Lebanon Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

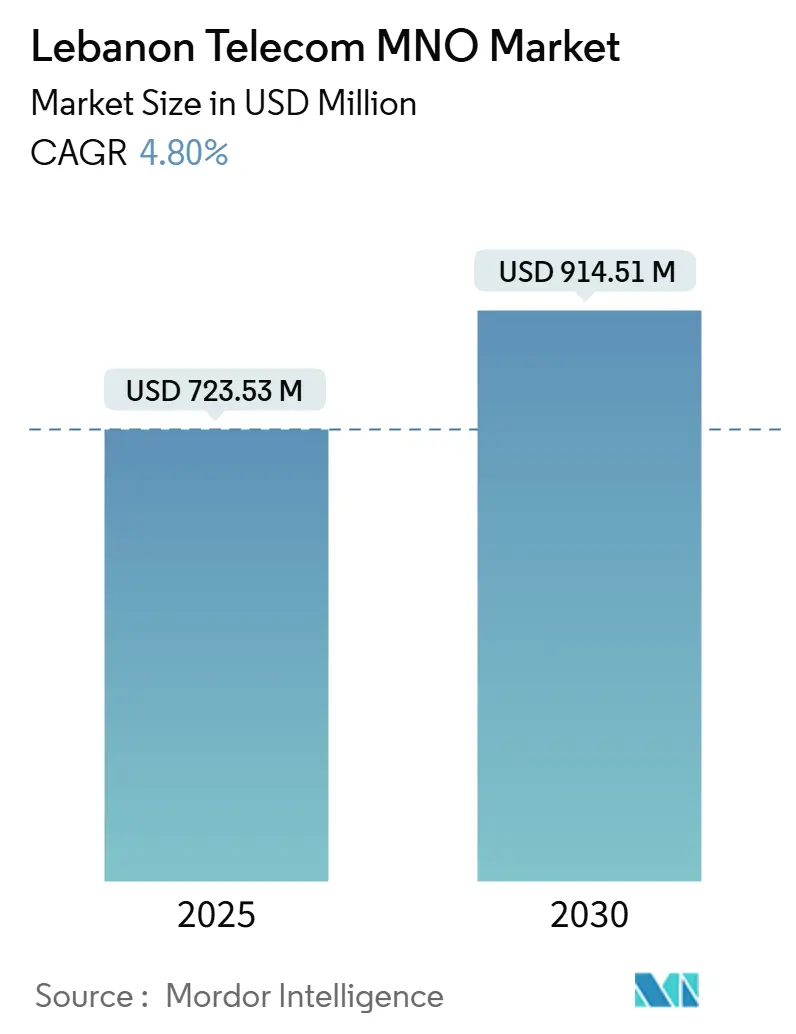

| Market Size (2025) | USD 723.53 Million |

| Market Size (2030) | USD 914.51 Million |

| Growth Rate (2025 - 2030) | 4.80% CAGR |

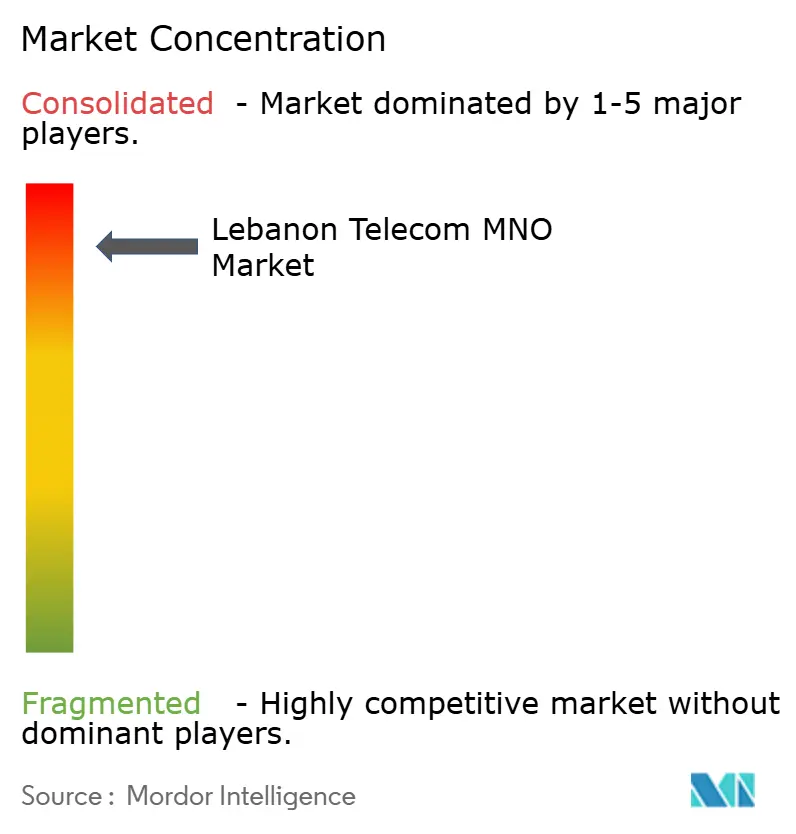

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lebanon Telecom MNO Market Analysis by Mordor Intelligence

The Lebanon Telecom MNO Market size is estimated at USD 723.53 million in 2025, and is expected to reach USD 914.51 million by 2030, at a CAGR of 4.80% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 5.5 million subscribers in 2025 to 7 million subscribers by 2030, at a CAGR of 5.06% during the forecast period (2025-2030).

Resilient demand for mobile data, a sharp pivot by enterprises toward digital applications, and the progressive rollout of national fiber backhaul underpin this trajectory despite currency shocks and chronic power-grid instability. State support for broadband, successful 5G testbeds, and the commercial urgency of cloud-connected applications are widening revenue opportunities even as hyper-inflation compresses discretionary consumer spend. The sector’s moderate growth profile illustrates how technological upside is being tempered by economic headwinds, infrastructure resilience costs, and a duopolistic market structure that limits disruptive competition. Operators are therefore prioritizing enterprise service diversification, diesel-powered network hardening, and dollar-denominated pricing to defend margins in a turbulent macroeconomic climate.

Key Report Takeaways

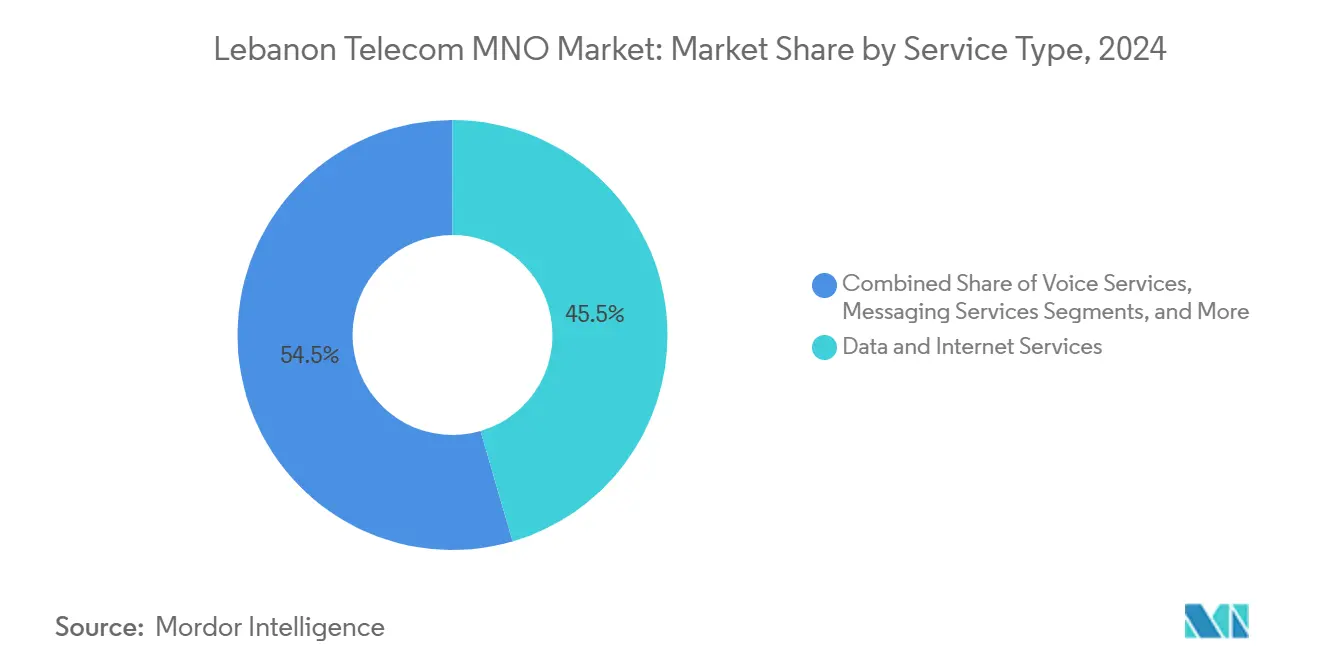

- By service type, data and Internet services held 45.48% of Lebanon Telecom MNO market share in 2024, while IoT and M2M services are projected to post the fastest 4.89% CAGR through 2030.

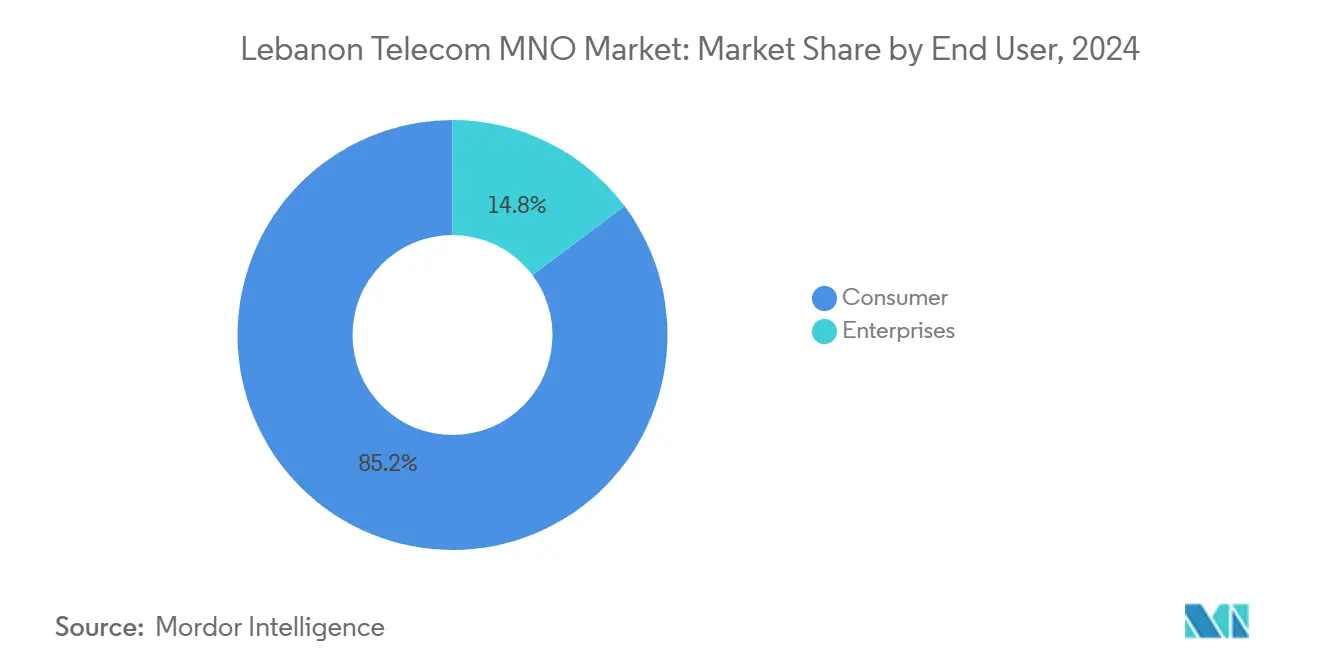

- By end user, the consumer segment commanded 85.24% share of the Lebanon Telecom MNO market size in 2024, whereas the enterprise segment is advancing at a 5.48% CAGR to 2030.

Lebanon Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile data–hungry population streaming-led traffic boom | +1.2% | Beirut and Mount Lebanon urban clusters | Short term (≤ 2 years) |

| State-funded FTTx roll-out under “Lebanon Broadband 2025” | +0.8% | Nationwide, urban first | Medium term (2-4 years) |

| 5G spectrum roadmap and 3.5 GHz testbeds | +0.6% | Major cities | Medium term (2-4 years) |

| Enterprise digitalization surge (cloud, SD-WAN, IoT) | +0.9% | Commercial districts nationwide | Short term (≤ 2 years) |

| Monetization of diaspora voice/data traffic | +0.4% | International gateway routes | Long term (≥ 4 years) |

| Dollar-denominated mobile-money solutions | +0.7% | Under-banked regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mobile Data–Hungry Population Streaming-Led Traffic Boom

Lebanon’s subscribers have shifted from voice-centric usage toward always-on data consumption, with streaming platforms now viewed as essential utilities for news, entertainment, and social connection during periods of restricted physical mobility. [1]Freedom House, “Lebanon – Freedom on the Net 2024,” freedomhouse.org Operators with robust 4G coverage experience peak-hour traffic density that pushes existing spectrum limits, prompting accelerated radio-access upgrades across Beirut’s dense districts. The willingness of many households to pay dollar-linked tariffs signals pricing elasticity for reliable data quality, an encouraging indicator for ARPU growth despite the broader inflation squeeze. [2]Philippe Hage Boutros, “Steep increases in mobile telephone rates commence Friday,” today.lorientlejour.com High-definition video and real-time gaming also influence backhaul investment priorities, concentrating capex on sites where evening congestion threatens quality of experience. The resulting focus on capacity expansion in urban corridors strengthens the competitive positioning of incumbents that hold the most contiguous spectrum blocks.

State-Funded FTTx Roll-Out Under “Lebanon Broadband 2025” Roadmap

The USD 300 million national fiber initiative aims to deliver a minimum of 50 Mbps access speeds, alleviating a copper bottleneck that historically limited mobile backhaul and enterprise connectivity. [3]OGERO, “Deployment Plan,” ogero.gov.lb OGERO’s deployment schedule favors Beirut, Sidon, and Tripoli in early phases, improving the economics of small-cell densification and 5G readiness for Alfa and Touch. Fiber availability is expected to cut microwave reliance, reduce latency for cloud services, and unlock revenue-accretive SD-WAN propositions for multi-site businesses. International cable redundancy upgrades further support the policy goal of positioning Lebanon as a digital services corridor for the Levant region. Successful execution, however, hinges on uninterrupted funding amidst fiscal austerity and the protection of outside-plant assets from cable theft incidents that have escalated since late 2023.

5G Spectrum Roadmap and Successful 3.5 GHz Testbeds by Alfa and Touch

Both operators demonstrated peak speeds above 1 Gbps during 3.5 GHz field trials, confirming radio-layer readiness for enterprise-grade fixed-wireless access and ultra-reliable low-latency applications. The Telecommunications Regulatory Authority’s draft allocation table harmonizes Lebanon with ITU band-n78 standards, enabling cheaper equipment procurement and seamless roaming for multinational customers. Commercial launch timelines are synchronized with fiber backhaul milestones because dense 5G cell grids require high-capacity links unachievable on legacy copper. Initial monetization is expected to target private campuses, media production hubs, and high-rise business districts where premium tariffs can justify rollout costs ahead of mass-consumer adoption. Competitive pressure from Gulf markets, already iterating toward 5.5 G, intensifies the urgency for timely Lebanese deployment to preserve regional relevance.

Enterprise Digitalization Surge (Cloud, SD-WAN, IoT)

Business customers are investing in automation, analytics, and cloud migration as cost-containment imperatives outweigh capital scarcity. [4]MDPI, “The Impact of AI Assimilation on Firm Performance in SMEs,” mdpi.com Telecom operators are natural connectivity partners, bundling multi-edge cloud access, managed SD-WAN, and IoT platforms that integrate asset tracking and predictive maintenance. The Middle East cloud services opportunity, sized at USD 183 billion by 2030, assigns telcos an estimated 6% value capture through interconnect and security overlays. Lebanese SMEs in logistics, light manufacturing, and facility management are early adopters, seeking remote visibility to mitigate labor shortages and ensure continuity during power outages. This enterprise momentum supports ARPU uplift and dilutes reliance on price-sensitive prepaid segments that dominate headline subscriber totals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-inflation shrinking discretionary spend | -1.8% | Rural and low-income urban zones | Short term (≤ 2 years) |

| Power-grid failures raising diesel OPEX | -1.1% | Remote base-station clusters | Short term (≤ 2 years) |

| Escalating copper and fiber theft | -0.6% | Perimeter and low-security areas | Medium term (2-4 years) |

| Telecom-engineer brain drain | -0.4% | National technical workforce | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyper-Inflation Shrinking Discretionary Telecom Spend

The Lebanese pound has lost 94% of its value since 2019, forcing households to re-prioritize spending toward food, fuel, and healthcare. Dollar-denominated tariff structures introduced in 2022 preserved operator revenues but widened affordability gaps for prepaid users whose wages remain pound-pegged. Internet penetration slipped 2.6 percentage points between January 2023 and January 2024, signaling demand elasticity under extreme currency volatility. Operators are responding with smaller data-bundle denominations and more aggressive off-peak promotions, though these tactics only partially offset churn among low-income subscribers. The imbalance nudges strategic focus toward enterprise and high-value diaspora traffic where pricing power remains intact.

Power-Grid Failures Raising Diesel OPEX and Service Outages

National electricity supply averages fewer than 4 hours daily, compelling telcos to run diesel generators across thousands of sites at an annual fuel bill that now exceeds USD 42 million. Persistent outages degrade call completion rates and data throughput, undermining premium-service propositions. Higher-power 5G radios and cooling systems will deepen this exposure unless operators accelerate solar and hybrid energy retrofits, which in turn require upfront capital not easily accessible under sovereign debt distress. Partial solar rollouts have multiplied eightfold since 2020, yet coverage still falls short of the 70 MWh daily energy demand of the macro-radio network. The reliability challenge therefore constrains both customer experience and the pace of network modernization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and Internet services accounted for 45.48% of Lebanon Telecom MNO market share in 2024, underscoring their centrality to revenue generation as voice and SMS revenues contract. IoT and M2M services are posting a 4.89% CAGR, reflecting enterprise efforts to embed connectivity in asset management and logistics chains. The Lebanon Telecom MNO market size attributable to data packages is projected to reach USD 423 million by 2030, supported by streaming-led demand peaks and 5G fixed-wireless access pilots. Voice services continue to monetize the diaspora’s need for international calling, while messaging revenues erode in favor of OTT alternatives operating over data pipes. Operators are bundling OTT video with premium data tiers in an effort to capture incremental ARPU and curb subscriber churn.

The rapid uptake of IoT platforms mirrors Lebanon’s wider enterprise efficiency narrative. Fleet operators are installing telematics to cut fuel usage; real-estate managers deploy smart meters to monitor generator diesel levels and avoid outages. These use cases validate premium connectivity even where macro conditions depress consumer spending. Other services, such as international roaming and virtual private network resale, offer niche margins but remain contingent on regional travel patterns and regulatory clarity around data localization.

By End User: Consumer Dominance Masks Enterprise Growth Potential

The consumer segment contributed 85.24% of Lebanon Telecom's MNO market size in 2024 as prepaid SIM volumes dwarf corporate account numbers. Nevertheless, enterprise accounts are expanding at a 5.48% CAGR, a faster clip than any other customer class, driven by cloud migration, SD-WAN uptake, and IoT adoption. The Lebanon Telecom MNO market share derived from enterprises is anticipated to climb to 20% by 2030 as organizations seek always-on connectivity to maintain competitiveness amid regional peers with more diversified infrastructure.

Operators are tailoring enterprise offers that integrate managed security, redundant fiber loops, and service-level agreements calibrated to mitigate power disruptions. Meanwhile, the consumer segment faces rising price sensitivity, compelling telcos to structure micro-bundle data plans denominated in sub-1 USD equivalents to retain lower-income users without eroding overall revenue per gigabyte. This bifurcated strategy allows operators to pursue premium growth where willingness to pay is proven while defending volume in the wider mass market.

Geography Analysis

Lebanon Telecom MNO market activity is naturally national in scope, yet economically concentrated along the coastal urban strip from Tripoli through Beirut to Tyre, where 70% of GDP is generated. Population coverage stands at 97.86% but the quality of service differs markedly between top-tier cities and mountainous hinterlands. Average download speeds of 25.96 Mbps in Beirut contract to under 10 Mbps in the Bekaa Valley, reflecting both terrain challenges and the lower commercial incentive to densify rural cell grids. This discrepancy frames an opportunity for 5G fixed-wireless access as a rural broadband substitute, assuming backhaul and power-supply bottlenecks can be overcome.

International connectivity is anchored by three submarine cable landings that provide redundancy for diaspora voice, data traffic, and emergency routing. Conflict-related damage to 175 transmission sites in November 2024 highlighted vulnerability hot-spots and catalyzed emergency satellite contingency planning. Alpha and Touch are evaluating Starlink backhaul in remote zones following early-stage discussions with SpaceX in June 2025, a potential hedge against both fiber sabotage and protracted grid failure.

From a regulatory vantage, national spectrum management and backbone ownership mean regional policy harmonization is less influential than in larger multi-province markets, yet Lebanon still tracks ITU guidelines to simplify roaming for its sizeable expatriate base. Overall, geography-linked deployment economics compel operators to weight capex toward high-density districts while leveraging wholesale rural tower sharing agreements to lower unit costs in low-ARPU zones.

Competitive Landscape

Lebanon Telecom MNO market remains a textbook duopoly: Alfa and Touch, each under state-directed management contracts. This structural concentration allows coordinated tariff adjustments such as the simultaneous switch to USD-pegged pricing in mid-2022. Competitive differentiation, therefore, gravitates to network reliability, customer-care responsiveness, and the breadth of enterprise service catalogues rather than price wars.

Infrastructure resilience is a strategic focus; both operators maintain diesel and battery reserves across critical base-station clusters and are selectively deploying solar hybrid power to temper OPEX exposures. On the technology front, Alfa’s 5G proof-of-concept in Hamra and Touch’s Grand Serail trial demonstrate parallel intentions to commercialize sub-6 GHz 5G once backhaul capacity is adequate. Partnership models are expanding: Alfa collaborates with local data-center providers on edge-compute nodes, while Touch integrates multinational SD-WAN vendors to enhance enterprise offers.

The creation of a dedicated Ministry for Information Technology and Artificial Intelligence in February 2025 introduces a potential reform vector by separating policy oversight from incumbent operational interests. International entrants remain barred from direct spectrum ownership, yet the government is exploring wholesale MVNO frameworks and satellite backhaul accords to diversify service availability in rural districts. For now, however, the market continues to reward scale and state affiliation over disruptive new entrants.

Lebanon Telecom MNO Industry Leaders

Alfa

Touch

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Lebanon established its first Ministry for Information Technology and Artificial Intelligence, signaling heightened policy attention on telecom-driven economic recovery.

- November 2024: Regional conflict damaged 175 transmission sites, causing an estimated USD 67 million loss and temporary service outages.

- August 2024: The government approved emergency internet contingency plans amid submarine-cable disruption fears, including conditional Starlink licensing for disaster scenarios.

Lebanon Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

Which service category is growing fastest in the Lebanon Telecom MNO market?

IoT and M2M services are expanding at a 4.89% CAGR through 2030 as enterprises seek operational efficiency from connected assets.

How large is data and Internet revenue in Lebanese mobile service?

Data and Internet services captured 45.48% of total 2024 revenue and are projected to exceed USD 423 million by 2030.

What is the outlook for 5G deployment in Lebanon?

Commercial 5G launch is expected once national fiber backhaul reaches scale, with Alfa and Touch already completing 3.5 GHz trials that achieved 1 Gbps speeds.

How are power outages affecting mobile operators?

Chronic grid failures force extensive diesel generator use, adding USD 42 million in annual OPEX and causing intermittent service outages that dampen user experience.

Why is enterprise demand important to Lebanese mobile revenue?

Enterprise accounts are growing at a 5.48% CAGR and increasingly purchase premium cloud, SD-WAN and IoT bundles that carry higher ARPU than consumer prepaid lines.

What government initiative supports broadband expansion?

The Lebanon Broadband 2025 roadmap allocates USD 300 million for nationwide fiber-to-the-premises, targeting minimum 50 Mbps speeds and underpinning 5G readiness.

Page last updated on: