India's USD 40 billion online beauty market, which is expanding rapidly due to increasing internet penetration and rising consumer preference for e-commerce platforms. TikTok-driven product discovery is playing a significant role in influencing purchasing decisions, particularly among younger demographics. Additionally, mandatory Halal certification requirements in Indonesia and Malaysia are shaping product formulations and marketing strategies, catering to the growing demand for Halal-compliant toiletries. Urban Chinese consumers are shifting their preferences from foreign brands to science-driven local labels, reflecting a growing trust in domestic innovation and quality. Meanwhile, Japanese companies are leveraging K-beauty sensory elements, such as unique textures and fragrances, to modernize and relaunch their heritage brands, aiming to appeal to both domestic and international markets.

North America and Europe are experiencing steady growth, influenced by premiumization trends and regulatory compliance challenges. California's PFAS ban and the EU's CMR prohibition have significantly increased reformulation costs for manufacturers, as they work to eliminate harmful substances from their products. However, these stringent regulations are creating opportunities for early adopters of natural and clean beauty products, which already meet compliance standards. This shift is driving the toiletries market toward higher average selling prices (ASPs) as consumers increasingly prioritize safety and sustainability. Furthermore, the recovery of travel retail across European and Middle Eastern hubs has revitalized demand for prestige miniatures and gift sets, particularly among international travelers seeking convenient and luxurious options.

Latin America and the Middle East & Africa present significant growth opportunities, driven by expanding urban middle classes and the implementation of formalized regulatory frameworks. In Brazil, the use of Amazonian botanicals is gaining traction as a key differentiator, helping local brands compete with imports by offering unique, sustainable, and culturally resonant products. Meanwhile, Nigeria's QR authentication system is addressing the widespread issue of counterfeit products, enhancing consumer trust and gradually steering purchasing behavior back to legitimate channels. These developments are fostering a more structured and reliable toiletries market in these regions, paving the way for sustained growth.

Competitive Landscape

The industry exhibits a moderate level of fragmentation. Multinational companies such as Procter & Gamble, Unilever, and L’Oréal leverage their scale in procurement, advertising, and research and development (R&D). These companies make significant investments in digital technologies; for instance, L’Oréal holds over 600 AI-related patents, while Unilever allocates more than USD 1 billion to regenerative agriculture programs aimed at enhancing ingredient resilience. Strategic partnerships further expand capabilities, such as Estée Lauder’s collaboration with Exuud to integrate biotech expertise into fragrance development, and Walgreens’ proposed merger with a Sycamore affiliate, which could reshape retail pharmacy shelf space.

Merger and acquisition (M&A) activity remains robust. Mars’ USD 35.9 billion acquisition of Kellanova in 2025, primarily targeting the snacking segment, highlights the ambition of conglomerates to diversify revenue streams and achieve efficiencies in shared shelf space. In response, smaller independent brands emphasize founder authenticity and sustainability, carving out niche markets that larger companies often acquire to remain competitive. Technology plays a dual role as both an enabler and a barrier: while AI-powered skin diagnostics lower entry barriers, the need to meet global quality and safety standards increases fixed costs, preventing the toiletries market from devolving into perfect competition.

Supply chain resilience continues to be a critical focus area. Companies mitigate raw material shortages through multi-source contracts and near-shoring of essential inputs, such as ethanol for sanitizer gels. However, sustainability goals face challenges, as the availability of recycled resin falls short of demand. Companies that successfully implement closed-loop packaging gain both cost and environmental advantages, appealing to regulators and consumers alike. Over the forecast period, the toiletries market is expected to experience ongoing portfolio adjustments and advancements in digital capabilities, which will remain central to competitive positioning.

Toiletries Industry Leaders

-

Procter & Gamble Company

-

Unilever plc

-

Colgate-Palmolive Company

-

Johnson & Johnson

-

L’Oréal S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TRONQUE introduced Triple Active Body Milk, formulated to combine cleansing, moisturizing, and anti-aging properties. It includes ingredients such as caffeine, green coffee, hyaluronic acid, and artichoke extract, aimed at nourishing the skin, improving firmness, and smoothing texture while addressing concerns like cellulite and elasticity.

- March 2025: Dr. Dennis launched the Gross 8-Pack Alpha Beta Glow Pad Self-Tanner, an all-in-one towelette that integrates exfoliation using AHA/BHA, soothing and antioxidant care, and natural tanning with encapsulated DHA. This product offers a multifunctional personal care solution, promoting skin renewal while providing a subtle glow.

- January 2025: The Inkey List introduced Ectoin Hydro-Barrier Serum, a multifunctional hydrating serum designed to strengthen the skin barrier and deliver intensive hydration. It features ectoin, a microbial-derived ingredient recognized for its ability to protect the skin from environmental stressors.

- December 2024: Sol de Janeiro launched Delicia Drench Shower Oil, a hydrating shower oil formulated to cleanse gently without drying the skin. It contains Brazilian oils, bacuri butter, and prebiotic hibiscus. According to the company, the product transforms from oil to foam, leaving the skin feeling moisturized and nourished, with a fragrance of sugared violet and vanilla orchid.

Global Toiletries Market Report Scope

| Soaps and body wash |

| Shampoos and conditioners |

| Toothpaste and toothbrushes |

| Deodorants and antiperspirants |

| Shaving supplies |

| Personal hygine products |

| Mass |

| Premium |

| Kids |

| Adults |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Soaps and body wash | |

| Shampoos and conditioners | ||

| Toothpaste and toothbrushes | ||

| Deodorants and antiperspirants | ||

| Shaving supplies | ||

| Personal hygine products | ||

| By Category | Mass | |

| Premium | ||

| By End User | Kids | |

| Adults | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the global toiletries market be by 2031?

The global toiletries market size is expected to reach USD 378.18 billion by 2031, expanding at a 6.57% CAGR from 2026 to 2031.

Which region offers the fastest growth opportunity?

Asia-Pacific leads with a projected 6.81% CAGR, underpinned by India’s booming e-commerce sector and Gen Z demand for Halal-certified, social-media-vetted brands.

What segment dominates current revenue?

Personal hygiene products held the highest 35.16% personal care products market share in 2025, anchored by wipes, sanitizers, and intimate care routines.

Which channel is growing quickest?

Online retail, including D2C platforms, is forecast to grow at 7.89% CAGR through 2031 as quick-commerce and influencer discovery reshape buying habits.

Page last updated on: