Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

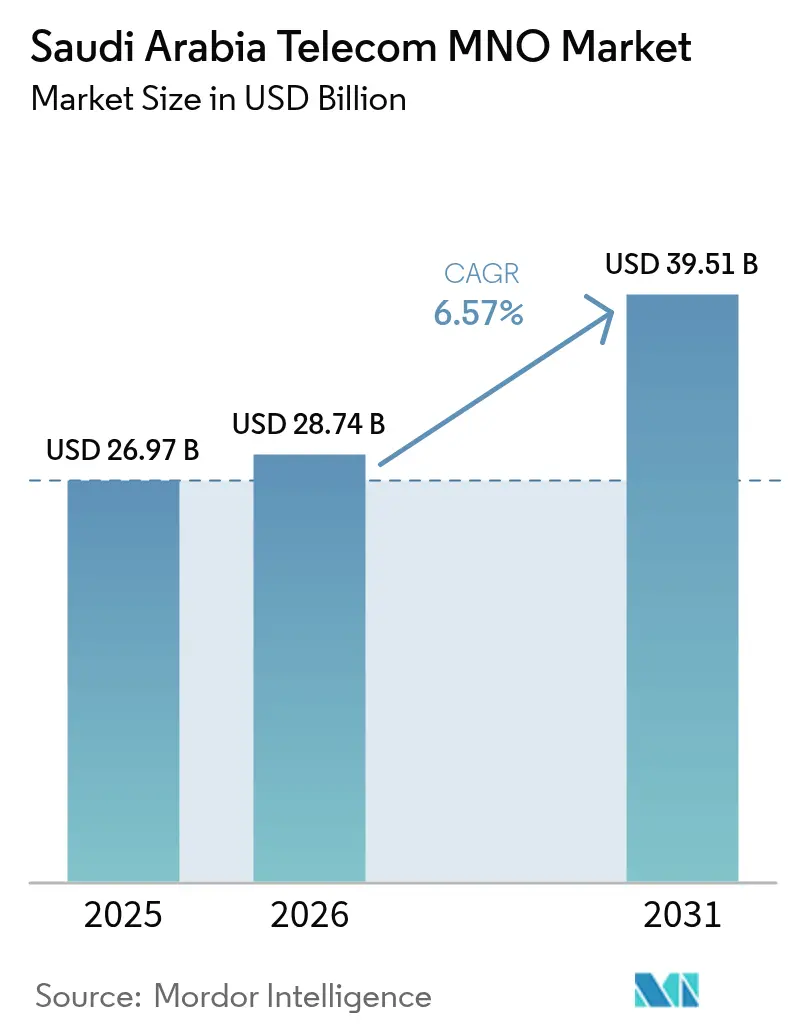

| Base Year Market Size (2025) | USD 26.97 Billion |

| Market Size (2026) | USD 28.74 Billion |

| Market Size (2031) | USD 39.51 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

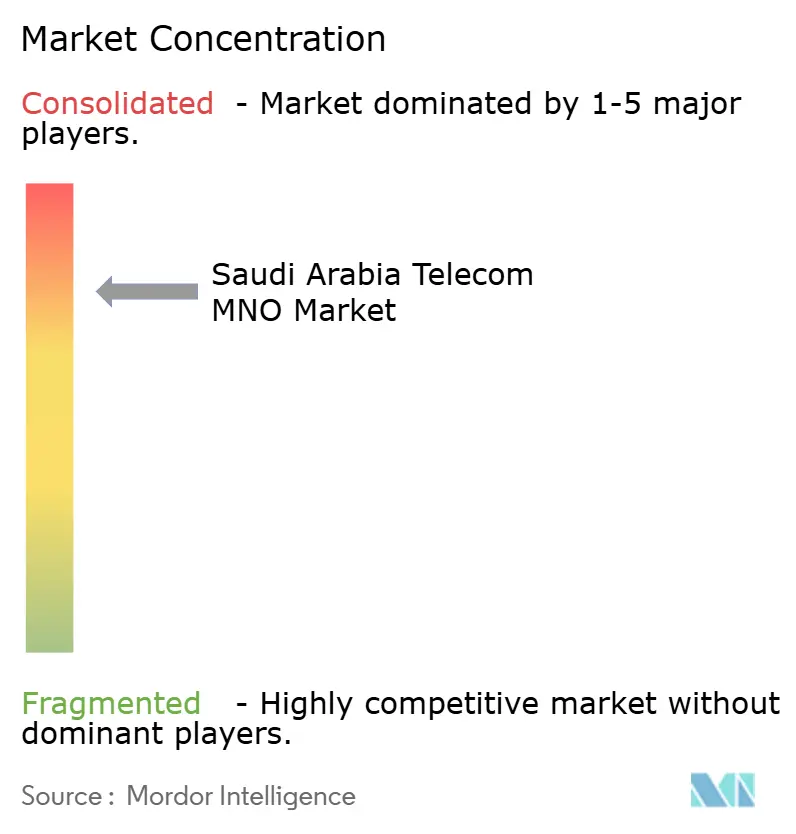

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Telecom MNO Market Analysis by Mordor Intelligence

The Saudi Arabia Telecom MNO Market size was valued at USD 26.97 billion in 2025 and estimated to grow from USD 28.74 billion in 2026 to reach USD 39.51 billion by 2031, at a CAGR of 6.57% during the forecast period (2026-2031).

Network investments supporting 78% 5G population coverage and average mobile download speeds of 322 Mbps continue to elevate user expectations, while Vision 2030 policies position telecom services as a cross-sector enabler [1]Iain Morris, “State of 5G in Saudi Arabia,” CIO, cio.com. New spectrum allocations in the 600 MHz, 700 MHz, and 3800 MHz bands are lowering per-bit costs and unlocking rural coverage gains. Data-driven revenue opportunities are expanding as smartphone penetration exceeds 95%, and the push toward private 5G networks sets a new growth frontier within industrial zones. At the same time, near-saturated subscriber penetration compels operators to prioritize average-revenue-per-user uplift through premium connectivity and digital-service bundles.

Key Report Takeaways

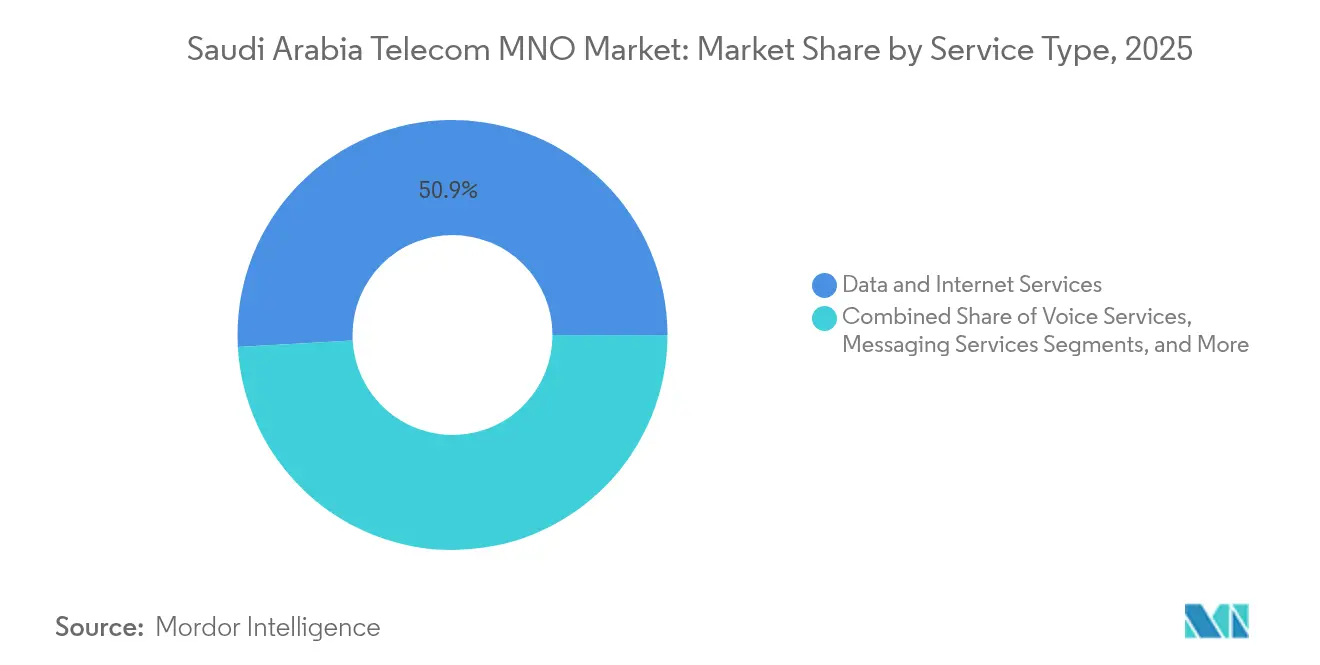

- By service type, data and internet services led with a 50.88% share of the Saudi Arabia telecom MNO market size in 2025. IoT and M2M services are projected to expand at a 6.67% CAGR through 2031.

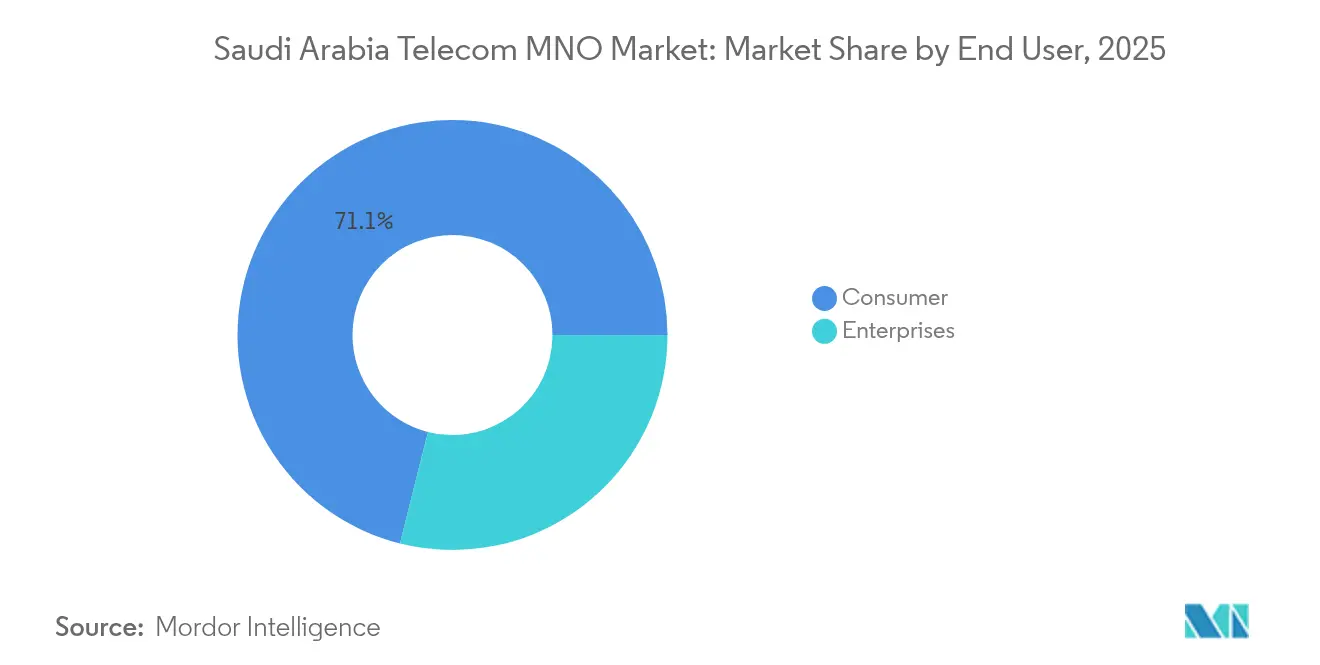

- By end user, the consumer segment held 71.07% of the Saudi Arabia telecom MNO market share in 2025, while the enterprise segment is advancing at a 6.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging mobile-data consumption amid >95% smartphone penetration | +1.8% | National, concentrated in Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| Vision 2030 digital-government and smart-city initiatives | +1.5% | National, with early gains in NEOM, Riyadh, Eastern Province | Long term (≥ 4 years) |

| Nationwide 5G roll-out and new mid-band spectrum auctions | +1.2% | National, urban areas first | Medium term (2-4 years) |

| Industrial private-5G pilots in NEOM and manufacturing zones | +0.9% | NEOM, Eastern Province industrial clusters | Long term (≥ 4 years) |

| LEO-satellite backhaul unlocking remote site economics | +0.6% | Remote areas, border regions | Medium term (2-4 years) |

| Fintech boom driving secure IoT-ready connectivity bundles | + 0.4% | Urban centers, financial districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 digital-government and smart-city initiatives

Large-scale e-government programs mandate ultra-reliable connectivity for real-time citizen services. The Ministry of Communications and Information Technology’s 2023 strategy aims to lift national ICT output by 50%, creating sizable enterprise contracts for operators [2]U.S. Department of Commerce, “Saudi Arabia ICT Guide,” trade.gov. NEOM’s 5G-based cognitive-city blueprint further elevates demand for network slicing and edge computing. These projects recast the Saudi Arabia telecom MNO market as a value-added infrastructure partner rather than a commodity bandwidth provider, enabling higher ARPU through managed solutions.

Nationwide 5G roll-out and new mid-band spectrum auctions

Spectrum auctions boosting licensed frequencies by 27% are accelerating 5G densification and lowering capacity costs [3]Communications, Space & Technology Commission, “Our Services,” cst.gov.sa. STC’s 5G footprint now spans more than 22,000 towers, and Huawei’s SuperLink initiative extends coverage to remote districts. Rising data consumption, up 19% year over year, requires efficient mid-band assets, reinforcing network investment while supporting emerging fixed-wireless-access uptake.

Industrial private-5G pilots in NEOM and manufacturing zones

Aramco Digital’s acquisition of 450 MHz spectrum allows direct industrial connectivity outside traditional MNO infrastructure, signaling fresh competition in premium enterprise segments. Pilot networks in oil, gas, and manufacturing sites illustrate latency reductions critical for predictive maintenance. MNOs are responding with tailored private-network and edge-service packages, protecting relevance within the Saudi Arabia telecom MNO market.

Fintech boom driving secure IoT-ready connectivity bundles

Card payment volumes jumped 57% during April 2024, and Google Pay’s entry is deepening the need for real-time, low-latency financial traffic segregation [4]Arab News Staff, “Saudi Tech-Market Surge,” arabnews.com. stc Bank leverages parent-network quality to guarantee transaction reliability, while Zain KSA broadens payment solutions. These developments create bundled offers pairing IoT-enabled point-of-sale devices with managed connectivity, producing incremental revenue streams.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-saturated subscriber base limits organic growth | -1.4% | National, particularly urban areas | Short term (≤ 2 years) |

| Elevated spectrum and tower-sharing costs pressure margins | -1.1% | National, concentrated in dense urban areas | Medium term (2-4 years) |

| Slow device readiness for mmWave 5G bands | -0.8% | Urban centers with mmWave deployment | Medium term (2-4 years) |

| OTT substitution eroding legacy voice/SMS revenue | -0.6% | National, youth demographics primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Near-saturated subscriber base limits organic growth

Mobile connections surpass 116% of the population, making incremental additions a zero-sum fight. stc posted a 5.2% profit decline in Q1 2024 despite higher revenue, illustrating margin compression in mature markets. Operators now focus on upselling premium services rather than chasing new lines, but competitive price promotions keep ARPU uplift modest.

OTT substitution eroding legacy voice/SMS revenue

Regulators still restrict WhatsApp voice calls, yet approved VoIP platforms nibble at international calling income. Messaging apps dominate daily communication, accelerating SMS decline. While data usage offsets some losses, persistent OTT migration pressures the long-term revenue mix of the Saudi Arabia telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data growth fuels IoT momentum

Data and internet services commanded 50.88% of the Saudi Arabia telecom MNO market in 2025, supported by over 32 million mobile internet users and 93% penetration. The Saudi Arabia telecom MNO market size attached to data services is projected to maintain mid-single-digit growth as 5G drives higher usage rates. IoT and M2M lines, though smaller in absolute revenue, are forecast to expand at a 6.67% CAGR, helped by industrial automation and smart-city setups. Voice remains relevant for enterprise calling and inbound roaming, yet younger segments rely predominantly on OTT channels. Messaging’s contribution continues to shrink as multimedia substitutes gain popularity, motivating operators to bundle Rich Communication Services with 5G plans.

Operator strategies emphasize differentiated content and cloud-edge features to lift data ARPU. stc’s enterprise-grade IoT platform connects oil-and-gas sensors to centralized analytics, illustrating premium pricing potential. Meanwhile, Mobily’s focus on fixed-wireless access has captured subscribers needing fiber-like speeds without civil works. OTT and PayTV services benefit from stc tv content tie-ups, while regulatory caps on international video apps constrain outside competition, indirectly supporting local offerings.

By End User: Enterprise traction reshapes revenue mix

The consumer base supplied 71.07% of the Saudi Arabia telecom MNO market size in 2025, but revenue per user is plateauing. Enterprises, by contrast, are scaling connectivity budgets for private 5G, edge computing, and secure cloud interconnects. The enterprise slice is growing at a 6.93% CAGR through 2031, and STC’s corporate-segment revenue rose 17% in Q1 2024, highlighting upside. Industrial clients in the Eastern Province are piloting network-slice solutions that guarantee deterministic latency, differentiating them from consumer services.

As public-sector digitization accelerates, operators package managed security, IoT device management, and unified communications under multi-year contracts. Zain KSA leverages its tower monetization proceeds to fund enterprise 5G-Advanced capabilities, while Mobily positions its wholesale arm as a trusted transit partner. Consumer growth now hinges on service innovation, gaming passes, cloud storage, and video streaming, rather than pure connectivity, reinforcing the shift in strategic focus.

Geography Analysis

Revenue concentration remains anchored in Riyadh, Jeddah, and Dammam, yet megaprojects are redrawing the Saudi Arabia telecom MNO market map. Urban areas exhibit the highest data-traffic density, supported by contiguous 5G coverage lanes. NEOM’s multibillion-dollar investment pipeline is catalyzing bespoke network build-outs, while the Eastern Province’s refinery corridor demands industrial-grade private networks for safety-critical systems. The Saudi Arabia telecom MNO market size accrued from these high-value zones is projected to outpace national averages through 2031.

Rural coverage gaps are shrinking due to LEO-satellite backhaul and newly allocated low-band spectrum that extends reach without costly fiber backhaul. Border regions, historically underserved, gain enhanced connectivity for logistics and security applications. Fixed-wireless-access adoption is strongest in peri-urban districts where fiber roll-outs lag, representing 20% of residential broadband connections in 2025.

Tourism peaks during Hajj and Umrah create seasonal traffic spikes in the Western Province, driving temporary capacity upgrades and network-optimization projects such as stc’s AI-powered MantaRay deployment. International submarine cable landings on the Red Sea and Arabian Gulf coasts reinforce Saudi Arabia as a transit corridor between Europe, Africa, and Asia, further diversifying geographic revenue streams within the Saudi Arabia telecom MNO market.

Competitive Landscape

The Saudi Arabia telecom MNO market is an oligopoly dominated by three operators that collectively capture a significant share. stc leads the market owing to early 5G deployment and state-backed infrastructure advantages. Mobily is anchored in enterprise wholesale strength, recently recognized with a regional wholesale award. Zain KSA pursues differentiation through 5G-Advanced trials and fintech expansion, recording 154% profit growth after monetizing tower assets.

Infrastructure consolidation is intensifying. The Public Investment Fund’s tower-company merger with stc forms the region’s largest passive-infrastructure platform, lowering duplication and freeing operator capital. Similar moves, such as Zain’s USD 805 million tower sale to PIF, signal a shift toward service-level competition rather than infrastructure spends.

Strategic technology alliances broaden competitive moats. Ericsson’s 2025 “Fusion” partnership with stc accelerates AI-driven network automation, while Huawei’s SuperLink roll-out enhances rural coverage. Aramco Digital’s USD 7.5 billion AI fund and newly obtained connectivity license introduce a formidable challenger in the enterprise slice, pushing incumbent MNOs to refine industrial solutions. As premium enterprise services rise in importance, customer-experience analytics and cybersecurity capabilities become decisive success factors across the Saudi Arabia telecom MNO market.

Saudi Arabia Telecom MNO Industry Leaders

stc (Saudi Telecom Company)

Mobily (Etihad Etisalat)

Zain KSA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: stc Group and Ericsson announced a “Fusion” partnership to scale AI-driven network automation, strengthening stc’s 5G leadership.

- December 2024: Nokia and stc launched AI-enabled operations solutions to enhance network efficiency and customer experience.

- November 2024: stc and Huawei debuted the SuperLink program to extend 5G into remote regions, supporting digital-inclusion targets.

- October 2024: Aramco Digital secured a specialized wireless license enabling industrial connectivity services across oil, gas, and logistics sectors.

- May 2024: Zain KSA announced a SAR 1.6 billion investment to expand its 5G network footprint in high-traffic areas.

Saudi Arabia Telecom MNO Market Report Scope

Telecommunication is an infrastructure that allows the transfer of all types of data, such as voice, text, audio, and video, across the world through a wired or wireless medium. The telecommunication sector is penetrating its services and coverage in remote areas and becoming vital to human lives. The telecom sector includes telephone, telecommunication, and internet service providers. The industry expanded in the past decades from telephonic voice calls to mobile data calls, internet calls, text, internet, and TV broadcasting services.

The Saudi Arabian telecom MNO market is segmented into telecom services (voice services [wired and wireless], data and messaging services, and OTT and pay-TV services) and telecom connectivity (fixed network and mobile network). Further, factors affecting the market's evolution in the near future, such as drivers and constraints, have been covered in the study. The market sizes and predictions are provided in terms of value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the forecast value of the Saudi Arabia telecom MNO market in 2031?

The market is expected to reach USD 39.51 billion by 2031.

Which operator currently leads in subscriber share?

Stc holds 55% of subscribers, making it the market leader.

How fast is the enterprise segment growing?

Enterprise service revenue is advancing at a 6.93% CAGR through 2031.

What percentage of the population is covered by 5G?

Current 5G networks cover 78% of residents.

Why are private 5G networks important for Saudi industry?

They deliver deterministic latency and security required for oil, gas, and manufacturing automation.

What major restraint could slow revenue growth?

Near-saturated mobile penetration limits new subscriber additions, pressuring ARPU.

Page last updated on: