Switzerland ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

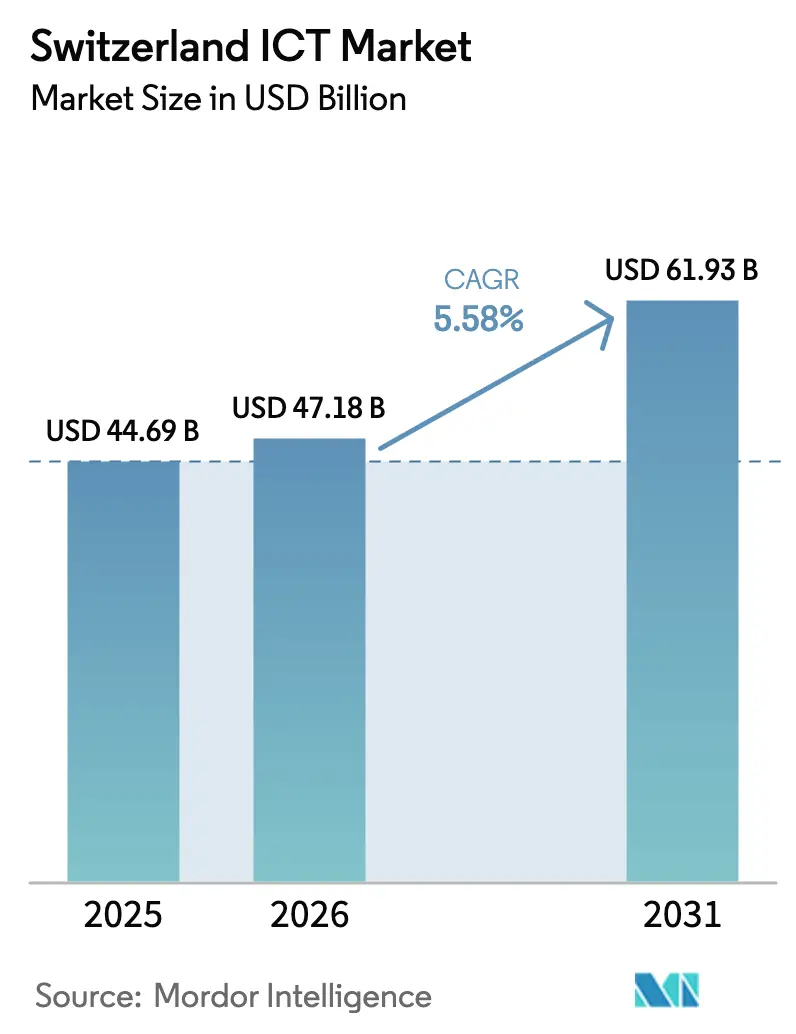

| Base Year Market Size (2025) | USD 44.69 Billion |

| Market Size (2026) | USD 47.18 Billion |

| Market Size (2031) | USD 61.93 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland ICT Market Analysis by Mordor Intelligence

The Switzerland ICT market size is expected to grow from USD 44.69 billion in 2025 to USD 47.18 billion in 2026 and is forecast to reach USD 61.93 billion by 2031 at 5.58% CAGR over 2026-2031. The Switzerland ICT market benefits from the nation’s top-ranked innovation ecosystem, a 3.4% R&D-to-GDP ratio, and rapid progress toward cloud-first and 5G architectures. Federal funding programs, hyperscale data-center investments, and blockchain experimentation inside the financial sector keep demand high while reinforcing Switzerland’s value proposition around data sovereignty. Multinational headquarters in Zurich, Geneva, and Basel drive large-enterprise spending, whereas digitally enabled small businesses now accelerate adoption thanks to simplified cloud migration paths. Competitive intensity is rising as global hyperscalers partner with local providers to blend regulatory compliance with scalability, further deepening the Switzerland ICT market’s growth runway.

Key Report Takeaways

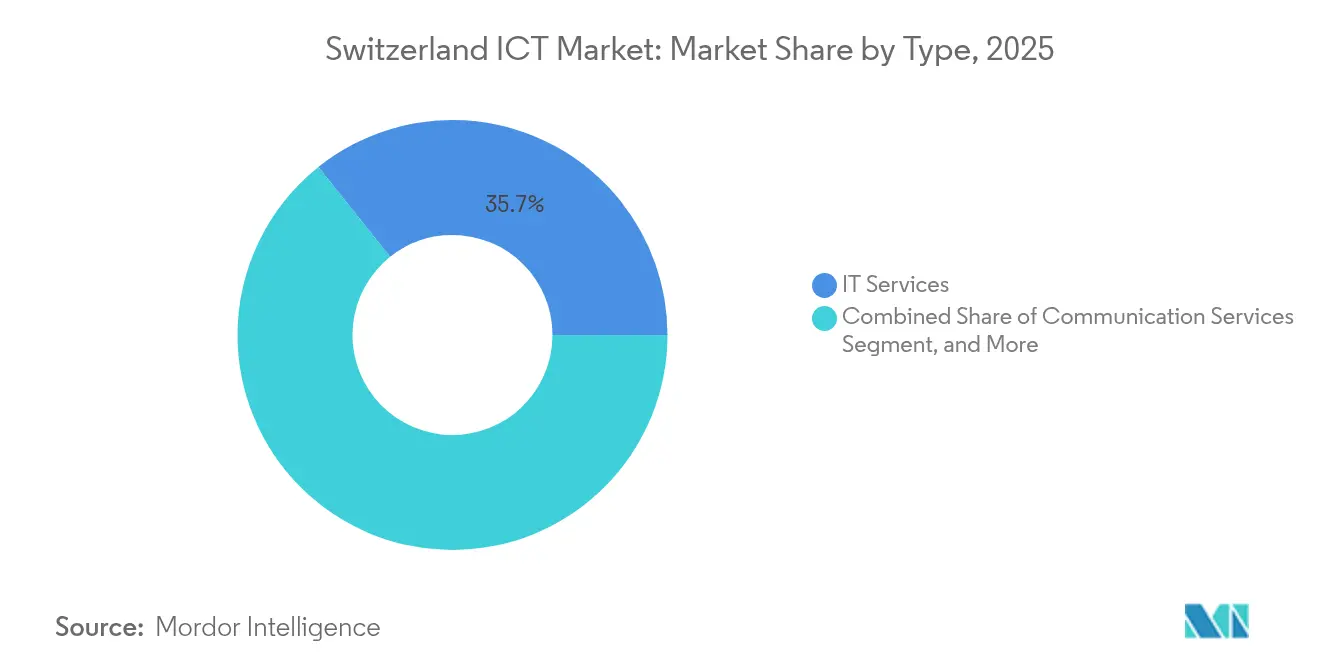

- By type, IT Services led with 35.72% of Switzerland ICT market share in 2025.

- By enterprise size, large enterprises captured 61.10% share of the Switzerland ICT market size in 2025, while SMEs are advancing at a 5.75% CAGR to 2031.

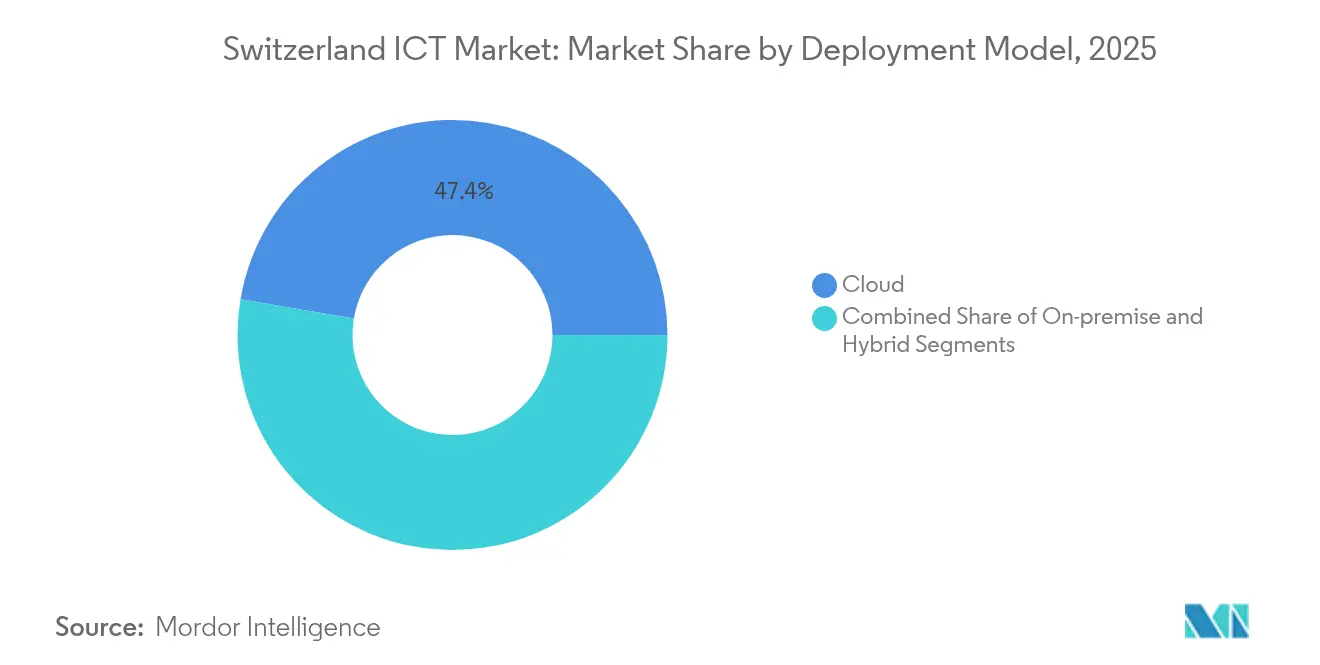

- By deployment model, the cloud segment accounted for 47.35% of Switzerland ICT market share in 2025; hybrid deployments are projected to grow at 6.03% CAGR through 2031.

- By end-user vertical, BFSI held 18.88% share of the Switzerland ICT market size in 2025; gaming and esports records the fastest 6.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid deployment of nationwide 5G network | +0.80% | National (Zurich, Geneva, Basel) | Medium term (2-4 years) |

| Favourable federal digital-innovation funding programmes | +0.60% | National innovation hubs | Long term (≥ 4 years) |

| Cloud-first adoption among Swiss enterprises | +1.20% | Urban centers | Short term (≤ 2 years) |

| High per-capita R&D expenditure on ICT | +0.90% | Tech clusters | Long term (≥ 4 years) |

| Surge in hyperscale and colocation data-center builds | +0.70% | Zurich and Geneva metros | Medium term (2-4 years) |

| Accelerating blockchain uptake within Swiss financial services | +0.40% | Crypto Valley (Zug) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid deployment of nationwide 5G network

Swisscom achieved 99% population coverage by 2024, and Sunrise introduced standalone 5G architecture in 2025, giving enterprises sub-10 millisecond latency for factory automation and autonomous logistics.[1]Mobile Europe, “Swisscom Achieves 99% 5G Coverage,” mobileeurope.co.uk Manufacturers leverage edge servers at 5G base stations to execute AI models that detect quality issues in real time. Logistics firms pilot computer-vision solutions for dynamic routing, improving efficiency and reducing carbon footprints. The network’s density allows pilot projects to scale nationally before rolling out across Europe, creating Swiss intellectual property. These early deployments anchor incremental investments in IoT platforms, cybersecurity, and analytics services within the Switzerland ICT market.

Favourable federal digital-innovation funding programmes

Innosuisse committed CHF 60.4 million (USD 66.4 million) to 33 projects in 2024, channeling capital toward quantum computing, AI, and cybersecurity.[2]Switzerland Global Enterprise, “Federal Innovation Funding Instruments,” s-ge.com Universities collaborate with corporates under Innovation Projects, shortening the lab-to-market cycle. Federal grants de-risk exploratory R&D, enabling local vendors to maintain multi-year research pipelines despite economic cycles. Start-up Coaching nurtures commercialization skills so prototypes convert into scale-ready products. The predictable funding cadence sustains demand for high-performance computing, DevOps services, and specialized software throughout the Switzerland ICT market.

Cloud-first adoption among Swiss enterprises

The revised Federal Act on Data Protection took effect in September 2023, clarifying cross-border processing rules and accelerating multi-cloud strategies.[3]ICLG, “Technology Sourcing Laws and Regulations Switzerland 2024-2025,” iclg.com Domestic providers such as MTF and UMB AG report a wave of hybrid migrations that keep sensitive workloads in country while using hyperscale resources for analytics. Financial firms deploy cloud management platforms to orchestrate data residency and encryption policies, spurring consulting and integration engagements. SMEs adopt software-as-a-service for ERP and CRM, cutting capital expenditure and accessing enterprise-grade security. Collectively, these moves lift demand for managed services, network connectivity, and cybersecurity solutions across the Switzerland ICT market.

High per-capita R&D expenditure on ICT

Private-sector R&D reached CHF 16.8 billion (USD 18.5 billion) in 2021, creating steady need for simulation software, scientific compute, and collaborative research platforms. Pharmaceutical labs require validated data-management systems that trace experiments end-to-end. Precision manufacturers invest in digital twins to simulate micron-level tolerances, pushing demand for GPUs and low-latency networks. Universities hosting 140,000 research staff purchase cloud credits and storage arrays to share datasets globally. The continuous R&D pipeline feeds a virtuous cycle of software development, services spending, and hardware refreshes inside the Switzerland ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and evolving data-privacy regulations (nFADP, GDPR) | –0.5% | National with cross-border | Short term (≤ 2 years) |

| Shortage of advanced ICT talent | –0.7% | Urban tech hubs | Medium term (2-4 years) |

| High electricity tariffs pressuring data-center OPEX | –0.3% | Varies by canton | Long term (≥ 4 years) |

| Swiss franc strength inflates imported hardware costs | –0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex and evolving data-privacy regulations (nFADP, GDPR)

Enterprises handling EU citizen data juggle Swiss and EU regimes, increasing legal review and project scoping costs. Financial-services outsourcers must satisfy FINMA’s Circular 18/03, adding months to vendor onboarding. Cloud migrations pause until firms finalize Standard Contractual Clauses with Swiss-specific amendments. Compliance teams work with security architects on encryption, audit trails, and data-classification schemes, diverting budgets away from innovation. Though frameworks will stabilize, interim uncertainty slows a portion of spending in the Switzerland ICT market.

Shortage of advanced ICT talent in domestic labor pool

Roles such as cloud architects and AI engineers remain scarce, pushing salary inflation and elongating deployment timelines. SMEs resort to managed services because recruiting a full security operations team is impractical. Large banks open technology centers in neighboring Germany and Poland to access broader talent pools while retaining governance in Zurich. Universities update curricula, yet lag the pace of quantum computing and edge-AI skill needs. The talent gap caps the speed at which ambitious digital initiatives translate into realized spending within the Switzerland ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Dominance Drives Market Evolution

IT Services held 35.72% share of the Switzerland ICT market in 2025 and continues growing as enterprises favor outcome-based contracts. Within services, cloud offerings expand at a 5.75% CAGR, adding subscription revenue that buffers vendors from hardware margin pressure. Managed Services win SME budgets by bundling security, backup, and compliance into predictable monthly fees. Business-Process-as-a-Service scales in banking and insurance, where regulatory reporting functions migrate to specialized providers.

Hardware revenue remains vital for high-performance workloads, yet vendors differentiate through vertical expertise in life-sciences lab automation and micro-fabrication. IT infrastructure refresh cycles accelerate to support container orchestration and software-defined networking. Security services command premium pricing as executives prioritize zero-trust architectures. These shifts reinforce a service-centric Switzerland ICT market where integration skills and domain knowledge define competitive advantage.

By Enterprise Size: SME Acceleration Reshapes Market Dynamics

Large enterprises generated 61.10% of value within the Switzerland ICT market size in 2025 owing to multinational headquarters and complex compliance requirements. They continue investing in custom integration and private 5G to digitize global supply chains. However, SMEs post a 5.75% CAGR, narrowing the capability gap through SaaS and low-code platforms. Government programs such as “Digital Switzerland” vouchers offset consulting costs, stimulating first-time cloud adoptions.

SMEs prefer standardized bundles with rapid provisioning, while corporates negotiate multi-vendor frameworks to mitigate lock-in. The divergent buying patterns encourage vendors to segment sales motions and pricing. Talent shortages push smaller firms toward outsourcing, whereas large enterprises establish in-house Centers of Excellence. Over time, SME uplift broadens the Switzerland ICT market’s customer base, reducing dependency on a handful of blue-chip spenders.

By Deployment Model: Hybrid Strategies Balance Innovation and Control

Cloud captured 47.35% Switzerland ICT market share in 2025, but hybrid deployments are the fastest riser at 6.03% CAGR. Enterprises classify workloads by sensitivity, retaining core banking systems on-premises while offloading analytics to public clouds. Cross-connects in Zurich data centers enable latency-sensitive links between private racks and hyperscale zones. Regulatory frameworks under nFADP reinforce the need for local data-stores coupled with foreign compute in a “local data, global processing” model.

On-premises installations remain essential for medical-device telemetry and secure research labs. Meanwhile, multi-cloud governance platforms gain traction, automating policy enforcement across AWS, Azure, and Google Cloud. This nuanced deployment mix necessitates advanced networking, observability, and cost-optimization tools, further enlarging the Switzerland ICT market.

By End-user Industry Vertical: BFSI Leadership Drives Sector Innovation

BFSI accounted for 18.88% of Switzerland ICT market share in 2025, underpinned by blockchain pilots, digital-asset custody, and algorithmic risk analytics. Neo-banks adopt cloud-native core systems, contracting local data-center providers for regulatory comfort. Gaming and esports expand the addressable base at a 6.69% CAGR, spurred by 5G, low-latency streaming, and a progressive stance on tokenized in-game assets.

Manufacturing integrates IoT sensors and AI quality inspection to preserve Switzerland’s precision reputation. Healthcare digitizes clinical pathways and real-world evidence capture through secure patient-clouds. Government modernizes registries and e-voting prototypes, while energy utilities roll out smart-grid analytics that predict renewable supply fluctuations. This vertical mosaic distributes growth drivers, keeping the Switzerland ICT market resilient across economic cycles.

Geography Analysis

Zurich, Geneva, and Basel form the core spending triangle, with ample fiber, multilingual talent, and immediate proximity to decision makers. Zurich alone hosts more than 50% of multinational headquarters, anchoring cloud adoption and cybersecurity investments. Geneva’s mix of international organizations and luxury-goods firms fuels demand for collaboration platforms and high-availability data centers. Basel leverages life-sciences R&D to purchase high-performance compute clusters for molecule simulation.

German-speaking cantons dominate Switzerland ICT market share thanks to industrial density and close ties to Bavarian suppliers. French-speaking Romandy complements growth through cross-border commerce with Lyon and digital-asset services for global NGOs. Italian-speaking Ticino remains smaller but gains traction in fintech sandboxes connecting Swiss privacy-law strength with Italian capital-market proximity.

Regional specialization deepens. Zug’s Crypto Valley houses over 1,000 blockchain entities, spawning demand for secure cloud, audit, and reg-tech solutions. Hyperscalers cluster data centers near Zurich Airport for low-latency European reach, yet electricity tariffs from 10 to 56 Rp/kWh push innovators to experiment with immersion cooling and renewables. Non-EU status enables flexible data-sovereignty positioning, albeit at the cost of dual-regime compliance overhead when serving EU clients.

Competitive Landscape

Competition blends global scale with local nuance. Swisscom, Sunrise, and Salt control connectivity, but hyperscalers such as Microsoft, Google, and AWS co-locate infrastructure to deliver sovereign-cloud offers. IBM, Accenture, and Capgemini partner with Swiss integrators like ELCA and AdNovum, combining regulatory expertise with global delivery. In security, Kudelski and Open Systems leverage Swiss privacy trust to win managed-detection contracts against international peers.

The software domain remains fragmented. Temenos leads in core banking, while Avaloq targets wealth management platforms. Mid-sized specialists Noser Group, Netcetera, and ti and m capture niche mandates in e-government and mobility. Start-ups in quantum key distribution and edge AI attract venture funds from both domestic pension funds and Silicon Valley investors, broadening the innovation funnel.

Strategic moves illustrate dynamism. Swiss Post bought Open Systems in 2024 to add SD-WAN security to its B2B portfolio. Calenso joined JRNI in 2025 to internationalize booking software. Aveniq restructured toward cloud and SAP services after workforce optimization. These maneuvers sharpen competitive positioning and raise the bar for service quality and regulatory alignment across the Switzerland ICT market.

Switzerland ICT Industry Leaders

Microsoft Corporation

Adobe Inc.

AdNovum Informatik AG

Google LLC

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Calenso became part of JRNI, gaining international infrastructure while retaining autonomy

- March 2025: U-Blox divested its cellular division to Trasna, refocusing on GNSS chips

- January 2025: Aveniq reduced staff by 5.8% to concentrate on cloud and security services

- January 2025: Nik Fuchs appointed CEO of itnetX ahead of expanded Microsoft Azure specialization

Switzerland ICT Market Report Scope

The study tracks ICT spending across various industry verticals in the country and highlights key technology preferences among industry verticals, including cloud and artificial intelligence.

The Swiss ICT market is segmented by type (hardware, software, it services, and telecommunication services), size of enterprise (small and medium enterprise, large enterprise), and end-user vertical (BFSI, it and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other end-user verticals). The report provides the market sizes and forecasts in terms of value (USD).

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

Why does BFSI spend the most on tech?

Banking and insurance firms need blockchain, AI risk models, and stringent compliance, giving BFSI 18.88% share in 2025.

What is holding back faster growth?

Dual nFADP/GDPR compliance and a shortage of advanced ICT talent subtract 0.5% and 0.7% from CAGR respectively.

Which Swiss regions host the most data centers?

Zurich and Geneva dominate due to fiber density and proximity to corporate headquarters, despite higher power tariffs.

Who are notable local champions?

Swisscom, Temenos, Kudelski, and Open Systems leverage regulatory expertise and trust to compete with global giants.

How large is the Switzerland ICT market in 2026?

It reached USD 47.18 billion in 2026 and is forecast to climb to USD 61.93 billion by 2031 at a 5.58% CAGR over 2026-2031.

Which deployment approach is growing fastest?

Hybrid deployment shows the highest 6.03% CAGR as firms combine on-premises control with public-cloud scale.

Page last updated on: