Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 53.43 Billion |

| Market Size (2026) | USD 55.01 Billion |

| Market Size (2031) | USD 63.64 Billion |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel ICT Market Analysis by Mordor Intelligence

The Israel ICT market size is expected to increase from USD 55.01 billion in 2026 to USD 63.64 billion by 2031, growing at a CAGR of 2.95% over 2026-2031. Steady expansion reflects widening cloud adoption, digital-government spending, and spillover from defense technology. Demand continues to pivot toward high-margin IT services as organizations trade capital-intensive hardware refreshes for operating-expense cloud subscriptions. Nationwide 5G-fiber rollouts and a resilient venture-capital ecosystem are raising the ceiling for data-heavy applications, while sovereign AI infrastructure reduces latency and data-residency risk. At the same time, talent shortages, geopolitical tension, and export-control limits on advanced GPUs temper the overall growth trajectory of the Israel ICT market.

Key Report Takeaways

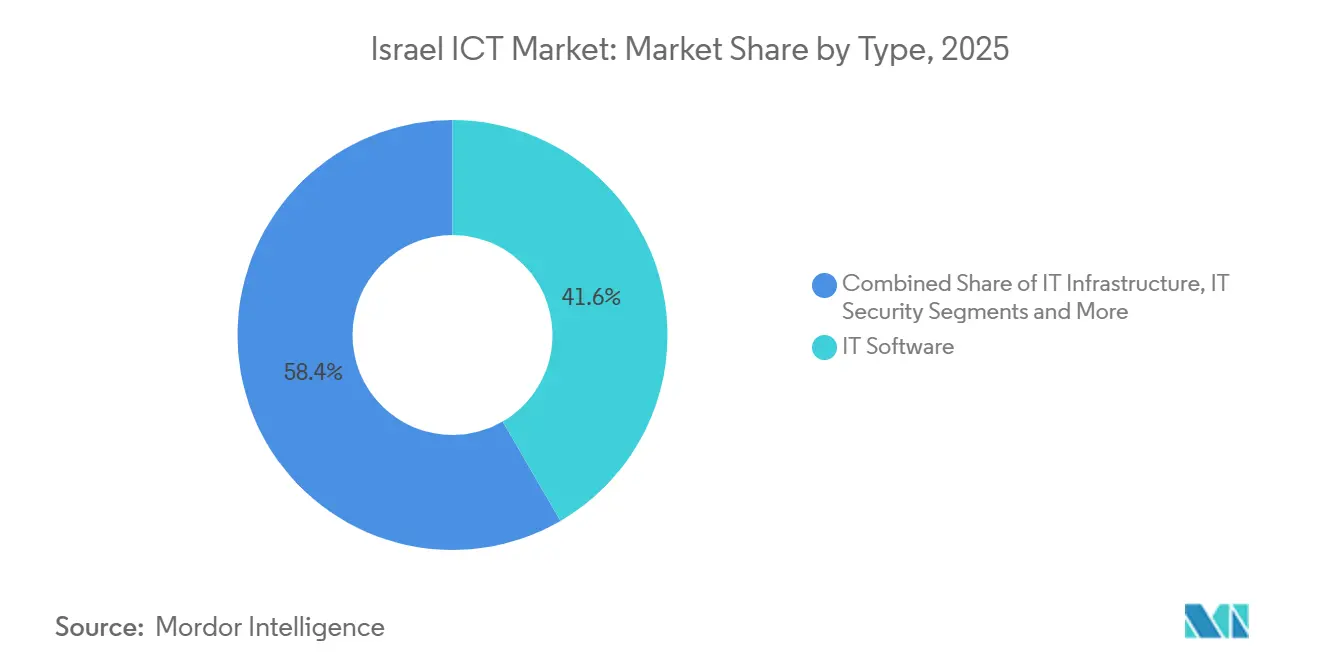

- By type, IT software led with 41.63% of the Israel ICT market share in 2025 and IT services is expanding at a 4.32% CAGR through 2031, underpinned by managed security and multi-cloud consulting.

- By enterprise size, large enterprises accounted for 63.74% of 2025 spending of the Israel ICT market, but small and medium enterprises are advancing at a 4.52% CAGR, catalyzed by the SHAAM e-invoicing mandate.

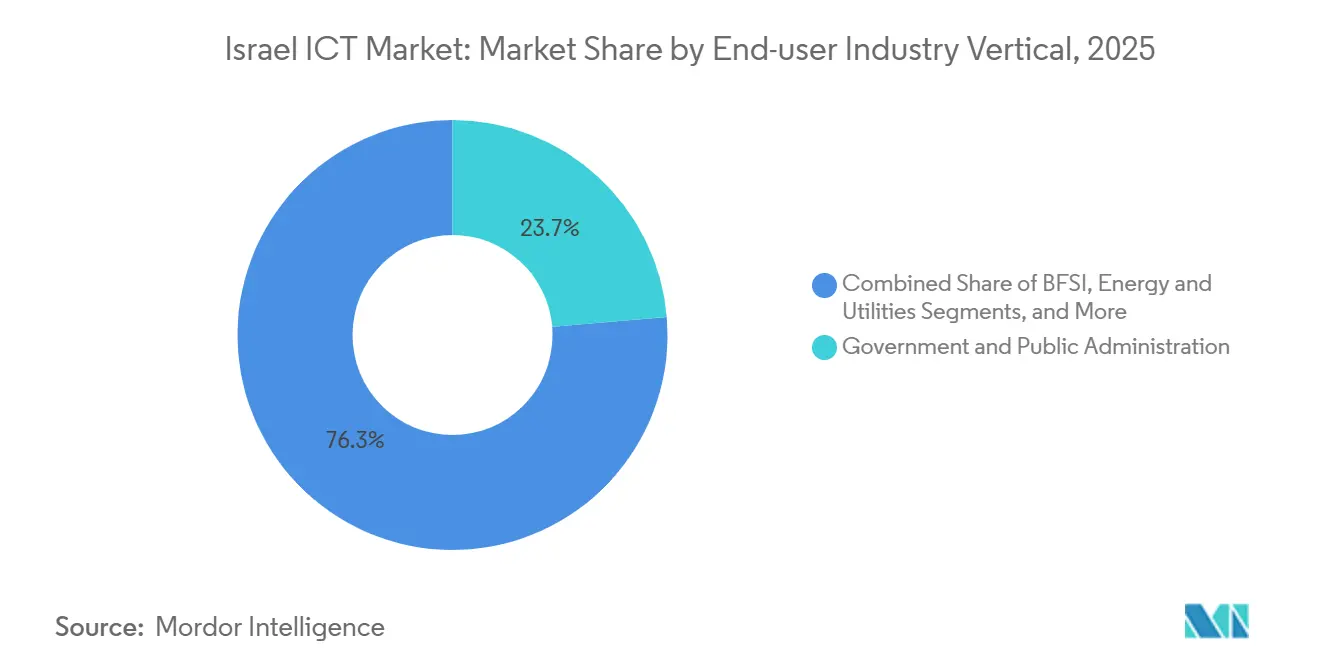

- By end-user industry, government and public administration held 23.74% of 2025 revenue of the Israel ICT market, while manufacturing is the fastest-growing vertical at a 3.89% CAGR, supported by roughly 230 Industry 4.0 startups.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Led Digital Israel and Project Nimbus Initiatives | +0.8% | National, concentrated in Tel Aviv, Jerusalem, Haifa metropolitan corridors | Medium term (2-4 years) |

| Nationwide 5G-Fiber Rollout Boosting Bandwidth Supply | +0.6% | National, with accelerated deployment in Tel Aviv, Haifa, Beersheba | Short term (≤ 2 years) |

| Venture-Capital Depth and World-Leading R&D Spend | +0.7% | National, spillover to regional innovation hubs in Beersheba, Haifa | Long term (≥ 4 years) |

| Hyperscale Cloud Region and Sovereign AI Supercomputing Capacity | +0.5% | National, with data-center concentration in central and northern Israel | Medium term (2-4 years) |

| Defense-Tech Spillover Accelerating Dual-Use ICT Innovation | +0.4% | National, strongest in Tel Aviv and Herzliya cyber corridors | Long term (≥ 4 years) |

| Hebrew-Arabic NLP Ecosystem Enabling Hyper-Local AI Solutions | +0.3% | National, with research centers in Jerusalem, Tel Aviv, Haifa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led Digital Israel and Project Nimbus Initiatives

Expanded budgets and strict service-accessibility rules are reshaping procurement cycles across ministries. January 2026 funding of NIS 40 million (USD 11.4 million) supports 13 AI projects, building on earlier pilots that validated cross-agency data-sharing platforms.[1]Government of Israel, “Digital Israel Initiative and AI Projects Announcement,” gov.il Dual sovereign-cloud regions operated by AWS and Google comply with local data-sovereignty law and accelerate migration of sensitive workloads.[2]AWS, “Project Nimbus: Sovereign Cloud Regions in Israel,” amazon.com The National Digital Directorate’s 2026 allocation of NIS 534.4 million (USD 152 million) funds shared APIs and synthetic data services. Mandatory WCAG 2.1 level-AA accessibility by December 2026 drives front-end modernization, and ISO 27001 is now baked into public tenders, channeling new contracts to integrators that specialize in compliance.

Nationwide 5G-Fiber Rollout Boosting Bandwidth Supply

Bezeq passed 2.72 million homes with fiber by Q1 2025 and signed 885,000 subscribers, a 32.5% penetration rate. Operators are deploying standalone 5G cores on newly auctioned 3.5 GHz and 26 GHz spectrum, opening ultra-low-latency use cases for manufacturing and logistics. A 2025 survey showed that SMEs with gigabit connectivity were 2.3 times more likely to adopt cloud ERP than DSL-dependent peers. Converged fixed-mobile packages bundle SD-WAN and security-as-a-service, turning connectivity providers into managed-service partners and expanding the Israel ICT market.

Venture-Capital Depth and World-Leading R&D Spend

Israel’s R&D intensity was 6.3% of GDP in 2023, the highest among OECD countries.[3]OECD, “Israel Economic Survey 2024-2025: Innovation and Technology Sector Analysis,” oecd.org Startups raised USD 11.0 billion in 2025, with cybersecurity capturing 43% of the total. Half of the founders with exits above USD 100 million served in IDF Unit 8200, seeding deep expertise in cryptography and real-time data pipelines. The Israel Innovation Authority’s 2026 budget rose 15% to NIS 2.2 billion (USD 626 million), widening early-stage grant coverage. Mega-deals such as Google’s USD 32 billion purchase of Wiz illustrate investor confidence, drawing fresh international capital into the Israel ICT market.

Hyperscale Cloud Region and Sovereign AI Supercomputing Capacity

AWS and Google Cloud regions launched under Project Nimbus let regulated entities process classified data locally. Parallel public funding of NIS 160 million (USD 45.5 million) enabled the creation of a Nebius-operated supercomputer with 1,000 NVIDIA B200 GPUs. NVIDIA is adding a USD 500 million R&D cluster with “several thousand” GPUs in northern Israel. These assets form a hybrid backbone that anchors AI startups, defense analytics, and sovereign SaaS workloads, cushioning the Israel ICT market from U.S. export-control quotas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical Conflict and Macro Uncertainty | -0.9% | National, with acute effects in southern and northern border regions | Short term (≤ 2 years) |

| Persistent Tech-Talent Shortages and Wage Inflation | -0.6% | National, most severe in Tel Aviv, Herzliya, Haifa technology corridors | Medium term (2-4 years) |

| GPU and High-End Compute Bottlenecks for AI Workloads | -0.4% | National, affecting AI startups and research institutions | Short term (≤ 2 years) |

| Tighter Foreign-Investment Screening on Sensitive ICT Assets | -0.3% | National, concentrated in cybersecurity, telecommunications, critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Conflict and Macro Uncertainty

Roughly 8,300 technology professionals emigrated between October 2023 and July 2024, while up to 20% of staff were called to military reserve duty. A survey of 637 startups found that 71% experienced funding delays and 48% suffered prolonged absences by critical employees. Output growth stalled in 2024-2025, though venture funding rebounded in 2025, suggesting investors remain confident in the long-term fundamentals of the Israel ICT market. Multinationals are hedging risk with redundant R&D nodes in Eastern Europe and India.

Persistent Tech-Talent Shortages and Wage Inflation

The national deficit of 17,000 skilled ICT workers widens salary gaps and slows project delivery. High-tech employment slipped for the first time in a decade, and Tel Aviv office rents rose 21% from 2023 to 2025. Education pipelines lag, only 13,850 students completed core technology coursework in 2023 against a projected need of 23,600 by 2028. To bridge gaps, vendors invest in low-code platforms, and the 2026 state budget allocates NIS 4.2 billion (USD 1.2 billion) to STEM programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Outpace Hardware Amid Cloud Migration

IT software held 41.63% of the Israel ICT market share in 2025, and IT services segment is broadening at a 4.32% CAGR as enterprises offload legacy infrastructure and governments outsource modernization. Enterprise software and a strong cybersecurity sector propel software to dominate the Israeli ICT market. Meanwhile, high-tech services, encompassing R&D and software development, lead the nation's technology exports. Managed security is flourishing on the back of 312 new defense-derived startups that entered from 2023 to 2025. Cloud and platform services accelerate as Project Nimbus clears regulatory hurdles, with systems integrators capturing recurring revenue through multi-year contracts. The Israel ICT market size for SaaS software reached an estimated USD 1.8 billion in 2026, with SaaS contributing 65% of software spend.

Hardware spending retreats as hyperscalers centralize bulk procurement and extend asset life cycles. Even so, sovereign-cloud mandates sustain discrete demand for on-premise security appliances and edge devices. Growth in communication services is tied to the 5G-fiber convergence, while zero-trust frameworks are reinforcing demand for next-generation firewalls across sectors. Government audits funded by the National Cyber Directorate incentivize ISO 27001 certification, guiding mid-market customers toward managed security bundles and locking in predictable fees in the Israel ICT market.

By Enterprise Size: SME Digitization Accelerates Under E-Invoicing Mandate

Large enterprises drove 63.74% of 2025 outlays, reflecting heavy investments in hybrid-cloud orchestration and data-platform modernization. However, small and medium enterprises represent the fastest-growing slice, compounding at 4.52% as the SHAAM e-invoicing rule pushes universal electronic billing by 2028. The regulation links tax compliance to real-time invoice authentication, pushing SMEs to adopt CRM, inventory automation, and messaging APIs, thereby expanding the Israel ICT market size at the lower end of the pyramid.

Hybrid cloud, advanced analytics, and Industry 4.0 platforms remain the preserve of large enterprises, but municipal authorities are narrowing the gap through Initiative 265 cybersecurity workshops. Local consultancies report FinOps engagements that trim cloud bills by roughly 40% for mid-market customers, reinforcing uptake across both enterprise bands. Continuous digitization at SMEs ensures the Israel ICT market sustains a stable pipeline of greenfield workloads.

By End-User Industry Vertical: Manufacturing Leads Growth as Government Anchors Demand

Government and public administration accounted for 23.74% of 2025 spending, driven by rising allocations for Digital Israel portals, Nimbus migrations, and AI pilots. January 2026 projects span health, education, tax, immigration, and park management, embedding machine-learning toolkits into routine public services. Manufacturing and Industry 4.0 is the fastest-growing vertical at a 3.89% CAGR, propelled by 230 startups and multinational IIoT ventures, giving the Israel ICT market fresh industrial applications.

BFSI continues to invest in core-bank modernization and fraud analytics, while telecom players implement network-function virtualization over 5G cores. Energy utilities deploy smart-grid platforms, and logistics firms double down on AI-based route optimization after raising USD 463 million in 2025. Healthcare is broadening telemedicine and genomics analytics, whereas oil and gas operators are piloting digital twins for offshore rigs. Collectively, these shifts diversify demand, cushioning the Israeli ICT market from single-sector shocks.

Geography Analysis

Tel Aviv-Yafo, Haifa, and Jerusalem account for most of the high-tech employment and venture deals. Tel Aviv hosts roughly 400,000 ICT workers, dense accelerator networks, and the lion’s share of startup capital. Haifa’s proximity to Technion and multinational chip labs anchors semiconductor and autonomous-systems research. Jerusalem concentrates government procurement and Hebrew-Arabic NLP labs, strengthening local expertise in linguistic AI.

Beersheba is maturing as a defense-tech node around IDF cyber units and Ben-Gurion University, with 160 defense-oriented startups founded since 2023. Project Nimbus anchored AWS and Google regions inside the country, satisfying data-residency rules. NVIDIA’s upcoming USD 500 million GPU cluster in northern Israel and the NIS 160 million sovereign supercomputer augment local AI compute. Uneven fiber penetration persists outside major corridors, yet the Ministry of Communications’ spectrum allocations support standalone 5G cores in secondary cities, thereby lifting digital equity metrics across the Israeli ICT market.

Regional incentives are calibrated to counter Tel Aviv-Haifa dominance. The Israel Innovation Authority earmarked part of its NIS 2.2 billion 2026 budget for peripheral grants. Initiative 265’s ISO 27001 workshops extend cybersecurity standards to smaller municipalities, shrinking the urban-rural digital divide. Still, emigration of 8,300 specialists in 2023-2024 hit Tel Aviv hardest, prompting policy makers to fast-track residency visas for returning tech talent. Geographic concentration therefore remains a defining feature of the Israel ICT market.

Competitive Landscape

The Israel ICT market is fragmented. AWS, Microsoft Azure, and Google Cloud dominate IaaS and PaaS, while Check Point, Palo Alto Networks, and Radware capture premium managed-security contracts. The Nimbus framework effectively creates a duopoly for government workloads, nudging smaller providers toward niche edge and vertical SaaS plays. Local integrators such as Matrix IT, Bynet, Malam-Team, Ness Technologies, and Taldor secure multi-year deals by wrapping migration, ISO 27001 compliance, and 24/7 SOC support in Hebrew.

Telcos Bezeq, Cellcom, Partner, Pelephone, and Golan Telecom are pivoting from pure connectivity to managed services, bundling SD-WAN, IoT, and security-as-a-service. White-space opportunities lie in Hebrew-Arabic NLP, SME Industry 4.0 platforms, and cloud-cost optimization. Defense-tech lineage remains a critical differentiator as roughly 50% of founders with exits above USD 100 million hail from Unit 8200. Consolidation continues, exemplified by Palo Alto Networks’ USD 25 billion purchase of CyberArk in March 2026 and Google’s USD 32 billion acquisition of Wiz in August 2025. ISO 27001 mandates and the SHAAM rollout collectively funnel incremental demand to compliance-oriented vendors, sustaining a dynamic yet moderately concentrated Israel ICT market.

Competitive dynamics revolve around three themes such as, AI integration, vertical specialization, and partnership ecosystems. Vendors embed machine-learning accelerators to differentiate ERP, observability, and network-security offerings. New entrants exploit defense-tech IP to challenge incumbents, especially in automated threat-hunting and edge-compute orchestration. Certification under Israel National Cyber Directorate confers credibility, giving local specialists an edge in sensitive tenders. Multinationals respond by launching joint innovation centers and venture funds, deepening ties with Israeli startups.

Israel ICT Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Oracle Corporation

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Check Point Software Technologies launched Infinity Platform upgrades with zero-trust network access and AI-driven threat hunting for Nimbus workloads.

- March 2026: Palo Alto Networks finalized the USD 25 billion acquisition of CyberArk, integrating identity management with network security.

- January 2026: The Government of Israel funded 13 new AI projects across multiple ministries with NIS 40 million.

- January 2026: Nebius opened the national AI supercomputer featuring 1,000 NVIDIA B200 GPUs, financed by NIS 160 million in public funds.

Israel ICT Market Report Scope

The Israel ICT market includes deep analysis of key technology investments such as cloud technologies and artificial intelligence. The Israel ICT Market Report is Segmented by Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, Communication Services), Enterprise Size (Small and Medium Enterprises, Large Enterprises), and End-User Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-Commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing | |

| Business Process Outsourcing | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-User Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-Commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Verticals |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing | ||

| Business Process Outsourcing | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-Commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Verticals | ||

Key Questions Answered in the Report

What is the current Israel ICT market size and its projected growth?

The Israel ICT market size stands at USD 55.01 billion in 2026 and is forecast to reach USD 63.64 billion by 2031, reflecting a 2.95% CAGR over the period [MORDOR INTELLIGENCE].

Which segment is expanding fastest within the Israel ICT market?

IT services, led by managed security and multi-cloud consulting, is growing at a 4.32% CAGR [MORDOR INTELLIGENCE].

How does the SHAAM mandate influence SME technology spending?

SHAAM requires electronic invoices on transactions above NIS 5,000 from June 2026, driving SMEs to adopt CRM, inventory, and API integrations, and powering a 4.52% CAGR for SME ICT outlays [MORDOR INTELLIGENCE].

What geographic areas are emerging as secondary tech hubs in Israel?

Beersheba and northern Israel are gaining traction with defense-tech startups and dedicated GPU clusters, complementing the Tel Aviv-Haifa-Jerusalem core [MORDOR INTELLIGENCE].

Which drivers most shape Israel’s ICT growth outlook?

Government digital programs, nationwide 5G-fiber rollout, deep venture capital pools, and sovereign AI infrastructure collectively add more than two percentage points to expected CAGR [MORDOR INTELLIGENCE].

Page last updated on: