Sweden Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

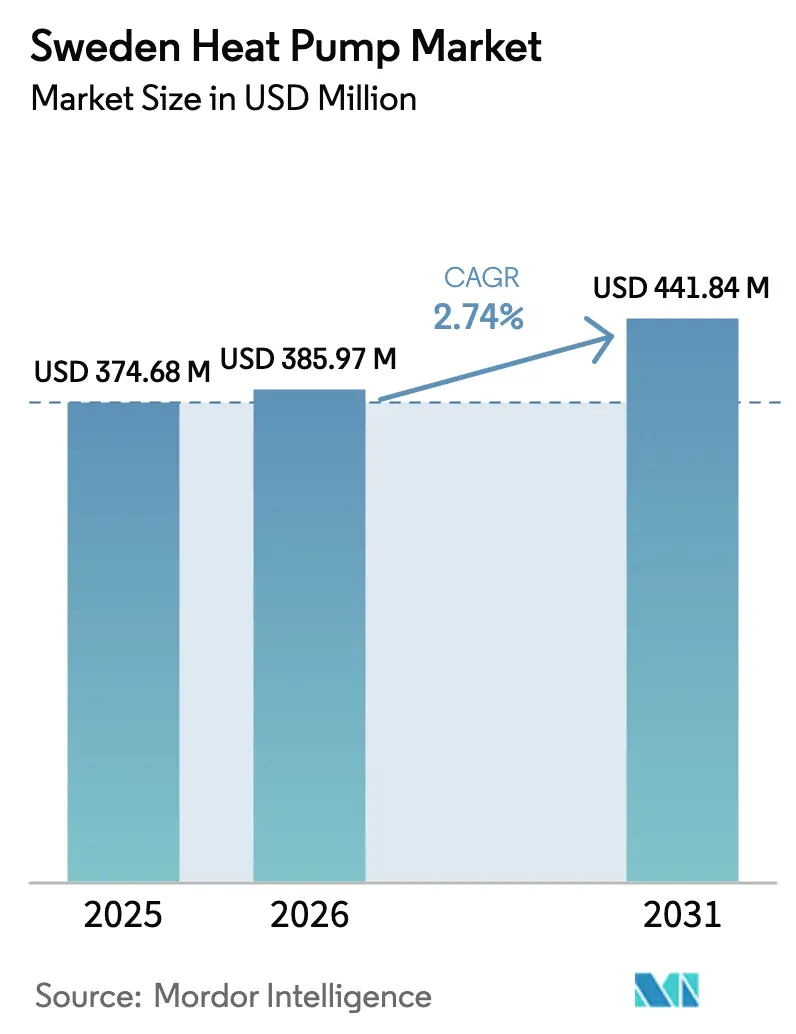

| Base Year Market Size (2025) | USD 374.68 Million |

| Market Size (2026) | USD 385.97 Million |

| Market Size (2031) | USD 441.84 Million |

| Growth Rate (2026 - 2031) | 2.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Heat Pump Market Analysis by Mordor Intelligence

The Sweden heat pump market size was valued at USD 374.68 million in 2025 and is estimated to grow from USD 385.97 million in 2026 to reach USD 441.84 million by 2031, at a CAGR of 2.74% during the forecast period (2026-2031). A policy-led push for electrification, the world’s highest carbon tax and a mature installed base of roughly 2.4 million units underpin demand momentum. Near-term volumes soften as the temporary 50% ROT tax credit expired at the end of 2025, yet structural drivers such as the EU F-Gas Regulation, industrial decarbonization grants and widening electricity-to-fossil price spreads sustain mid-term growth. Grid-capacity bottlenecks in the southern SE3 and SE4 zones, together with a shortage of 5 000-10 000 certified installers, create friction that shifts some projects toward hybrids rather than pure electrification. Manufacturers accelerate propane adoption, and domestic leaders NIBE and CTC defend share while global brands leverage service-network acquisitions to penetrate commercial segments. Across every customer class, digital controls and demand-response capabilities become must-have features as effect tariffs arrive in 2027.

Key Report Takeaways

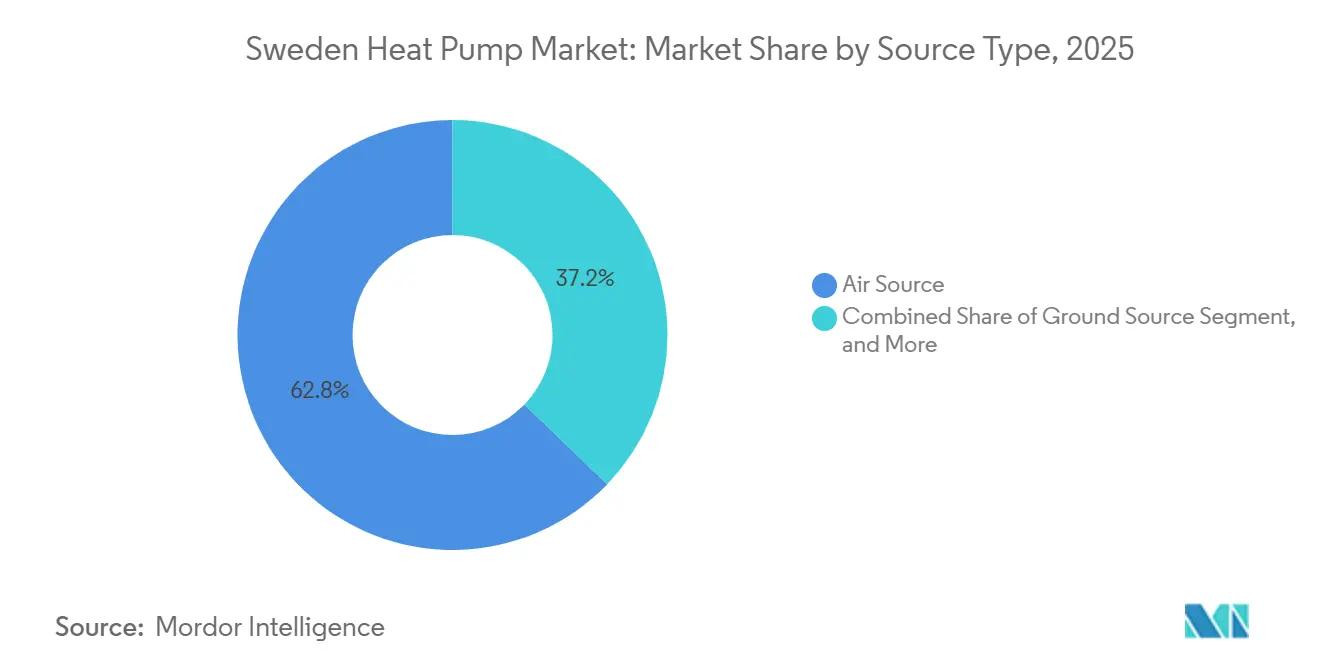

- By source type, air-source systems captured 62.78% of Sweden heat pump market share in 2025, while hybrid configurations are projected to expand at a 3.61% CAGR through 2031.

- By technology, air-to-water technology held 54.48% of the Sweden heat pump market size in 2025, and ground-to-water solutions represent the fastest growing technology at 3.02% CAGR through 2031.

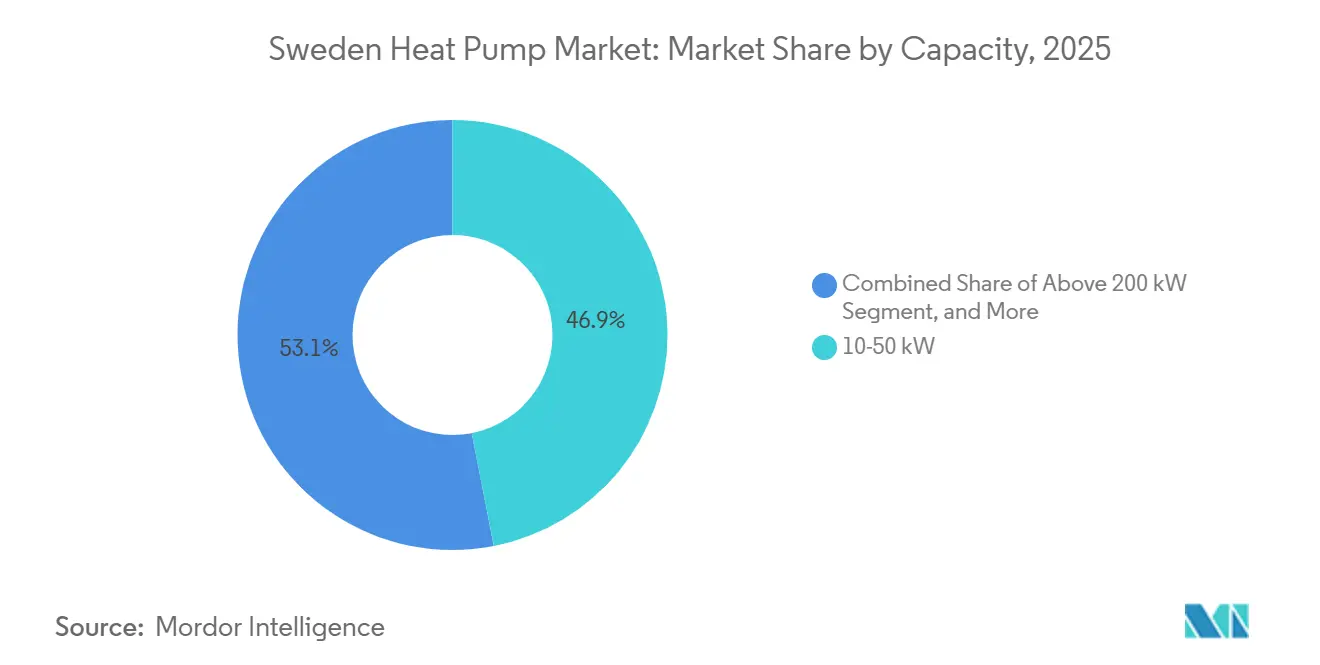

- By capacity, the 10-50 kW capacity band accounted for 46.93% of demand in 2025; systems above 200 kW are advancing at a 2.92% CAGR to 2031.

- By application, space heating led with a 66.52% share of the Sweden heat pump market size in 2025, whereas industrial and process heating is forecast to post the highest 4.86% CAGR to 2031.

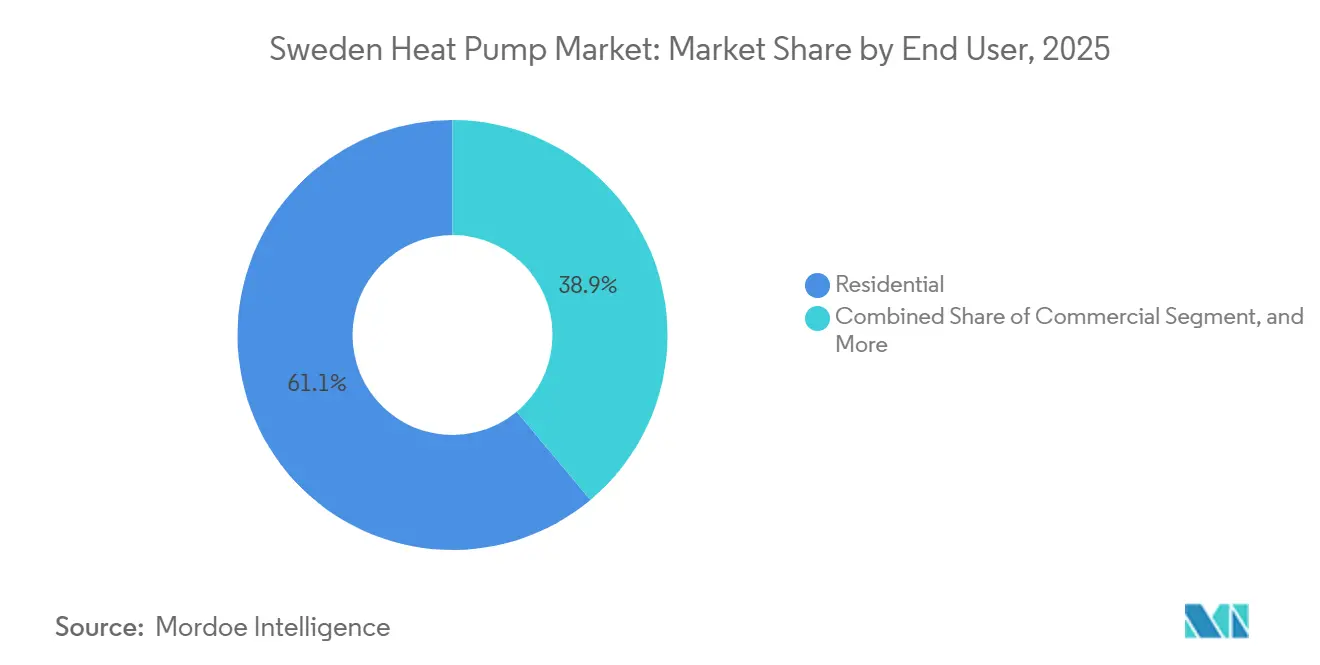

- By end user, residential users commanded 61.09% of demand in 2025, yet the industrial end-user segment is set to grow the quickest at a 2.98% CAGR through 2031.

- By installation, new installations contributed 59.21% of sales in 2025, while retrofit activity is projected to expand at a 2.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sweden Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Government Rebates and ROT Tax-Credit Scheme | +0.9% | National, higher uptake in SE3 and SE4 | Short term (≤ 2 years) |

| Carbon-Tax Escalation and EU ETS Phase IV Pressure | +0.7% | National, spillover to industrial clusters in SE1 and SE2 | Medium term (2-4 years) |

| Surge in Low-GWP Refrigerant Adoption (R290, CO₂) | +0.5% | National, led by residential air-source deployments in SE3, SE4 | Medium term (2-4 years) |

| Rising Electricity-to-Fossil-Fuel Price Differential | +0.4% | SE4 most affected; SE1, SE2 benefit from lower prices | Long term (≥ 4 years) |

| Demand-Response Integration with Smart-Home IoT Platforms | +0.2% | SE3, SE4 urban zones | Medium term (2-4 years) |

| Industrial Cluster Demand for Hydrogen-Ready High-Temp Heat Pumps | +0.3% | SE1, SE2 industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Government Rebates and ROT Tax-Credit Scheme

The elevated 50% ROT deduction that applied through December 2025 shortened payback periods for air-source units to as low as five years, driving a 15-20% surge in 2025 installations.[1]Skatteverket, “ROT Deduction Rules 2025-2026,” skatteverket.se The complementary small-house efficiency grant adds SEK 30,000 (USD 3,160) to material budgets and remains in place until 2030, sustaining baseline residential demand. Uptake concentrates in Stockholm and Malmö where high incomes and aging oil-boiler stock coexist with steep district-heating connection fees. As the ROT share reverts to 30%, a demand normalization is visible for 2026-2027, yet eligibility rules that require ISO 9001 contractors and F-gas certified technicians tighten supply and support pricing.[2]Swedish Energy Agency, “Industrial Electrification Program,” energimyndigheten.se

Carbon-Tax Escalation and EU ETS Phase IV Pressure

Sweden’s carbon tax climbed to SEK 1,520 (USD 160) per tonne CO₂ in 2026, leaving oil boilers economically untenable and shrinking their residential presence to 2.6%.[3]Naturvårdsverket, “Sweden’s Climate Emissions 1990-2024,” naturvardsverket.se ETS2 will add an allowance cost from 2027, cementing fossil-fuel uncompetitiveness in both buildings and industry. Pulp, steel and chemical plants in SE1 and SE2 therefore deploy megawatt-scale high-temperature heat pumps to recycle waste heat and slash Scope 1 emissions, exemplified by Metsä Board’s Husum mill and SSAB’s Hybrit project.

Surge in Low-GWP Refrigerant Adoption (R290, CO₂)

Propane use jumped to 51% of exhaust-air units in 2024 as EU Regulation 2024/573 bans high-GWP hydrofluorocarbons in small capacity systems from 2027.[4]EU Official Journal, “Regulation (EU) 2024/573,” eur-lex.europa.eu NIBE reports more than 80% of its residential portfolio already relies on R290, using sub-kilogram charges that mitigate flammability riskSweden’s additional ventilation and installer-training stipulations lengthen permitting by a few weeks but have not derailed adoption, particularly as propane enables supply temperatures up to 75 °C that satisfy legacy radiator circuits.

Rising Electricity-to-Fossil-Fuel Price Differential

Regional spreads hit 49 öre per kWh in 2025, with SE4 paying triple the northern SE1 average. Natural-gas prices more than double the EU mean cement the economic edge for heat pumps whose seasonal COP exceeds 3.5. Upcoming capacity-based effect tariffs make load-shifting essential; households on dynamic contracts already use negative-price hours to pre-heat storage tanks, amplifying the saving over gas boilers.[5]Swedish Energy Markets Inspectorate, “Dynamic Pricing Report 2025,” ei.se

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Capacity Bottlenecks in Rapidly Urbanizing Zones | -0.6% | SE3 Stockholm, SE4 Malmö and Gothenburg | Short term (≤ 2 years) |

| High Upfront Equipment and Drilling Costs for GSHPs | -0.4% | National, stronger in rural SE1 and SE2 | Medium term (2-4 years) |

| Skilled-Labor Shortage for Large-Scale Retrofits | -0.3% | National, acute in SE3 and SE4 | Medium term (2-4 years) |

| Regulatory Uncertainty around EU F-Gas Revision Timeline | -0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Capacity Bottlenecks In Rapidly Urbanizing Zones

Ellevio’s alert of 10-15 year connection delays for loads above 100 kW in Stockholm freezes many commercial projects.[6]Ellevio, “Grid Capacity Statement 2025,” ellevio.se Thousands of pending applications and transformer deficits of up to 40% in Malmö and Gothenburg hinder pure electrification, so developers specify diesel or pellet backup until substations are upgraded. Although Svenska Kraftnät invests SEK 100 billion (USD 10.5 billion) for backbone reinforcement, local distribution remains the choke point. Effect tariffs arriving in 2027 will penalize peak consumption, squeezing users that cannot shift heat demand away from morning and evening peaks

High Upfront Equipment and Drilling Costs For GSHPs

Residential ground-source installations typically cost SEK 150,000-300,000 (USD 15,840-31680) with drilling alone accounting for nearly half that total.[7]Geological Survey of Sweden, “Drilling Permit Regulations,” sgu.se Permit processes add months, and water-protection zones rule out ground loops in roughly 15% of Swedish territory. As a result, annual ground-source sales slid from 40,000 units in 2015 to about 15,000 in 2023 despite their superior COP near 6.0. The small-house grant covers material, not drilling, leaving a long 10-15 year payback that deters rural buyers even where electricity is cheap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Configurations Hedge Grid Uncertainty

Air-source units delivered 62.78% of the Sweden heat pump market share in 2025, firmly anchoring residential and small-commercial replacements of direct electric and oil systems. Their two-day typical installation window, lower capital cost and eligibility for ROT rebates underpin the volume edge. The Sweden heat pump market size within this segment now stabilizes as saturation grows in single-family homes, but sales remain resilient because aged stock still rotates out each year. Hybrid systems that couple a heat pump with pellet or diesel backup are scaling fastest at a 3.61% CAGR through 2031 because developers in the constrained SE3 and SE4 zones must hedge grid-access delays. Water-source designs stay niche, limited to lakeside properties and industrial cooling loops, while ground-source systems fight higher drilling expenses even though they post seasonal coefficients of performance above 6.0.

Forward momentum centers on hybrids that can switch to biomass or fossil fuel during peak-price hours or grid curtailments, thereby controlling total cost of ownership despite volatile electricity tariffs in southern Sweden. Ground-source retains meaningful rural share in SE1 and SE2 where hydropower-linked prices are low and bedrock conditions ease drilling. Air-source suppliers defend dominance through propane-charged, cold-climate models such as NIBE’s S2125 series that maintain 100% capacity at -15 °C and reach 75 °C supply temperature, enabling retrofits to legacy radiator circuits. As installers face a 5,000-10,000 technician shortfall, products that minimize labor hours and commissioning complexity should preserve the air-source lead within the Sweden heat pump market.

By Technology: Ground-To-Water Gains In Industrial Process Heat

Air-to-water technology accounted for 54.48% of the Sweden heat pump market size in 2025, serving most space-heating and domestic hot-water duties in detached houses and multi-family blocks. Its popularity stems from moderate equipment pricing, generally SEK 80,000-120,000 (USD 7,500-11,300), and a permitting path that avoids drilling. However, ground-to-water systems post a stronger 3.02% CAGR through 2031 as pulp, steel and chemical facilities require 150-180 °C steam and cannot tolerate the performance swings tied to outdoor air temperatures. Water-to-water remains a sub-3% niche, tied to data-center or lakeside applications.

Industrial users now leverage Swedish Energy Agency grants that subsidize up to 30% of ground-loop projects above 1 MW, compressing payback periods to four years and pulling the segment ahead despite higher upfront cost. Residential adopters still favor air-to-water for its quick installation, yet propane-based versions match many of the temperature requirements previously reserved for ground-loops, narrowing the functional gap. Air-to-air units, common for supplemental room heating in older stock, continue to lose share because new Ecodesign labels penalize partial-coverage solutions. These shifts collectively realign technology preference but leave air-to-water as the numerical leader of the Sweden heat pump market.

By Capacity: Large-Scale Systems Serve District Heating And Industry

The 10-50 kW band held 46.93% of 2025 shipments, reflecting its fit with single-family homes and small commercial properties where design loads rarely exceed 15 kW. Despite that dominance, growth moderates to about 2.5% annually because new-build penetration already exceeds 85%. Systems above 200 kW, in contrast, post a 2.92% CAGR through 2031 as district-heating utilities, wastewater plants and industrial campuses electrify process heat and valorize waste streams. Projects at this scale benefit from labor cost economies, installation averages SEK 150-200 (USD 15-21) per kW versus SEK 400-500 (USD 42-52) per kW for residential units, and from preferential grid-access terms offered by transmission operators that value flexibility contributions.

Large-capacity installations also capture revenue by enrolling in Svenska Kraftnät reserve markets through aggregators, adding a financial layer unavailable to smaller devices. Mid-range 50-200 kW machines fill the multi-family and medium-commercial gap and will continue to expand as condominium associations in SE3 and SE4 approve retrofit budgets. Under-10 kW units are pressured by tighter refrigerant rules that raise bill-of-materials costs without equivalent pricing power. Overall, capacity migration toward the upper end raises the average selling price in the Sweden heat pump market and draws international competitors that specialize in megawatt-scale, high-temperature technology.

By Application: Industrial Process Heating Surges Past Space-Heating Growth

Space heating still generated 66.52% of 2025 demand, anchoring the Sweden heat pump market, yet industrial and process heating expands at a 4.86% CAGR through 2031 as decarbonization targets tighten. High-temperature projects such as SSAB’s Hybrit steel line and Stora Enso’s Fors mill prove that ground-to-water systems can deliver 150-180 °C steam with coefficients of performance near 4, replacing natural-gas or biomass boilers. Domestic hot-water duty follows space-heating trends because most residential and multi-family installations bundle the two loads. Cooling remains marginal, below 5% of shipments, although offices in the SE4 zone add reversible heat pumps to mitigate summer peaks.

Forward growth tilts toward industrial users that qualify for Swedish Energy Agency grants covering up to 30% of capex above 1 MW, compressing paybacks to under five years. Process-heat customers also sign wind-power purchase agreements in the SE1-SE2 zones at 15-18 öre per kWh, locking in energy below southern pricing and protecting margins. Residential space heating retains absolute volume leadership, but installer scarcity and grid delays slow retrofits just when 2 million legacy oil and resistance systems remain addressable. The result keeps the overall Sweden heat pump market on a steady rather than explosive trajectory while shifting its mix steadily toward higher-temperature, higher-value machines.

By End User: Industry Overtakes Commercial Growth Pace

Residential buyers accounted for 61.09% of 2025 shipments, yet industrial sites record the fastest 2.98% CAGR through 2031 as pulp, chemicals and green-steel operators electrify heat streams above 100 °C. Megawatt-scale plants, often 10 MW or more, now close within three to four years under grant support, outpacing commercial retrofits that must wait for grid slots in SE3 and SE4. Commercial buildings, hotels, offices, retail, face condominium-board or landlord approvals that lengthen decision cycles, so their CAGR holds just above 2.5%.

Industrial projects also unlock ancillary revenue by selling flexibility to Svenska Kraftnät’s reserve markets through aggregators such as Fortum’s Hiven platform. Commercial adopters leverage thermal mass plus effect-tariff incentives, especially in Malmö where peak-hour charges exceed 200 öre per kWh. Residential uptake divides between affluent SE4 households installing smart, propane-charged air-to-water units and rural SE1-SE2 owners who still favor ground-source for long-term stability. The widening split means industrial offtake will supply a rising share of the Sweden heat pump market revenue even if households preserve numerical dominance.

By Installation: Retrofit Acceleration Checked By Labor And Grid Limits

New-builds captured 59.21% of 2025 sales, benefiting from code mandates that require renewable heating, but retrofits grow at a 2.86% CAGR as Sweden heat pump market penetration in existing stock remains only about one-third. The temporary 50% ROT credit pulled roughly 15,000-20,000 projects forward into 2025, creating a 2026–2027 lull. Retrofit economics still favor air-source units thanks to five-to-eight-year paybacks versus 10-plus years for ground-loops, yet drilling exemptions in water-protection zones and installer shortages keep nationwide retrofit throughput below 100,000 units per year.

Developers planning multi-family retrofits in Stockholm and Gothenburg engineer hybrid systems so that diesel or pellet boilers supply peaks until Ellevio or Vattenfall can provide additional capacity. New-construction in single-family homes already posts penetration above 85%, so upside there is limited and hinges mainly on larger capacity or smarter controls. Retrofit flow therefore becomes the swing factor for the Sweden heat pump market, but it is gated by the pace of technician training under EU Regulation 2024/573, which requires a 40-hour course and keeps wages at a 20-30% premium over general HVAC trades.

Geography Analysis

Sweden’s four bidding zones display divergent adoption profiles that shape the national Sweden heat pump market. SE1 and SE2 in the north enjoy hydropower-backed prices of 18-20 öre per kWh in 2025, half the national mean, which enables widespread ground-source penetration exceeding 40% in rural homes. Industrial clusters around Luleå and Sundsvall run iron-ore, pulp and chemical assets that now install 10 MW-class high-temperature pumps to recycle waste heat and cut carbon levy exposure. Bedrock geology in these regions also lowers drilling risk and cost.

SE3 Stockholm faces the nation’s worst grid constraints; Ellevio quotes 10–15-year waits for loads above 100 kW, causing developers to fit hybrids or defer entirely. Yet the zone logged more than 300 hours of negative pricing in 2025, a benefit exploited by households on hourly contracts to pre-heat storage tanks. Condominium retrofit approvals lengthen timelines, so penetration lags the national average. Uppsala proved that aggregated heat pumps can shave 1.5 MW peaks, and the model now scales via cloud platforms that sell frequency-containment services.

SE4 Malmö and Gothenburg pay the highest tariffs at 67 öre per kWh yet still accelerate uptake because air-source units offer four-to-six-year paybacks even without subsidies. Coastal municipalities leverage Baltic seawater for source energy, letting district-heating operators such as Gothenburg Energi replace coal peakers. Inland Skåne prefers hybrid air-source and pellet solutions to hedge volatile spot prices. Installer density remains highest in SE3 and SE4, about 60% of certified technicians, leaving northern customers to tolerate four-to-eight-week wait lists. These asymmetries explain why the Sweden heat pump market still posts incremental rather than exponential growth despite policy and pricing advantages.

Competitive Landscape

The Sweden heat pump market shows moderate concentration as NIBE and CTC together hold roughly 45% share, supported by vertically integrated factories, Nordic-tuned product lines and nationwide service fleets. Both suppliers fast-tracked propane transitions, 80% of NIBE’s residential portfolio already runs R290, and rolled out cloud controls that qualify for demand-response programs. Their scale secures component allocations and installer loyalty, reinforcing barriers to entry for smaller domestic challengers.

International majors pursue share through local partnerships. Daikin’s 2025 buyout of Kylslaget added 32 technicians and 7 000 service contracts, trimming response times in SE3-SE4. Bosch leverages its Tranås IVT plant for cold-climate R32 lines and is funneling additional volumes from a EUR 100 million (USD 115 million) Aveiro expansion that opens late 2026. Mitsubishi, Carrier and Johnson Controls fight for industrial megawatt plants where high-temperature capability commands margins. Each vendor embeds smart-grid APIs so that installations can bid into Svenska Kraftnät’s ancillary markets.

Emerging players tilt toward software and aggregation layers. Fortum’s Hiven platform, now FCR-D certified, clusters electric vehicles and heat pumps to deliver sub-two-second reserve, paying owners more than SEK 500 (USD 52) per MWh. Qvantum and 1KOMMA5° fuse AI scheduling with smaller propane products aimed at households on dynamic contracts, advertising 20-30% bill savings. Patent activity targets low-charge propane compressors, Fraunhofer’s 760-gram design for 28 kW output being a headline example. Because installer scarcity constrains scale more than factory capacity, service-network acquisitions and training academies stand out as the strategic battleground through 2031.

Sweden Heat Pump Industry Leaders

Daikin Industries Ltd.

NIBE Industrier AB

Carrier Global Corporation

Thermia AB

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Qvantum partnered with 1KOMMA5° to integrate Heartbeat AI load-optimization into its propane heat pumps, targeting dynamic-pricing households.

- December 2025: Bosch Thermotechnology joined E.ON Sweden and Podero to roll out grid-responsive optimization across 10,000 units by end-2026.

- August 2025: Panasonic committed EUR 320 million (USD 339 million) to a Czech factory prioritizing R290 models for Nordic delivery.

- August 2025: CTC released the EcoAir 720M, a 22.7 kW propane air-to-water unit aimed at SE3-SE4 commercial retrofits.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Swedish heat-pump market as the annual value of factory-built air-source, ground-source, water-source, and hybrid units up to 100 kW that are supplied for space heating, space cooling, or combined sanitary hot water duties across residential, commercial, and small industrial premises.

Scope exclusion: stand-alone heat-pump water heaters sold without any space heating function, portable spot coolers, and absorption chillers are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, heat-pump OEM sales managers, energy service companies, and regional energy offices across Stockholm, Skåne, and Norrland. Discussions verified average selling prices after grants, typical sizing rules in retrofit projects, and the share of imported outdoor units versus locally assembled systems, allowing us to fine-tune model assumptions.

Desk Research

We began by mapping Sweden's installed base, replacement cycle, and new-build demand using open datasets such as Statistics Sweden's building permits, the Swedish Energy Agency's energy balance tables, Eurostat trade codes 841861/62, EHPA country statistics, and SKVP quarterly shipment reports. Company filings, tender notices, and reputable press clarified brand shares, while D&B Hoovers and Volza helped our team check importer-exporter values. These public and paid sources provided the baseline but seldom revealed channel discounts or subsidy pass-throughs, which are critical in Sweden's ROT credit environment. The sources listed are illustrative; many other publications informed data validation.

Market-Sizing & Forecasting

A top-down demand pool build starts with dwelling stock by house type, average heated floor area, and prevailing penetration rates; these are multiplied by replacement and first install propensities to obtain unit volumes, which are then priced with weighted average transaction prices from primary checks. Supplier roll-ups of the ten largest brands serve as a selective bottom-up cross-check. Key variables include electricity to oil price ratio, rebate uptake rate, building renovation completions, average system capacity (kW), and seasonal COP improvement. Forecasts rely on multivariate regression blended with scenario analysis, capturing the impact of carbon tax escalations and mortgage rate swings. Gaps in bottom-up data are bridged by applying conservative mark-ups anchored to documented margin ranges.

Data Validation & Update Cycle

Outputs pass a three-step review: automatic anomaly flags, analyst peer review, and final sign-off by a senior reviewer. We refresh the model every twelve months, with interim updates triggered by policy shocks or greater than 10 percent volume variance signals.

Why Our Sweden Heat Pump Baseline Proves Dependable

Published figures often diverge because providers choose different product mixes, price definitions, and update rhythms.

Key gap drivers include: some studies fold in service contracts or dedicated water heater sales, others rely on customs values that inflate totals by including VAT and freight, while a few present district-scale units exceeding 1 MWth that our scope omits. Mordor's disciplined segmentation, annual refresh, and dual-track validation minimize such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 364.7 m | Mordor Intelligence | - |

| USD 865.9 m | Global Consultancy A | Includes accessories and maintenance revenues; last full refresh 2022 |

| USD 1 000 m | Industry Dataset B | Uses customs values without dealer margin adjustments |

| USD 172.6 m | Trade Journal C | Covers only large-scale (greater than 10 MWth) district heating pumps |

In sum, our balanced mix of official statistics, field intelligence, and transparent assumptions gives decision-makers a repeatable Swedish heat-pump baseline they can trust.

Key Questions Answered in the Report

What annual growth is expected for Swedish heat-pump installations between 2026 and 2031?

Volumes are forecast to rise at a 2.74% CAGR, advancing the Sweden heat pump market from USD 385.97 million in 2026 to USD 441.84 million by 2031.

Which technology is gaining fastest traction for high-temperature industrial use?

Ground-to-water units delivering steam above 150 °C lead growth at a 3.02% CAGR as pulp, steel and chemical plants electrify process heat.

How do grid-capacity limits affect large commercial projects?

In SE3 and SE4, connection waits of 10-15 years push developers toward hybrid designs or delay pure electrification, restraining near-term industrial and commercial uptake.

Why are hybrids becoming popular in southern Sweden?

They hedge electricity-price volatility and bridge grid-connection delays by pairing air-source pumps with pellet or diesel boilers, especially around Malmö and Gothenburg.

What refrigerants dominate new residential models?

Propane (R290) is now used in more than 80% of NIBE's residential range and is spreading rapidly across other brands to comply with EU Regulation 2024/573 phase-down rules.

How severe is the installer shortage?

Sweden needs an extra 5 000-10 000 certified technicians by 2030; the shortfall lengthens retrofits and sustains wage premiums of 20-30% above standard HVAC rates.

Page last updated on: