Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

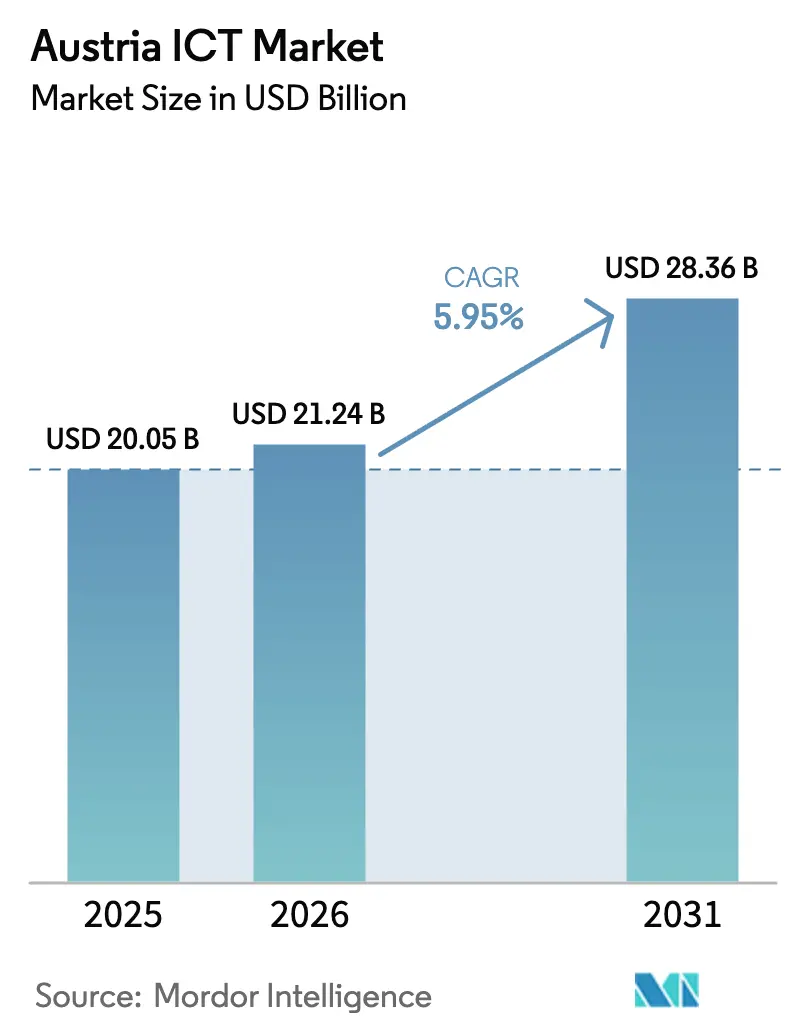

| Base Year Market Size (2025) | USD 20.05 Billion |

| Market Size (2026) | USD 21.24 Billion |

| Market Size (2031) | USD 28.36 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria ICT Market Analysis by Mordor Intelligence

Austria ICT market size in 2026 is estimated at USD 21.24 billion, growing from 2025 value of USD 20.05 billion with 2031 projections showing USD 28.36 billion, growing at 5.95% CAGR over 2026-2031. Digital-bridge positioning between Western Europe and the CEE region, Vienna’s ascent as a hyperscale data-center hub, and aggressive public-sector digitalization sustain the current growth curve. Federal cloud-first rules, EU-funded SME up-skilling grants, and nationwide 5G + FTTH roll-outs generate steady enterprise and household demand. Competitive intensity deepens as global hyperscalers and incumbent telecom operators contest contracts that increasingly require data-sovereignty compliance. Nonetheless, the Austria ICT market encounters structural friction from a chronic talent shortfall, elevated electricity tariffs for data-center operators, and economic caution within export-oriented manufacturers.

Key Report Takeaways

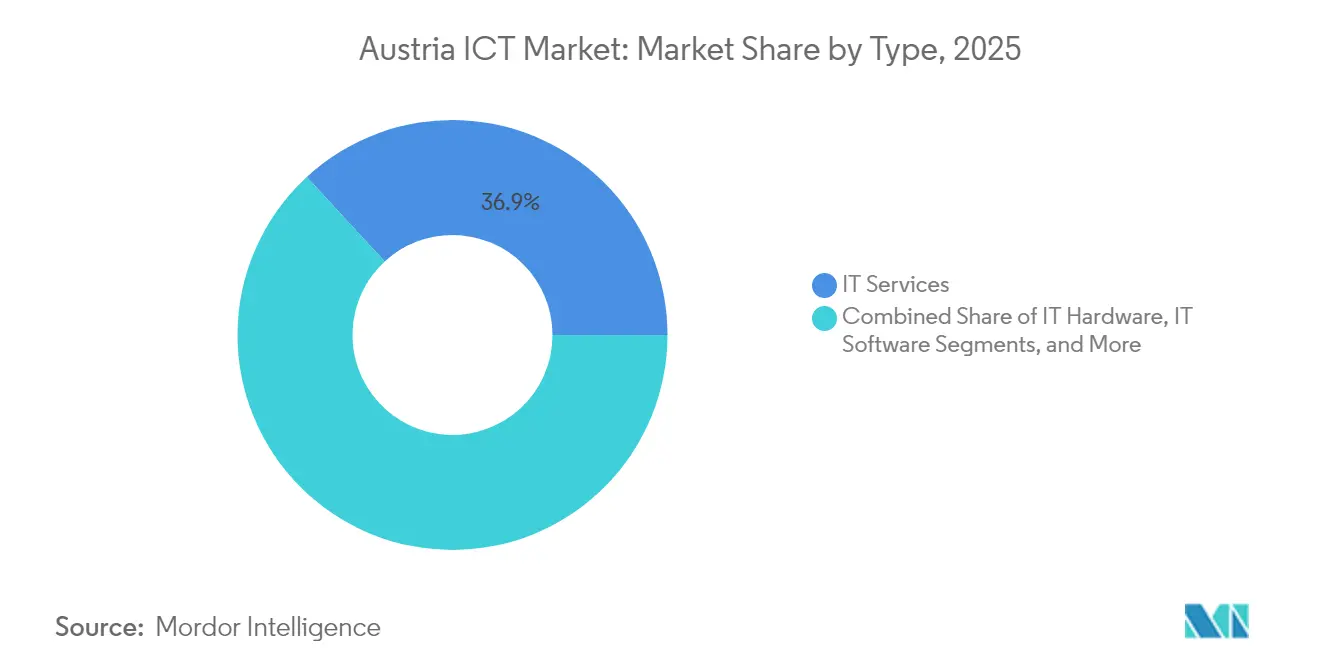

- By type, IT services led with 36.85% of the Austria ICT market share in 2025; cloud services are projected to expand at a 6.18% CAGR through 2031.

- By enterprise size, large enterprises held 62.80% of the Austria ICT market size in 2025, while SMEs record the highest projected CAGR at 6.5% to 2031.

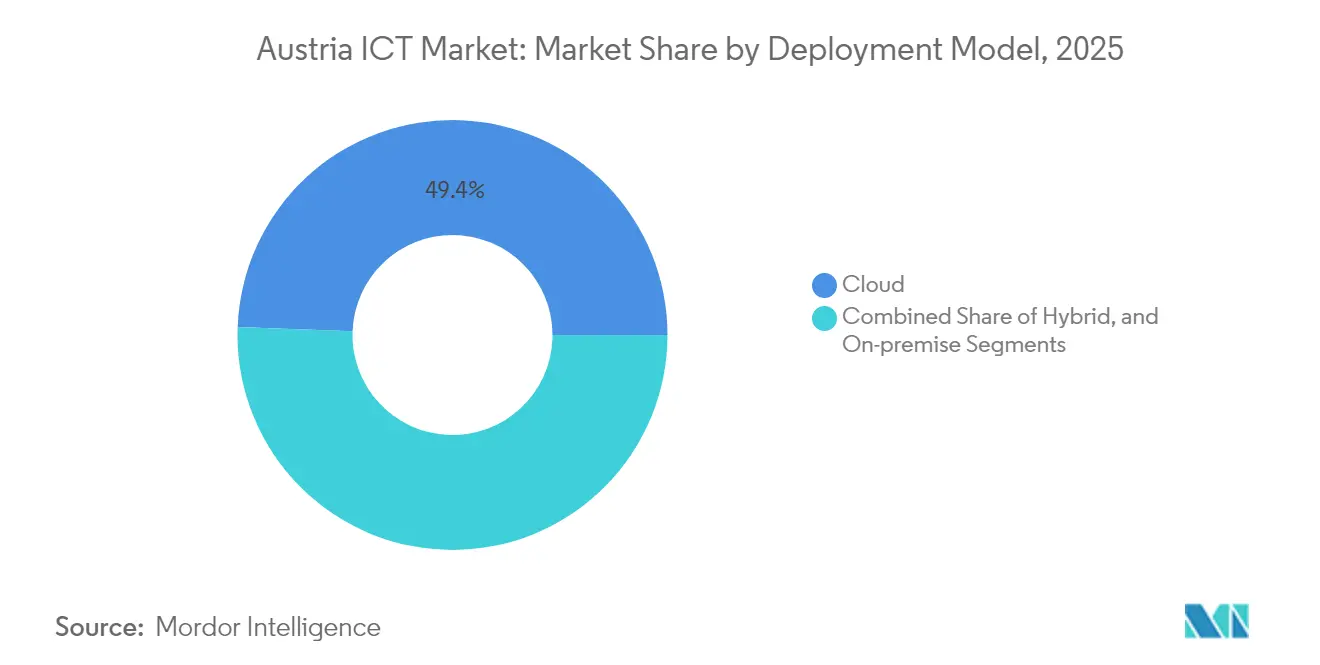

- By deployment model, cloud captured 49.40% revenue share in 2025 and is advancing at a 6.55% CAGR through 2031.

- By end-user vertical, government and public administration accounted for a 17.10% share of the Austria ICT market size in 2025, whereas gaming and esports will accelerate at a 6.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation of public services | +1.2% | Vienna and state capitals | Medium term (2-4 years) |

| Nationwide 5G and FTTH deployment | +0.9% | Urban centers first | Short term (≤ 2 years) |

| EU-funded SME up-skilling subsidies | +0.7% | Rural emphasis | Medium term (2-4 years) |

| Federal cloud-first procurement | +0.8% | Countrywide | Short term (≤ 2 years) |

| Near-shoring CEE data-center workloads | +0.6% | Vienna metro & Lower Austria | Long term (≥ 4 years) |

| Vienna smart-city carbon-neutral goals | +0.4% | Vienna region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G and Fiber Infrastructure Acceleration Drives Enterprise Spending

Nationwide 5G availability combined with fiber-to-the-home connections to 1.2 million households creates the low-latency backbone required for cloud migration and Industry 4.0 roll-outs. Manufacturing clusters in Upper Austria and Styria now pilot real-time analytics and IoT sensor grids reliant on sub-10 ms round-trip times. Operators reported 15% growth in enterprise data-service revenue after businesses increased their Austria ICT market budgets by 8.2% in 2024.

EU Digital Upskilling Subsidies Unlock SME Potential

The KMU.DIGITAL program disburses grants covering up to 80% of cloud, cybersecurity, and e-commerce costs for eligible firms. With USD 327 million allocated through 2027, SMEs that join post 23% productivity gains, catalyzing peer adoption across the 330,000-strong SME base. Participation already reaches 35% in Tyrol and Vorarlberg, underscoring untapped demand in eastern regions.

Federal Cloud-First Policies Create Vendor Consolidation Pressure

Since 2024, every new federal IT project must be cloud-evaluated first, repurposing a USD 3.47 billion annual segment. Procurement centralization through the Federal Computing Center standardizes architectures and favors suppliers with hybrid cloud capabilities. European providers and local data centers gain a sovereignty edge as ministries insist on in-country data residency.[1]Republic of Austria, “Digital Austria Act – 117 Digitalization Measures,” digitalaustria.gv.at

Vienna Smart-City Initiatives Generate Specialized ICT Demand

A USD 890 million pipeline in smart grids, digital twins, and urban analytics emerges as Vienna pursues carbon neutrality by 2040. The 2024 digital-twin launch requires dense IoT sensing and edge processing across 220,000 public buildings, steering opportunities toward vendors with proven municipal integration credentials. Comparable programs budgeted at USD 445 million spread to Graz, Linz, and Salzburg through 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight IT-talent pipeline | -0.8% | Vienna and Graz hubs | Short term (≤ 2 years) |

| Macroeconomic slowdown | -0.6% | Manufacturing belts | Medium term (2-4 years) |

| Cyber-sovereignty limits on hyperscalers | -0.4% | Federal and enterprise | Long term (≥ 4 years) |

| High electricity costs for data centers | -0.3% | Vienna and Lower Austria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IT Talent Shortage Constrains Service Delivery

Austria posts 24,000 unfilled ICT vacancies against 3,200 annual graduates, inflating wages 12% each year. Cybersecurity proves most constrained, with 75% of firms unable to source specialists, forcing premium consultancies or project delays. Salary bands of USD 98,000-130,000 for senior roles erode service-provider margins and limit the Austria ICT market’s capacity to scale.

Economic Uncertainty Delays Enterprise Transformation

Energy-cost volatility and supply-chain disruptions erode manufacturing cash flows, prompting 7% cuts in mid-market ICT budgets during 2024. CFOs defer multi-year modernization and focus on essential compliance projects, lengthening decision cycles and tempering the Austria ICT market growth in export-oriented industries.[2]Austrian National Bank, “Economic Outlook 2024,” oenb.at

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Leadership Amid Cloud Transformation

The segment accounts for 36.85% of the Austria ICT market share in 2025 while cloud services log a 6.18% CAGR, underscoring a pivot from on-premises assets to consumption-based models. The Austria ICT market size tied to IT services benefits from outsourcing appetite among 330,000 SMEs lacking internal staff. Demand for hybrid-cloud architectures strengthens as companies seek performance parity with sovereignty compliance.

Hardware refresh cycles stay stable in manufacturing and banking yet shift toward edge-optimized devices supporting IoT analytics. SaaS subscriptions lift software growth, while security outlays climb as daily incident ratios surge to 22%. Telecom operators leverage fiber and 5G footprints to bundle transformation consulting, creating convergence between connectivity and IT outsourcing.

By Enterprise Size: SME Acceleration Challenges Large-Enterprise Dominance

Large enterprises deliver 62.80% of 2025 revenue but their incremental expansion moderates as projects mature. EU grants push SMEs to a 6.5% CAGR, injecting fresh volume into the Austria ICT market size. Standardized migration bundles from firms such as CANCOM Austria reduce cost and complexity, accelerating adoption among resource-constrained owners.

SMEs now view cloud storefronts and cybersecurity certification as prerequisites for export contracts, while large enterprises reallocate budgets toward AI optimization and continuous compliance. Vendors capable of offering modular solutions, regional language support, and bundled financing capture the outsized momentum in this customer tier.

By Deployment Model: Cloud Dominance Reflects Sovereignty Concerns

Cloud deployments hold 49.40% of 2025 revenue and rise at 6.55% CAGR. Hybrid architectures dominate design briefs, allowing sensitive workloads to remain on-premise while benefiting from public-cloud elasticity. The Austria ICT market share for on-premise infrastructure stabilizes in regulated health and banking segments where in-country data residency is mandated.

Federal cloud-first rules accelerate SaaS adoption, yet procurement clauses favor European providers to mitigate extraterritorial jurisdiction risks. This dynamic spurs hyperscalers to open Vienna regions and offer contractual sovereignty add-ons, while local integrators orchestrate multi-cloud governance for risk-averse enterprises.

By End-User Industry Vertical: Gaming Disrupts Traditional Hierarchies

Government and public entities absorb 17.10% of 2025 spending, propelled by 117 federal digital measures. Gaming and esports lead growth at 6.85% CAGR as Austria’s 5.3 million player base and official sport recognition trigger infrastructure upgrades. BFSI digitization advances with AI advisory pilots, whereas manufacturing trails the EU cloud-adoption average, highlighting latent upside.

Healthcare spending normalizes post-pandemic but telemedicine and electronic records keep momentum. Retail and logistics funnel double-digit e-commerce growth into omnichannel fulfillment and last-mile analytics, diversifying revenue for platform providers in the Austria ICT industry.

Geography Analysis

Vienna commands roughly 44% of Austria ICT market spending due to federal government projects, financial services headquarters, and concentrated data center capacity. Microsoft’s USD 1.09 billion region plus AtlasEdge edge nodes deepen the capital’s gravity for hyperscale and edge workloads, enabling sub-5 ms connectivity to major EU metros.

Industrialized Upper Austria and Styria rank next in value as automotive and machinery clusters deploy IoT, MES, and predictive maintenance stacks. Western states Tyrol and Vorarlberg exhibit the highest SME grant uptake at 35%, signaling robust grassroots digitalization despite smaller population bases.

Austria’s EU membership and stable regulatory climate allow ICT providers to pilot GDPR-compliant services locally and then export across the single market. Netskope’s Vienna launch typifies suppliers leveraging central location, skilled labor, and pan-EU rail-and-fiber corridors to serve CEE customers seeking sovereign cloud access.

Competitive Landscape

The Austria ICT market features moderate fragmentation where top telecom incumbents, global cloud platforms, and mid-sized integrators share influence. A1 Telekom Austria extends beyond connectivity into managed services, while Magenta Telekom and Hutchison Drei monetize 5G private-network projects. Hyperscalers Microsoft, AWS, and Google intensify regional hiring after local-zone launches, heightening price and service competition.

Data-sovereignty clauses elevate European clouds and Vienna-based colocation specialists that guarantee in-country data residency. CANCOM Austria, T-Systems, and Bechtle exploit this opening by integrating multi-cloud orchestration with cybersecurity operations centers that address the talent shortage pain point for mid-market clients.

Global consultancies such as Capgemini, Accenture, and Atos chase large-enterprise outsourcing renewals but must localize to Austria’s German-language workflows and stringent public-sector procurement rules. SME-tailored bundles, managed detection-and-response offerings, and vertical smart-city solutions remain fertile whitespace for agile domestic providers.

Austria ICT Industry Leaders

A1 Telekom Austria AG

Amazon Web Services, Inc.

Atos SE

Capgemini SE

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Microsoft opened its USD 1.09 billion Vienna data-center campus, provisioning capacity for 500,000+ regional customers.

- November 2024: A1 Telekom Austria partnered with Ericsson on a USD 218 million private-5G program for 150+ manufacturing facilities.

- October 2024: The Federal Computing Center awarded IBM Austria a USD 164 million hybrid-cloud modernization contract.

- September 2024: UNIQA Insurance Group launched an USD 87 million tri-country cloud and AI upgrade.

Austria ICT Market Report Scope

Austria's ICT market delves deep into pivotal tech investments, spotlighting areas like cloud technologies as well as artificial intelligence.

Austria's ICT Market is segmented by type (hardware, software, IT services, telecommunication services), by size of the enterprise (small and medium enterprises, large enterprises), by end-user vertical (BFSI, IT & telecom, government, retail, and e-commerce, manufacturing, energy, and utilities, and other industry verticals). The market sizes and forecasts are in terms of value (USD) for all the above segments.

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Deployment Model

| On-premise |

| Cloud |

| Hybrid |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

What is the current value of the Austria ICT market?

The Austria ICT market stands at USD 21.24 billion in 2026.

How fast is the Austria ICT market expected to grow?

The market is projected to rise to USD 28.36 billion by 2031, reflecting a 5.95% CAGR.

Which segment shows the highest revenue share?

IT services lead with 36.85% of 2025 revenue.

Which deployment model is growing fastest?

Cloud deployments post the highest CAGR at 6.55% through 2031.

Why is the talent shortage a concern for providers?

Austria faces 24,000 unfilled ICT roles, pushing wages up and constraining project capacity.

Which vertical is expanding most rapidly?

Gaming and esports record the strongest growth at a 6.85% CAGR to 2031.

Page last updated on: