Iraq Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

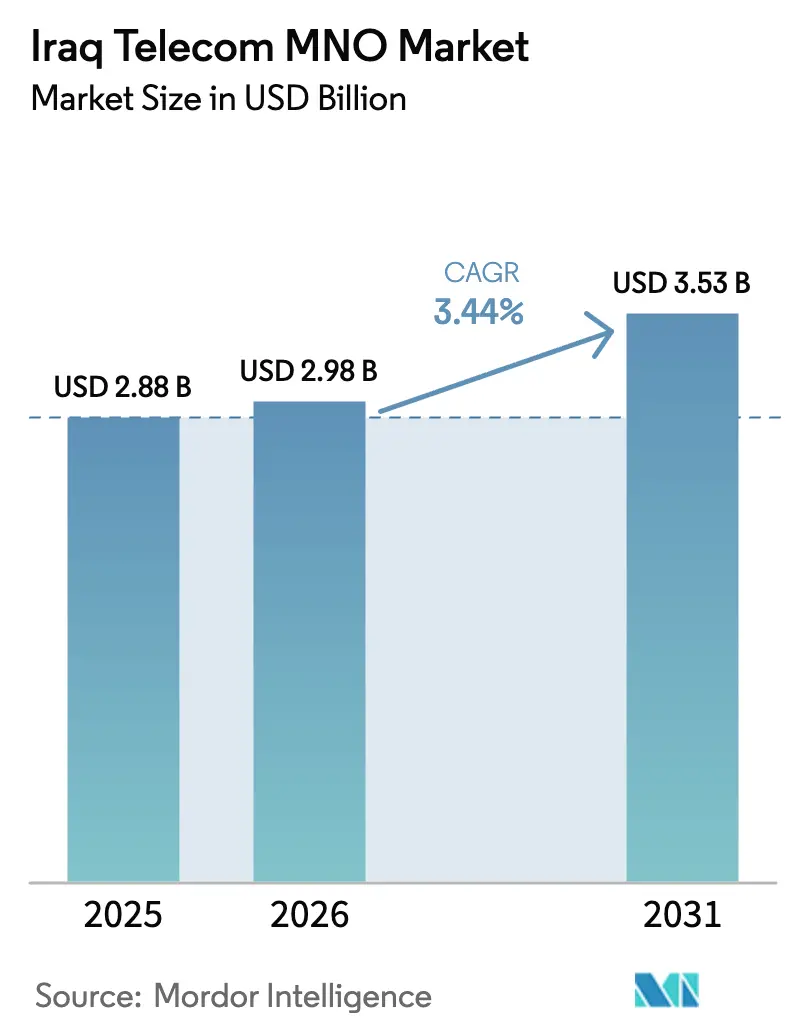

| Base Year Market Size (2025) | USD 2.88 Billion |

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

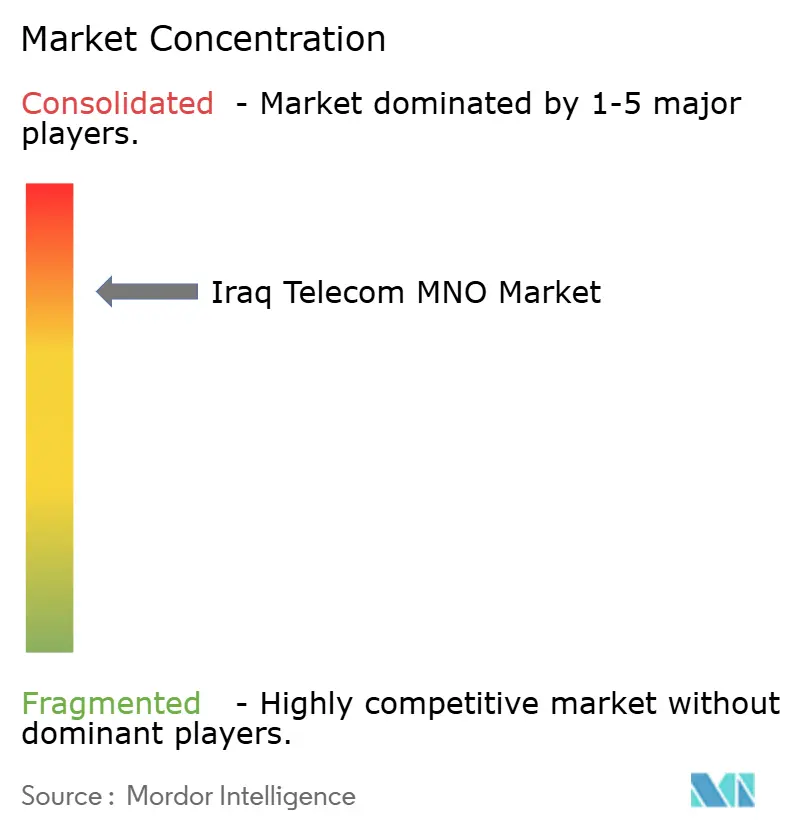

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq Telecom MNO Market Analysis by Mordor Intelligence

The Iraq Telecom MNO Market size is expected to grow from USD 2.88 billion in 2025 to USD 2.98 billion in 2026 and is forecast to reach USD 3.53 billion by 2031 at 3.44% CAGR over 2026-2031.

This measured expansion is underpinned by nationwide digital-transformation agendas, expanding 4G coverage, and the government’s move to launch a state-owned National Mobile Company in March 2025. Mobile penetration has reached 103% while internet penetration has climbed to 81.7%, signaling a maturing but still growth-oriented environment. Intensifying competition, swift device affordability, and expanding international bandwidth from the forthcoming Fiber in Gulf subsea cable are expected to support higher data traffic and average revenue per user. Operators are modernizing transport networks with E-band microwave links to alleviate longstanding backhaul bottlenecks. Enterprise digitization across the oil, banking, and public sectors is opening premium revenue streams, while security risks and volatile fee regimes continue to temper network-expansion ambitions.

Key Report Takeaways

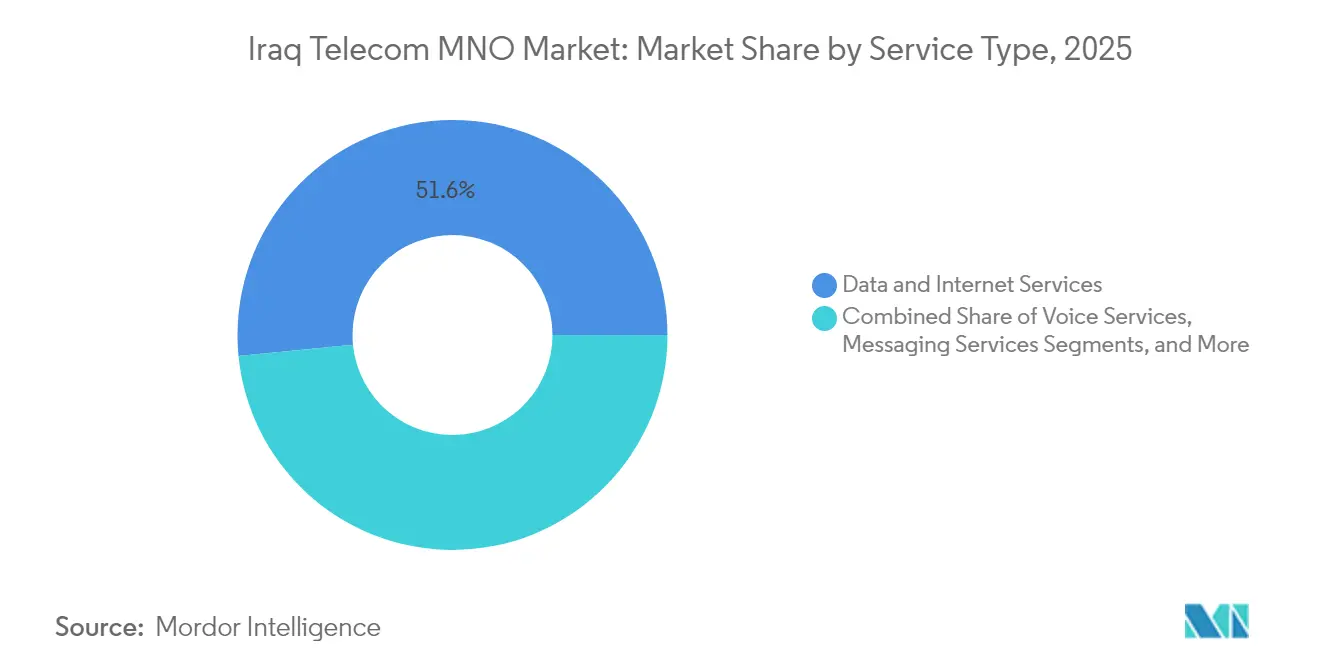

- By service type, data and internet services led with 51.55% revenue share in 2025; IoT and M2M services are projected to grow at a 3.51% CAGR to 2031.

- By end user, the consumer segment held 83.20% of the Iraq Telecom MNO market share in 2025, while the enterprise segment is advancing at a 4.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iraq Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive mobile-data usage and smartphone adoption | +1.2% | Baghdad, Basrah, Erbil | Short term (≤ 2 years) |

| 4G license renewals and planned 5G spectrum auction | +0.8% | Major cities nationwide | Medium term (2-4 years) |

| Government-backed national fiber backbone rollout | +0.6% | Nationwide | Long term (≥ 4 years) |

| Enterprise digitization and cloud connectivity demand | +0.7% | Oil-producing regions | Medium term (2-4 years) |

| Private-LTE / IoT networks for oil-field automation | +0.4% | Southern oil fields, Kurdistan | Long term (≥ 4 years) |

| Rapid eSIM uptake via super-apps and digital channels | +0.3% | Urban tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive Mobile-Data Usage and Smartphone Adoption

Average mobile download speed reached 36.39 Mbps in 2025, up 25.1% year over year, and this uplift directly boosted data-plan subscriptions and ARPU [1]Speedchecker Ltd., “Sawad Land Speed Test,” broadbandspeedchecker.co.uk. Affordable Android devices priced below USD 100, together with broader 4G coverage, have fostered mass-market migration from basic voice to data-centric bundles. Zain Iraq’s three-year microwave-modernization program with Nokia is easing spectral congestion by shifting heavy backhaul loads onto high-capacity E-band links. Higher network quality is accelerating video streaming, social media, and emerging AR/VR usage, which in turn justifies further investment in transport and RAN upgrades. Digital payment adoption, now 48.5% of all transactions, adds another layer of always-on data demand as consumers rely on banking apps and e-commerce platforms [2]International Journal of Religion, “Digital Banking Impact,” ijor.org . This virtuous cycle positions data traffic as the chief revenue catalyst across the Iraq Telecom MNO market.

4G License Renewals and Planned 5G Spectrum Auction

The Communications and Media Commission is finalizing 5G auction terms that will allocate 3.5 GHz and millimeter-wave blocks, reshaping competitive hierarchies among Iraq’s three private operators and the forthcoming National Mobile Company. Asiacell already operates 8,201 LTE sites nationwide, giving it an upgrade-ready grid for early non-stand-alone 5G launches. Market observers expect bidding conditions to include population-coverage thresholds that compel faster rural roll-outs. Technical studies conducted in Najaf validated 28 GHz propagation feasibility, confirming that spectrum assignments, rather than engineering constraints, will dictate launch timelines. A more rigorous renewal process also raises spectrum fees, nudging operators toward revenue-diversification strategies such as private networks and IoT services.

Government-Backed National Fiber Backbone Rollout

The National Investment Commission has earmarked IQD 39,582.1 billion for telecoms infrastructure, with fiber routes prioritized to connect governorates and industrial zones. Private players such as iQ Networks already retail FTTH packages between IQD 39,000 and IQD 49,000, demonstrating latent demand for high-speed fixed connectivity. The 720 Tbps Fiber in the Gulf cable, due Q4 2027, will expand international capacity by multiples, reducing transit costs and positioning Iraq as a traffic transit hub between Asia and Europe. A resilient backbone also lessens over-reliance on microwave backhaul, enabling higher 4G and future 5G cell-throughputs, especially in secondary cities.

Enterprise Digitization and Cloud Connectivity Demand

Oil-field operators are installing IoT sensors for real-time pipeline monitoring, predictive maintenance, and remote-guided drilling, generating continuous telemetry that requires dedicated, low-latency uplinks. Banking digitization has reached an inflection point with electronic payments at 48.5% of transaction value, driving the need for secure, high-availability connections. Government e-services mandates add further bandwidth demand, particularly for identity verification and cross-agency data exchange. Enterprise ARPU runs three to five times higher than consumer levels, offering operators a lucrative hedge against slowing subscriber growth. Local systems integrators, such as E2NEXT, are emerging to bundle managed connectivity, cloud migration, and cybersecurity with mobile private networks, expanding the Iraq Telecom MNO market’s enterprise addressable revenue base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent security risks to outside-plant assets | -0.9% | Rural and border areas | Long term (≥ 4 years) |

| Volatile tax and regulatory fee regime | -0.6% | Nationwide | Medium term (2-4 years) |

| Microwave-heavy backhaul limiting 4G/5G capacity | -0.4% | Rural, secondary cities | Medium term (2-4 years) |

| Low banking penetration slowing digital payments | -0.3% | Rural, low-income areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Security Risks to Outside-Plant Assets

Operator assets remain vulnerable to vandalism, fuel theft, and sabotage. TASC Towers applies multiple layers of perimeter surveillance and rapid-response protocols, yet insurance costs still exceed regional norms, inflating overall site-opex. Field technicians often navigate fragmented security jurisdictions, adding delays to fault repairs and inhibiting rural coverage expansion. Fiber runs through remote areas face risk from both accidental construction damage and deliberate tampering, forcing duplicated trenching and route diversity that raise capital requirements.

Volatile Tax and Regulatory Fee Regime

The Communications and Media Commission’s new influencer-registration fees, ranging from IQD 250,000 to IQD 1,000,000, underscore the unpredictability of ancillary levies that can quickly erode margins for value-added services [3]Dana Taib Menmy, “Iraq imposes sweeping fees on influencers,” The New Arab, newarab.com. Corporate tax remains 15%, but import duties on telecom gear fluctuate with fiscal needs, complicating capex planning. Outstanding government receivables, Asiacell at IQD 121 trillion and Zain Iraq above USD 4 million, tighten operator cash flows and may delay 5G investment schedules. Currency volatility between the dinar and vendors’ billing currencies further clouds budgeting accuracy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-Led Revenue Transformation

Data and Internet services captured 51.55% of the Iraq Telecom MNO market share in 2025, reflecting the traffic tilt toward video streaming, social media, and cloud applications. IoT and M2M services are set to record the fastest 3.51% CAGR on the back of private LTE deployments in oil fields and smart-city pilots around Baghdad and Erbil. Operators package OTT video and PayTV as optional add-ons to defend against commoditization, yet rampant piracy through illicit IPTV boxes still suppresses formal revenue. Enterprise and wholesale products command premium pricing owing to strict service-level agreements and low latency needs, and they increasingly bundle cloud-connect gateways with secure VPN overlays.

Operators have launched eSIM support via in-app activation, a move that reduces physical-SIM logistics and heightens cross-border tourist uptake. Prepaid bundles remain dominant but are gradually giving way to post-paid plans, particularly among young professionals drawn to handset-financing offers. Meanwhile, legacy SMS volumes continue to decline as over-the-top messaging displaces P2P texts. Voice revenue erosion is cushioned by inbound international calling charges from the Iraqi diaspora, though traffic is shifting to app-based voice over IP. In rural governorates, basic voice still plays an essential role where smartphone affordability and literacy levels lag urban standards.

By End User: Enterprise Momentum Intensifies

Enterprise accounts are forecast to expand at a 4.01% CAGR, supported by upstream shale and downstream petrochemical investments that demand rugged, mission-critical connectivity. Oil majors require redundant backhaul and private-LTE slices to monitor field instrumentation and automate wellheads, with some pilots already transmitting gigabytes of telemetry daily. Banks and fintech operators are adopting multi-factor authentication and real-time fraud monitoring, lifting bandwidth per-branch demand above 50 Mbps. Government agencies are shifting citizen services, such as passport renewals, onto digital channels, requiring secure government clouds tied to operator data centers.

The consumer segment, despite its 83.20% revenue share in 2025, faces decelerating growth as penetration is already above 100%. However, ARPU uplift remains achievable through content bundles, device financing, and lifestyle super-apps that integrate ride-hailing and micro-lending. The state-backed National Mobile Company is expected to target the mass market with aggressive pricing, putting pressure on incumbent consumer margins but also sparking service-innovation cycles.

Geography Analysis

Baghdad, Basrah, and Erbil jointly generate nearly one-third of national telecom revenue, driven by corporate headquarters, diplomatic missions, and affluence that support premium data bundles. Basrah’s oil terminals draw sustained enterprise connectivity investment, making it the leading non-capital governorate by telecom spend. Kurdistan Region benefits from a decade-long corporate-tax holiday, spurring faster deployment of LTE-Advanced and igniting competitive tariff promotions. Rural provinces such as Anbar and Diyala lag in both coverage and speed owing to security constraints and sparse population density that dampen return on capex.

The Iraq Telecom MNO market size attributable to the Baghdad metro is projected to rise 4.15% CAGR through 2031, underpinned by data-center expansions and government-cloud procurement. Southern governorates enjoy a parallel tailwind from brownfield refinery upgrades that trigger large-scale IoT deployments. Northern border areas remain transmission bottlenecks until microwave backhaul is swapped for fiber spurs, a process tied to the national backbone timeline. Once the Fibre in Gulf cable lands in Q4 2027, wholesale transit prices are expected to fall sharply, improving margins on international bandwidth resold to ISPs and hyperscalers.

Power-supply instability remains universal, with only 12 hours grid electricity per day, forcing operators to maintain diesel generators whose fuel logistics can raise site opex by 25%. In the most remote towns, solar-hybrid power systems are undergoing trials, but capital costs remain high. Under universal-service rules, operators must achieve 90% population coverage by 2028; compliance will depend on a mix of low-band spectrum, tower-sharing, and subsidy allocations.

Competitive Landscape

The Iraq Telecom MNO market is presently shared among Zain Iraq, Asiacell, and Korek Telecom, though the March 2025 decree establishing a National Mobile Company will introduce a new fourth player with sovereign backing. Zain Iraq registered USD 1.1 billion revenue in 2024 and 11% year-over-year growth, bolstered by a network-modernization pact with Nokia that inserted 3,000 high-capacity microwave hops, raising average cell throughput by 35%. Asiacell leverages its 8,201 LTE sites to advertise “deep-indoor” coverage and has piloted 5G non-stand-alone services for enterprise clients in Erbil’s oil-service corridor. Korek Telecom differentiates via Kurdish language content bundles and partnerships with regional OTT providers.

Strategic plays center on enterprise digitization. Zain Iraq and Schlumberger are co-designing a managed private-LTE bundle for well-site automation, while Asiacell is deploying multi-edge computing appliances in Baghdad to serve low-latency cloud workloads. Operators are also hunting new revenue in fixed wireless access, bundling 4G routers with unlimited data to address unserved households that lack fiber. Nokia supplies E-band microwave, Huawei provides massive-MIMO radios, and Ericsson frames initial standalone 5G lab trials.

An adjacent competitive arena involves roughly 350 autonomous-system ISPs that manage limited transit adjacencies; consolidation is expected as mobile operators bundle fixed broadband to upscale ARPU. Wholesale lease-of-tower arrangements with TASC Towers and IHS Towers aim to accelerate rural coverage while trimming capex. Regulatory spectrum fees and universal-service levies remain top cost variables and influence pricing elasticity.

Iraq Telecom MNO Industry Leaders

Asiacell Communications PJSC

Zain Iraq (Zain Group)

Korek Telecom Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Iraqi Cabinet approved a state-owned National Mobile Company to compete with Asiacell, Zain Iraq, and Korek Telecom.

- March 2025: Communications and Media Commission introduced social-media-influencer registration fees between IQD 250,000 and IQD 1,000,000.

- September 2024: Nokia signed a three-year accord with Zain Iraq to modernize microwave transport using E-band solutions.

Iraq Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The telecom MNO market includes in-depth trend analysis based on connectivity, such as fixed networks, mobile networks, and telecom towers. Several factors, including an increasing demand for 5G, are likely to drive the adoption of telecom services.

Iraq telecom MNO market is segmented by services (voice services (wired and wireless), data and messaging services, OTT, and PayTV services). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Iraq Telecom MNO market?

The market is valued at USD 2.98 billion in 2026.

How fast is the market growing?

The market is projected to expand at a 3.44% CAGR through 2031.

Which service type leads revenue?

Data and Internet services command 51.55% of 2025 revenue.

Why is enterprise demand rising?

Oil-field automation, banking digitization, and government e-services require high-quality, secure connectivity.

What major regulatory change occurred in 2025?

The government created a state-owned National Mobile Company and introduced influencer-registration fees.

How will the Fibre in Gulf cable affect Iraq?

It will add 720 Tbps of capacity, lower transit costs, and position Iraq as a regional data hub by late 2027.

Page last updated on: