Tunisia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

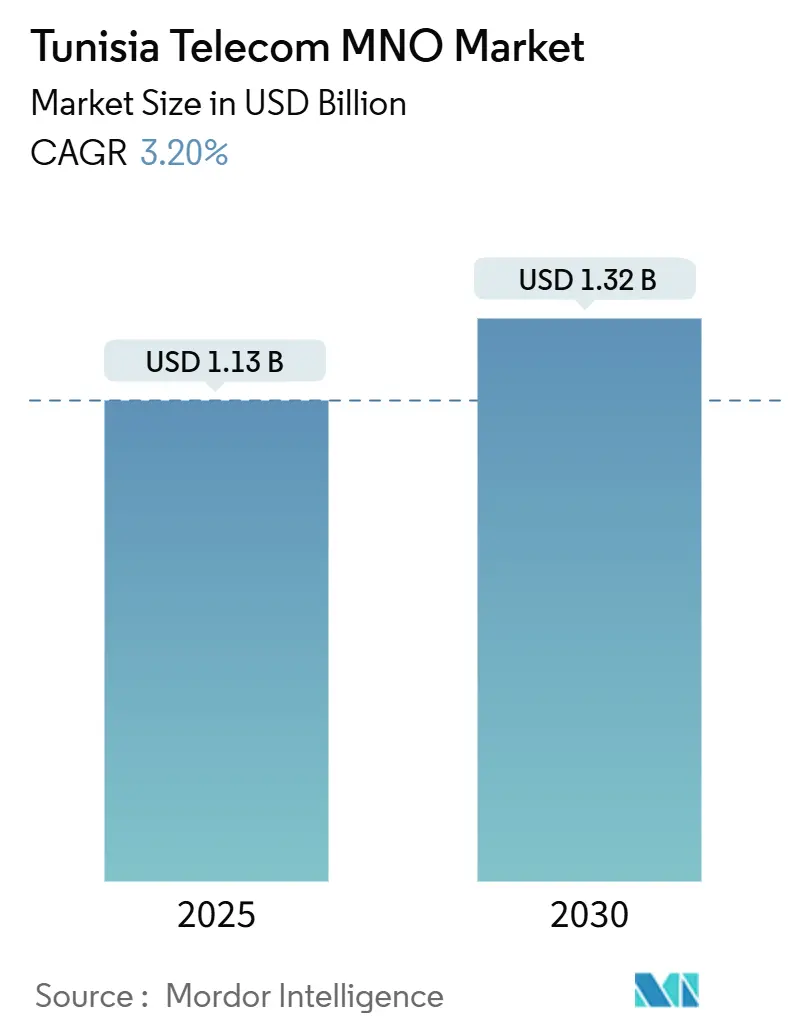

| Market Size (2025) | USD 1.13 Billion |

| Market Size (2030) | USD 1.32 Billion |

| Growth Rate (2025 - 2030) | 3.20% CAGR |

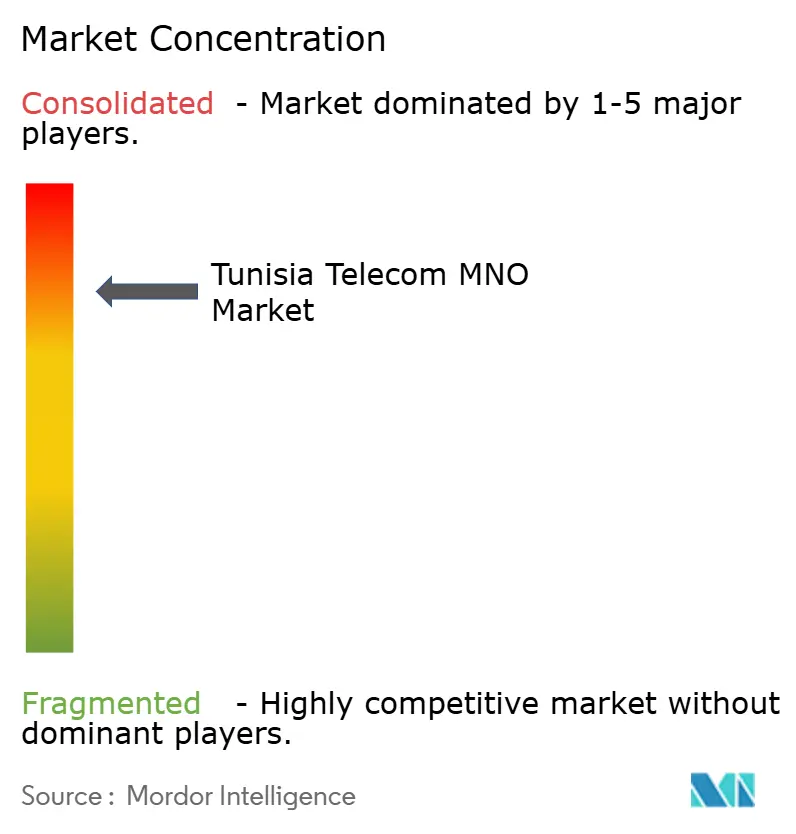

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tunisia Telecom MNO Market Analysis by Mordor Intelligence

The Tunisia Telecom MNO Market size is estimated at USD 1.13 billion in 2025, and is expected to reach USD 1.32 billion by 2030, at a CAGR of 3.20% during the forecast period (2025-2030).

The Tunisia telecom MNO market is advancing on the back of 5G launches, rapid fiber upgrades, and rising data consumption, even as macro-economic headwinds suppress discretionary spending. Government programs under Digital Tunisia 2025 keep capital flowing into network infrastructure, while the February 2025 commercial 5G debut created a premium tier that lifts average revenue per user. Operators are capitalizing on 84% internet penetration, modern submarine cables, and a young, mobile-first population to diversify beyond voice into cloud, cybersecurity, and fintech services. At the same time, dinar depreciation, high sector-specific taxes, and energy price spikes temper cash flow, forcing carriers to prioritize projects with near-term payback. Competitive intensity remains healthy because technology leadership, rather than price discounting, is the main battleground.

Key Report Takeaways

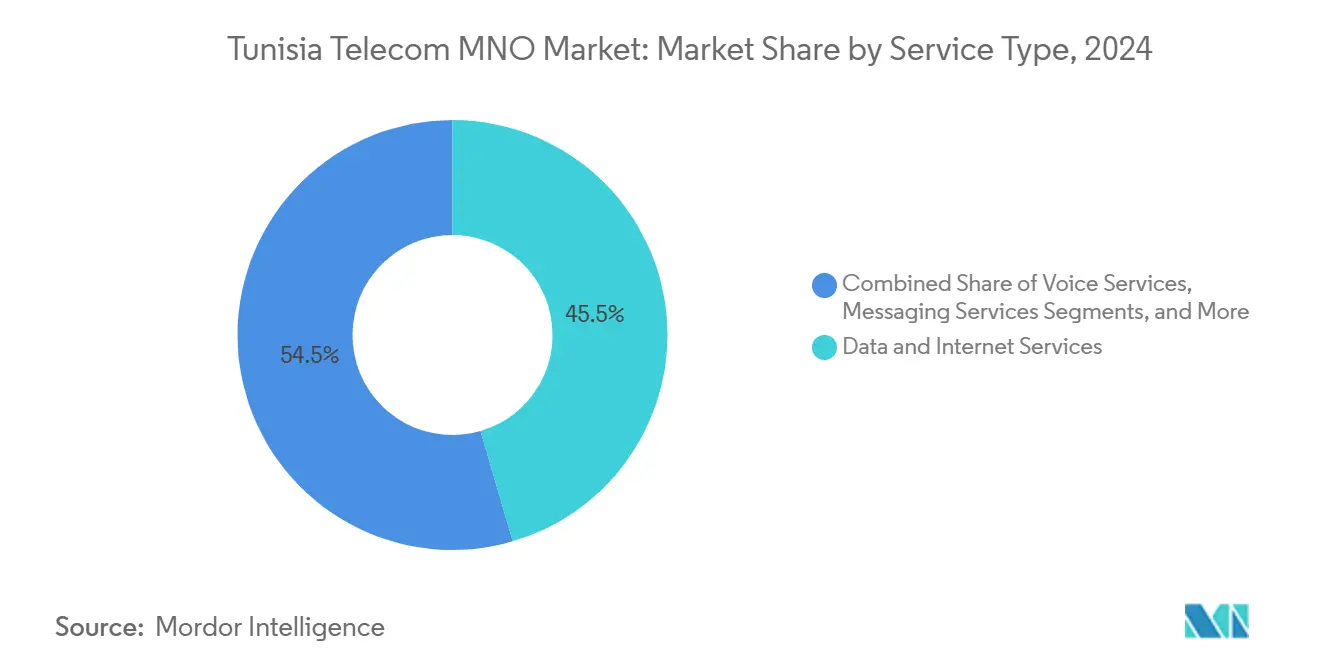

- By service type, data and internet services held 45.47% of Tunisia telecom MNO market share in 2024, while IoT and M2M services are projected to expand at a 3.33% CAGR through 2030.

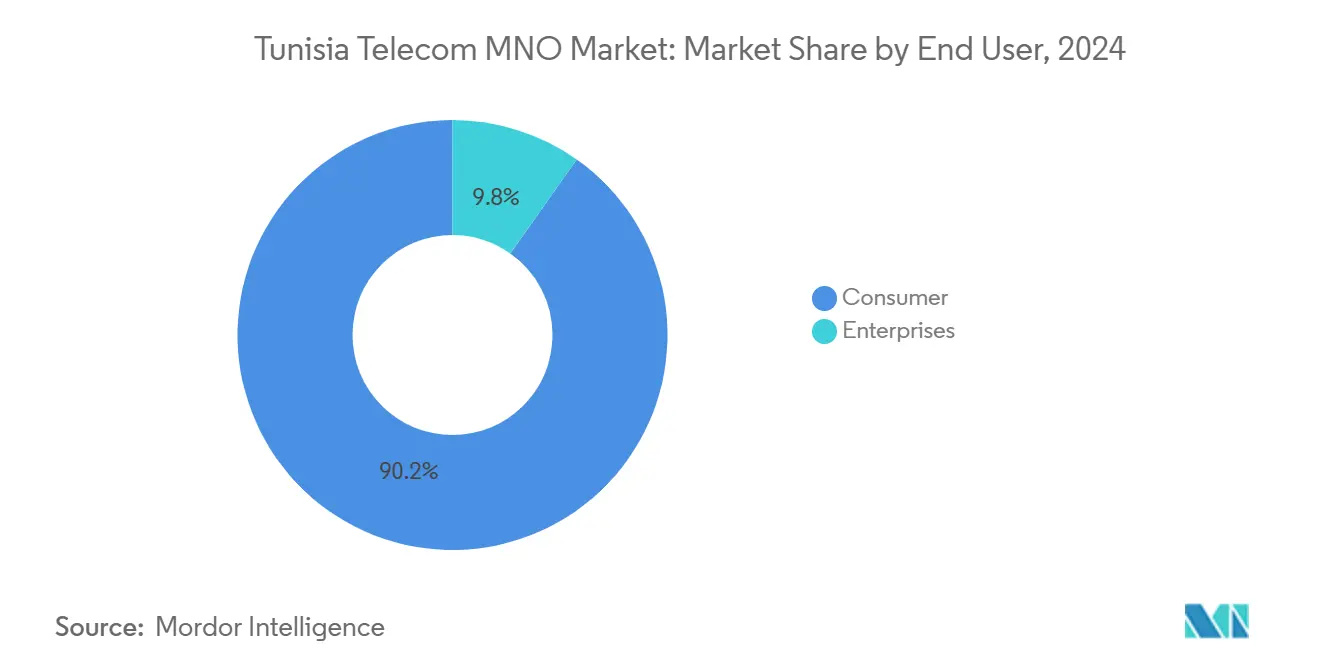

- By end user, consumers accounted for 90.19% of Tunisia telecom MNO market share in 2024, whereas the enterprise segment is forecast to grow at a 4.21% CAGR through 2030.

Tunisia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led 5G spectrum release and accelerated rollout | +1.2% | National, early gains in Tunis, Sfax, Sousse | Medium term (2–4 years) |

| Explosive mobile-data demand from 84% internet penetration | +0.8% | National, stronger in urban centers | Short term (≤ 2 years) |

| Rapid FTTH and VDSL build-out by incumbent TT | +0.6% | National, prioritizing underserved regions | Medium term (2–4 years) |

| SME and enterprise digitization (cloud, cybersecurity, SD-WAN) | +0.4% | National, concentrated in business districts | Long term (≥ 4 years) |

| New submarine cables boosting international capacity | +0.3% | National, enabling wholesale capacity growth | Long term (≥ 4 years) |

| Mobile-money and fintech ecosystems driving service stickiness | +0.2% | National, higher adoption in under-banked areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government-led 5G spectrum release and accelerated rollout

The Ministry of Communication Technologies assigned 700 MHz and 3.5 GHz bands to every operator in December 2024, giving carriers 15-year certainty that supports long-range capex planning. Commercial service went live in February 2025, and Tunisie Telecom immediately demonstrated 2.1 Gbit/s downlink, putting the Tunisia telecom MNO market ahead of regional peers. [1]Ericsson, “Tunisie Telecom and Ericsson Launch 5G,” ericsson.com With spectrum fragmentation removed, operators can pursue nationwide rollouts at lower cost per site, and fixed-wireless access now offers an economical alternative where fiber is lacking.

Explosive mobile-data demand from 84% internet penetration

Mobile broadband usage now drives network traffic more than subscriber additions. Average speeds of 128.22 Mbps position Tunisia 56th worldwide, but operator-specific gaps, Ooredoo’s 39.05 score versus Orange’s 26.13, shape competitive messaging. [2]Speedtest, “Tunisia Global Index,” speedtest.net Video streaming, gaming, and low-latency enterprise apps generate stickiness that supports premium tariffs, helping the Tunisia telecom MNO market defend margins despite inflation pressures.

Rapid FTTH and VDSL build-out by incumbent TT

Tunisie Telecom plans to double fiber homes-passed to 500,000 by 2025 and is upgrading copper loops to VDSL, lifting average fixed speeds to 30 to 50 Mbps. [3]Telecoms, “Tunisie Telecom Charts Optical Progress,” telecoms.com Its gigabit-grade “Giga Rapido” package proves there is appetite for ultra-fast tiers and increases switching costs for households, anchoring retention in the Tunisia telecom MNO market.

SME and enterprise digitization (cloud, cybersecurity, SD-WAN)

More than 1,040 tech startups operate under the pro-innovation StartupAct, and cybersecurity roles are expanding 27% annually. Enterprises need managed connectivity, private cloud, and secure multi-site networking, which lets operators bundle SD-WAN and threat-monitoring solutions to raise contract value. The result is a growing B2B share in the Tunisia telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macro-economic volatility and dinar depreciation squeezing CAPEX | -0.9% | National, affects all operators | Short term (≤ 2 years) |

| High sector-specific taxes and licence/USF fees | -0.6% | National, regulatory burden on all operators | Medium term (2–4 years) |

| Low 5G-device readiness (~7% of base) | -0.4% | National, early adopters in cities | Medium term (2–4 years) |

| Rising energy costs and grid outages inflating network OPEX | -0.3% | National, acute at remote towers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macro-economic volatility and dinar depreciation are squeezing CAPEX

Real GDP expanded only 0.4% in 2023, while inflation hit 9.3%, tightening household budgets and eroding operator cash flows. The state now relies heavily on domestic borrowing, crowding out private credit and inflating the cost of imported radio and optical equipment that must be paid in hard currency. Capital-intensive 5G and fiber timetables risk slipping, which could slow rural coverage and limit the full potential of the Tunisia telecom MNO market.

High sector-specific taxes and license/USF fees

Telecom operators still pay a 35% corporate tax and must contribute to a Universal Service Fund that acts as an additional levy. [4]United Nations Conference on Trade and Development, “Tunisia Finance Law,” unctad.org Up-front spectrum fees also strain liquidity right when 5G network densification demands peak. These burdens compress margins and can deter smaller players, increasing the regulatory risk profile of the Tunisia telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Shift

Data and internet services contributed 45.47% of Tunisia telecom MNO market revenue in 2024, underscoring how usage has migrated from voice to broadband. The Tunisia telecom MNO market size for data-centric services is projected to widen further as streaming, cloud gaming, and 5G applications mature. IoT and M2M lines, though small today, are rising at a 3.33% CAGR, powered by drone-LoRa smart farming pilots and municipal sensor grids. Voice and messaging now play a defensive role, supporting customer retention but suffering wallet share loss to OTT alternatives. Operators are countering with bundled VoLTE, rich communication services, and value-added TV packages. Submarine cable capacity gains let carriers wholesale bandwidth to hyperscalers, opening extra revenue channels. VAS and roaming still matter, yet regional roaming rate cuts have thinned margins, pushing operators to upsell digital content. The service mix, therefore, tilts progressively toward higher-quality data plans, enterprise networking, and fintech add-ons that increase average revenue and reduce churn across the Tunisia telecom MNO market.

Second-order growth stems from content partnerships and cloud storage offers that raise perceived value. Tunisie Telecom bundles 1 Gbps home fiber with OTT video and smart-home devices, while Ooredoo trials edge computing for gaming cafés. Orange monetizes network APIs for fraud management and carrier billing. These initiatives keep the Tunisia telecom MNO market nimble and ready for future 6G and satellite backhaul integrations.

By End User: Enterprise Segment Accelerates Despite Consumer Dominance

Consumers still represent 90.19% of active SIMs and revenue, reflecting prepaid popularity and high mobile-first engagement. Yet the Tunisia telecom MNO market size attributed to enterprises is growing faster, expanding at a 4.21% CAGR as firms digitalize. SMEs demand secure SD-WAN links for branch connectivity and cloud adoption, while large firms invest in private LTE for logistics yards. Public-sector e-identity and smart-city projects add further momentum. Postpaid ARPU is more than double prepaid, encouraging operators to convert high-usage households to contract plans with device financing. Enterprise contracts bring longer tenures, predictable revenue, and cross-sell of cybersecurity services, reducing exposure to price-sensitive mass markets in the Tunisia telecom MNO market.

Carriers now segment B2B offers by vertical, such as agriculture, manufacturing, and tourism. Ooredoo partners with hospitality groups to deploy managed Wi-Fi that integrates loyalty platforms. Orange launched an IoT marketplace targeting utilities and transport, while Tunisie Telecom pilots 5G slicing for media production. Each initiative deepens enterprise stickiness and diversifies revenue streams, improving resilience to consumer cycles.

Geography Analysis

Urban corridors spanning Tunis, Sfax, and Sousse account for more than half of the national telecom turnover. These cities enjoy dense fiber rings, multiple cell-on-wheels, and early 5G launches, making them the highest ARPU zones in the Tunisia telecom MNO market. Operators prioritize them for small-cell deployment and millimeter-wave trials to manage soaring data traffic. Coastal provinces also benefit from direct links to submarine cables such as Ifriqya, enabling low-latency backhaul that supports cloud and gaming services.

Interior governorates still rely heavily on 3G and limited fixed wireless. Government subsidies and USF grants encourage tower build-outs and rural fiber spurs, but thin household incomes and challenging terrain raise payback hurdles. Nonetheless, smart-agriculture pilots in Medenine show how IoT can justify coverage, signaling new revenue pools for the Tunisia telecom MNO market. Operators use solar-hybrid sites to cut diesel costs where grid outages persist, improving reliability and emissions metrics.

International capacity is strengthening Tunisia’s role as a North African transit hub. The Medusa system, scheduled for service in 2026, will link Bizerte to Marseille and Barcelona, adding resiliency and attracting data-center investors. Orange’s May 2025 Tier III facility near Sousse marks a shift toward decentralized cloud anchoring that shortens path distance for inland users. As a result, regional latency gaps narrow, promoting uniform service quality and supporting nationwide adoption of video conferencing, e-learning, and tele-health, key revenue catalysts within the Tunisia telecom MNO market.

Competitive Landscape

The Tunisia telecom MNO market features three network operators: Tunisie Telecom, Ooredoo Tunisia, and Orange Tunisie. Technology is the prime differentiator; Tunisie Telecom’s 5G-NSA first-mover advantage delivered the market’s fastest recorded downlink speed of 2.1 Gbit/s in March 2025. Ooredoo countered by lighting the Didon submarine cable with Orange, cutting IP transit costs and improving redundancy.

Infrastructure-sharing agreements lower rural rollout expenses and support environmental goals by reducing duplicate towers. Number portability, enforced since 2024, raises churn risk yet pushes carriers to invest in loyalty apps and bundle incentives rather than price wars, sustaining overall ARPU in the Tunisia telecom MNO market. White-space players such as Be Wireless Solutions operate in narrow-band IoT niches, partnering with MNOs for core connectivity and giving carriers a route to enterprise verticals without heavy capex.

Orange teamed with Flouci for mobile money, while Tunisie Telecom pilots blockchain-based remittances. Ooredoo leverages parent-group scale to negotiate favorable vendor contracts, enabling faster RAN modernization. Such moves underscore that scale, spectrum portfolio, and digital partnerships outweigh raw subscriber numbers in shaping competitive outcomes across the Tunisia telecom MNO market.

Tunisia Telecom MNO Industry Leaders

Tunisie Telecom

Ooredoo Tunisia

Orange Tunisie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Orange launched a data center facility outside Sousse to meet cloud demand and lower latency for regional enterprises.

- May 2025: Orange Tunisia partnered with fintech firm Flouci to expand mobile payment offerings and enhance digital financial inclusion.

- March 2025: Ericsson and Tunisie Telecom completed the first commercial 5G launch in North Africa, recording 2.1 Gbit/s downlink on 3.5 GHz spectrum.

- February 2025: Tunisie Telecom, Orange, and Ooredoo activated 5G services after simultaneous license approvals, each securing 700 MHz and 3.5 GHz blocks.

Tunisia Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What revenue growth is forecast for Tunisia’s mobile operators through 2030?

Market value is projected to climb from USD 1.13 billion in 2025 to USD 1.32 billion by 2030, implying a 3.20% CAGR.

How significant is 5G to operators’ future earnings?

5G offers premium data speeds and enables fixed wireless access, positioning carriers to upsell high-ARPU services despite macro challenges.

Which service category holds the largest share of operator revenue?

Data and internet services contributed 45.47% of total 2024 revenue and continue to expand as usage intensifies.

Why is enterprise connectivity growing faster than consumer segments?

SMEs are adopting cloud, cybersecurity, and SD-WAN solutions, driving a 4.21% CAGR in enterprise revenue compared with mature consumer growth.

How are operators mitigating high energy costs?

Carriers deploy solar-hybrid power at remote sites and share infrastructure to limit OPEX escalation tied to grid outages.

What makes Tunisia attractive as a regional data hub?

New submarine cables, favorable geography, and recent data-center investments reduce latency and raise international bandwidth, supporting hub status.

Page last updated on: