Sudan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

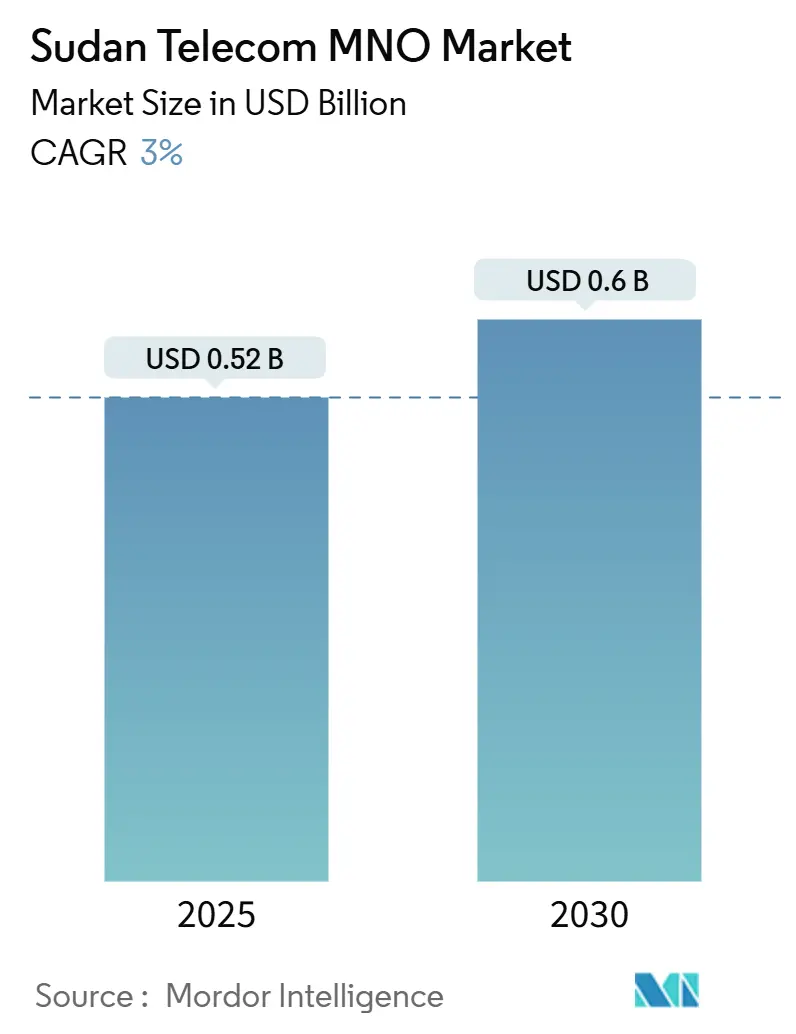

| Market Size (2025) | USD 0.52 Billion |

| Market Size (2030) | USD 0.6 Billion |

| Growth Rate (2025 - 2030) | 3.00% CAGR |

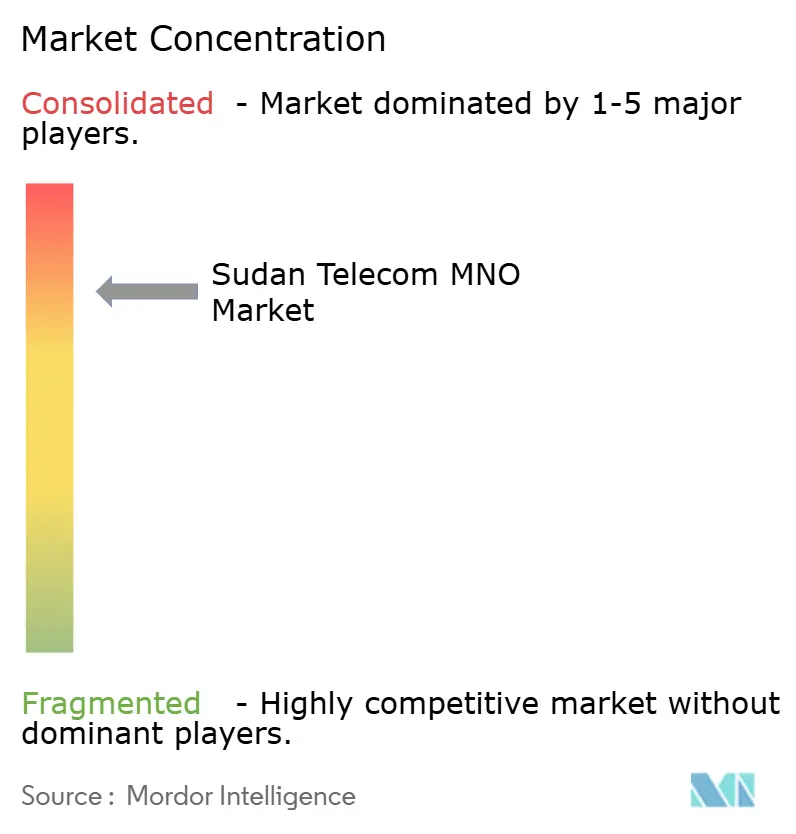

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sudan Telecom MNO Market Analysis by Mordor Intelligence

The Sudan Telecom MNO Market size is estimated at USD 0.52 billion in 2025, and is expected to reach USD 0.6 billion by 2030, at a CAGR of 3% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 23.93 million Subscribers in 2025 to 29.69 million Subscribers by 2030, at a CAGR of 4.41% during the forecast period (2025-2030).

The Sudan telecom MNO market has preserved forward momentum even as civil conflict, currency depreciation, and power-grid failures test the resilience of every operator. Sustained demand for mobile data, mobile money, and satellite-backed contingencies continues to underpin revenue stability, while a World Bank-funded national fiber backbone promises future cost efficiencies. Competitive behavior now revolves around network hardening, hybrid satellite partnerships, and digital-wallet ecosystems rather than rapid geographic expansion. At the same time, unmet connectivity needs in agriculture, oilfields, and remote communities position the Sudan telecom MNO market for targeted service innovation once macro-economic headwinds recede. [1]World Bank, “Central African Backbone Program Project Paper,” worldbank.org

Key Report Takeaways

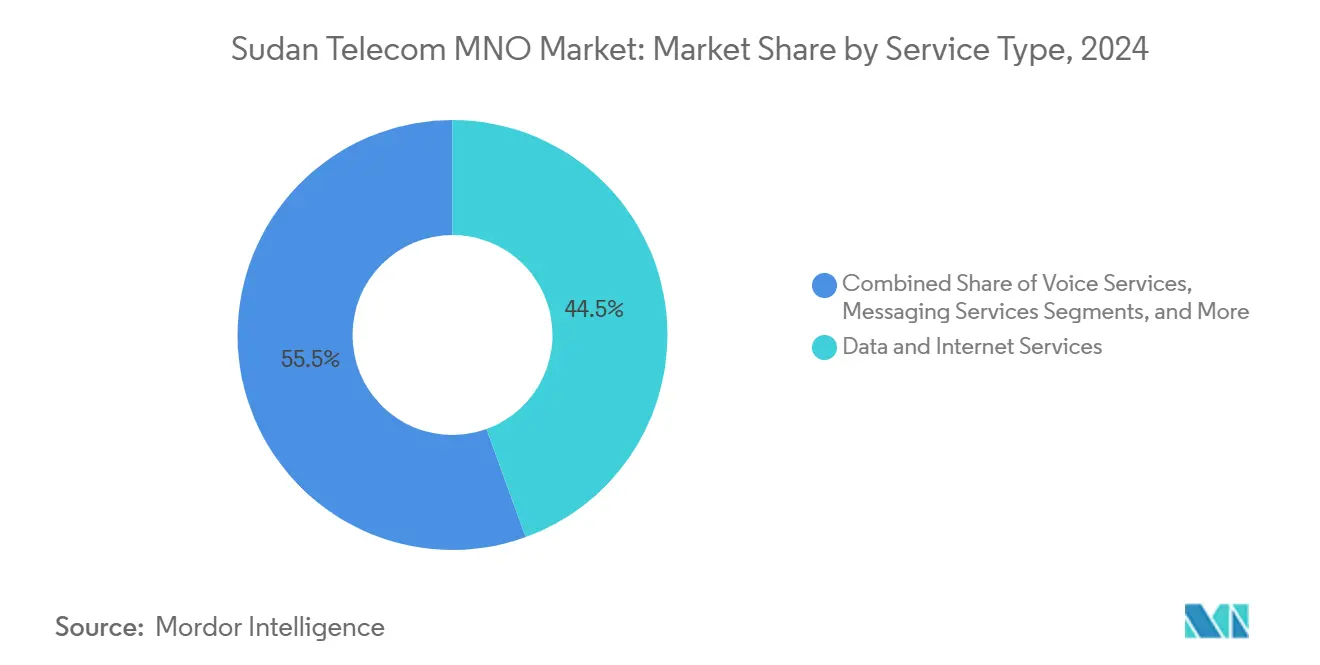

- By service type, data and internet services held 44.46% of the Sudan telecom MNO market share in 2024. IoT and M2M services are projected to advance at a 3.06% CAGR through 2030.

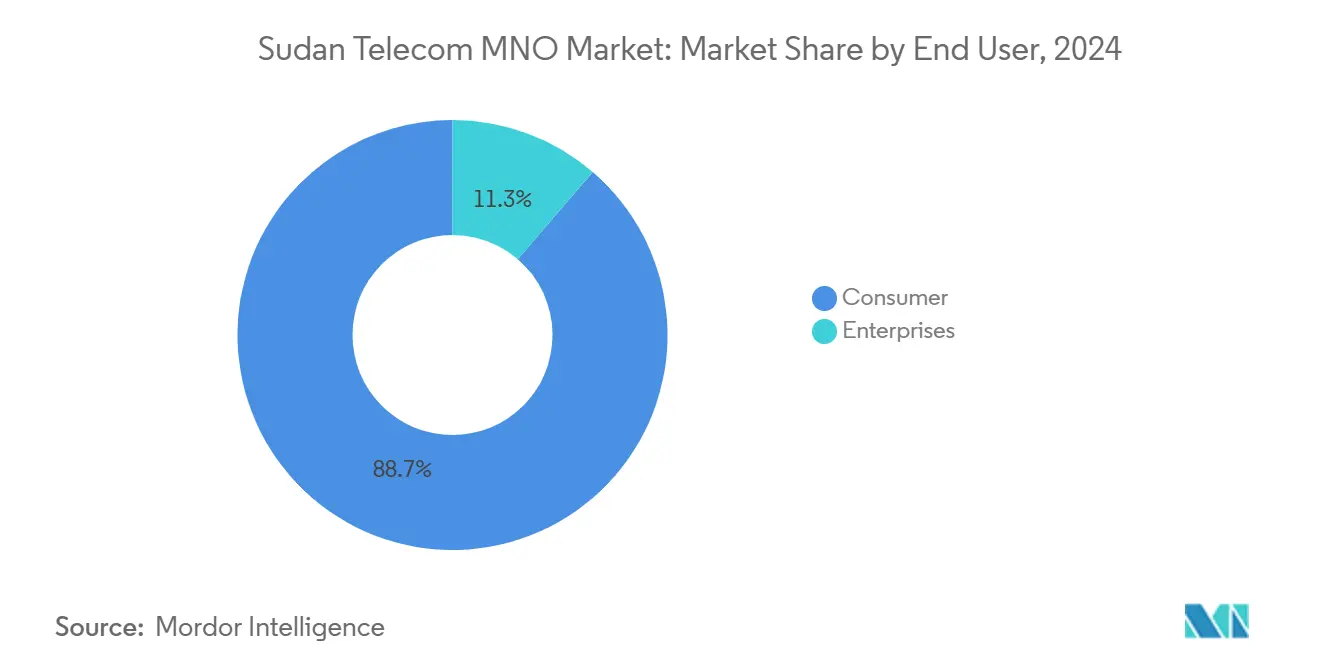

- By end user, the consumer segment captured 88.69% share of the Sudan telecom MNO market size in 2024, and enterprise connectivity is forecast to expand at a 3.88% CAGR to 2030.

Sudan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 4G expansion and pending 5G trials | +0.8% | Khartoum, Port Sudan, Kassala | Medium term (2-4 years) |

| Explosive mobile data usage and social-media video | +0.6% | Urban centers nationwide | Short term (≤ 2 years) |

| World Bank-backed national fiber backbone | +0.5% | Major inter-city corridors | Long term (≥ 4 years) |

| Mobile-money monetization flywheel | +0.4% | Conflict-affected zones nationwide | Short term (≤ 2 years) |

| IoT uptake in agriculture and oilfields | +0.3% | Rural farmlands and oil blocks | Long term (≥ 4 years) |

| Liberalized spectrum auctions drawing FDI | +0.2% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising 4G expansion and pending 5G trials

Sudatel began 5G proof-of-concept testing in 2025 using its metropolitan fiber grid, signalling confidence in Sudan’s long-term data demand trajectory. [2]Sudatel Group, “Financial Results Update 2025,” gulfnews.com Operators have also deployed solar-backed base stations to stabilise rural coverage during grid outages, reflecting capital reallocation toward resilience rather than green-field growth. Zain Sudan’s early 4G licence helped the company lock in urban high-value users, but conflict-related tower damage later diverted cash to repairs. [3]CommsUpdate, “Zain Sudan Secures 4G License,” commsupdate.com Initial 5G rollouts are expected in Port Sudan where undersea cable landing points justify next-generation throughput, while Khartoum’s timetable depends on security improvements. Expanded 4G footprints meanwhile enable streaming, remote schooling, and mobile banking that now anchor everyday digital life across the Sudan telecom MNO market.

Explosive mobile-data usage and social-media video

Video consumption on Facebook, TikTok, and X continues to surge, with average monthly mobile-data traffic reaching 8 GB per subscriber in early 2025, double the 2023 level. Operators respond with night-time bundles and app-specific passes to defend ARPU in a hyper-inflationary climate. Data-heavy mobile money authentications also add incremental packet loads. In conflict zones, citizens turn to compressed video clips for real-time safety updates, further widening the data-to-voice revenue gap. This usage spike underscores why the Sudan telecom MNO market continues investing in backhaul upgrades even when macro conditions deteriorate.

World Bank-backed national fiber backbone

The Central African Backbone Program earmarked USD 14.9 million for Sudan’s terrestrial fiber, promising lower wholesale bandwidth costs and diversified international routes. Redundant rings connecting Port Sudan to Khartoum and western corridors aim to mitigate single-point failures that plagued the network during the 2024 tower fires. Operators anticipate margin upside once domestic IP transit prices ease, allowing mass-market video and cloud services to flourish. Sudan’s geographic location also positions the fiber spine as a transit option for landlocked neighbors, opening a fresh wholesale revenue lane for the Sudan telecom MNO market.

Mobile-money monetization flywheel

Zain’s Bede wallet and MTN’s Samarat platform reached a combined 13 million registered users in 2025, facilitating salary disbursements, remittances, and humanitarian cash transfers. Every transaction generates micro-fees and stimulates additional data sessions, creating a reinforcing revenue cycle. Conflict-induced bank branch closures accelerated wallet sign-ups, with 90% of adults now outside the traditional banking grid. Regulators fast-tracked e-KYC norms to keep services running, underscoring the sector’s central role in economic recovery. The sustained uptrend in wallet activity shields the Sudan telecom MNO market from voice-revenue erosion common in other emerging economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political instability and network outages | -1.2% | Khartoum, Darfur hotspots | Short term (≤ 2 years) |

| FX crunch, hyper-inflation hitting CapEx and ARPU | -0.9% | Nationwide | Medium term (2-4 years) |

| Chronic power-grid interruptions | -0.5% | Urban and peri-urban areas | Short term (≤ 2 years) |

| Vendor-supply constraints from sanctions | -0.3% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political instability and network outages

Fires at the Khartoum NTC tower and the February 2024 nationwide blackout underscored how telecom edifices have become tactical targets. [4] Information Res, “Flash Report: Khartoum’s NTC Tower Up in Flames,” info-res.org Thirty million users lost mobile access for days, pushing demand toward Starlink satellite kits that circumvent terrestrial damage. Operators rushed to build micro-data centers in coastal zones perceived as safer, yet each relocation inflates opex and drags on the Sudan telecom MNO market growth trajectory. Unpredictable security incidents complicate multi-year spectrum and CapEx planning, curbing investor confidence until a durable ceasefire materializes.

FX crunch, hyper-inflation hitting CapEx and ARPU

The Sudanese Pound lost 40% of its value in 2024-2025, swelling imported-equipment invoices and shrinking consumer spending power. MTN Sudan’s H1 2024 service revenue fell 89.4% in USD terms, exemplifying how volatile exchange rates distort top-line reporting. Operators downgraded expansion plans to focus on network repairs, while handset subsidies virtually disappeared. Data pricing battles turned defensive, as carriers balanced affordability with survival, further moderating the Sudan telecom MNO market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-Centric Growth Leads Shifting Revenue Mix

Data and internet packages generated 44.46% of 2024 revenue, confirming their anchor position in the Sudan telecom MNO market size. Customers now consider basic data access as essential as voice, especially for social-media video and mobile-money apps. Voice still commands loyalty among older demographics, but OTT messaging erodes traditional SMS traffic. The IoT and M2M slice, though starting from a small base, is forecast to post a 3.06% CAGR through 2030 on the back of oil-field telemetry and precision-irrigation pilots.

Operators leverage bundled propositions to preserve ARPU, tailoring app-passes, night-surf deals, and education portals to segmented needs. The Sudan telecom MNO market share for OTT and PayTV is constrained by occasional platform blocks such as the July 2025 WhatsApp call restriction, yet domestic content providers pivot to local hosting to stay live. Value-added services like missed-call alerts, cloud storage, and enterprise VPNs round out incremental revenue, cushioning against voice price compression. Network rehabilitation timelines will dictate how quickly data quality can match the surging appetite.

By End User: Enterprise Uptake Outpaces Consumer Volume Growth

Consumers accounted for 88.69% of revenue in 2024, mirroring Sudan’s prepaid, mass-market profile. Yet enterprises are on track for a 3.88% CAGR, outstripping the broader Sudan telecom MNO market trajectory as ministries, agribusinesses, and oil majors digitalize processes. Corporates demand SLAs, dedicated APNs, and cybersecurity add-ons, commanding premium pricing that aids margin expansion.

Government-run hospitals and schools now prioritize robust connectivity to deliver tele-health and e-learning amid conflict displacement, driving bulk capacity contracts. Oil-field operators in Block 6 implemented sand-control IoT sensors relayed via private LTE, illustrating industry-specific use cases. Meanwhile, humanitarian agencies leverage enterprise SIMs for cash-transfer verification, further embedding operators in relief logistics. Over time, sustained enterprise momentum can offset slowing consumer growth, ensuring the Sudan telecom MNO market remains viable for investors.

Geography Analysis

Khartoum historically delivered more than one-third of the Sudan telecom MNO market size, yet repeated tower damage compelled operators to reroute traffic to Port Sudan, where international undersea cables land. Coastal hubs now enjoy lower latency and more stable power, attracting corporate colocation demand and reinforcing regional digital hubs. Northern corridors along the Egypt border experience spill-over effects from Cairo’s impending 5G launch, nudging traffic onto roaming and cross-border fibre conduits that improve redundancy.

Western Darfur witnessed the sharpest service contraction as conflict troops sabotaged switching sites, making satellite terminals the lifeline technology of choice. Even so, NGOs operating field hospitals created micro-demand pockets that the Sudan telecom MNO market began serving via compact VSAT and 4G repeaters. In southern agricultural belts, irrigation IoT pilots rely on edge computing gateways paired with low-band 4G to conserve power and data budgets. These rural deployments highlight how targeted innovation can unlock latent demand where conventional ARPU metrics appear weak.

The Medusa submarine cable, scheduled for completion by 2026, promises additional international capacity for Port Sudan and surrounding Red Sea states, potentially lowering transit costs by 20% on completion. Eastern states already leverage proximity to fibre landing stations to court outsourcing firms seeking resilient connectivity, thereby diversifying the Sudan telecom MNO market revenue base beyond pure retail mobile. As security stabilises, operators intend to knit these disparate regional islands into a cohesive nationwide network, reinforcing growth prospects toward the decade’s end.

Competitive Landscape

Sudan’s three-player structure produces an oligopoly where sheer coverage breadth, not deep discounting, sets market power. Zain stems from early 4G adoption and a proactive self-healing network strategy that uses satellite overlays when terrestrial links fail. MTN doubled down on social-payment integration, linking its Samarat wallet with humanitarian cash-transfer programs to widen stickiness despite an 89.4% revenue slide during H1 2024. Sudani banks on wholesale fiber and the upcoming 5G brand positioning to differentiate in urban corporate segments.

Recent strategy pivots revolve around redundancy build-outs rather than green-field coverage. All three signed term sheets with Low-Earth-Orbit satellite providers to reroute backhaul traffic during terrestrial outages, illustrating a cooperative resilience mindset unthinkable in peacetime competition. CapEx allocations prioritize diesel-hybrid generators, lithium storage, and solar panels to curb power-grid volatility, indirectly benefiting ESG metrics outlined in Liquid Intelligent Technologies’ 2024 sustainability audit.

Vendor negotiations remain fraught as US and EU sanctions complicate hardware imports. Therefore, carriers increasingly source open-RAN components from neutral jurisdictions, making Sudan a test-bed for vendor-agnostic architectures that lower long-run TCO. These moves hint at a gradual shift in the Sudan telecom MNO market away from legacy turnkey models toward modular, cloud-native stacks. Competitive intensity thus centers on agility and ecosystem breadth rather than subscriber poaching through aggressive tariffs.

Sudan Telecom MNO Industry Leaders

Zain Sudan

MTN Sudan

Sudani (Sudatel)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Egypt’s communications regulator confirmed commercial 5G launch for H1 2025, adding competitive urgency for Sudan’s planned 5G pilots.

- February 2024: Starlink kit prices fell 33% as Sudanese demand spiked during a nationwide mobile outage.

Sudan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the expected value of the Sudan telecom MNO market in 2030?

It is projected to reach USD 0.6 billion by 2030, reflecting a 3% CAGR during 2025-2030.

Which service type currently generates the largest revenue?

Data and internet services lead with a 44.46% share of 2024 revenue.

How big is Zain Sudan’s customer base?

Zain Sudan serves more than 12 million active users, equal to 42% of national mobile connections.

Why is enterprise demand growing faster than consumer demand?

Enterprises require secure IoT, cloud, and payment-integration services, pushing a 3.88% CAGR compared with slower consumer growth.

How are operators mitigating network outages?

Carriers deploy solar-hybrid towers, satellite backhaul, and distributed data centers to maintain service during conflict-driven disruptions.

Page last updated on: