Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.97 Billion |

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Cybersecurity Market Analysis by Mordor Intelligence

The Switzerland cybersecurity market size was valued at USD 0.97 billion in 2025 and estimated to grow from USD 1.04 billion in 2026 to reach USD 1.43 billion by 2031, at a CAGR of 6.75% during the forecast period (2026-2031). A confluence of regulatory mandates, rapid digitalization across core industries, and the nation’s longstanding focus on data privacy propel this consistent expansion. Cloud-first strategies, particularly those hosted in Swiss data centers, are accelerating even as on-premise deployments retain primacy among highly regulated banks. Simultaneously, managed detection and response services are gaining favor with organizations that lack in-house expertise. In parallel, the launch of real-time payment rails, the roll-out of connected pharmaceutical manufacturing, and heightened awareness of hybrid threats are each deepening the addressable opportunity for providers across the Switzerland cybersecurity market.

Key Report Takeaways

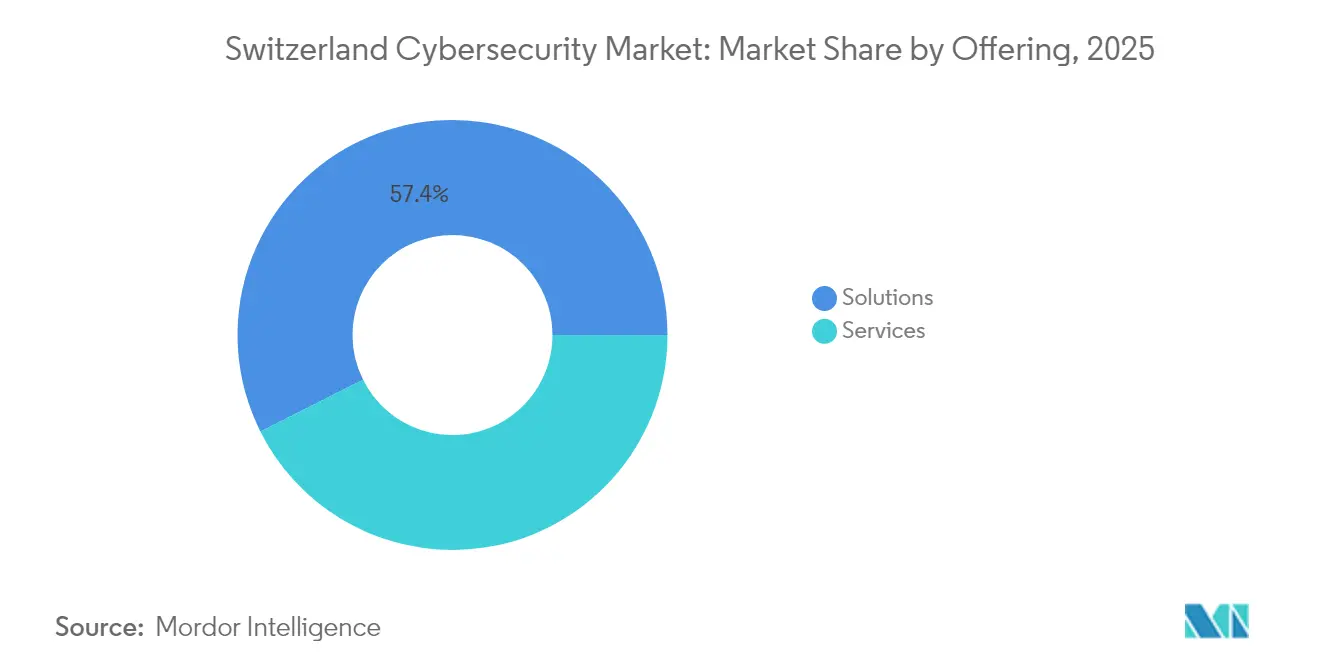

- By offering, solutions led with 57.40 % Switzerland cybersecurity market share in 2025, while services are on track to grow at a 13.20 % CAGR to 2031.

- By deployment mode, on-premise still commanded 64.10 % of the Switzerland cybersecurity market size in 2025; cloud deployments are expanding at a 11.60 % CAGR through 2031.

- By end user industry, the BFSI segment held 28.10 % of the Switzerland cybersecurity market size in 2025, while healthcare exhibit the fastest 12.70 % CAGR to 2031.

- By end-user enterprise size, large enterprises accounted for 69.70 % revenue share in 2025, whereas SMEs are poised for an 10.60 % CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitalization across banking, pharma and manufacturing | +2.1 % | Zurich, Basel, Geneva | Medium term (2-4 years) |

| Revised Federal Act on Data Protection (FADP) | +1.8 % | National | Short term (≤2 years) |

| Surge in sophisticated ransomware attacks | +1.2 % | Cantonal governments & SMEs | Short term (≤2 years) |

| Switzerland’s crypto-asset hub momentum | +0.9 % | Zug, Zurich, Geneva | Medium term (2-4 years) |

| Accelerated cloud and SaaS adoption | +0.8 % | National | Medium term (2-4 years) |

| Government-backed CYD Campus initiatives | +0.4 % | Academic centers | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Rapid Digitalization Across Swiss Banking, Pharma and Manufacturing Elevates Threat Surface

The accelerated rollout of real-time payments, connected drug-production lines and smart factories has expanded the national threat surface. Banks handling SIC Instant Payments manage up to 10,000 daily transactions that must clear fraud and sanctions filters in milliseconds, driving uptake of zero-trust verification at each hop. Pharma plants in Basel now link clinical-trial data with global partners, which forces segmentation of laboratory networks from administrative IT. Likewise, industrial firms merging operational technology with IT understand that a single misconfigured sensor can halt an entire batch, prompting widespread deployment of predictive-monitoring analytics. Collectively, these use-cases advance the Switzerland cybersecurity market toward integrated defense platforms instead of isolated point tools.

Stringent Swiss Federal Act on Data Protection Revision Driving Mandatory Security Spend

The 2023 FADP revision raised executive accountability by imposing personal fines up to CHF 250,000 (USD 313,600) for serious negligence, thereby making cybersecurity spend a board-level necessity [1]SecurePrivacy, “Swiss Federal Act on Data Protection Explained,” secureprivacy.ai. Foreign entities processing Swiss residents’ data must appoint an in-country representative, instantly opening niche advisory demand inside the Switzerland cybersecurity market. Because auditors now test for “privacy by design” controls, solution vendors that can map safeguards to legal clauses enjoy shorter sales cycles. The law’s swift enforcement cadence also explains why managed services with built-in compliance reporting are outgrowing traditional appliances.

Surge in Sophisticated Ransomware Attacks on SMEs and Cantonal Governments

The Play ransomware gang’s 2023 compromise of IT provider Xplain exposed 65,000 classified files and demonstrated how supplier breaches ricochet through federal systems [2]Swiss National Cyber Security Centre, “Xplain Breach Analysis,” ncsc.admin.ch. In response, the National Cyber Security Centre made 24-hour breach reporting mandatory for critical infrastructure beginning April 2025, with fines. The directive spurs firms—especially cantonal agencies and SMEs—to formalize incident-response playbooks and onboard managed detection partners. Remarkably, attackers now craft Swiss German and French phishing lures using AI text models, raising defense complexity and propelling email-security subscriptions across the Switzerland cybersecurity market.

Switzerland’s Crypto-Asset Hub Status Necessitates Advanced FinTech Security

Home to more than 1,100 blockchain ventures, Zug’s “Crypto Valley” attracts sophisticated adversaries seeking to exploit smart contracts and wallet infrastructure. FINMA guidance now anticipates end-to-end key-management controls for tokenized assets, pushing vendors to embed crypto-specific safeguards into conventional banking platforms. Banks experimenting with digital securities increasingly request offerings that marry ISO 27001 frameworks with on-chain analytics, blending two historically separate domains and enlarging total addressable spend within the Switzerland cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of certified cyber-talent | −1.5 % | Rural cantons > cities | Medium term (2-4 years) |

| High cost sensitivity among SMEs | −1.0 % | National | Short term (≤2 years) |

| Data-residency concerns for cloud workloads | −0.8 % | National | Medium term (2-4 years) |

| Fragmented federal vs cantonal compliance layers | −0.5 % | Varies by canton | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Certified Cyber-talent in Swiss Regions

An ENISA survey found 89 % of Swiss organizations anticipate adding cybersecurity staff, yet vacancies persist for months, inflating wages and delaying projects. Rural cantons struggle most, compelling firms to automate baseline monitoring and lean heavily on managed detection services. Universities and the CYD Campus expand graduate pipelines, but near-term relief is limited, a dynamic that directs incremental budget into day-one-operational offerings across the Switzerland cybersecurity market.

High Cost Sensitivity Among SMEs Toward Advanced Solutions

Three in five Swiss SMEs that suffer a major breach cease operations within six months, yet budget ceilings still deter adoption of comprehensive defenses. Vendors respond with modular, pay-as-you-grow bundles that cover essentials: endpoint protection, cloud email security and encrypted backup. Insurance carriers have begun discounting premiums for SMEs that meet baseline security-control checklists, effectively subsidizing adoption and partially offsetting this restraint for the Switzerland cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Race Ahead of Solutions

Solutions held 57.40 % Switzerland cybersecurity market share in 2025, but ervices are on track for a 13.20 % CAGR through 2031. Growth correlates with a 60,000-person skills gap that drives buyers toward outcome-based contracts. Identity and access-management suites now ship natively in SaaS form, and new MDR offerings promise sub-15-minute containment windows, delivering measurable reductions in dwell time. Vendors that couple consulting, implementation and MDR under one invoice report renewal rates above 95 %, underscoring the value of integrated portfolios.

The surge in services also reflects boardroom comfort with opex budgeting. Kudelski Security’s FusionDetect™ XDR platform delivered a 249 % four-year ROI according to an independent study, energizing demand for outsourced detection . Government agencies likewise tender multi-year MDR contracts to satisfy 24-hour reporting rules, widening public-sector revenue channels. Overall, managed offerings are poised to command an even greater portion of the Switzerland cybersecurity market by decade’s end.

By Deployment Mode: Cloud Acceleration Balances Sovereignty

On-premise deployments controlled 64.10 % of the Switzerland cybersecurity market size in 2025, yet cloud-hosted controls are advancing at a 11.60 % CAGR. Healthcare providers lean into Swiss-hosted clouds that meet FADP data-residency provisions while enabling cross-hospital record sharing. The hybrid model—sensitive data on premises, analytics in the cloud—emerges as the dominant architecture, letting CISOs fine-tune risk tolerance by workload.

Organizations also adopt SCION-based path-aware networking, funded by ventures such as Anapaya Systems, to guarantee data stays on Swiss soil during cloud hops. As native cloud controls prove audit-ready and hyperscalers add Swiss regions, cultural resistance erodes and incremental spend gravitates toward subscription-based security tools, reinforcing cloud’s climb inside the Switzerland cybersecurity market.

By End-user Industry: Healthcare Outpaces Traditional Banking Leadership

BFSI retained a 28.10 % slice of the Switzerland cybersecurity market size in 2025, reflecting decades of security investment. Yet healthcare & life sciences outstrip all verticals with a 12.70 % CAGR to 2031. Programs like DigiSanté that mandate interoperable electronic health records compel hospitals to invest in encryption, multi-factor authentication and continuous compliance tooling.

Banks meanwhile confront tokenization and open-banking APIs. They pilot blockchain custody modules that merge SWIFT-level controls with smart-contract audits, deepening vendor requirements. Manufacturers on the other hand focus on OT segmentation and AI-based anomaly detection across factory floors. Collectively, these divergent needs keep the Switzerland cybersecurity market diversified by end-user spend, reducing over-reliance on any single sector.

By End-user Enterprise Size: SMEs Narrow the Protection Gap

Large enterprises contributed 69.70 % of Switzerland cybersecurity market revenue in 2025. However, SMEs are accelerating at an 10.60 % CAGR, spurred by regulatory obligations that now apply to supply-chain partners. Secnovum’s “cyber-fitness” campaigns and simplified questionnaires help smaller firms identify priority controls without drowning in jargon.

Peer recommendations inside regional chambers of commerce often dictate purchase lists, so vendors invest in multilingual collateral to win trust. Consumption-based licenses that start below CHF 1,000 per month lower entry barriers, and once an SME onboards basic protection, upsell conversations pivot on concrete metrics such as phishing click-through reductions. The trend draws fresh entrants specializing in right-sized packages, thereby broadening competitive intensity across the Switzerland cybersecurity market.

Geography Analysis

Zurich anchors the Switzerland cybersecurity market, housing global banks, fintech incumbents and a dense start-up ecosystem. Strong university pipelines feed research labs, yet competition from financial institutions means independent vendors must offer equity or remote flexibility to secure talent. Regulatory bodies headquartered in the city facilitate rapid feedback loops between law drafts and product designs, giving local providers a home-field advantage. Demand concentrates on identity-first security, driven by real-time payments and open-finance APIs.

Basel follows, propelled by life-sciences titans that treat intellectual-property leakage as existential risk. Here, biomedical cybersecurity consultancies embed bio-ethicists alongside security engineers, reflecting dual obligations to protect patient privacy and trade secrets. Cross-border workforce flows with Germany and France introduce multilingual spear-phishing vectors, so companies showcase tri-lingual awareness programs. Pilot deployments of zero-trust micro-segmentation inside laboratory environments are later replicated in production plants, reinforcing ecosystem learning.

In Geneva and neighboring cantons, international organizations and commodity traders demand dual compliance with Swiss and EU regulations. Vendors fluent in both legal frameworks command premium retainers. The city’s status as a diplomatic hub heightens fear of espionage, leading to above-average investment in data-loss-prevention suites and secure collaboration platforms. Rural cantons lag, yet federal subsidies and shared Security Operations Centers aim to close this gap, expanding the Switzerland cybersecurity market’s geographic footprint.

Competitive Landscape

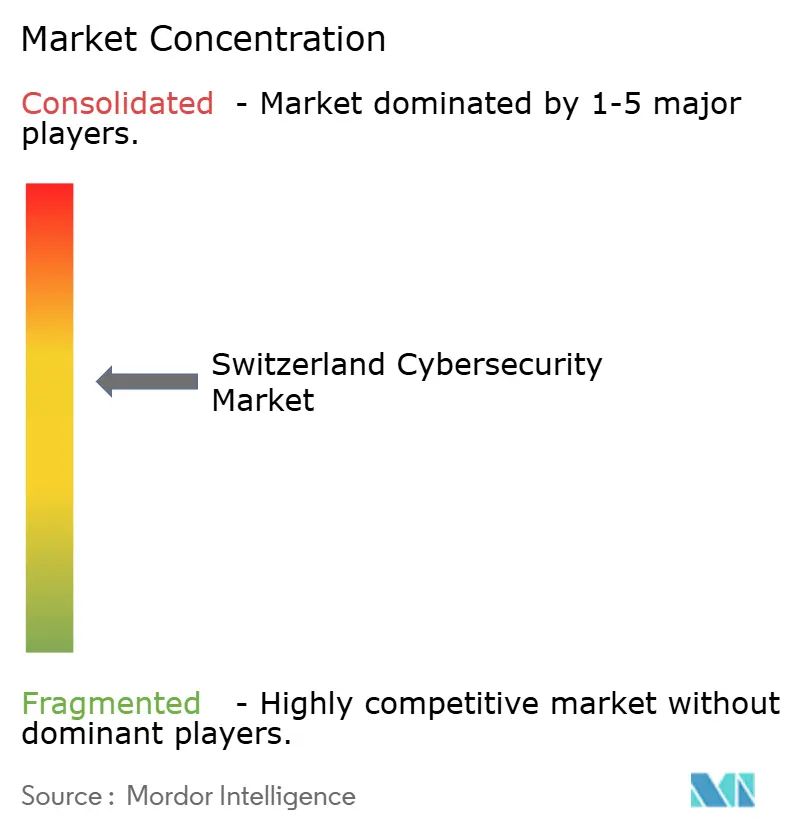

Global suppliers such as IBM, Cisco and Microsoft maintain broad product portfolios that appeal to multinational clients, yet they must localize for strict Swiss data-sovereignty rules. Domestic champions—including Swisscom, Kudelski Security, InfoGuard AG and Exeon Analytics—capitalize on canton-specific compliance know-how and bilingual service desks, often edging multinationals in public-sector bids. The resulting equilibrium prevents any firm from exceeding 15 % revenue share, signaling moderate concentration within the Switzerland cybersecurity market.

M&A activity underscores an appetite for cloud-native and service-centric expansion. Swiss Post’s 2024 acquisition of Open Systems integrated secure access service edge (SASE) capabilities into its existing communication portfolio, aligning with the surge in remote work and hybrid cloud adoption [4]Swiss Post, “Acquisition of Open Systems Completes,” post.ch. VINCI Energies’ purchase of Fernao Group added 600 cybersecurity consultants across the DACH region, boosting bench strength for complex infrastructure projects. Such deals highlight a race to combine scale with specialized expertise.

Investment flows mirror strategic bets on automation and quantum-resilient encryption. Kudelski Security’s USD 166 million funding round in 2024 accelerates deployment of its FusionDetect™ XDR across Europe. Meanwhile, start-ups in Zug raise seed capital to fuse on-chain analytics with ISO-aligned controls, bridging gaps between crypto custody and traditional finance. Competitive differentiation thus hinges on cross-domain skill sets, continuous compliance reporting and rapid threat-intel integration—all increasingly non-negotiable for winning share in the Switzerland cybersecurity market.

Switzerland Cybersecurity Industry Leaders

Swisscom

Kudelski Security

IBM Corporation

Fortinet Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Trust Valley has rolled out Trust4SMEs, a pilot initiative aimed at bolstering cybersecurity for 25 SMEs in the Lake Geneva area.

- January 2025: HUB Cyber Security Ltd. announced its acquisition of BlackSwan Technologies for expanded financial-sector offerings.

- October 2024: Swiss Post completed its purchase of Open Systems, adding SASE expertise to its service catalog.

- July 2024: Kudelski Security raised USD 166 million from Farallon Capital Management, earmarked for MDR expansion.

Switzerland Cybersecurity Market Report Scope

Cybersecurity solutions enable an organization to monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware, malware, and phishing to maintain data confidentiality.

The Switzerland cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What revenue will the Switzerland cybersecurity market generate by 2031?

The market is expected to reach roughly USD 1.43 billion by 2031, growing at a 6.75% CAGR from 2026.

Why is healthcare driving fresh demand for cybersecurity solutions?

Digitization of patient records and telemedicine under frameworks like DigiSanté requires encryption, multi-factor authentication and strict audit controls, fueling a 12.70 % CAGR in healthcare spend.

How do Swiss data-sovereignty rules influence cloud adoption?

They encourage hybrid architectures that retain sensitive datasets on Swiss soil while running analytics in domestic cloud regions, spurring local data-center investment.

Are SMEs actively investing despite cost pressures?

Yes. Tiered, pay-as-you-grow bundles and insurance premium discounts motivate smaller firms to adopt baseline defenses, leading to an 10.60 % CAGR in SME security outlays.

Page last updated on: