Syria Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

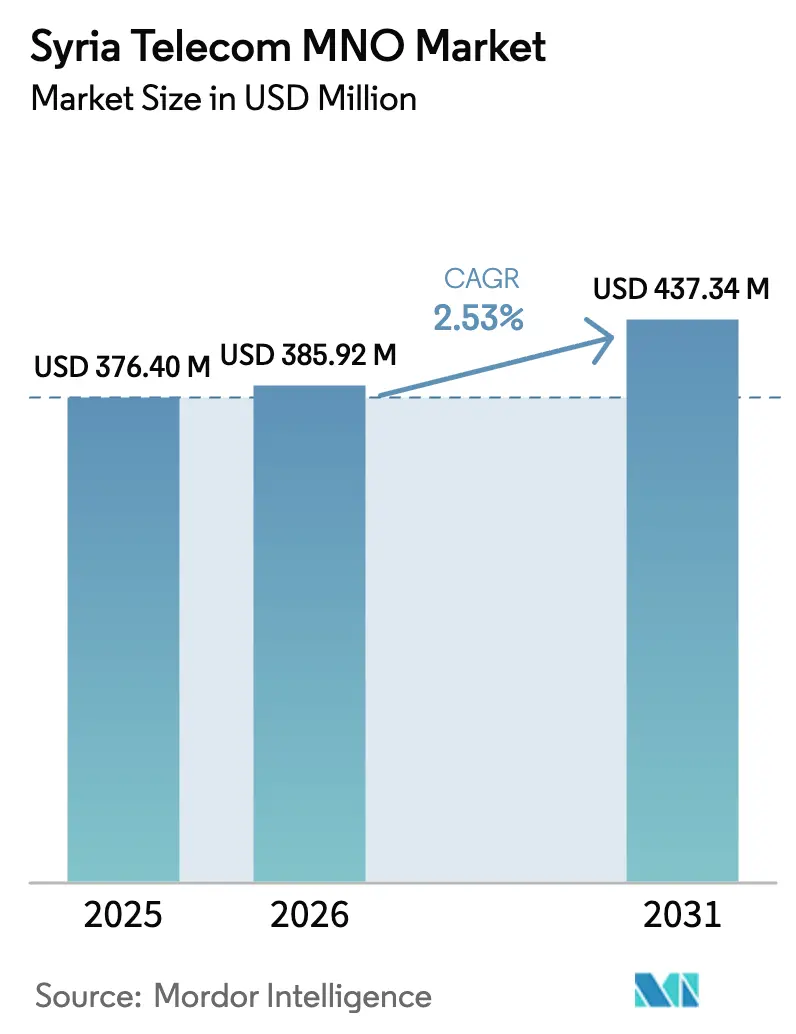

| Base Year Market Size (2025) | USD 376.40 Million |

| Market Size (2026) | USD 385.92 Million |

| Market Size (2031) | USD 437.34 Million |

| Growth Rate (2026 - 2031) | 2.53% CAGR |

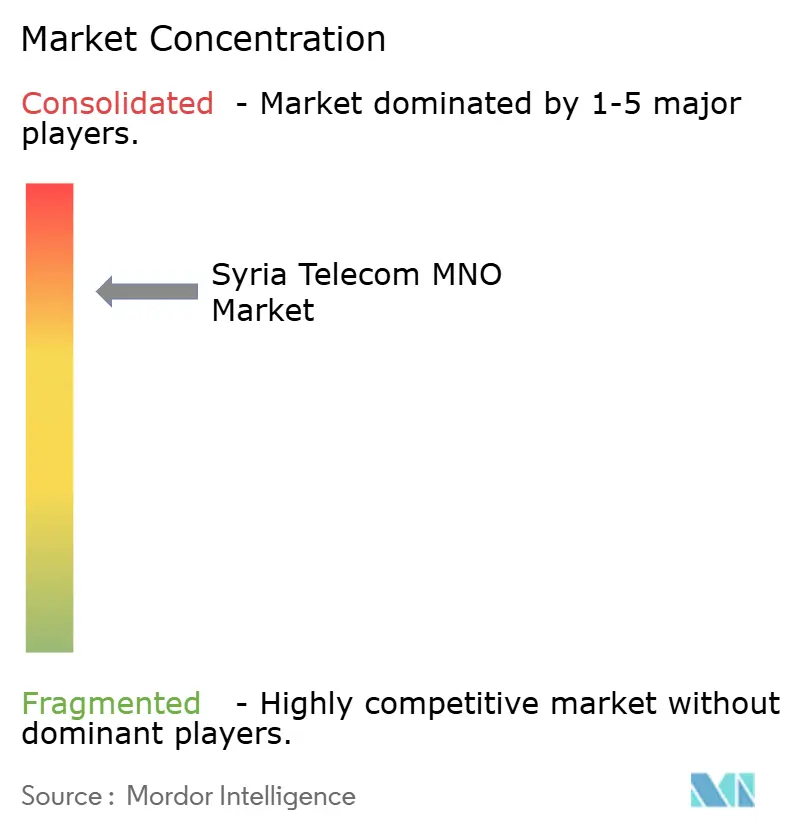

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Syria Telecom MNO Market Analysis by Mordor Intelligence

The Syria Telecom MNO Market size was valued at USD 376.40 million in 2025 and estimated to grow from USD 385.92 million in 2026 to reach USD 437.34 million by 2031, at a CAGR of 2.53% during the forecast period (2026-2031).

Demand for essential connectivity, the rapid restoration of damaged towers in government-controlled territories, and diaspora-funded smartphone upgrades underpin this resilient yet modest growth path. Operators are prioritizing 4G coverage in Damascus, Aleppo, and Homs to monetize data traffic, while sanctions-driven vendor restrictions have nudged them toward infrastructure-sharing frameworks that temper capital intensity. Consumer affordability pressures remain acute, 69% of citizens live in poverty, yet prepaid voice and low-tier data bundles still attract steady volumes, and the prospect of a World Bank-backed fiber-backbone program provides a long-term uplift to network quality. Competitive dynamics tightened sharply after MTN’s exit in 2021, leaving Syriatel with a commanding position, even as newcomer Wafa Telecom readies Iranian-sourced equipment to contest high-ARPU urban districts.

Key Report Takeaways

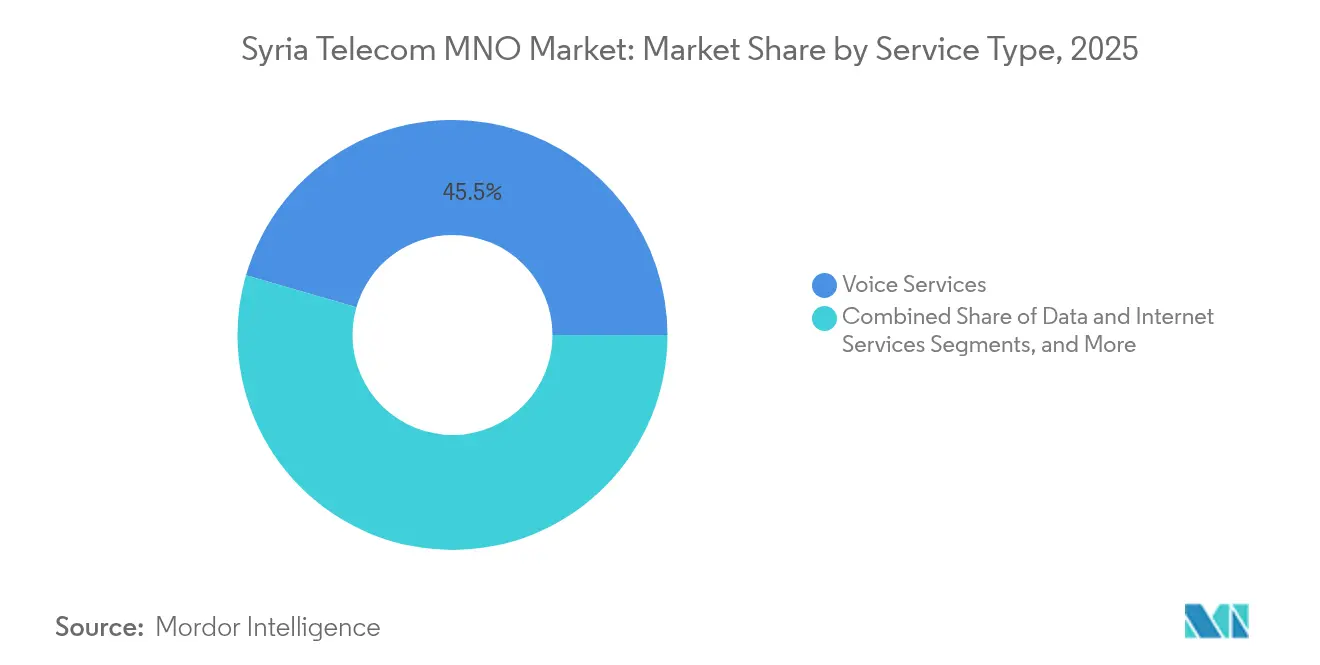

- By service type, voice services led with 45.52% of the Syria Telecom MNO market share in 2025, whereas other services are projected to grow fastest at a 2.59% CAGR through 2031.

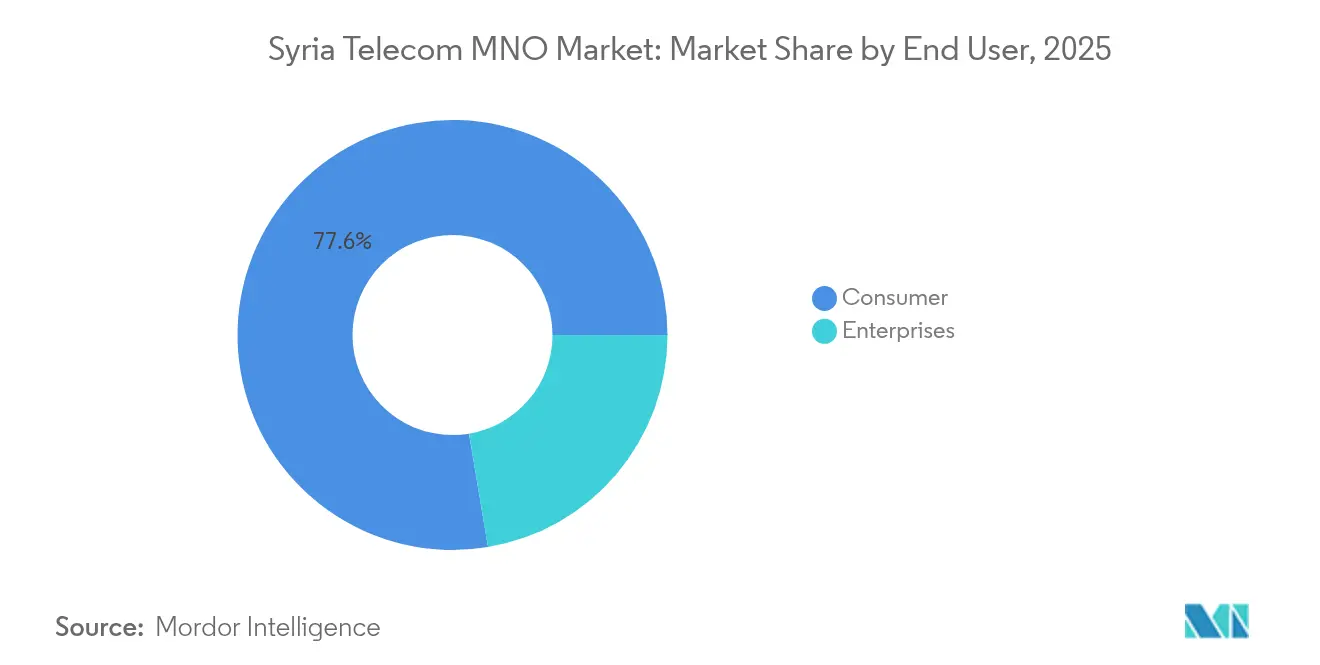

- By end user, the consumer segment accounted for 77.64% of the Syria Telecom MNO market size in 2025, while the enterprise segment is forecast to expand at a 2.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Syria Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G rollout in government-controlled areas | +0.8% | Government-controlled territories, Damascus, Aleppo, Homs | Medium term (2-4 years) |

| Growing demand for video-streaming and OTT content | +0.6% | Urban centers, Damascus Metropolitan Area | Short term (≤ 2 years) |

| Surge in diaspora remittances driving smartphone upgrades | +0.4% | National, concentrated in Damascus, Aleppo | Medium term (2-4 years) |

| World Bank-backed fiber-backbone rehabilitation projects | +0.3% | National infrastructure, rural connectivity focus | Long term (≥ 4 years) |

| Public-sector digitalization (ID, tax, customs) | +0.2% | Government-controlled areas, administrative centers | Medium term (2-4 years) |

| UN-funded connectivity for humanitarian agencies | +0.1% | Refugee camps, humanitarian zones, cross-border areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid 4G rollout in government-controlled areas

Aggressive site densification across Damascus, Aleppo, and Homs has lifted median mobile download speeds to 26.4 Mbps, enabling operators to reposition plans around data volume rather than voice minutes. [1]Speedtest, “Global Index – Syria,” speedtest.net Network improvements lower churn, justify marginal price premiums, and create a scalable platform for enterprise VPNs and e-government services. Concentrated capex in secure regions shortens payback periods and limits exposure to asset loss, an acute concern in contested zones. The driver adds a virtuous cycle: higher speeds stimulate OTT usage, which in turn increases average revenue per user (ARPU) and finances further coverage expansion. Consequently, the Syria Telecom MNO market now sees data traffic growing more than three times faster than voice traffic despite macro-economic headwinds.

Growing demand for video streaming and OTT content

Urban Syrians increasingly rely on mobile data to access regional entertainment platforms, driving double-digit growth in average monthly gigabyte consumption. [2]Christian Science Monitor, “As Syrians Struggle to Rebuild,” csmonitor.com Operators have responded by tiering bundles around HD-video thresholds, nudging subscribers toward pricier packages. This consumption boom reinforces the 4G investment case and pushes policymakers to allocate additional spectrum in the 1800 MHz band. Content-driven traffic also encourages partnerships with regional OTT providers, opening co-branding revenue streams that partially offset the ARPU drag from inflation-linked currency devaluation. Overall, heightened video demand adds 0.6 percentage points to the forecast CAGR for the Syria Telecom MNO market.

Surge in diaspora remittances driving smartphone upgrades

Remittances, estimated at 9% of GDP, flow directly into handset purchases and data-heavy plans, insulating a sizable user cohort from domestic income shocks. Families prioritizing cross-border communication opt for mid-range Android devices and higher-tier data allotments, bolstering operator unit revenues. The phenomenon also sustains demand for international calling add-ons and roaming bolt-ons, two of the few high-margin product lines under sanctions. Crucially, remittance-fueled spending is geographically diverse, spreading traffic beyond Damascus to Aleppo, Latakia, and Hama, which supports a broader base-station upgrade strategy.

World Bank-backed fiber-backbone rehabilitation projects

The World Bank’s 2025 decision to clear Syria’s USD 15 million arrears unlocks concessional funding for a 1,500 km fiber rebuild that will interlink governorate capitals and boost backhaul capacity by 70%. A modern backbone reduces latency, cuts leased-line costs, and enables nationwide 4G expansion without prohibitive microwave reliance. Wholesale leasing opportunities emerge, letting smaller ISPs and humanitarian agencies piggyback on carrier fiber, creating a secondary revenue layer. Importantly, multilateral financing sidesteps some sanctions hurdles, giving operators access to approved vendors and long-dated credit on favorable terms.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S./EU sanctions limiting vendor options and capital | -0.9% | National, affecting all operators | Long term (≥ 4 years) |

| Chronic electricity outages are hampering QoS | -0.7% | National, particularly rural and conflict-affected areas | Medium term (2-4 years) |

| Currency depreciation eroding consumer purchasing power | -0.5% | National, urban centers most affected | Short term (≤ 2 years) |

| Security-related shutdowns and network damage in conflict zones | -0.3% | Border regions, contested territories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

U.S./EU sanctions limiting vendor options and capital

The export-control regime blocks access to most Western RAN and core platforms, forcing reliance on a narrow set of exempt or secondary-market suppliers. [3]Digital Medusa, “Sanctions and the Internet,” accessnow.org Procurement costs rise by roughly 25%, delivery lead times stretch, and multi-band 5G-ready gear remains largely out of reach. Financing is equally constrained; foreign banks shun Syrian risk, leaving operators dependent on cashflow funding and sporadic state-linked loans. Strategic planning horizons shorten, resulting in reactive, piecemeal upgrades instead of holistic modernization. This restraint knocks almost 1 percentage point off the long-term CAGR of the Syria Telecom MNO market.

Chronic electricity outages hampering QoS

National power-grid availability hovers near 60%, with rural pockets dipping below 40%, obliging MNOs to deploy diesel gensets, batteries, and small-scale solar at thousands of sites. [4]Christian Science Monitor, “As Syrians Struggle to Rebuild,” csmonitor.com Backup OPEX absorbs an estimated 10% of annual revenue, squeezing margins already pressured by inflation-driven cost escalation. Intermittent power degrades call-setup success rates and download speeds, prompting subscriber complaints and occasional churn to Turkish or Jordanian roaming signals along the border communities. Until broader grid reforms materialize, energy unreliability will continue to suppress the Syria Telecom MNO market’s service-quality perception and revenue potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Voice sservices held 45.52% of the Syria Telecom MNO market size in 2025, reflecting the indispensability of basic calling in a low-income landscape where handset replacement cycles extend beyond three years. Although per-minute usage is sliding, prepaid bundles remain the default communication entry point for 80% of subscribers, cushioning revenue erosion. Data and Internet Services, buoyed by the 4G build-out, now account for nearly one-third of total revenue and post mid-single-digit traffic growth quarterly. Messaging revenues plateau as users pivot to OTT chat apps, yet SMS retains importance for two-factor authentication and humanitarian alerts.

Other Services, VAS, international roaming, and enterprise VPNs represent the bright spot, forecast to expand at a 2.59% CAGR and capture an incremental share of the Syria Telecom MNO market by 2031. Operators package diaspora-oriented IDD minutes with micro-roaming bundles, harvesting premium yields from families split across borders. Meanwhile, IoT and M2M connections languish below 0.5% of SIM base, hamstrung by limited enterprise digitization and the absence of a national numbering plan for LPWAN. Still, incremental pilots in smart-metering point to a nascent Syria Telecom MNO industry opportunity once sanctions ease and power-grid stability improves.

By End User: Consumer Dominance Masks Enterprise Opportunity

Consumers accounted for 77.64% of the Syria Telecom MNO market share in 2025, underlining the sector’s dependence on mass prepaid volumes. High poverty levels cap ARPU at one of the lowest in MENA, compelling operators to prioritize cost-to-serve efficiency and digital self-care channels to protect margins. Nevertheless, discrete high-value niches exist: remittance-funded households regularly purchase 20 GB data packs, and urban youth segments fuel OTT-video traffic spiking at peak evening hours.

Enterprise accounts, only 22.36% of revenue today, are projected to grow fastest at 2.94% CAGR, aided by public-sector modernization projects funded by multilaterals and the UN. Ministries adopting e-procurement and customs digitization need secure APNs, while NGOs require resilient voice/data links in field offices. Such contracts typically run three-year tenures with service-level agreements that command margin uplifts of 6-8 percentage points over retail business. As sanctions relief discussions progress, industrial IoT and oil-field telemetry could unlock an even larger Syria Telecom MNO industry revenue pool beyond 2030.

Geography Analysis

Government-controlled corridors encompassing Damascus, Aleppo, and Homs capture over 65% of traffic and the bulk of new 4G investment, ensuring superior throughput and elevating ARPU by 15-20% against the national average. The Syria Telecom MNO market size attributed to the Damascus metropolitan cluster alone is estimated at USD 148.6 million, supported by a 6 million urban population and dense retail footprint. Coastal governorates benefit from relatively intact fiber routes via Tartus, yet radio networks suffer weather-related outages that intermittently depress service quality.

Central and northeastern swathes, once battlefield zones, display patchwork coverage; operators rely on microwave hops where fiber ducts remain mined or looted. Cross-border leakages are common: Turkish carriers inadvertently roam into Idlib and Raqqa, creating informal competition that forces local price promotions. Eastern oilfields present an untapped high-ARPU enclave, but security risks and checkpoint fees deter tower maintenance crews.

Rural highlands lag farthest behind; less than 50% of villages enjoy 3G, let alone 4G. World-Bank-financed backbone reconstruction, slated to reach final acceptance in 2028, should extend high-capacity rings to Latakia, Daraa, and Deir ez-Zor, narrowing the digital divide by the end of the decade. Until then, satellite-backhauled sites and humanitarian Wi-Fi hubs funded by the Emergency Telecommunications Cluster will remain vital stopgaps along fragile corridors.

Competitive Landscape

Syriatel wields an estimated 80% subscription grip, translating into near-national distribution control and first call on vendor inventory during sanctions-induced shortages. Its aggressive 4G overlay, 1,200 sites lit since mid-2023, delivers measurable QoS advantages that justify a 5-10% tariff premium in urban bundles. Capital discipline centers on tower-sharing, with 42% of new masts co-located to trim OPEX.

Wafa Telecom, holder of the third mobile license awarded in 2022, prepares a phased launch leveraging Iranian vendor financing and swap deals that skirt Western export controls. The entrant’s go-to-market plan targets underserved peri-urban belts with deep-indoor 700 MHz coverage and diaspora-bundled international minutes. A non-negligible 10% share target by 2030 could dilute Syriatel’s dominance if spectrum refarming accelerates.

Beyond subscriber counts, strategic differentiation pivots on enterprise contracts and rural public-private partnerships. Operators court ministries with managed MPLS and secure cloud access, while humanitarian-sponsored base stations unlock subsidies that defray diesel costs in off-grid areas. Vendor alliances are equally crucial; Chinese and Iranian OEMs provide deferred-payment terms that outcompete cash-on-delivery European alternatives, an edge visible in the Syria Telecom MNO market’s recent uptick in multi-band indoor small-cells.

Syria Telecom MNO Industry Leaders

Syriatel

MTN Syria

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Gulf telecommunication groups entered a competitive tender for Syria’s national fiber-optic corridor, signaling renewed regional appetite for infrastructure stakes.

- December 2024: Syriatel unveiled 2025 prepaid data plans priced from SYP 14,000 for 4 GB to SYP 40,000 for 20 GB per month, bundling night-time rollover and zero-rated civil-service portals.

Syria Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Syria Telecom MNO market?

The sector is valued at USD 385.92 million in 2026 and is projected to reach USD 437.34 million by 2031.

Which segment leads by revenue?

Voice Services remain largest, holding 45.52% of revenue in 2025.

Which service category is growing fastest?

Other Services, including VAS and roaming, are forecast to post a 2.59% CAGR to 2031.

How concentrated is operator control?

Syriatel controls about 80% of subscriptions, giving the market a high concentration score of 8.

What external funding could accelerate network upgrades?

World Bank-backed fiber-backbone projects offer concessional capital and vendor access to modernize nationwide infrastructure.

Are sanctions still the biggest hurdle?

Yes; U.S./EU restrictions limit vendor choices and financing, trimming almost 1 percentage point from long-term CAGR.

Page last updated on: