Chad Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

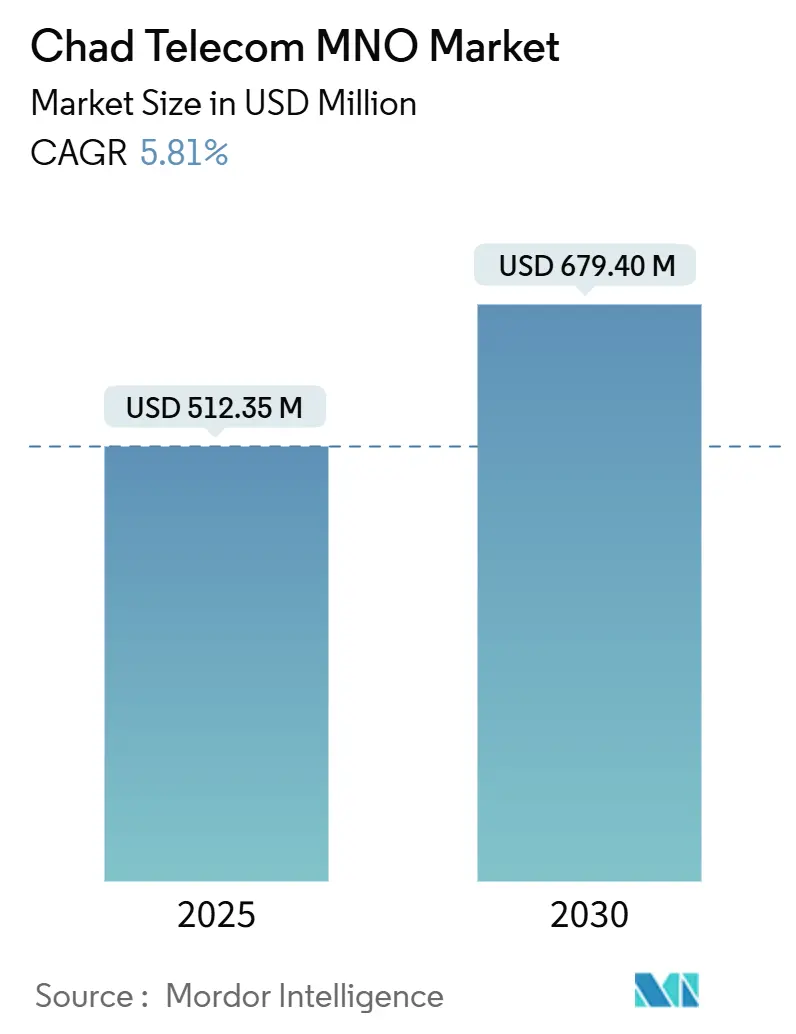

| Market Size (2025) | USD 512.35 Million |

| Market Size (2030) | USD 679.40 Million |

| Growth Rate (2025 - 2030) | 5.81% CAGR |

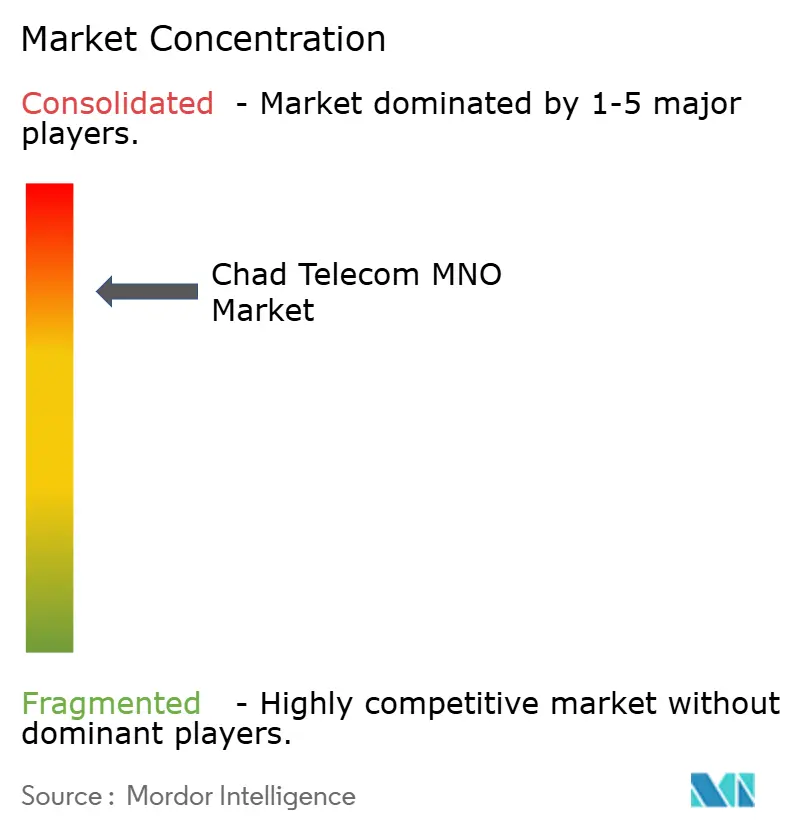

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chad Telecom MNO Market Analysis by Mordor Intelligence

The Chad Telecom MNO Market size is estimated at USD 512.35 million in 2025, and is expected to reach USD 679.40 million by 2030, at a CAGR of 5.81% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 13.93 million Subscribers in 2025 to 17.69 million Subscribers by 2030, at a CAGR of 4.89% during the forecast period (2025-2030).

Rising smartphone adoption, expanding mobile-money ecosystems, and stepped-up 4G investments are steering revenue away from basic voice lines toward bandwidth-intensive data services. Public-private infrastructure projects, including the World Bank-financed Digital Transformation Project, are helping operators close rural coverage gaps despite persistent grid-power shortages. Competitive intensity remains moderate because Moov Africa Chad and Airtel Chad collectively command the bulk of subscribers, yet looming satellite broadband entry and the planned Sotel divestiture signal a more open playing field. Wide-ranging sector-specific taxes and episodic internet shutdowns temper growth by squeezing household affordability and dampening investor confidence, though recent tariff cuts and temporary excise-duty relief demonstrate a policy shift toward market stimulation.

Key Report Takeaways

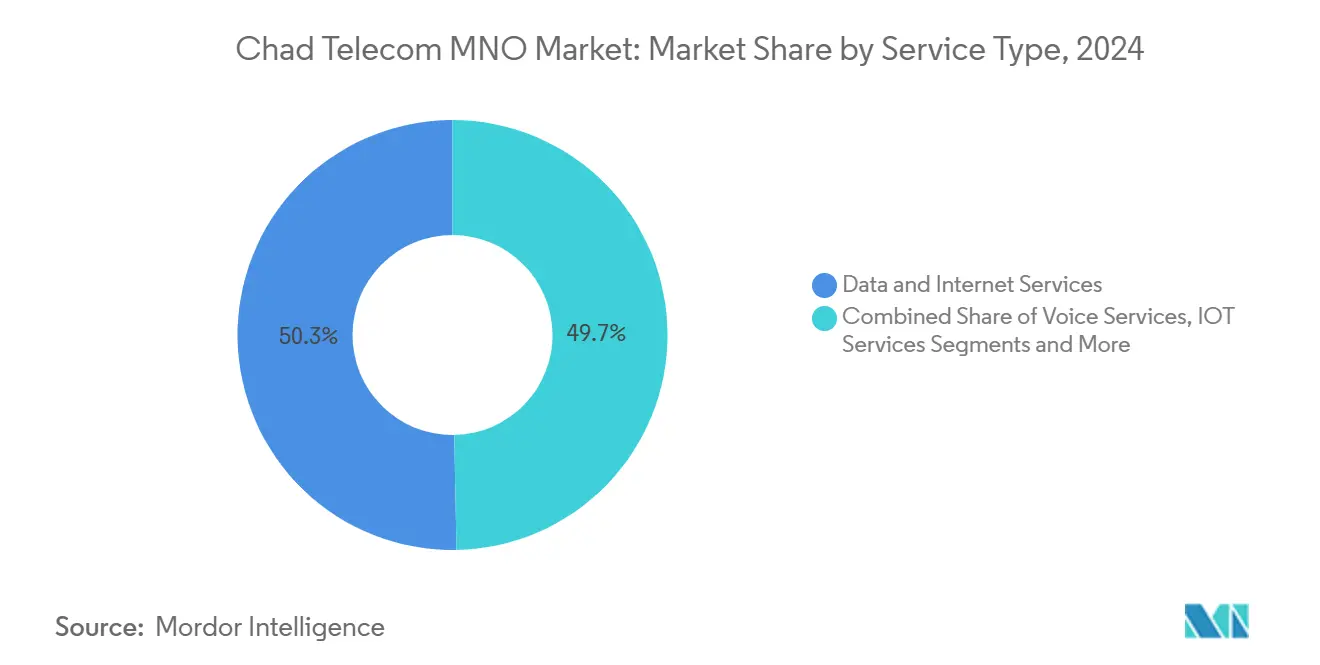

By service type, data services held 50.29% of the Chad telecom market share in 2024 and are projected to compound at a 5.86% CAGR through 2030.

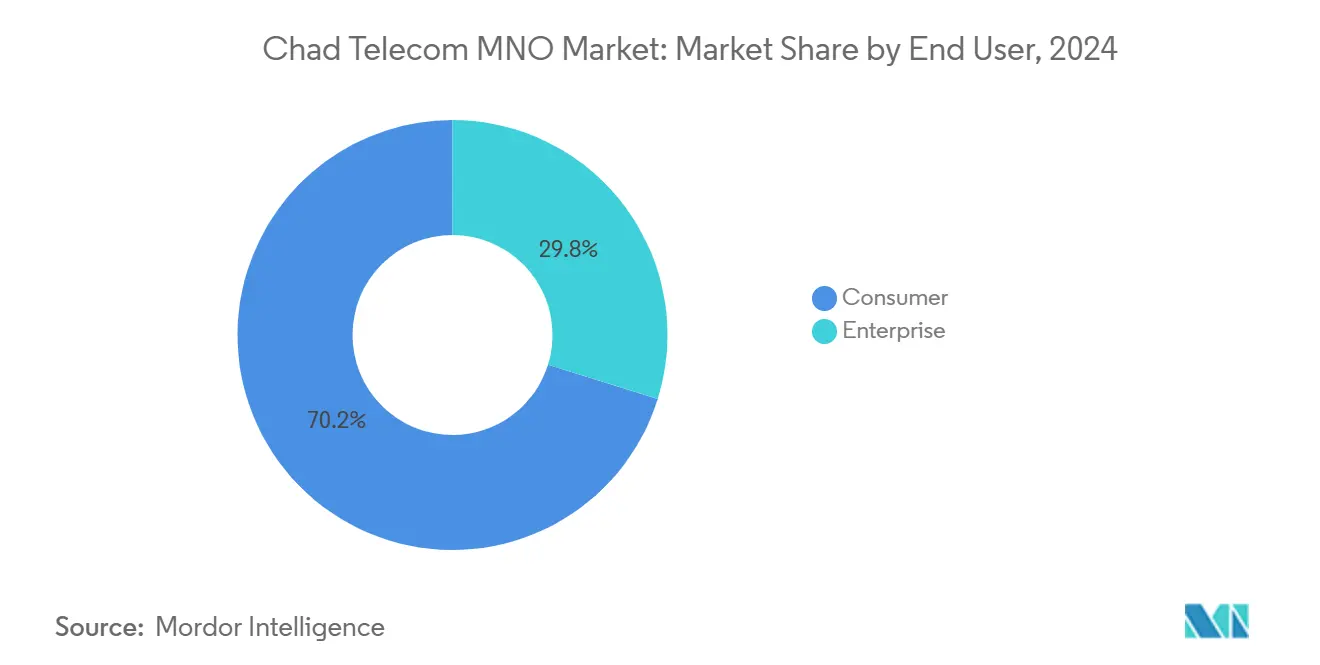

By end-user, consumer services accounted for 70.19% of the Chad telecom market size in 2024, while the enterprise segment records the highest forecast CAGR at 6.15% over 2025-2030.

Chad Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive 4G and upcoming 5G CAPEX by incumbent operators | +1.2% | National, initial focus on N’Djamena and Moundou | Medium term (2-4 years) |

| Mobile-money–led surge in data traffic | +0.9% | National, strongest in dense urban corridors | Short term (≤2 years) |

| Government digital-service programmes under National Plan | +0.8% | Country-wide, anchored in public-sector platforms | Long term (≥4 years) |

| Cheaper Chinese smartphones widening the addressable base | +0.7% | Rural and peri-urban districts | Short term (≤2 years) |

| Youth-driven OTT video and e-sports adoption | +0.5% | Urban hubs and second-tier cities | Medium term (2-4 years) |

| New subsea systems lowering international bandwidth costs | +0.6% | National, import routes to global backbone | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aggressive 4G and Upcoming 5G CAPEX by Incumbent Operators

Regional carriers have scaled network-modernization budgets, with MTN Group alone allocating USD 300 million for Cameroon over 2024-2026, a spending template extended to Chad operations.[1]Developing Telecoms, “MTN Cameroon to Receive Major Investment Boost,” developingtelecoms.com Airtel directed more than USD 20 million to build 202 urban 4G sites since 2018, lifting national 4G coverage from 24% to 36%. Larger channel widths and fiber backhaul upgrades cut latency and boost average downlink speeds past 25 Mbps, enabling operators to upsell premium data bundles to enterprises and high-usage youth segments. Equipment-sharing accords lower CAPEX per site and accelerate rural roll-outs, while planned 5G trials position carriers to chase emerging IoT and low-latency use cases once spectrum becomes available. As coverage widens, penetration elasticities drive fresh subscriber additions and lift data ARPU, translating the +1.2% uplift in forecast CAGR.

Mobile-Money–Led Surge in Data Traffic

Orange Money’s African customer base crossed 62 million in 2024, and Chad’s cash-lite policy stance is prompting households to shift everyday payments to mobile wallets. Airtel’s headline price cut from 12,000 FCFA to 1,500 FCFA per GB made always-on smartphone access possible for low-income users.[2]Orange, “Africa & Middle East Lead Way for Orange Growth,” developingtelecoms.comEach wallet authentication, balance query, or QR transaction consumes data, creating a steady baseline of packet demand independent of video streaming peaks. Merchants onboarding to wallet acceptance platforms widen transaction nodes, further normalizing data use. The result is a virtuous cycle in which financial-inclusion goals directly stimulate broadband uptake, adding +0.9% to the Chad telecom market CAGR forecast.

Government Digital-Service Programmes under National Plan

The National Development Plan channels USD 22.25 billion toward structural transformation, with the World Bank’s USD 92.2 million Digital Transformation Project earmarking funds for e-government platforms that will serve 2 million citizens. Ministries must procure secure links to host electronic tax, land, and ID systems, spurring enterprise-connectivity contracts that lift operator B2B revenue. Huawei’s memorandum with Chad covers ICT training and cloud-service pilots, signalling long-run enterprise digitization pipelines. The public sector’s early adoption serves as a proof case that nudges banks, agribusinesses, and retailers toward similar cloud and IoT solutions, injecting another +0.8% into the growth curve.

Youth-Driven OTT Video and E-Sports Adoption

With a median age of 15.8 years, Chad has one of the youngest populations globally. TikTok alone captured 1.68 million adult users by early 2025. This cohort demands high-resolution streaming and latency-sensitive multiplayer gaming, pushing network planners to prioritise capacity augments in N’Djamena and Moundou. Operators bundle zero-rated social-media passes and unlimited-night data to monetise binge-watch habits, while content creators localise short-form videos in French and Sara. Rising e-sports tournaments increase demand for low-jitter connections, reinforcing the +0.5% driver impact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sector-specific tax on SIM cards and devices | -0.8% | Nationwide, heavy drag on low-income uptake | Short term (≤2 years) |

| Frequent internet shutdowns during political unrest | -0.6% | Mostly urban business districts | Short term (≤2 years) |

| Limited power grid forcing diesel-run towers | -0.5% | Remote northern and eastern zones | Long term (≥4 years) |

| Cyber-security talent gap slowing FTTH adoption | -0.3% | Urban enterprise clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Sector-Specific Tax on SIM Cards and Devices

Despite repeal of an 18% excise levy on service charges in 2020, import duties on handsets and activation taxes continue to inflate the effective cost of joining the Chad telecom market.[3] International Trade Administration, “Chad – Telecommunications,” trade.govPrice-sensitive rural consumers delay switching from shared feature-phones to entry-level Android models, slowing incremental subscriber growth. Operators must absorb part of these taxes through promotions, compressing margins and curbing reinvestment capacity. The fiscal burden also widens the cost delta with neighbouring Cameroon and Sudan, complicating cross-border roaming propositions and undermining regional harmonisation efforts.

Frequent Internet Shutdowns During Political Unrest

Nationwide blackouts ordered during security incidents suspended mobile-data services for cumulative weeks in 2024, paring operator revenue and eroding trust among SMEs dependent on cloud systems.Recurrent interruptions raise the perceived risk premium for foreign investors evaluating data-centre and fintech ventures. Operators cannot forecast or hedge against such edicts, producing operational disarray and customer-churn spikes that weigh on year-end profitability. Each shutdown lengthens payback periods on network assets, reducing incentive for deep-rural 4G expansion and subtracting 0.6 percentage points from projected CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data services contributed 50.29% of 2024 revenue within the Chad telecom market and are set to expand at 5.86% through 2030, while voice retained 40.06% with a near-identical 5.85% pace. The cost plunge to 1,500 FCFA per GB triggered elasticity effects, lifting average monthly data usage above 3.4 GB. Voice resilience stems from fewer than 1 fixed-line connections per 100 inhabitants, leaving mobile as the de facto national dial-tone. IoT still captures only 4.79% yet enjoys policy tailwinds from agri-sensor pilots and planned smart-meter roll-outs.

Smartphone imports from Shenzhen-based manufacturers now retail below 22,000 FCFA, coaxing first-time users online. OTT bundles align with the youth cohort’s content tastes, and PayTV streaming piggybacks on upgraded 4G backhaul. IoT uptake should quicken after operators standardise NB-IoT firmware on existing LTE bands. As each service class matures, operators cross-sell cloud storage and cybersecurity, amplifying lifetime value per subscriber and supporting the structural swing toward data-centric earnings within the Chad telecom market.

By End-User: Enterprise Momentum Outpaces Consumer Volume

Consumers still produced 70.19% of 2024 turnover yet logged a milder 5.66% CAGR, reflecting price sensitivity among low-income rural households. Enterprises booked 29.81% of receipts but will accelerate at 6.15% through 2030 as multinationals, NGOs, and ministries demand SLA-backed links. The World Bank programme targets 40,000 trainees in digital skills, broadening the corporate talent pool that depends on high-availability broadband.

Corporate ARPU surpasses retail by more than 4 x thanks to value-added layers spanning MPLS, cloud peering, and managed security. Operators bundle Microsoft 365 and AWS outposts, capturing incremental share of ICT budgets. As oil-field contractors digitise asset telemetry and banks roll out API-driven mobile apps, enterprise slices will deepen, raising the overall revenue mix contributed by businesses in the Chad telecom market.

Geography Analysis

Urban corridors led by N’Djamena, Moundou, and Sarh generated more than 62% of Chad telecom market revenue in 2024, supported by 4G density averaging 15 macro sites per 10,000 inhabitants. Rural prefectures across the Sahel belt lag on both coverage and usage, yet they hold the largest unconnected population block of 4.5 million people targeted by the Digital Transformation Project. Operators prioritize highway fiber routes that trunk traffic back to submarine landing stations in Cameroon, shedding international transit costs by up to 40%.

Second-tier towns such as Abeche and Bongor are next in the rollout hierarchy because each hosts provincial administrations shifting payroll processing online. Solar-hybrid power systems are being piloted to cut diesel spend by 35%, improving operating economics in off-grid cells. The World Bank’s rural broadband subsidy regime underwrites passive-infrastructure co-location, encouraging both incumbents to blanket sparsely inhabited zones without duplicative towers.

Northern Tibesti and Borkou prefectures remain coverage dark-spots because security logistics complicate site maintenance. Starlink’s low-earth-orbit beams may backhaul traffic from new VSAT hubs, allowing operators to provision voice-over-satellite overlays until microwave rings extend north. Over 2026-2028 the geography mix should tilt as rural penetration rises in response to smartphone cost declines and cash-transfer programmes credited through mobile wallets, enlarging the nationwide customer base of the Chad telecom market.

Competitive Landscape

Moov Africa Chad closed 2024 with 53% subscriber share, while Airtel Chad held 47%, establishing a tightly held duopoly in the Chad telecom market. Both exploit scale benefits to negotiate vendor pricing and co-site leases, yet differentiation hinges on network experience scores rather than tariffs. Airtel’s early 4G launch captured high-usage youth in the capital, prompting Moov to accelerate LTE rollouts at 1,800 MHz.

Salam Mobile, a subsidiary of state-owned Sotel, secured spectrum blocks and is prepping a 2026 commercial debut that could under-price incumbents on entry-level data packs. The government’s plan to sell 60% of Sotel is expected to bring in a strategic investor with cash for rapid network build and potentially bundled satellite-fiber offers. Starlink’s license awards the first non-terrestrial competitor franchise, aiming initially at NGOs, mining camps, and high-ARPU households beyond fiber corridors.

Strategic alliances shape competitive arsenals. Airtel partners with Huawei for cloud core and with Mastercard for wallet interoperability, whereas Moov integrates Orange Money rails to drive fintech stickiness. Both incumbents lobby for further tax relief and right-of-way reforms to lower capex. Consolidated cashflow finances ongoing 4G densification and trial 5G non-standalone cells, underscoring technology leadership as the main weapon in the Chad telecom market.

Chad Telecom MNO Industry Leaders

Airtel Chad

Moov Africa Chad

Salam Mobile (Sotel)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Airtel upgraded 30 rural 3G sites to 4G using solar-powered radio units.

- December 2024: MTN Group earmarked USD 300 million over three years for Central African network upgrades.

- November 2024: Starlink obtained final frequency clearance to launch satellite broadband in Chad.

Chad Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

Which service category generates the most revenue?

Data services lead with 50.29% revenue share in 2024 and sustain the fastest growth at 5.86% CAGR through 2030.

Who are the main operators?

Moov Africa Chad and Airtel Chad jointly hold the entire mobile segment, with Salam Mobile preparing market entry and Starlink entering satellite broadband in 2025.

What is the growth outlook for enterprise connectivity?

Enterprise revenue is forecast to rise at 6.15% CAGR, outpacing consumer gains as public-sector digitization drives corporate network demand.

How will satellite broadband influence the market?

Starlink’s 2025 launch will supply high-throughput links to underserved regions, enhancing rural coverage and injecting new competitive pressure on terrestrial operators.

Page last updated on: