South Sudan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

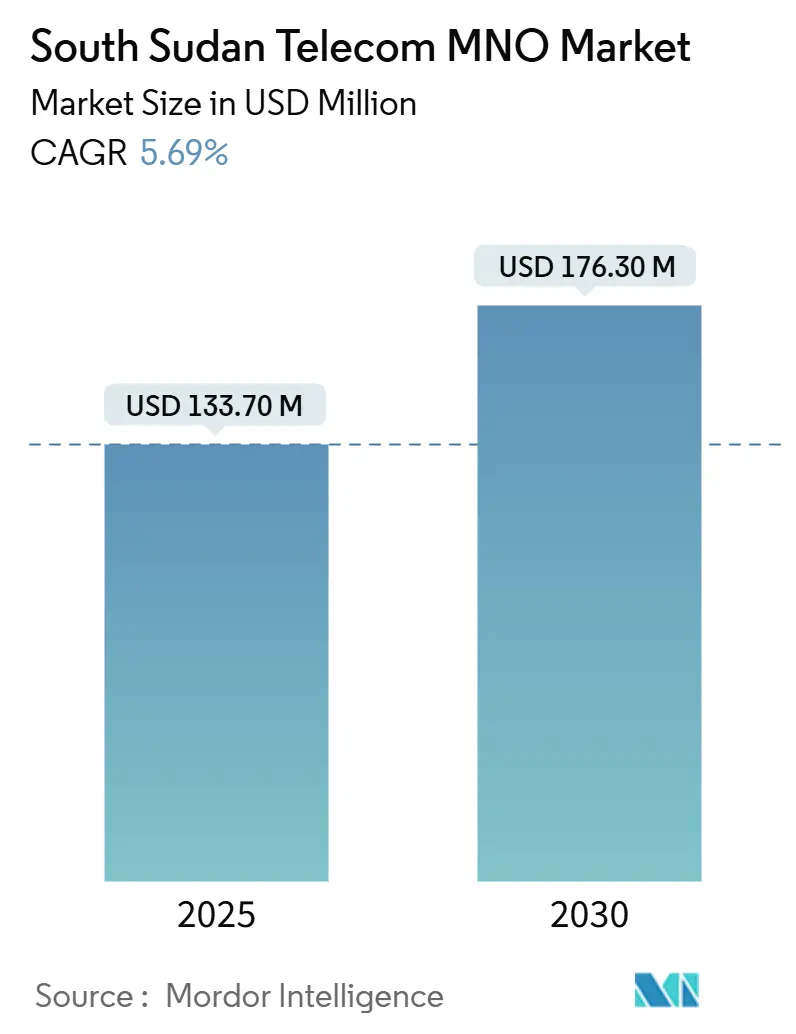

| Market Size (2025) | USD 133.70 Million |

| Market Size (2030) | USD 176.30 Million |

| Growth Rate (2025 - 2030) | 5.69% CAGR |

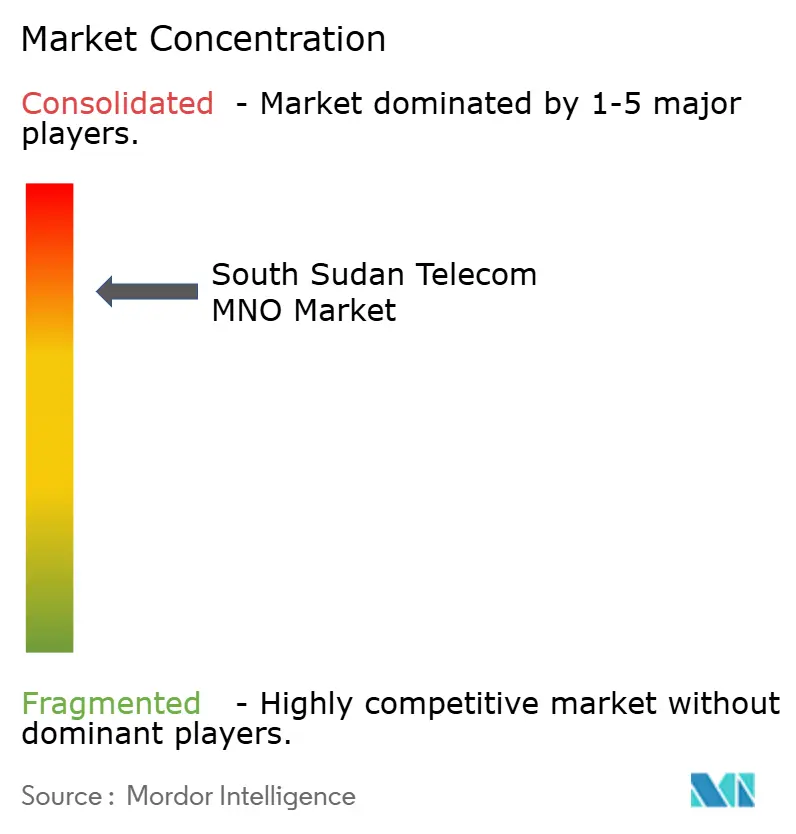

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Sudan Telecom MNO Market Analysis by Mordor Intelligence

The South Sudan Telecom MNO Market size is estimated at USD 133.70 million in 2025, and is expected to reach USD 176.30 million by 2030, at a CAGR of 5.69% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 3.76 million Subscribers in 2025 to 4.5 million Subscribers by 2030, at a CAGR of 3.66% during the forecast period (2025-2030).

A four-fold jump in MTN South Sudan’s Q1 2025 service revenue confirmed that demand remains robust even amid security risks.[1]MTN Group, “FY 2024 Integrated Report,” MTN Group, mtn.comMobile connections stood at 4.47 million—equal to 37.1% population penetration—while mobile broadband already accounts for 80.6% of total subscriptions. Network upgrades, mobile-money uptake, and cross-border fibre links are accelerating the shift from voice-centric to data-centric usage patterns. Operators focus first on Juba, Wau, and Malakal, but renewable-powered towers are starting to push basic coverage into rural counties. Fintech services, enterprise IoT projects, and regulatory reforms signal multiple monetisation paths that can diversify revenues and support long-term profitability across the South Sudan telecom market.

Key Report Takeaways

- By service type, data services led with 49.50% revenue share in 2024, while IoT recorded the fastest 5.76% CAGR outlook through 2030.

- By end user, the consumer segment captured 70.19% of 2024 revenue; the enterprise segment is expanding at 5.54% CAGR to 2030.

South Sudan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rollout of 3G/4G coverage across major urban corridors | +2.1% | National; concentrated in Juba, Wau, Malakal | Medium term (2-4 years) |

| Growing mobile-money adoption boosting data usage | +1.8% | National; urban concentration | Short term (≤ 2 years) |

| Government spectrum releases & regulatory reforms | +1.5% | National regulatory framework | Long term (≥ 4 years) |

| Rising enterprise digitisation demand for IoT connectivity | +1.2% | Urban centres; expanding to rural areas | Medium term (2-4 years) |

| Cross-border fibre links via Ethiopia & Kenya lowering IP cost | +1.0% | National; enhanced international connectivity | Long term (≥ 4 years) |

| Community-network initiatives unlocking rural voice demand | +0.8% | Remote counties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rollout of 3G/4G Coverage Across Major Urban Corridors

Mobile broadband coverage expanded by 7 percentage points during 2024, helped by MTN’s addition of 1,556 4G sites across its African footprint. Those investments underpin South Sudan’s transition from voice to data revenue models, with traffic across MTN markets rising 35.7% year-on-year. Concentrating sites in high-density corridors maximises near-term revenue and provides a platform for future 5G upgrades once spectrum is released. Urban-first deployment, however, widens the urban-rural divide that public connectivity programmes are trying to close through subsidised rollout and rural USO funds.

Growing Mobile-Money Adoption Boosting Data Usage

Mobile money contributed USD 150 billion to Sub-Saharan African GDP between 2013 and 2022. MTN Fintech’s February 2025 launch of a school-fees payment service illustrates how financial inclusion tools stimulate recurring data usage by embedding connectivity in daily transactions. Zain’s renegotiated licensing prepares it for similar gains, especially in counties where formal banking is scarce. Because each transaction requires authentication, balance checks, and messaging, mobile finances create a self-reinforcing cycle: more transactions produce more data sessions, thereby justifying additional network investment and raising ARPU.[2]GSMA, “Connectivity for Refugees in South Sudan,” GSMA, gsma.com

Government Spectrum Releases & Regulatory Reforms

The National Communication Authority is finalising new allocation rules to harmonise spectrum with International Telecommunication Union guidelines. Clear and affordable spectrum pricing lowers the cost of capital for operators and allows long-term planning for 5G. Stable policy environments also attract foreign direct investment in backhaul and data-centre assets, complementing ongoing regional roaming and wholesale arrangements for the South Sudan telecom market.

Rising Enterprise Digitisation Demand for IoT Connectivity

Enterprise transformation programmes lift demand for M2M and sensor-based solutions. An IOSR study of South Sudanese SMEs found a 0.983 correlation between digital communication adoption and on-time project completion, underscoring tangible productivity gains. Zain’s M2M-ready SIM modules and MTN’s enterprise VPN offers illustrate evolving B2B portfolios geared toward agriculture, logistics, and energy. Enterprise traffic delivers higher margins and lower churn, generating a second growth vector for the South Sudan telecom market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic power-grid deficits inflating network OPEX | -2.5% | National; severe in rural areas | Long term (≥ 4 years) |

| Political instability deterring FDI | -1.8% | National; varies by region | Medium term (2-4 years) |

| Scarcity of hard currency limiting equipment imports | -1.2% | National economic constraint | Short term (≤ 2 years) |

| High taxation on international bandwidth transit | -0.9% | National regulatory framework | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Power-Grid Deficits Inflating Network OPEX

Only 2% of South Sudanese households have grid electricity, forcing operators to rely on diesel generators that elevate site OPEX. A USD 20 million programme funded by the Energy Inclusion Facility and Finnfund will solarise towers, targeting 99.97% uptime while cutting fuel costs. Clear Blue Technologies is deploying hybrid solar solutions that show payback periods under four years, offering a blueprint for sustainable rural coverage.[3]Clear Blue Technologies, “Solar Power for South Sudan Telecom Sites,” Clear Blue Technologies, clearbluetechnologies.com

Political Instability Deterring FDI

Recurring security flare-ups raise insurance, logistics, and currency-hedging costs, as evidenced by MTN South Sudan’s 12.3% revenue drop in FY 2023. The IMF forecasts continued fiscal strain, potentially restricting public-sector support for ICT investments. Still, regional projects such as the Ethiopia–South Sudan highway could foster trade and improve macro-stability if implemented on schedule.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data services contributed 32.24% of total 2024 revenue as smartphone uptake accelerated and enterprises digitised workflows. Mobile data held 70.21% of the segment, reinforcing the role of handheld devices in broadening access. MTN’s open-market smartphone bundle, launched March 2025, gives new users 1 GB of monthly data for six months, improving affordability and cementing digital habits. Fixed data remains limited by fibre backhaul gaps, yet its 10.10% CAGR through 2030 signals upside once cross-border routes reach secondary cities. Voice still matters—wireless voice retained 67.45% market share—but its 8.86% CAGR trails the projected 10.00% rise in IoT traffic.

IoT is the fastest-growing niche, benefiting from agriculture-monitoring pilots and asset-tracking projects supported by Zain’s M2M service. The GSMA notes that refugees and displaced people keep phones where coverage exists, proving latent demand for sensor-enabled humanitarian and supply-chain applications. OTT messaging and emerging pay-TV video represent ancillary revenue paths that operators can bundle with data plans to lift ARPU in the South Sudan telecom market.

By End User: Consumer Dominance with Enterprise Acceleration

Consumer accounts generated 71.24% of 2024 revenue, mirroring the 4.47 million mobile connections primarily used for personal communications. Prepaid dominates, but data-heavy services and fintech apps are raising monthly spend levels in urban counties. The South Sudan telecom market size for consumer services is slated to widen alongside device subsidies and the rollout of renewable tower power systems that lower operating costs and enable rural expansion.

Enterprise revenue is smaller yet crucial; its 10.40% CAGR reflects digitisation across NGOs, agribusinesses, and construction firms. High correlation between digital-tool usage and project success boosts willingness to pay for dedicated bandwidth, MPLS VPN, and IoT services. Operators are strengthening account-management teams and offering service-level agreements to secure long-term contracts, protecting margins and diversifying the revenue base within the South Sudan telecom industry.

Geography Analysis

Urban corridors around Juba, Wau, and Malakal host the bulk of radio-access infrastructure. These zones deliver the highest ARPU, driven by dense populations and relatively reliable power. MTN and Zain concentrate 4G base stations here, achieving median download speeds above 20 Mbps, while Digitel targets underserved neighbourhoods to claw share. The South Sudan telecom market size attributable to urban counties is projected to expand at 8.5% CAGR through 2030, supported by rising smartphone penetration and fintech adoption.

Secondary towns along the Ethiopia and Kenya fibre spurs are seeing falling wholesale bandwidth prices, enabling ISPs to offer 15% cheaper fixed-wireless packages. A direct fibre link completed in 2020 continues to lower IP transit costs, and the USD 738 million Ethiopia-South Sudan highway will facilitate additional duct-sharing opportunities. Cross-border agreements within the East African Community streamline roaming and spectrum harmonisation, easing expansion barriers for operators.

Rural coverage remains sparse, hampered by power shortages, security issues, and limited income. But the USD 20 million solar tower programme, coupled with Starlink’s entry as a low-earth-orbit provider, improves the economics of reaching isolated communities. Renewable energy cuts generator refuelling trips, while low-orbit backhaul can bridge microwave gaps, albeit at Mbps rates below urban averages. Community-network pilots provide another template for affordable rural voice and data, suggesting gradual convergence in service availability across the South Sudan telecom market.

Competitive Landscape

The South Sudan telecom market is controlled by MTN South Sudan, Zain South Sudan, and Digitel. MTN leads in subscribers and revenue, leveraging group-wide procurement to reduce capex per site and accelerating 4G densification. Its Q1 2025 revenue quadrupled year-on-year, reflecting pent-up demand once network stability improved. In parallel, MTN is trialling 5G to future-proof spectrum strategy and offer enterprise-grade fixed-wireless access.

Zain follows with a clear fintech thrust. After securing a mobile-money licence in 2024, the operator is integrating wallet features with voice and data bundles to defend market share. Its M2M platform, already proven in other Middle-East and African markets, is being localised for South Sudanese agribusiness and NGO segments.

Digitel retains first-mover brand recognition, especially in remote counties where its legacy 2G network offered the initial telecom lifeline. The company is now partnering with tower-co investors to swap diesel power for solar hybrids, freeing cash for LTE upgrades. All three carriers recognise that fintech, enterprise IoT, and wholesale fibre resale will be decisive differentiators once basic voice coverage approaches saturation across the South Sudan telecom market.

South Sudan Telecom MNO Industry Leaders

MTN South Sudan

Zain South Sudan

Digitel Telecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MTN South Sudan introduced an open-market smartphone bundle offering 1 GB of monthly data for six months to new customers.

- February 2025: MTN Fintech South Sudan launched a School Fees Payment product that lets parents pay tuition via MoMo wallets.

- November 2024: MTN Group turned on commercial 5G in Benin and Congo and initiated 5G trials in South Sudan.

- September 2024: Clear Blue Technologies secured a contract to deploy renewable power systems on rural towers in South Sudan.

South Sudan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What are the biggest restraints on market growth

Chronic power shortages that inflate operating costs and persistent political instability that dampens foreign investment are the two largest drag factors identified in the analysis.

How important is mobile money to telecom revenue?

Mobile-money platforms are a major driver of data usage and ARPU, evidenced by MTN’s recent fintech launches and Zain’s new licensing agreements that open fresh revenue streams in the South Sudan telecom market.

How fast is the market expected to grow

The market is projected to post a 5.69% CAGR during 2025-2030.

Which service category holds the largest share

Data services led with 49.50% revenue share in 2024, underpinned by growing smartphone and mobile-money adoption.

Page last updated on: