Intimate Hygiene Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

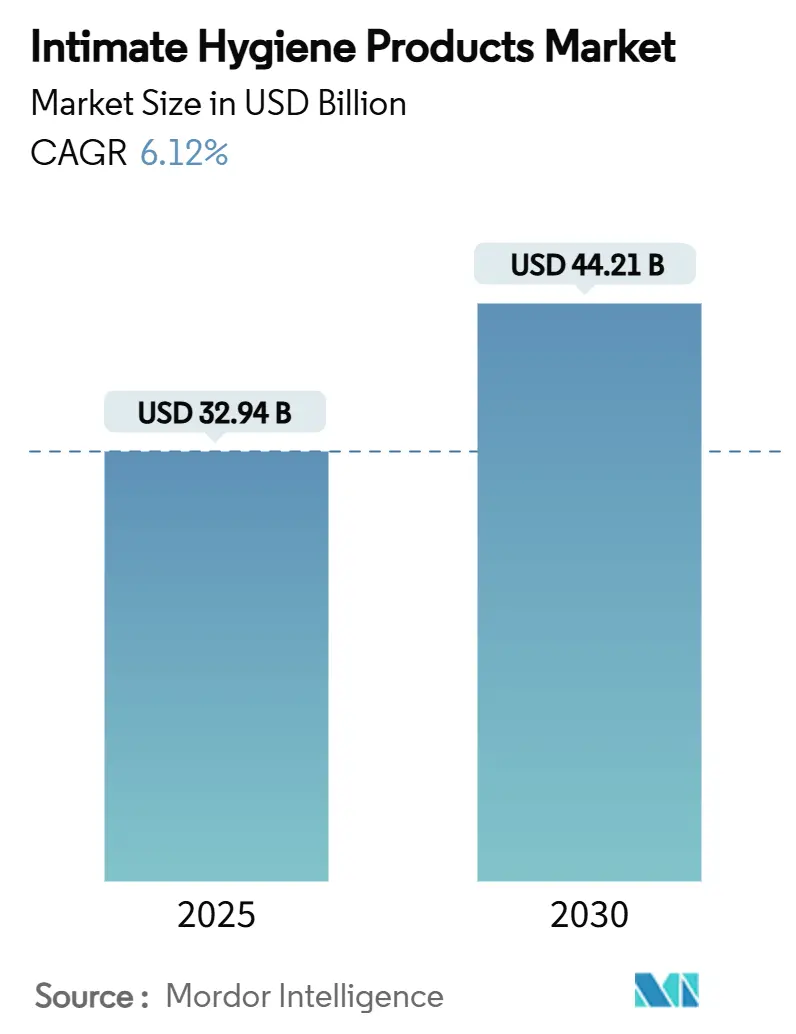

| Market Size (2025) | USD 32.94 Billion |

| Market Size (2030) | USD 44.21 Billion |

| Growth Rate (2025 - 2030) | 6.12% CAGR |

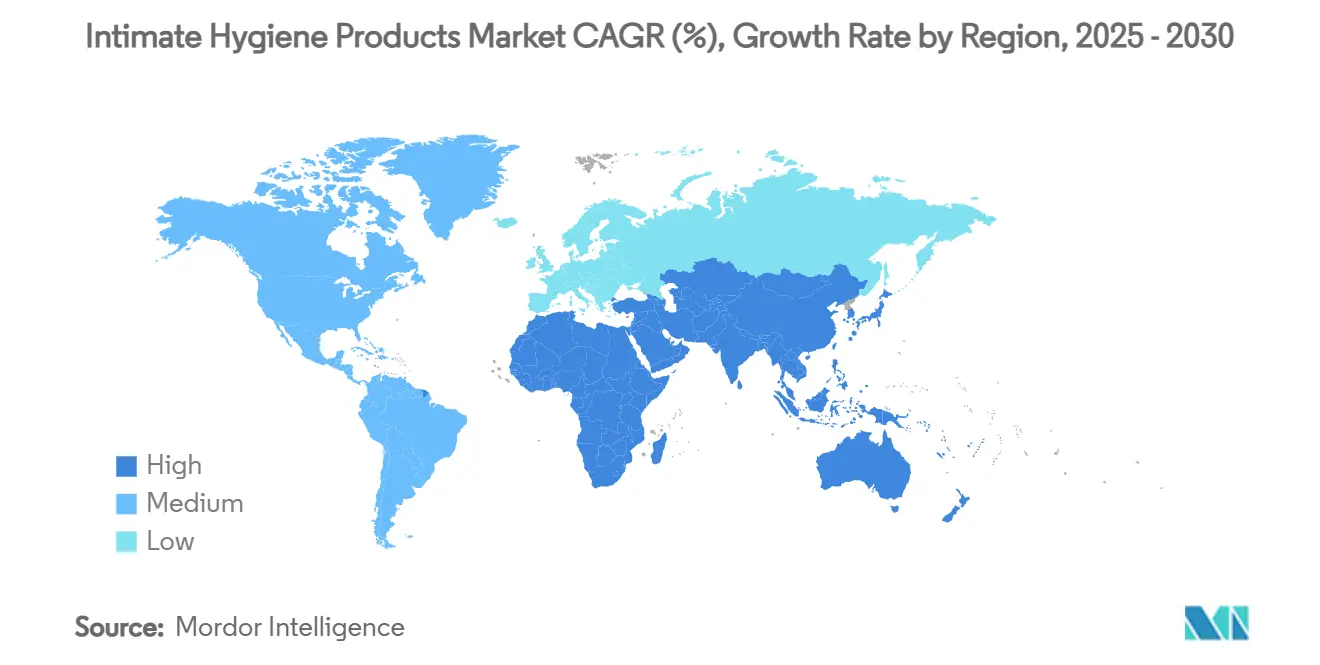

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Intimate Hygiene Products Market Analysis by Mordor Intelligence

The intimate hygiene products market size is estimated to be USD 32.94 billion in 2025 and is forecast to reach USD 44.21 billion by 2030, translating into a 6.12% CAGR. Rising destigmatization of intimate wellness, product innovations that respect microbiome balance, and stronger digital engagement position the intimate hygiene products market for steady expansion. Besides, North America leads in revenue strength, yet Asia-Pacific shows the quickest pace as government hygiene programs, urbanization, and middle-class growth lift penetration. Intensifying regulatory scrutiny in the United States and Europe pushes companies to reformulate with clinically vetted, naturally derived ingredients and sustainable packaging. Competitive energy remains high as multinationals consolidate niche brands, while direct-to-consumer entrants leverage influencer education and subscription models to tap Gen Z and millennial buyers.

Key Report Takeaways

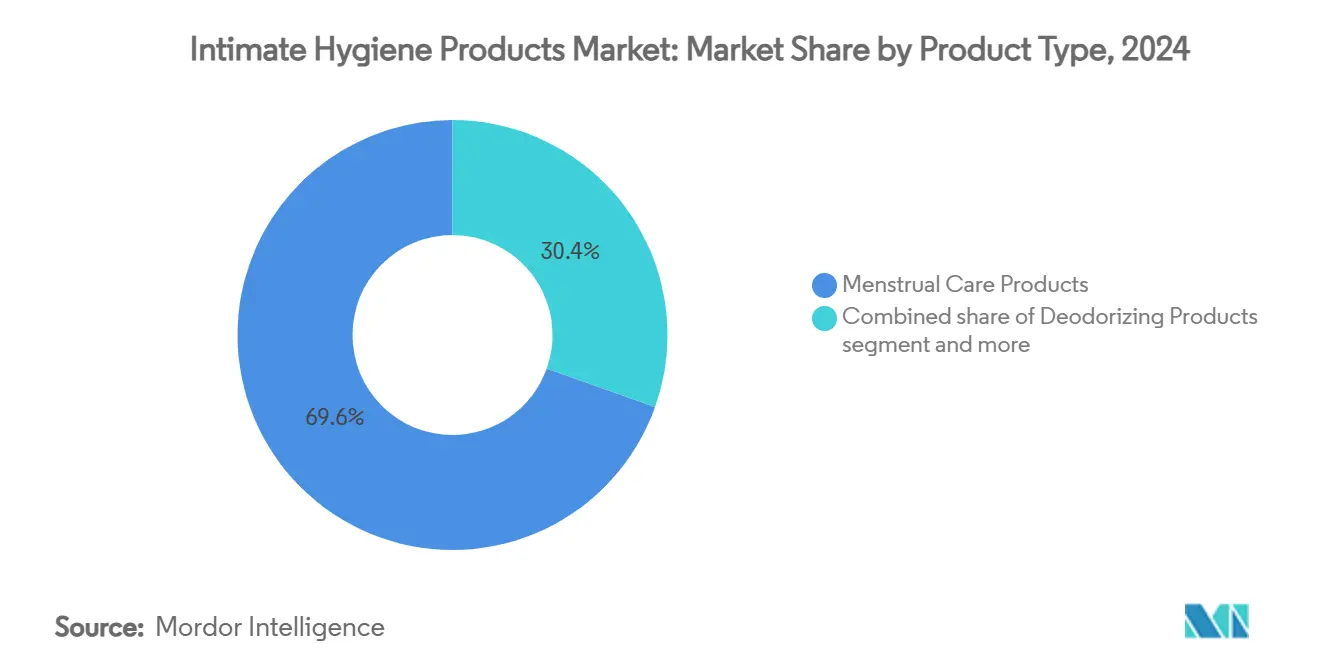

- By product type, menstrual care commanded 69.56% of the intimate care products market share in 2024; intimate cleansing solutions are projected to expand at a 7.37% CAGR through 2030.

- By gender, women accounted for 95.18% of the intimate care products market size in 2024, whereas the men's segment is accelerating at an 8.04% CAGR to 2030.

- By nature, conventional products held 85.74% revenue share in 2024; natural/organic offerings are forecast to post a 7.85% CAGR over the same horizon.

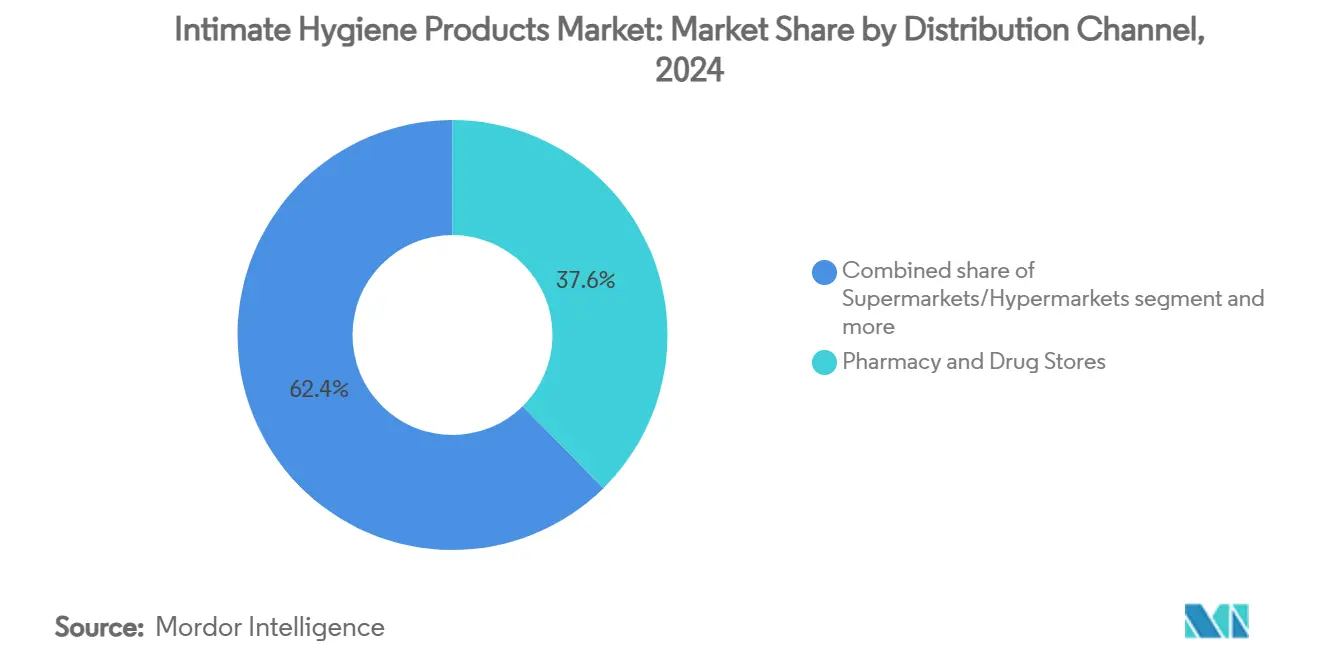

- By distribution channel, pharmacies and drug stores captured a 37.62% share of the intimate care products market in 2024, while online retail is set to climb at a 7.06% CAGR to 2030.

- By geography, North America retained a 37.93% share in 2024, while Asia-Pacific is primed for a 6.70% CAGR through 2030.

Global Intimate Hygiene Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness and education about intimate hygiene and sexual health | +0.9% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Social media and influencer marketing boosting visibility and acceptance of intimate care products | +0.7% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Product innovations in natural, organic, and pH-balanced formulations | +0.9% | North America and Europe leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing prevalence of active lifestyles and sports | +0.5% | Global, with emphasis in developed markets | Long term (≥ 4 years) |

| Growing consumer concerns about infections, skin sensitivities, and allergies | +0.6% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Increasing governmental and NGO initiatives promoting feminine hygiene awareness in developing regions | +0.8% | Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising awareness and education about intimate hygiene and sexual health

Healthcare organizations and government initiatives drive market growth through education programs establishing preventive healthcare standards. UNICEF's menstrual hygiene programs address 1.8 billion menstruators globally, focusing on dignity and safety while supporting governments in developing national strategies inclusive of marginalized groups, including girls with disabilities and transgender individuals. Similarly, the World Health Organization promotes menstrual health within universal health coverage frameworks, working with UNFPA and the Global Menstrual Health Collective to develop implementation tools for ten countries. This institutional support has established healthcare discussions in clinical settings, schools, and workplaces, generating consistent demand for evidence-based products. The impact extends beyond menstrual care into broader wellness categories, as education programs normalize discussions about pH balance, microbiome health, and preventive care practices. Furthermore, healthcare professional partnerships strengthen this development, exemplified by Kenvue's launch of Versalie in March 2024, a digital platform offering expert-reviewed content and virtual care services for menopause and women's hormonal wellness.

Social media and influencer marketing boosting visibility and acceptance of intimate care products

The market has evolved as digital platforms transform personal care product marketing from private discussions to mainstream wellness conversations. Healthcare professionals and influencers now use social media to educate audiences about personal health and normalize product usage across demographics. This shift in communication particularly appeals to younger consumers who value authenticity and peer recommendations more than traditional advertising. The market expansion has accelerated by reaching previously underserved segments, as demonstrated by men's personal care brand Manscaped, which grew from USD 3 million to USD 300 million in revenue within three years through digital marketing. Moreover, social media engagement influences product development, with companies adapting to consumer feedback regarding ingredient safety, sustainability, and inclusivity. Online discussions generate rapid awareness for new product categories, such as personal care serums and pH-balancing washes, while increasing pressure on brands to be transparent about their formulations and manufacturing processes. Direct-to-consumer brands benefit from this trend as they can modify their messaging and products based on immediate social media feedback, giving them an advantage over traditional retailers with extended product development timelines.

Product innovations in natural, organic, and pH-balanced formulations

Research and development in feminine hygiene formulations focuses on maintaining the microbiome and utilizing natural ingredients. Companies develop products that maintain vaginal pH levels between 3.8-4.5 and incorporate ingredients such as aloe vera, tea tree oil, and hyaluronic acid to enhance comfort and safety. Peer-reviewed research validates the effectiveness of natural biomaterial formulations in menstrual care products, particularly in absorbent materials and antimicrobial properties. Companies incorporate natural ingredients like coconut oil, sea buckthorn oil, and mandarin orange blossom oil while excluding parabens and synthetic dyes. The industry has also adopted sustainable packaging and biodegradable formulations to address environmental concerns without compromising product effectiveness. The FDA's MoCRA implementation requires thorough safety documentation for cosmetic products, prompting manufacturers to use clinically proven natural ingredients instead of synthetic alternatives. Manufacturing advancements enable the integration of probiotics and prebiotics in feminine hygiene products, supporting microbiome balance and addressing specific concerns such as odor control, dryness, and irritation through botanical compounds.

Growing prevalence of active lifestyles and sports

Between November 2023 and November 2024, Sport England reported that 63.7% of adults in England, approximately 30 million people, met recommended physical activity levels. This figure increased by over 2.4 million since 2016, indicating a significant shift toward more active lifestyles [1]Source: Sport England, "Record numbers playing sport and taking part in physical activity", sportengland.org. The rising number of athletes and fitness-conscious consumers generates demand for specialized hygiene products that address sweat management, chafing prevention, and post-exercise cleansing requirements. This trend influences product development in cleansing and deodorizing segments, where formulations need to balance antimicrobial effectiveness with pH maintenance during physical activity. Research in sports medicine highlights the necessity of proper hygiene to prevent infections and maintain comfort during prolonged exercise, which generates opportunities for hygiene products targeting active consumers. Thus, companies including Procter & Gamble, Kenvue, Bodyform, The Honey Pot, and Vagisil have developed products with sustainable packaging and probiotic-infused formulations to meet the needs of athletes and fitness-focused consumers. The market now offers a range of products including wipes, washes, creams, and biodegradable alternatives, distributed through e-commerce platforms and promoted via social media channels. Hence, the market's development is supported by scientifically validated products and marketing strategies that address the relationship between physical activity, perspiration, and hygiene, with product innovation focused on meeting the requirements of the active population.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulation and scrutiny over personal care ingredients and claims | -0.6% | Global, with stricter enforcement in North America and Europe | Medium term (2-4 years) |

| Environmental concerns over single-use plastics in pads and wipes | -0.4% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Concerns about allergic reactions and side effects | -0.3% | Global, with higher sensitivity in developed markets | Short term (≤ 2 years) |

| Limited access to specialized products in rural and remote areas | -0.4% | Asia-Pacific, Africa, South America, and rural North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing regulation and scrutiny over personal care ingredients and claims

The expanding regulatory landscape across regions creates compliance challenges and cost pressures, particularly affecting smaller manufacturers with limited regulatory capabilities. The FDA's Modernization of Cosmetics Regulation Act requires facility registration, product listing, adverse event reporting, and safety documentation for cosmetic products, with Good Manufacturing Practices requirements becoming effective by October 2025. Additionally, five United States states have implemented regulations on heavy metals in cosmetics, while the European Union's Single-Use Plastics Directive addresses feminine hygiene products and wet wipes through Extended Producer Responsibility schemes and consumer awareness measures [2]Source: European Commission, "Single-use plastics", environment.ec.europa.eu . These regulations require significant investments in testing, documentation, and compliance systems, which may slow product innovation and raise market entry barriers. Regulatory oversight also encompasses marketing claims, requiring clinical evidence for statements about pH balance, antimicrobial properties, and skin compatibility. Companies must comply with different international standards while ensuring consistent product quality globally, creating operational challenges that benefit larger corporations with established regulatory departments rather than resource-constrained startups.

Environmental concerns over single-use plastics in pads and wipes

Allergic reactions and side effects associated with personal hygiene products have emerged as significant concerns in the global market. Users commonly experience symptoms such as redness, itching, burning, rashes, swelling, and skin peeling in sensitive areas. These reactions typically stem from ingredients like synthetic fragrances, chemical dyes, parabens, and preservatives found in sanitary pads, wipes, and feminine washes. Prolonged exposure to irritants can lead to more severe conditions, including blistering, oozing, and secondary infections. These complications may result in long-term health issues such as vaginal flora imbalances and yeast infections. The prevalence of these reactions has increased the demand for dermatologically tested, pH-balanced, and hypoallergenic formulations. Companies like The Honey Pot, Summer's Eve, and Evvy have responded by developing products with natural, fragrance-free, and plant-based ingredients suitable for sensitive skin. Healthcare professionals recommend limiting the use of products containing harsh chemicals and replacing items that irritate. Users experiencing persistent symptoms should seek medical consultation for proper diagnosis and treatment, including the removal of irritants and application of soothing balms. The increased awareness of these health concerns has influenced the global market, encouraging product innovation focused on safety and sustainability. This trend aligns with consumer preferences for transparent ingredient lists and wellness-oriented personal care products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Menstrual Care Dominance Drives Innovation

The market share of menstrual care products reached 69.56% in 2024, driven by their essential nature and consistent repurchase patterns. The intimate cleansing segment demonstrates the highest growth rate with a 7.37% CAGR through 2030, supported by increased awareness of pH balance and microbiome health. Government initiatives strengthen the menstrual care segment, including India's Menstrual Hygiene Scheme, which provides subsidized sanitary napkins to rural adolescent girls. In Kenya, government support for local production has facilitated partnerships, such as Unicharm and Toyota Tsusho's manufacturing facility opening in January 2025. The menstrual care segment focuses on developing sustainable products, including biodegradable options made from banana fiber and bamboo-based materials that maintain absorption effectiveness while reducing environmental impact. Besides, the intimate cleansing segment grows through products featuring lactic acid for pH balance and botanical ingredients with antimicrobial properties, responding to increased consumer knowledge about intimate health.

The market for deodorizing products and intimate moisturizers forms stable segments that address consumer needs for personal comfort and confidence. Hair removal products in the intimate hygiene category align with broader grooming trends, particularly among younger consumers influenced by social media. The intimate hygiene market operates under diverse regulatory frameworks, with menstrual care products classified as medical devices in some regions, while cleansing products follow cosmetic regulations. These varying requirements influence manufacturers' compliance strategies and market entry approaches across different intimate hygiene product categories.

By Gender: Men's Segment Accelerates Despite Women's Dominance

The women segment represents 95.18% of the global intimate hygiene products market in 2024. This significant market share reflects the extensive product development focused on female care needs, including specialized washes, wipes, and moisturizers that maintain pH balance and protect sensitive skin. Major brands such as Always, Vagisil, and Summer's Eve have established market presence by addressing specific feminine hygiene requirements. The market growth is supported by women's preference for convenient purchasing options, including subscription services and online retail channels that offer discreet delivery.

Meanwhile, the men's personal care segment is growing at a CAGR of 8.04% through 2030. This growth stems from evolving cultural perspectives on masculinity and increased acceptance of male grooming practices. Companies like Skin Elements and Manscaped are developing products specifically for men's needs, incorporating features such as higher pH tolerance and masculine fragrances. The packaging design emphasizes masculine elements to appeal to male consumers. Men show preferences for discrete purchasing channels and rely on recommendations for product discovery. The market also reflects broader inclusivity through pH-neutral products that accommodate diverse consumer groups, including transgender and non-binary individuals.

By Distribution Channel: Online Retail Transforms Traditional Patterns

The market share of pharmacy and drug stores stands at 37.62% in 2024, as consumers trust healthcare professionals' recommendations for personal care products in medical retail settings. Whereas online retail stores show the highest growth rate at 7.06% CAGR through 2030, supported by privacy, convenience, and subscription services. The retail landscape continues to evolve as companies like Walmart expand their women's health product range across 1,000 locations while strengthening their e-commerce presence in April 2025. Similarly, digital platforms provide personalized recommendations and educational content beyond traditional retail capabilities, exemplified by Vush's AI implementation that improved conversion rates by 10% through automated assistance and private educational resources. The subscription model format proves effective for personal care products due to consistent replenishment requirements and consumer preferences for automated delivery services.

Supermarkets/hypermarkets cater to consumers seeking value and convenience, while specialty retailers focus on premium products and personalized service. The distribution landscape continues to transform as younger consumers increasingly adopt online and subscription-based purchasing, while older demographics prefer traditional retail stores that offer face-to-face interactions and instant product access. Companies are implementing multi-channel strategies to maximize market reach and enhance consumer engagement points.

By Nature: Natural/Organic Gains Despite Conventional Leadership

The market share of conventional products stands at 85.74% in 2024, supported by established manufacturing infrastructure, cost efficiency, and proven efficacy. The natural/organic segment is growing at a 7.85% CAGR through 2030, driven by increasing consumer demand for clean ingredients and environmental sustainability. Regulatory requirements and consumer demands for ingredient transparency strengthen the natural/organic segment's position. Companies like Grace & Green manufacture zero-waste, organic products using organic materials and sustainable packaging. Natural formulations now include scientifically validated ingredients such as aloe vera, tea tree oil, and hyaluronic acid, while excluding parabens, sulfates, and synthetic fragrances that could affect microbiome balance. B Corp certifications and climate-neutral commitments further enhance the segment's appeal to environmentally conscious consumers who accept higher prices for sustainable products.

The production of natural and organic products faces operational challenges, including supply chain consistency for ingredients, product longevity constraints, and increased manufacturing costs compared to synthetic alternatives. These factors impact pricing strategies and market penetration in cost-sensitive regions. The regulatory framework supports natural and organic product growth through ingredient restrictions and safety documentation requirements, which favor well-documented botanical ingredients over synthetic compounds with limited safety data. Market expansion in the natural and organic segment requires comprehensive consumer awareness programs focused on product application methods, storage specifications, and performance parameters compared to conventional synthetic alternatives.

Geography Analysis

North America holds a dominant 37.93% market share in 2024, supported by strong consumer demand and an extensive retail network across pharmacies, supermarkets, and e-commerce channels. The FDA's MoCRA implementation provides regulatory clarity by establishing standardized safety requirements while supporting innovation in natural and organic formulations. In the United States, consumers show increased spending on personal care products, exemplified by Kenvue's launch of the Versalie digital platform for menopause and hormonal wellness services. Additionally, Canada's single-use plastics regulations promote sustainable product development, pushing manufacturers toward biodegradable materials and circular economy practices. Mexico's market growth centers on natural care products, presenting opportunities for organic brands despite regulatory requirements for CBD products and imports.

Asia-Pacific registers the highest growth rate at 6.70% CAGR through 2030, driven by government programs, middle-class expansion, and increasing urbanization that enhances modern retail access. Manufacturing investments strengthen the regional market, including Unicharm's third Indian factory and Toyota Tsusho's partnership for Kenyan production in January 2025. Government initiatives support market development, with India's Menstrual Hygiene Scheme offering subsidized sanitary napkins to rural adolescent girls [3]Source: Ministry of Health & Family Welfare, "Menstrual Hygiene Scheme (MHS)", nhm.gov.in . Besides, Cell Biotech's expansion into Thailand and the Philippines with probiotic health products in July 2025 reflects growing consumer interest in probiotics and favorable health supplement regulations. The region's expansion stems from increased healthcare awareness, digital commerce growth, and evolving cultural attitudes toward health and wellness discussions.

Furthermore, Europe shows consistent market expansion through regulatory initiatives in sustainability and ingredient safety. The European Union's Single-Use Plastics Directive addresses hygiene products and wet wipes by implementing Extended Producer Responsibility schemes and consumer awareness measures. The United Kingdom's upcoming ban on plastic-containing wet wipes in September 2025 demonstrates the region's environmental commitment while encouraging the development of biodegradable alternatives. Germany, the United Kingdom, and France drive market advancement through robust retail networks and consumer adoption of premium products. Eastern European markets, particularly Poland, offer growth potential due to rising disposable income and changing consumer preferences. Furthermore, South America and the Middle East and Africa markets exhibit substantial unmet demand, especially in rural regions. The limited traditional retail infrastructure in these areas creates opportunities for innovative distribution methods and affordable product development.

Competitive Landscape

The market shows moderate consolidation, with established multinational corporations operating alongside direct-to-consumer (DTC) brands. These DTC companies are transforming the industry through digital marketing and subscription-based sales models. While Procter & Gamble and Kenvue maintain market dominance through extensive product portfolios and global distribution, newer companies effectively use social media and influencer partnerships to connect with younger consumers. The market's consolidation continues, as demonstrated by WellSpring Consumer Healthcare's acquisition of vH essentials in 2024 to expand its women's health segment. This consolidation indicates established companies' need to expand their product range in response to changing consumer preferences and segment-specific demand growth.

The market presents growth opportunities in men's intimate hygiene, sustainable packaging, and personalized formulations based on microbiome and hormonal analysis. The men's intimate hygiene segment is expanding through brands that focus on specific male requirements, offering targeted formulations and appropriate branding. Environmental concerns drive demand for eco-friendly packaging, including biodegradable materials and reusable containers. The personalization trend, supported by microbiome science advances, enables companies to develop targeted skincare solutions for individual needs. Luna Daily demonstrates this trend's success, securing Unilever Ventures funding and growing through products developed with dermatologists and gynecologists to meet consumer demand for clinically validated solutions.

Furthermore, manufacturing processes are evolving through increased automation and precise formulation capabilities, improving product quality and operational efficiency. Modern production methods, including air-through bonding systems and airlaid technology, enable high-quality product development at scale. Market success now requires companies to combine clinical effectiveness, ingredient transparency, and sustainable packaging with educational content rather than traditional marketing focused on discretion. Successful brands emphasize clear ingredient disclosure, environmental responsibility, and educational initiatives to build consumer trust. Companies that combine scientific innovation with authentic consumer engagement are well-positioned in the global market.

Intimate Hygiene Products Industry Leaders

-

Kenvue Inc.

-

Procter & Gamble Company

-

Kimberly-Clark Corporation

-

Unicharm Corporation

-

Edgewell Personal Care Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Niches & Nooks launched its intimate care product line exclusively at Target, introducing pH-balanced body care items. The product range included a gentle cleanser, refreshing towelettes, anti-chafing barrier spray, and body fragrance mist, addressing intimate wellness and personal hygiene requirements. The brand's initial collection comprised Wash Your Nooks Gentle Cleanser, Wipe Your Nooks Refreshing Towelettes, Dry Your Nooks Sweat Absorbing Chafing Barrier Spray, and Freshen Your Nooks Body & Fabric Fragrance Mist.

- January 2025: Lola, a female wellness brand, expanded its product portfolio with a postpartum care product line through its website and Walmart retail locations. The initial collection included stretch mark prevention cream, organic cotton postpartum pads, and perineal gel pads for both hot and cold therapy.

- August 2024: Kiehl's expanded its product portfolio with 'Kiehl's Personals,' a new intimate care product line supported by clinical testing. The range comprised two products developed for intimate areas. The 'Ingrown Hair & Tone Corrective Intimate Drops,' formulated for all skin types, tones, and genders, contained AHAs, Astaxanthin, and Jojoba Oil to reduce ingrown hairs, enhance skin tone, and reinforce the skin barrier. The 'Over & Under Cream to Powder Deodorant' delivered 96-hour protection for underarms and intimate areas through acid blends and a cream-to-powder formula, without aluminum or talc.

Global Intimate Hygiene Products Market Report Scope

| Menstrual Care Products (e.g. pads, tampons, period panties, menstrual cups) |

| Intimate Cleansing Products (e.g. washes, wipes, gels, soaps, sprays) |

| Deodorizing Products |

| Intimate Moisturizers and Creams |

| Hair Removal Products |

| Women |

| Men |

| Conventional |

| Natural/Organic |

| Supermarkets/Hypermarkets |

| Pharmacy and Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Menstrual Care Products (e.g. pads, tampons, period panties, menstrual cups) | |

| Intimate Cleansing Products (e.g. washes, wipes, gels, soaps, sprays) | ||

| Deodorizing Products | ||

| Intimate Moisturizers and Creams | ||

| Hair Removal Products | ||

| By Gender | Women | |

| Men | ||

| By Nature | Conventional | |

| Natural/Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacy and Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the intimate hygiene products market in 2025?

The intimate hygiene products market size is USD 32.94 billion in 2025 and is on track to reach USD 44.21 billion by 2030 at a 6.12% CAGR.

Which product category generates the most revenue?

Menstrual care products account for 69.56% of 2024 revenue, reflecting essential monthly use and government subsidy programs.

Which region shows the fastest growth through 2030?

Asia-Pacific is set for the quickest advance, rising at a 6.70% CAGR thanks to public-sector hygiene initiatives and expanding middle-class demand.

What is driving the rise in male intimate hygiene consumption?

Evolving perceptions of masculinity, influencer education, and discrete DTC subscription models are enabling an 8.04% CAGR in the men’s segment.

Page last updated on: