Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

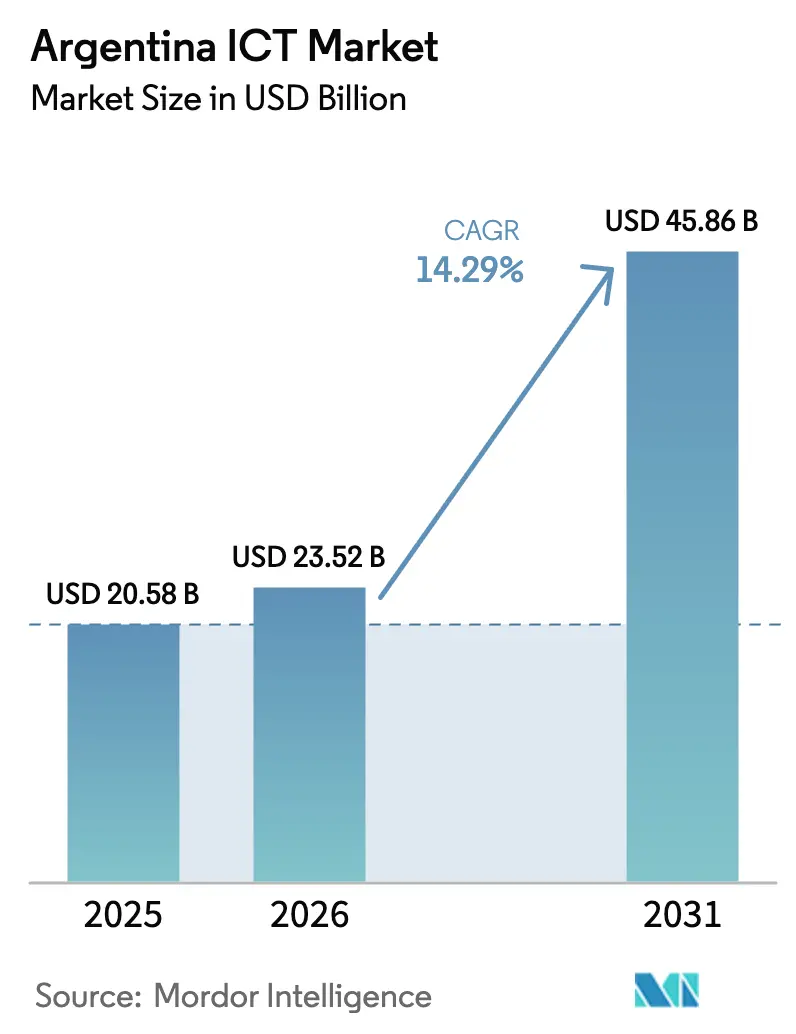

| Base Year Market Size (2025) | USD 20.58 Billion |

| Market Size (2026) | USD 23.52 Billion |

| Market Size (2031) | USD 45.86 Billion |

| Growth Rate (2026 - 2031) | 14.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina ICT Market Analysis by Mordor Intelligence

The Argentina ICT market size is expected to grow from USD 20.58 billion in 2025 to USD 23.52 billion in 2026 and is forecast to reach USD 45.86 billion by 2031 at 14.29% CAGR over 2026-2031. The surge traces to deregulation that opened satellite internet competition, dismantled currency controls, and endorsed a digital-first public-service mandate. Private operators rolled out standalone 5G networks while federal and provincial agencies digitized more than 180 services, compressing paperwork lead times from weeks to hours. Enterprises accelerated cloud migration to offset hardware import delays and to tap favorable exchange rates for export services. Energy-efficient data centers in Buenos Aires and tax incentives for projects over USD 200 million further deepen the Argentina ICT market growth runway.

Key Report Takeaways

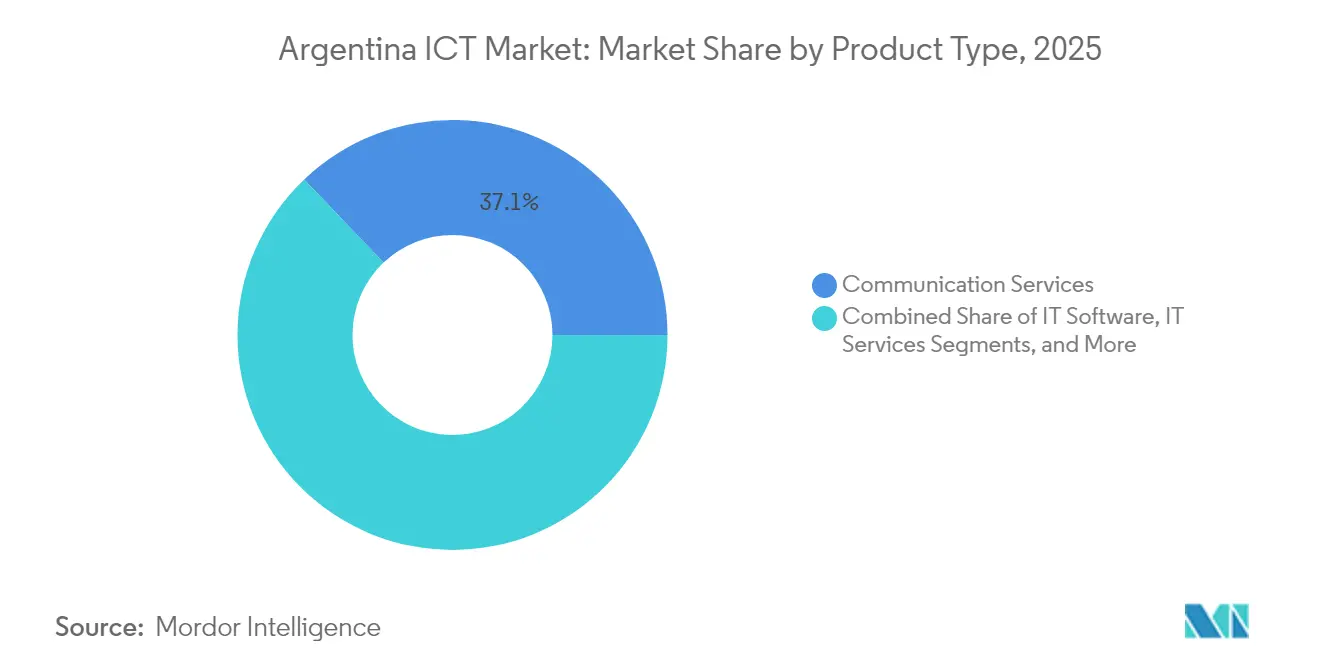

- By Product Type, Communication Services held 37.12% of Argentina ICT market share in 2025; Cloud Services are projected to post the fastest 14.55% CAGR through 2031.

- By Enterprise Size, Large Enterprises accounted for 60.72% revenue in 2025, whereas SMEs are set to lead with a 14.89% CAGR to 2031.

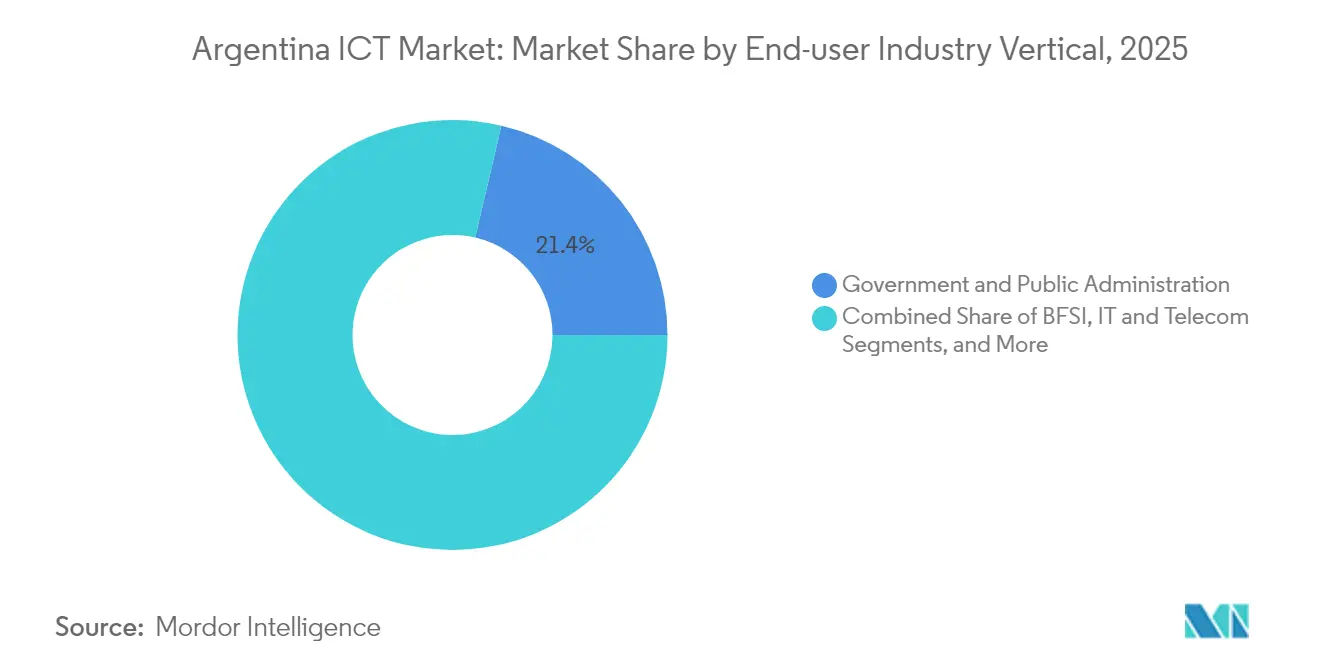

- By End-user Industry Vertical, Government and Public Administration made up 21.35% of 2025 demand, and Gaming and Esports is positioned to expand at a 15.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital-public-services expansion | +2.8% | National with focus on Buenos Aires and provincial capitals | Medium term (2-4 years) |

| Roll-out of 5G spectrum and infrastructure | +3.2% | Buenos Aires, Córdoba, Santa Fe with national expansion | Medium term (2-4 years) |

| Acceleration of cloud and SaaS adoption by enterprises | +2.1% | Nationwide, strongest in AMBA tech corridors | Short term (≤ 2 years) |

| Remote-work led broadband upgrades | +1.4% | Suburban and secondary cities nationwide | Short term (≤ 2 years) |

| Public-private edge data-center initiatives | +1.8% | Buenos Aires, Mendoza, Córdoba zones | Long term (≥ 4 years) |

| Peso-hedge demand for IT export services | +2.3% | Software clusters across the country | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital-Public-Services Expansion

The Mi Argentina platform unified more than 180 public services and processed millions of digital transactions in 2024, illustrating how state digitization stimulates enterprise demand for cybersecurity, cloud hosting, and workflow software. [1]ENACOM, “Reglamento de Gestión Documental Electrónica,” argentina.gob.ar The GDE system cut documentation cycles from weeks to hours, pushing ministries toward paperless operations that ripple into private sector efficiency projects. Digital signatures, e-invoice mandates, and open-data portals reinforce a legal backbone that legitimizes electronic records in court and commerce. Provincial administrations clone the federal blueprint, spreading procurement of SaaS and AI analytics beyond Buenos Aires. ENACOM enforces data-protection rules aligned with international norms, which bolsters confidence among multinationals evaluating the Argentina ICT market. These policies combine to lift the adoption of enterprise platforms that underpin public-sector digital engagement.

Roll-out of 5G Spectrum and Infrastructure

Claro’s Nokia-powered launch and Telecom Argentina’s standalone 5G core deliver sub-10-millisecond latency, enabling industrial automation use cases that neighboring countries cannot yet support.[2]Nokia, “Nokia and Claro Expand 5G in Argentina,” nokia.com Additional spectrum auctions scheduled for 2025 cement a roadmap for contiguous coverage that extends to logistics corridors in Santa Fe and Córdoba. Manufacturers integrate machine-vision quality checks over private 5G slices, while smart-city pilots deploy edge AI for traffic management. Spectrum licenses require rural build-out, expanding broadband reach and indirectly enlarging the Argentina ICT market. The low-latency grid also supports cloud gaming and immersive learning, spawning service niches for carriers and hyperscalers.

Acceleration of Cloud and SaaS Adoption by Enterprises

Microsoft and the SME ministry trained more than 100,000 participants in Azure, AI, and cybersecurity by 2025, closing critical skills gaps that historically stunted SaaS uptake. SAP partner Baitcon reports a wave of S/4HANA migrations as firms race to retire legacy R/3 ahead of the 2027 deadline, a trend mirrored by IBM channel allies. Subscription pricing buffers budgets from peso volatility, appealing to finance managers wary of capital spend. Hybrid architectures flourish, blending local data residency with scalable cloud analytics for manufacturing and BFSI clients. Collectively, these shifts add urgency to vendor roadmaps and inject fresh momentum into the Argentina ICT market.

Remote-Work Led Broadband Upgrades

Starlink’s entry at ARS 56,100 per month forces incumbents to boost speeds and broaden fiber footprints, while Amazon Kuiper’s 2025 arrival promises even lower rates and local-currency billing. Software developers in Rosario, Mendoza, and Mar del Plata gain access to stable low-latency links that match metropolitan quality, encouraging diaspora talent to remain in regional cities. Enterprises adopt SD-WAN overlays to bond satellite and terrestrial links, safeguarding uptime for global client delivery. Accelerated last-mile upgrades enlarge the Argentina ICT market addressable base by turning connectivity from a constraint into an enabler. Broadband competition also cuts prices for rural schools and clinics, supporting inclusive digitization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic economic instability and high inflation | -3.1% | National, most severe in consumer and SME segments | Short term (≤ 2 years) |

| Import controls on ICT hardware | -2.4% | National, concentrated impact on hardware-dependent sectors | Medium term (2-4 years) |

| Cybersecurity and AI skills shortage | -1.8% | National, acute in Buenos Aires and technology corridors | Long term (≥ 4 years) |

| Rising energy costs for data-center operations | -1.2% | Buenos Aires, Córdoba, and industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Economic Instability and High Inflation

Inflation decelerated to 117.8% in 2024 yet still erodes purchasing power, prompting enterprises to defer capital IT projects and pivot toward opex-based SaaS. Peso swings inflate the local currency sticker price of licenses denominated in USD, pressuring SME budgets. Investors factor macro risk into discount rates, raising hurdle returns for long-dated ICT ventures. Consumer electronics demand remains elastic, reducing near-term growth in the Argentina ICT market. Conversely, fintech and export-service providers thrive under volatility, proving that sub-segments can outperform macro headwinds.

Import Controls on ICT Hardware

SEDI registration, statistical charges, and 35% tariffs add 15–30 days to inbound hardware deliveries, complicating timelines for data-center buildouts and 5G base-station expansion.[3]US Trade Administration. "Argentina - Information and Communication Technology." trade.gov Value-added resellers monetize the complexity but pass compliance costs through to clients. Enterprises respond by extending refresh cycles and adopting virtualized alternatives that lighten hardware footprints. Hybrid cloud strategies gain traction as an import-mitigation tactic, although latency-sensitive industries still need local gear. Overall, import frictions cap the upside for hardware-heavy slices of the Argentina ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Communication Services Lead Infrastructure Modernization

Communication Services captured 37.12% of Argentina ICT market share in 2025 as telcos funneled capital into standalone 5G cores and fiber backhaul, cementing network readiness for data-intensive workloads. The segment underpins demand for OTT video, IoT telemetry, and high-frequency trading links that ride on low-latency bandwidth. Cloud Services, projected to post a 14.55% CAGR, represent the pivot away from capex-heavy server rooms toward scalable IaaS and PaaS models. IT Services follow with managed-service contracts that blend on-site support and remote monitoring, cushioning enterprises against talent shortages. IT Hardware trails due to import delays that stretch procurement timelines and inflate landed costs.

The service-centric pivot signals that buyers prioritize flexibility and rapid deployment over ownership, a stance reinforced by peso volatility. Cybersecurity spending courses through every category, rising from USD 1.58 billion in 2024 to an expected USD 2.35 billion by 2029, a trend that puts integrated platform vendors in pole position. Argentina ICT market size for Communication Services is forecast to expand steadily as 5G monetization broadens, while the relative importance of hardware depreciates. Vendors tie connectivity with SaaS bundles, enabling cross-sell synergies that raise average revenue per user and defend margins against price competition.

By Enterprise Size: SMEs Drive Digital Transformation

Large Enterprises controlled 60.72% of 2025 revenue, leveraging dedicated IT budgets to roll out ERP, CRM, and data-lake initiatives that span multiple business units. However, SMEs outpace with a 14.89% CAGR as cloud vouchers, no-code platforms, and government-sponsored training democratize access to advanced tooling. Argentina ICT market size attributable to SMEs is projected to climb sharply as fintech solutions replace bank branch visits and virtual wallets reach 64% usage penetration.

SMEs display agility, adopting pay-as-you-go models that shield cash flow and reduce lock-in. Survey data show 68% of SME executives in software and IT expect higher sales in 2025, further energizing demand for SaaS, cybersecurity, and digital marketing stacks. Large Enterprises confront legacy integration and compliance challenges that slow decision cycles, yet they sustain baseline volume for tier-one vendors within the Argentina ICT industry. Dual-track growth broadens the customer pyramid, forcing suppliers to segment offerings and pricing with precision.

By End-user Industry Vertical: Gaming Emerges as Growth Leader

Government and Public Administration delivered 21.35% of 2025 demand as electronic invoicing, digital IDs, and open data portals required robust software, cybersecurity, and systems integration. Gaming and Esports, buoyed by the BA Gaming program and nationwide tournaments, is forecast to grow at a 15.12% CAGR, catalyzed by affordable 5G latency and municipal esports labs. BFSI continues to ride fintech momentum with 383 firms expanding 11.7% year over year, relying on micro-services and API-based wallets.

Manufacturing taps IoT sensors and digital twins for predictive maintenance, while Healthcare expands telemedicine built on encrypted video and AI-assisted triage. Energy and Utilities harness smart-grid management software that reconciles renewable intermittency with consumer demand. Retail and Logistics lean on real-time inventory visibility and last-mile route optimization, themes that intersect with the Argentina ICT market appetite for analytics and automation. The wide spectrum of vertical use cases diffuses risk and supports an all-weather growth profile.

Geography Analysis

Buenos Aires anchors the Argentina ICT market with the densest concentration of data centers, cloud points of presence, and headquarters for Globant, Mercado Libre, and major telcos. The metro hosts edge facilities optimized for AI inference, while city grants bankroll pilot projects in blockchain land registries and e-mobility. Córdoba and Santa Fe emerge as secondary hubs thanks to university talent and public-private incubators that specialize in ag-tech and industrial automation.

Satellite internet extends advanced connectivity to Patagonia, Cuyo, and Northwest regions, reducing the urban-rural digital divide and spawning micro-outsourcing clusters in cities such as Salta and Neuquén. RIGI incentives lure hyperscaler investments to Mendoza where low seismic risk and cool nighttime temperatures favor efficient data-center operations. Cross-border links position Argentina as a nearshore alternative for North American clients, shortening latency compared with Asian destinations.

The national dispersion of skilled labor, renewable resources, and policy incentives allows provinces to carve niche competencies, reinforcing resilience across the Argentina ICT market. Initiatives such as the proposed nuclear-powered AI hub in Patagonia signal ambition to convert natural advantages into high-value services infrastructure. As network backbones and talent pipelines mature, regional ecosystems inside Argentina interconnect into an integrated digital economy that also plugs seamlessly into Latin American trade corridors.

Competitive Landscape

Global vendors like IBM, Microsoft, and SAP command strategic accounts through extensive local partner networks that tailor solutions to Spanish-language workflows and regulatory specifics. Telco infrastructure remains concentrated among Claro, Telecom Argentina, and Telefónica Movistar, yet satellite entrants Starlink and upcoming Amazon Kuiper disrupt pricing and coverage assumptions.

Local champions Globant, Baitcon, and ADP Consultores leverage cultural proximity and agile delivery to win modernization projects from mid-market clients that prize rapid iteration. Fintech disruptors Mercado Pago, Ualá, and Naranja X exploit high cash usage and inflation hedging behavior, registering double-digit growth despite macro pressures. Cybersecurity service providers scramble to staff SOCs amid soaring incident rates, opening doors for niche MSSP specialists.

Import barriers and currency swings reward firms with logistics know-how and hedged balance sheets. Vendors that bundle financing with hardware or offer peso-indexed SaaS tiers edge competitors reliant on hard-currency billing. Overall, rivalry centers on navigating regulation, delivering talent at scale, and capturing vertical niches driving the Argentina ICT market expansion.

Argentina ICT Industry Leaders

-

Microsoft Australia Pty Ltd

-

Amazon Web Services Australia Pty Ltd

-

Telstra Group Limited

-

Alphabet Inc. (Google Australia Pty Ltd)

-

IBM Australia Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amazon and DirecTV unveiled plans to launch Project Kuiper satellite internet in Argentina, pledging lower prices than Starlink and billing in local currency.

- April 2025: Baitcon detailed a 2025 program to migrate mid-market clients in Córdoba and Santa Fe to SAP S/4HANA with embedded AI functions.

- March 2025: The securities regulator CNV issued regulations under Law 27,739 that impose capital, registration, and cybersecurity standards on virtual-asset service providers.

- February 2025: KIP Protocol partnered with National Technological University Buenos Aires to co-develop Web3 and AI curricula for government and private-sector adoption.

Argentina ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

The Argentina ICT Market is Segmented by Type (Hardware, Software, IT Services, and Telecommunication Services), the Size of the Enterprise (Small and Medium Enterprise and Large Enterprises), and Industry Vertical (BFSI, IT and Telecom, Government, Retail and E-commerce, Manufacturing, and Energy and Utilities). The report provides the market sizes and forecasts in terms of value in USD.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Gaming and Esports |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Gaming and Esports | ||

| Other Verticals | ||

Key Questions Answered in the Report

What is the projected value of the Argentina ICT market in 2031?

The sector is forecast to reach USD 45.86 billion by 2031, reflecting a 14.29% CAGR over 2026-2031.

Which segment is growing fastest within the Argentina ICT space?

Cloud Services are expected to expand at a 14.55% CAGR through 2031 as enterprises migrate workloads to scalable platforms.

How are SMEs influencing technology demand in Argentina?

SMEs are projected to post a 14.89% CAGR by leveraging cloud vouchers, fintech tools, and government-backed training that lower adoption barriers.

Why is 5G important for Argentina’s digital agenda?

Standalone 5G networks enable low-latency applications in manufacturing, logistics, and gaming, making them a cornerstone for next-generation digital services.

What challenges do hardware imports face?

SEDI registration, tariffs up to 35%, and extended currency-approval timelines add 15–30 days to delivery, raising costs and slowing infrastructure deployments.

How is satellite internet shaping connectivity?

Starlink’s rollout and Amazon Kuiper’s planned launch boost rural broadband competition, prompting incumbent ISPs to enhance fiber and pricing models.

Page last updated on: