Libya Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

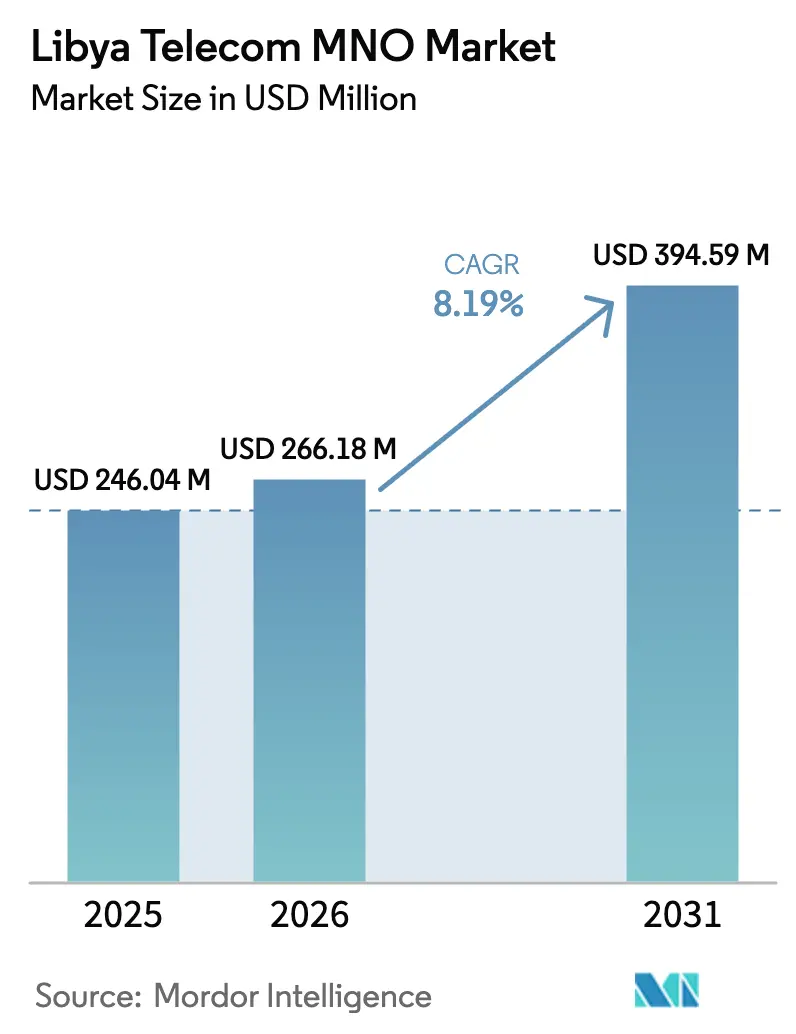

| Base Year Market Size (2025) | USD 246.04 Million |

| Market Size (2026) | USD 266.18 Million |

| Market Size (2031) | USD 394.59 Million |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

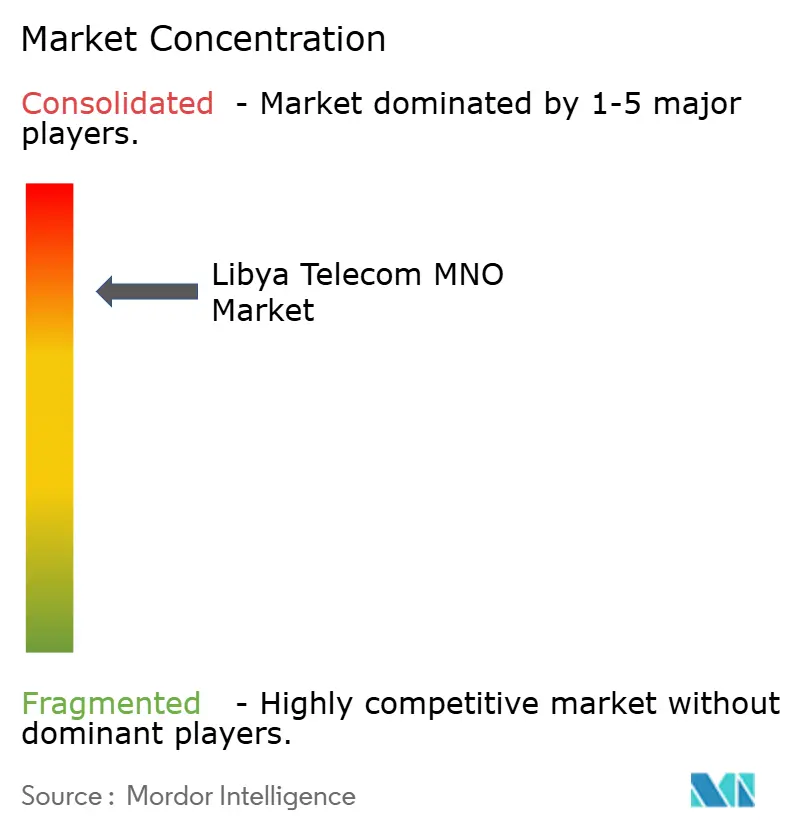

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Libya Telecom MNO Market Analysis by Mordor Intelligence

Libya Telecom MNO Market size in 2026 is estimated at USD 266.18 million, growing from 2025 value of USD 246.04 million with 2031 projections showing USD 394.59 million, growing at 8.19% CAGR over 2026-2031.

Market momentum stems from rapid 4G coverage growth, enterprise digitization across oil and public-sector verticals, and ongoing submarine-cable landings that lift international bandwidth. Elevated mobile penetration of 179.1% and internet usage reaching 89% of the population keep baseline demand resilient even when macro conditions fluctuate. Rising smartphone adoption, a prepaid-heavy customer mix, and governmental e-services together deepen data consumption, while the impending 5G transition incentivizes fresh capital allocation to radio and fiber backhaul infrastructure. Competitive differentiation hinges on service reliability during chronic power interruptions, foreign-exchange scarcity, and regional security pockets that complicate tower roll-outs. Sub-sea connectivity upgrades and European Union-backed digital programs further underline Libya’s strategic position as a North African transit node.

Key Report Takeaways

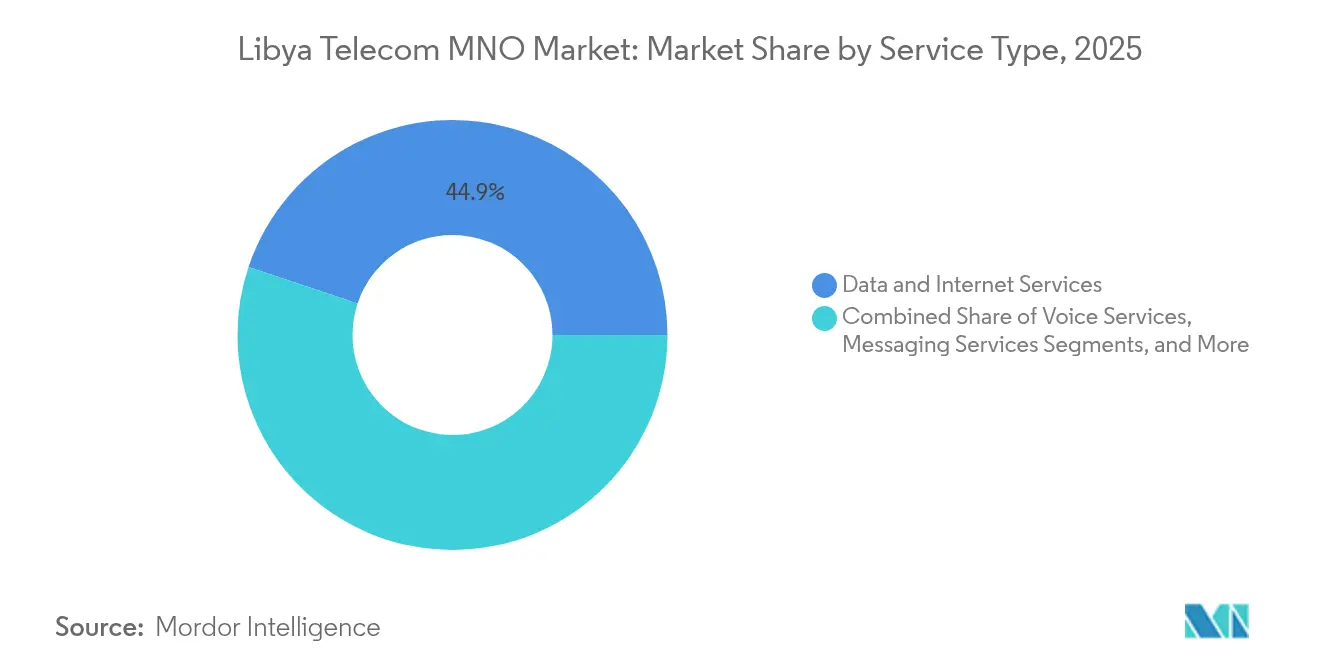

- By service type, data and internet services held 44.88% of the Libya telecom MNO market share in 2025, while OTT and PayTV are projected to register the fastest 8.41% CAGR through 2031.

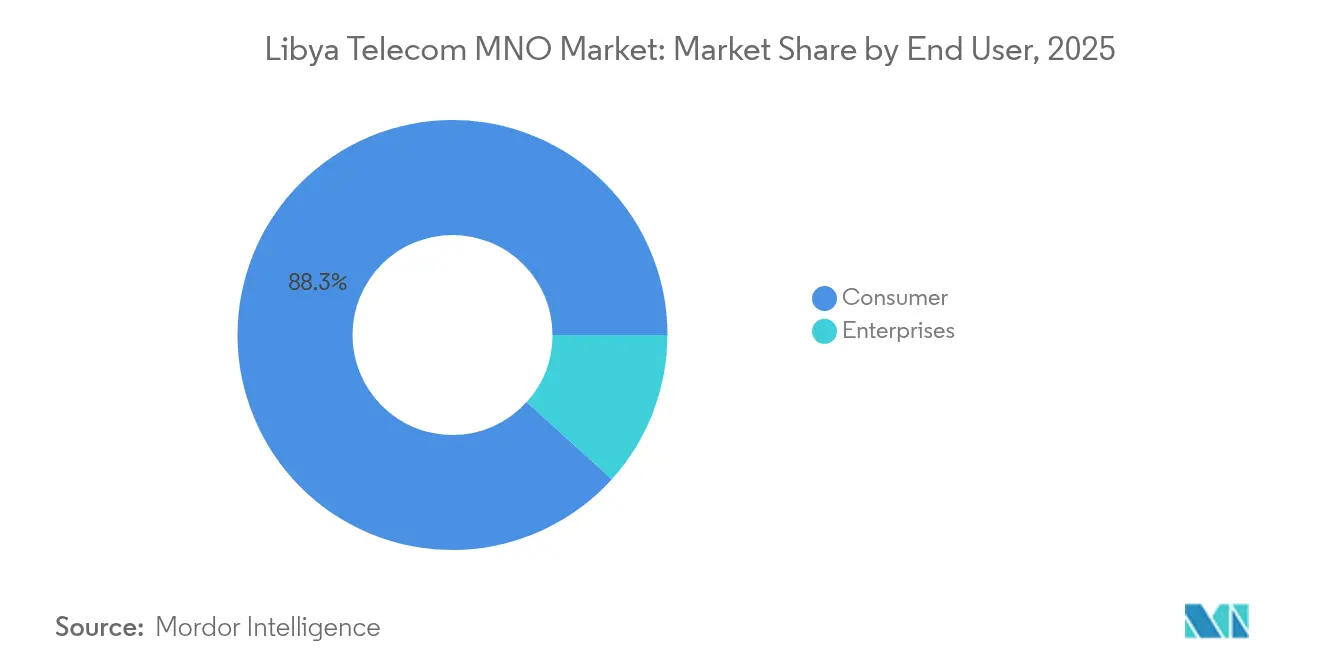

- By end user, consumers accounted for 88.29% of the Libya telecom MNO market size in 2025, and enterprises are set to grow at a 9.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Libya Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fiber backhaul roll-out in Tripoli and Benghazi | +1.2% | Tripoli and Benghazi metropolitan areas | Medium term (2-4 years) |

| Aggressive 4G/4.5G network expansion by Libyana and Al Madar | +1.8% | National, with priority in major cities | Short term (≤ 2 years) |

| Government e-services push boosting data consumption | +1.5% | National, concentrated in urban centers | Medium term (2-4 years) |

| Growing diaspora remittance apps are catalyzing mobile money | +0.9% | National, with higher adoption in rural areas | Long term (≥ 4 years) |

| Surge in foreign Oil and Gas remote-site IoT links post-2024 security pact | +1.1% | Oil and gas production regions | Short term (≤ 2 years) |

| Sub-sea cable landings turning Libya into a North-African transit hub | +0.7% | Coastal regions with international connectivity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid fiber backhaul roll-out in Tripoli and Benghazi

Broadband bottlenecks that once throttled 4G speeds are easing as Libya Telecom and Technology accelerates urban fiber deployment to projects like Bab Tarabulus. The focus on Tripoli and Benghazi matters because these two cities host roughly 40% of residents and generate a disproportionate share of network traffic. [1]Sami Zaptia, “LTT to Provide High-Speed Fibre-Optic Network to LIDCO’s Bab Tarabulus Project,” Libya Herald, LIBYAHERALD.COM Higher backhaul capacity allows operators to raise average revenue per user through HD video, cloud apps, and enterprise VPN contracts. Fiber presence also equips networks for 5G’s dense-cell architecture, protecting long-term asset value. Operators possessing larger metropolitan fiber footprints gain a measurable quality advantage that helps contain churn among premium data subscribers.

Aggressive 4G/4.5G network expansion by Libyana and Al Madar

Both mobile network operators extend LTE sites beyond coastal cores into secondary towns, closing legacy coverage gaps left by conflict-era under-investment. [2]“لمحة عن المدار الجديد,” Al Madar Al Jadid, ALMADAR.LY Strong 4G availability supports Libya’s mobile-first browsing pattern, where 63% of web sessions originate on handsets. Roll-outs now emphasize capacity rather than pure coverage, with carrier aggregation and 2100 MHz refarming that prepare spectrum for upcoming 5G pilots. Faster data plans pave the way for value-added services such as mobile money, IoT telemetry, and high-definition VoLTE, enabling operators to diversify revenue sources. The race for LTE quality also amplifies tower-sharing talks because challenging regions require cost pooling to reach commercial break-even.

Government e-services push boosting data consumption

A EUR 5 million European Union grant funds digital-identity portals, online licensing, and the Libyan Digital Lab’s innovation map. [3]Abdo M., “Libyan Digital Lab Launches Innovations Map to Foster Nationwide Digital Transformation,” Libya Update, LIBYAUPDATE.COM Citizens now rely on smartphones to obtain official transcripts and pay municipal fees, turning administrative tasks into persistent data-traffic drivers. Public-sector portals raise the relevance of reliable broadband in remote districts where physical offices are scarce, nudging households toward higher data bundles. Policy makers also publish minimum broadband standards for e-government access, indirectly mandating network quality upgrades from carriers keen to win public contracts. As digital public services mature, they generate datasets and cybersecurity requirements that open fresh enterprise-connectivity revenue streams.

Growing diaspora remittance apps are catalyzing mobile money

Libya’s far-flung expatriate community historically remitted funds through informal hawala channels. Mobile-wallet providers such as MIZA now digitize these flows, offering lower fees and real-time transaction alerts. Each remittance sparks data sessions for both sender and receiver while reinforcing stickiness to a single operator’s wallet ecosystem. Successful wallet adoption spawns add-on micro-credit, merchant QR payments, and bill-pay features that widen non-voice revenue. Rural households in particular benefit from mobile money because bank branch density remains thin outside coastal corridors, making telephony networks the default financial-services backbone.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic electricity blackouts are disrupting BTS uptime | -1.4% | National, with severe impact in southern regions | Short term (≤ 2 years) |

| FX scarcity is inflating capex and vendor payment cycles | -1.1% | National, affecting all operators | Medium term (2-4 years) |

| Fragmented militias intermittently taxing fiber routes | -0.8% | Southern and remote regions | Short term (≤ 2 years) |

| Low ARPU ceilings due to high prepaid dominance | -0.6% | National, with urban-rural variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic electricity blackouts are disrupting BTS uptime

Grid unreliability compels cell-site diesel generation that can double operating costs and shorten hardware life. Repeated outages undermine network quality, triggering spikes in dropped-call ratios and data latency that frustrate subscribers. Urban districts often restore power within hours, yet sparsely populated southern areas endure extended blackouts, widening the digital divide. [4]Logistics Cluster, “Libya – 3.4 Telecommunications,” LOGCLUSTER.ORG Operators allocate scarce batteries to revenue-dense zones, postponing rural upgrades and limiting potential enterprise solutions for mining and agriculture. Chronic power problems also slow 5G roll-outs because next-generation radios demand tighter power tolerances and larger backhaul switches.

FX scarcity is inflating capex and vendor payment cycles

After the 2021 currency devaluation, operators experienced sudden import-cost spikes for radios, optical modules, and billing software, lengthening project timelines. Delays ripple through network expansion roadmaps, risking spectrum-license penalties. Extended vendor receivables push suppliers to require steeper advance payments, worsening cash-flow strain. Uncertain foreign-exchange allocation from the central bank nudges carriers to prioritize swift-payback densification over long-dated fiber builds, potentially constraining long-term capacity. High import bills also lift handset prices, dampening smartphone upgrades that fuel premium-data adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and internet services captured 44.88% of Libya telecom MNO market revenue in 2025 on the back of ubiquitous LTE access, a social-media-centric youth base, and fiber backhaul initiatives. OTT and PayTV are on track for an 8.41% CAGR, pivoting the service mix toward on-demand video libraries and live sports bundles that ride submarine-cable bandwidth. Voice’s contribution erodes yet remains relevant for rural groups still gravitating toward 2G handsets. Messaging revenue tumbles as WhatsApp and Telegram entrench, but IoT traffic rises in oil-field telemetry, where foreign energy majors demand SCADA links with sub-second latency. As a result, operators are bundling SIM-based industrial VPNs with cloud dashboards, elevating margin per connection. OTT video growth also persuades carriers to resell content-delivery-network capacity, embedding Libya into regional cache hierarchies.

Growing smartphone penetration amplifies data-bundle volumes, especially after handset vendors rolled out Arabic-localized UI at sub-USD 60 price points. The Libya telecom MNO market size for data packages is projected to outpace overall topline growth as usage surpasses 12 GB per subscriber monthly by 2030. Operators targeting diaspora engagement co-brand streaming plans with North African media houses, driving regional content partnerships. Simultaneously, rising PayTV adoption pressures bandwidth caps, nudging carriers to upsell fiber-to-the-home where civil-works security allows trenching. This synergy between mobile and fixed plays positions converged operators to capture end-to-end content value chains.

By End User: Enterprise Growth Accelerates Digital Transformation

Consumer accounts stood at 88.29% of 2025 revenue, anchored in prepaid bundles and social-media data packs that underscore Libya telecom MNO market stickiness. Retention hinges on price agility and network uptime rather than expansive service portfolios. Yet enterprises promise outsized future value, with a forecast 9.09% CAGR tied to oil-sector IoT, government cloud migrations, and SME e-commerce storefronts. The segment’s expansion aligns with World Bank projections of 12.3% non-oil GDP growth in 2025.

International oil companies restarting upstream projects now demand dedicated microwave rings, satellite redundancy, and MPLS backbones for remote camps, lifting the average contract size. Public-sector bodies digitizing licensing introduce managed-LAN tenders that include cybersecurity monitoring, opening high-margin annuity streams. Enterprises also require cross-border links into European data centers; carriers leverage new sub-sea paths like Medusa to sell guaranteed-latency SLAs. Collectively, these factors grow the enterprise slice of the Libya telecom MNO market share while insulating revenue against prepaid-price volatility.

Geography Analysis

Coastal districts inform the revenue core as Tripoli and Benghazi host the densest clusters of LTE users and fiber loops, contributing more than half of the Libya telecom MNO market. Mobile coverage nationwide attains roughly 90%, yet quality splits appear once networks traverse the sparsely populated Sahara, where radio backhaul depends on microwave paths vulnerable to militia checkpoints. In urban settings, per-capita data consumption already exceeds 14 GB monthly, a figure forecast to double once 5G small cells blanket commercial zones.

The strategic Mediterranean shoreline fuels aspirations to act as a regional traffic hub. The 8,760 km Medusa system, landing by 2026 with 20 Tbps design capacity, will interconnect Libya with Spain, France, and Egypt, trimming wholesale IP costs and positioning carriers to resell transit to landlocked Sahel markets. A second wave of international cables, such as Meta’s Project Waterworth, is under study, which could foster data-center colocation clusters in Misrata ports, transforming the Libya telecom MNO market economics by adding neutral peering points.

Southern provinces remain underserved as chronic electricity blackouts and security fees inflate tower OPEX by over 30%. Operators experiment with solar-hybrid power and VSAT aggregation to widen rural footprints, but breakeven thresholds stay steep due to low household densities. Despite hurdles, rural coverage projects receive multilateral financing earmarked for economic inclusion, suggesting gradual narrowing of the digital gap through 2030. As connectivity evolves, agriculture and tourism in Fezzan region gain the bandwidth needed for drone surveys and online bookings, opening fresh local revenue pockets.

Competitive Landscape

The duopoly structure confers moderate bargaining power on both Libyana Mobile Phone and Al Madar Al Jadid, which together serve 8.5 million SIMs and around 98% of mobile lines. Libyana leads with 60% subscriber share, leveraging earlier LTE roll-outs and brand familiarity. Al Madar counters by signing exclusive arrangements with Vox Solutions for international A2P traffic filtering, enhancing messaging integrity for banks and OTT players. Both carriers intensify network investment in urban corridors while co-leasing rooftop sites in secondary towns to cut shared logistics costs.

Fixed broadband remains fragmented; Libya Telecom and Technology commands DSL and fiber but faces competition from 25+ licensed ISPs. The fixed space nonetheless represents only a single-digit slice of the Libya telecom MNO market size owing to limited last-mile copper and high consumer price sensitivity. As mobile networks upgrade to LTE-Advanced Pro, wireless broadband increasingly cannibalizes xDSL, encouraging LTT to form MVNO collaborations to retain broadband loyalty.

Future competitive differentiation is expected to pivot on cloud edge services, where low-latency hosting of Arabic social-media apps could attract regional eyeballs and diversify revenue beyond classic connectivity.

Libya Telecom MNO Industry Leaders

Libyana Mobile Phone

Almadar Aljadid

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sparkle reinforced partnership with Al-Bawaba to enhance corporate service offerings in Libya, expanding enterprise telecommunications capabilities and international connectivity options.

- August 2024: VOX Solutions became exclusive gateway for international A2P SMS and voice delivery into Al Madar Al Jadid’s network, enhancing security and fraud-prevention capabilities for international communications.

- March 2024: Libyan Digital Lab launched an innovations map to foster nationwide digital transformation, creating new demand for telecommunications services and data connectivity across government and private sectors.

Libya Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Libya telecom MNO market in 2026?

The Libya telecom MNO market size stands at USD 266.18 million in 2026 and is forecast to reach USD 394.59 million by 2031.

What is the projected growth rate for Libya’s telecom sector to 2031?

Aggregate revenue is expected to rise at an 8.19% CAGR through the forecast period (2026-2031).

Which service type currently leads revenue?

Data and internet services hold 44.88% of 2025 revenue, reflecting Libya’s mobile-first usage habits.

Who are the main telecom operators in Libya?

Libyana Mobile Phone commands roughly 60% subscriber share, while Al Madar Al Jadid serves most of the remaining lines.

How will submarine cables influence Libyan connectivity?

The Medusa system landing by 2026 will add 20 Tbps design capacity, reduce wholesale IP costs, and position Libya as a Mediterranean traffic hub.

Why is enterprise telecom demand accelerating?

Oil-field IoT, government cloud projects, and SME digital commerce are lifting enterprise revenue, projected at 9.09% CAGR to 2031.

Page last updated on: