Spain Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

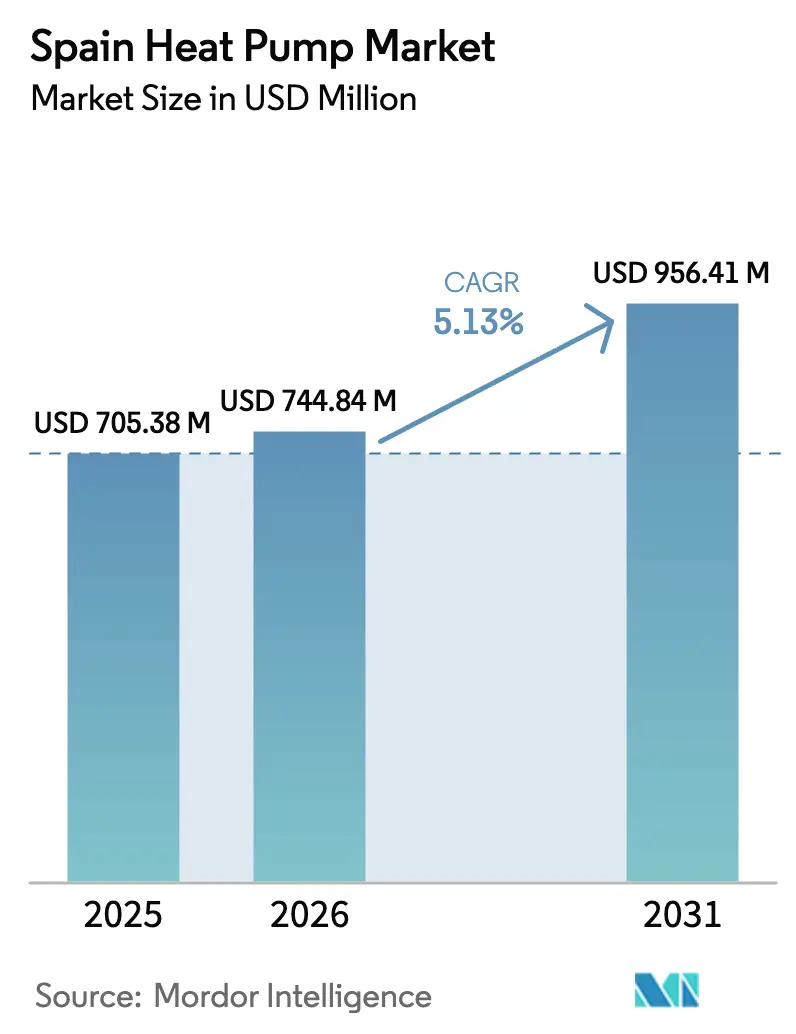

| Base Year Market Size (2025) | USD 705.38 Million |

| Market Size (2026) | USD 744.84 Million |

| Market Size (2031) | USD 956.41 Million |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Heat Pump Market Analysis by Mordor Intelligence

The Spain heat pump market size is expected to increase from USD 705.38 million in 2025 to USD 744.84 million in 2026 and reach USD 956.41 million by 2031, growing at a CAGR of 5.13% over 2026-2031. Decarbonization deadlines are steering buyers toward electrified heating even as grid saturation challenges impose higher connection costs. Retrofit demand dominates because three-quarters of 2025 installations occurred in existing buildings, yet the pipeline of zero-emission new-build projects is rising as the 2028-2030 construction mandates approach. Subsidies covering up to 75% of project cost in leading regions continue to compress payback periods, while hybrid configurations offer a transitional path for customers unwilling to abandon backup gas boilers. Investor interest is shifting from pure equipment supply toward heat-as-a-service models that bundle financing, installation, and long-term clean-power contracts.

Key Report Takeaways

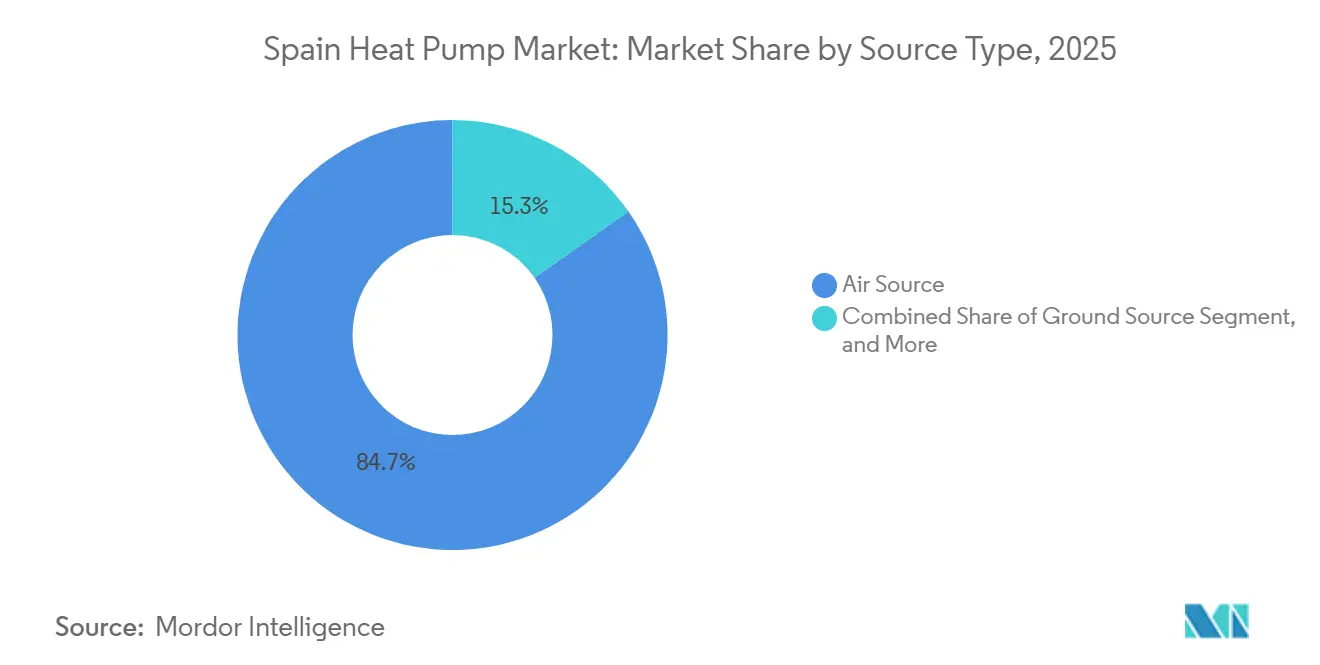

- By source type, air source led with 84.73% revenue share in 2025; hybrid systems are projected to advance at a 5.49% CAGR through 2031.

- By technology, air-to-water accounted for 38.31% of the Spain heat pump market share in 2025, and it is poised to expand at a 5.69% CAGR to 2031.

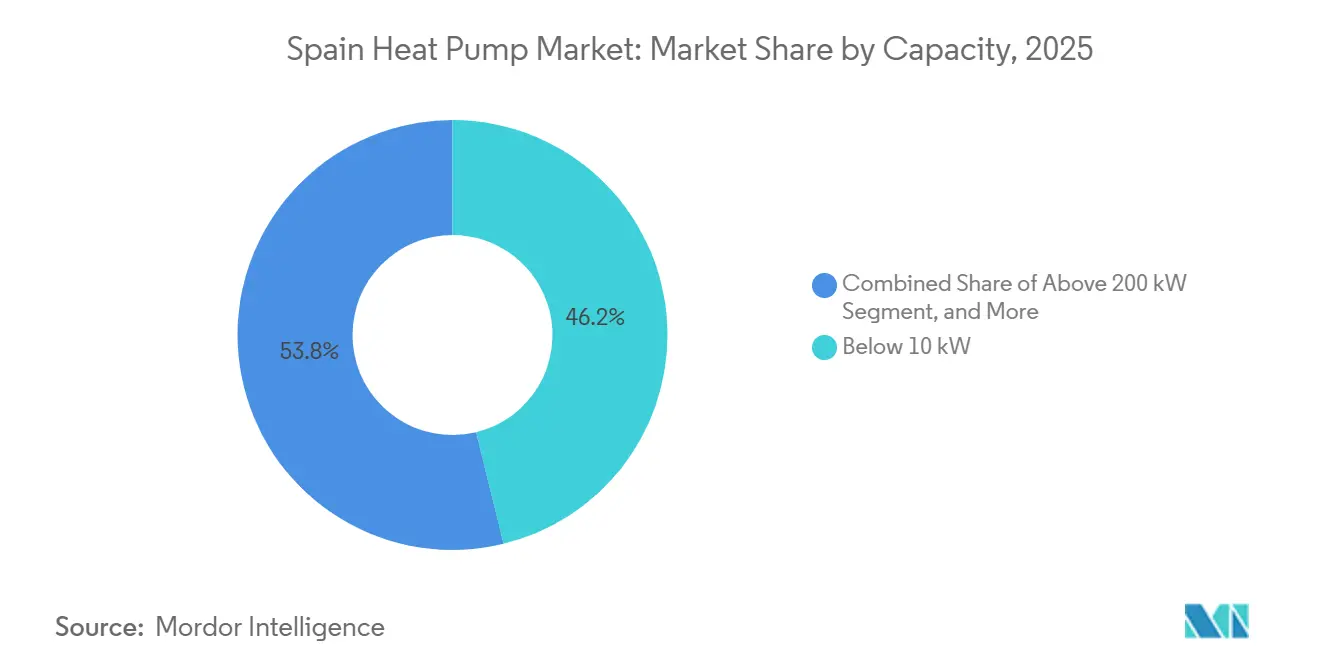

- By capacity, below 10 kW units commanded 46.18% of the Spain heat pump market size in 2025, while systems above 200 kW record the fastest projected CAGR at 5.44% through 2031.

- By application, domestic and sanitary hot water captured 29.96% share in 2025, whereas industrial and process heating is forecast to advance at a 5.36% CAGR during the outlook period.

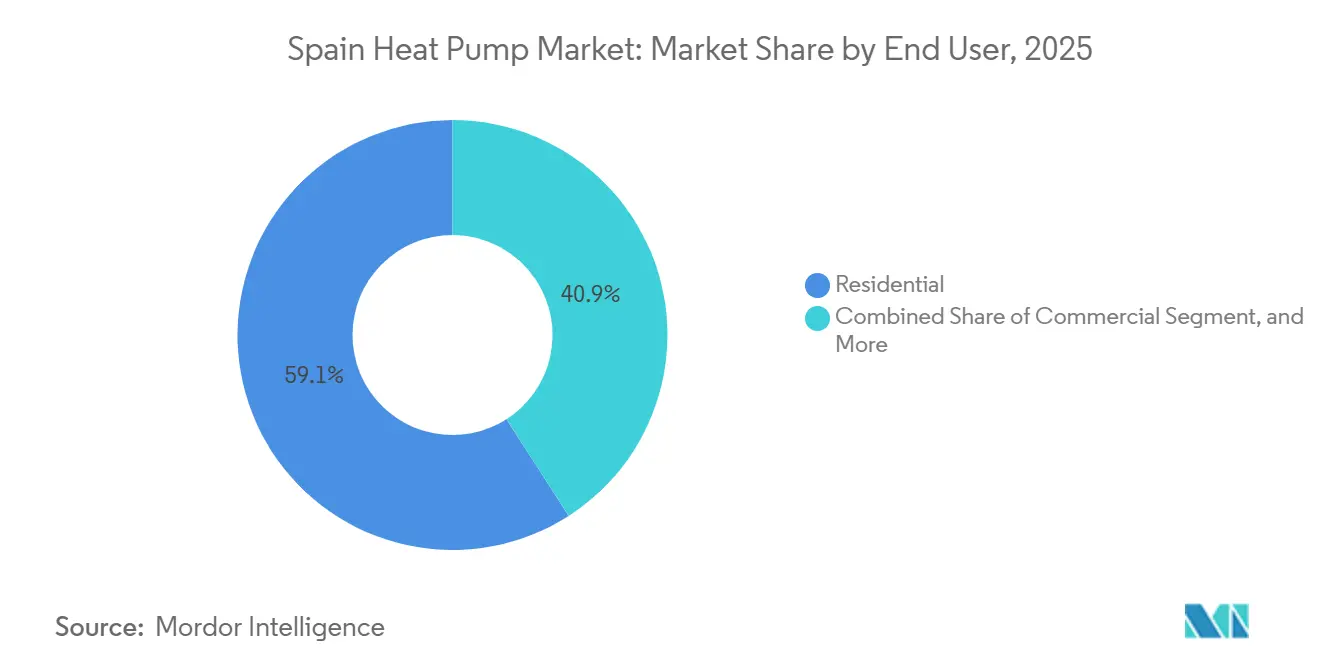

- By end user, residential buyers held 59.09% share in 2025, yet the commercial segment is projected to grow at 5.28% CAGR to 2031.

- By installation, retrofit projects represented 54.43% of 2025 revenue, while new installations are expected to register the highest CAGR at 5.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives and Environmental Subsidies | +1.2% | Catalonia, Madrid, Basque Country, Andalusia | Short term (≤ 2 years) |

| EU Green Deal and EPBD Compliance Deadlines | +1.0% | National | Medium term (2-4 years) |

| Rising Electricity-to-Gas Price Ratio Boosting TCO | +0.8% | National | Medium term (2-4 years) |

| Advancements in Low-GWP Propane-Based Heat Pumps | +0.6% | National | Long term (≥ 4 years) |

| Uptake of Hybrid Heat Pumps Leveraging Cooling Base | +0.5% | Southern and coastal regions | Medium term (2-4 years) |

| Hospitality Decarbonization Driven by Tourism Boom | +0.4% | Balearic Islands, Andalusia, Catalonia, Madrid, Canary Islands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Incentives and Environmental Subsidies

Spain’s tiered funding stack blends national recovery grants with autonomous-community top-ups, delivering household rebates of EUR 3,000-5,000 (USD 3.39-5.65 thousand) and, in Barcelona, project support worth up to EUR 18,800 (USD 21.24 thousand). Catalonia’s 40% capital grants and Andalusia’s new EUR 61.9 million (USD 69.95 million) thermal-storage line have pulled installer capacity toward high-incentive regions, leaving lower-subsidy provinces underserved. Grant intensity that reaches 75% for public entities under the 2026 RENORED program extends electrification into district energy schemes. While incentives shorten payback periods to as little as five years, they also create regional labor imbalances and accelerate the need for installer upskilling.[1]Ministerio para la Transición Ecológica, “MITECO Climate and Energy Programmes,” miteco.gob.es

EU Green Deal and EPBD Compliance Deadlines

The May 2026 transposition of the recast Energy Performance of Buildings Directive forces developers and owners to lock in zero-emission solutions before fossil boiler bans cascade through regional codes. Buildings rated below class D must be upgraded by 2033, concentrating retrofit activity in Spain’s pre-1980 housing stock that lacks insulation or low-temperature radiators. Commercial property owners are pivoting toward air-to-water and hybrid systems to retain eligibility for green finance, a trend reflected in large pre-order backlogs with installers in Madrid and Barcelona.[2]European Commission, “Energy Performance of Buildings Directive,” ec.europa.eu

Rising Electricity-to-Gas Price Ratio Boosting TCO

An average 2.5-to-1 power-to-gas price ratio in 2025 raised the operating-cost hurdle, yet air source units delivered seasonal COP values above 3.5 in Spain’s mild zones. A Universitat Politècnica de València field study found hybrids cut annual running costs by 50% across Bilbao, Madrid, and Valencia by activating gas backup only during brief winter peaks. Renewable penetration already above 25% magnifies the emissions advantage, and time-of-use tariffs linked to midday solar oversupply widen the cost gap when paired with thermal storage.[3]Universitat Politècnica de València, “Hybrid Heat Pumps Study,” catenerg.webs.upv.es

Advancements in Low-GWP Propane-Based Heat Pumps

Impending F-Gas bans propel R290 systems into the mainstream. Commercial units up to 230 kW introduced in 2025 deliver COP gains exceeding 8% versus R410A peers while meeting EN 378 safety thresholds. Spain’s involvement in the Fraunhofer LC R290 project accelerates installer familiarity with low-charge designs, although current certification tracks do not yet mandate propane competency. Joint ventures providing integrated R290 compressor-inverter platforms promise EUR 500-800 per-unit cost reductions by 2028, potentially reshaping the mid-capacity competitive field.[4]Fraunhofer Institute for Solar Energy Systems, “LC R290 Project,” ise.fraunhofer.de

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortage for Installations | -0.9% | Madrid, Barcelona, Valencia, Seville | Short term (≤ 2 years) |

| High Up-Front Equipment and Retrofit Costs | -0.7% | National, high in rural and low-income areas | Medium term (2-4 years) |

| Grid Capacity Limits in Urban Districts | -0.5% | Madrid, Barcelona, Valencia, Bilbao, Seville | Medium term (2-4 years) |

| Limited Roof/Riser Space in Multi-Family Buildings | -0.3% | Urban cores of Madrid, Barcelona, Valencia, Zaragoza | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage for Installations

Spain must train thousands more technicians to reach its proportional share of the EU-wide 500,000-installer goal by 2030. Current certification pipelines graduate fewer than 8,000 specialists yearly, inflating lead times from four to 12 weeks in major cities. Hydronic retrofits require hydraulic balancing and low-temperature radiator sizing skills rare among crews focused on cooling splits, pushing labor premiums 15-25% higher for complex jobs. Corporate buyers are acquiring installer teams outright to lock in scarce capacity.[5]Joint Research Centre, “Clean Energy Technology Observatory: Heat Pumps,” publications.jrc.ec.europa.eu

High Up-Front Equipment and Retrofit Costs

Installed air-to-water systems average EUR 10,000 (USD 11.30 thousand) and ground source exceeds EUR 17,000 (USD 19.21 thousand), leaving households to self-finance half the bill even after grants. Legacy apartments need radiator swaps and panel upgrades that add EUR 2,000-4,000. Service-contract models that spread cost across 10-15 years mitigate the barrier, but legal complexity and owner-approval rules slow multi-family adoption. Banks remain cautious until default data on heat-as-a-service loans mature.[6]European Heat Pump Association, “EHPA Market Data and Statistics,” ehpa.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Uptake Signals Transitional Hedging

Hybrid units, though a small base today, are projected to post a 5.49% CAGR and draw on Spain’s five-million-unit cooling fleet to minimize incremental investment. They allow operators to retain gas boilers for sparse peak-load hours, delivering 60% emissions cuts without straining winter grid capacity. In contrast, air source equipment dominates the Spain heat pump market with an 84.73% 2025 share, buoyed by benign winter temperatures that support seasonal COP above 3.5.

Hybrid momentum aligns with power-to-gas price spreads and policy uncertainty over near-term grid upgrades. Manufacturers bundle predictive controls that switch fuels dynamically, creating a cost-optimized pathway into full electrification once network reinforcement arrives. The Spain heat pump market therefore shows a bifurcated profile in which pure electrification leads coastal regions, while hybrids anchor northern provinces still wary of cold-spell reliability.

By Technology: Hydronic Systems Overtake Cooling-Centric Installations

Air-to-water platforms are winning share thanks to their compatibility with underfloor heating and domestic hot water loops required by zero-carbon building codes. Holding 38.31% share in 2025, this cohort is projected to grow at 5.69% CAGR, gradually eroding the air-to-air installed base. Schools, hotels, and hospitals are standardizing on hydronics to secure taxonomy-aligned finance, a trend reinforcing the Spain heat pump market pivot away from cooling-only solutions.

The transition also affects supply chains; compressors and circulators rated for 55-60 °C delivery temperatures face rising demand, and installers retrain on hydraulic balancing. Digital commissioning tools now streamline flow-rate optimization, cutting start-up time by one-third. As such, the Spain heat pump market size allocated to hydronic retrofits is expected to eclipse EUR 300 million (USD 340 million) annually by 2031.

By Capacity: Industrial-Scale Growth Unlocks New Revenue Streams

Systems above 200 kW are forecast to expand at 5.44% CAGR, propelled by food and chemical plants that need process heat up to 160 °C. Early projects recovering waste heat from refrigeration compress the Spain heat pump market payback to four-to-six years when paired with off-peak tariffs. Residential demand centers on sub-10 kW units, which captured 46.18% of 2025 revenue but face slower growth as multi-dwelling retrofits scale.

Policy initiatives such as the EUR 50 million (USD 54.5 million) RENORED program mandate minimum 1 MW thermal capacity in district schemes, effectively steering grant flows toward industrial-scale arrays. Suppliers responding with modular 50-kW skids enable phased expansion while lowering on-site labor, reinforcing capacity bifurcation within the Spain heat pump market.

By Application: Process Heating Escapes Niche Status

Industrial and process heating promises the fastest trajectory at 5.36% CAGR, supported by EU funds covering high-temperature pilot lines. Demonstrations in chocolate, dairy, and textiles prove steam-boiler displacement at delivered heat costs under EUR 40 (USD 45) /MWh, placing electrified thermal loops inside board-approved capex thresholds. Domestic and sanitary hot water remains the largest single use case, holding 29.96% share in 2025 thanks to straightforward cylinder integration and solar PV synergies.

Growing time-of-use incentives now value midday load shifting, making thermal storage an integral design element. Consequently, the Spain heat pump market share tied to dual service, space heating plus hot water, is climbing as developers bundle both loads into one rightsized hydronic plant, improving utilization across seasons.

By End User: Commercial Buyers Monetize Green-Finance Premiums

Hotels, hospitals, and offices are accelerating purchases at a 5.28% CAGR by leveraging energy-as-a-service contracts that remove capex and capture subsidies. Residential still comprised 59.09% of 2025 demand, dominated by single-family homes with unilateral decision authority. In apartments, retrofit momentum relies on municipality-led aggregation models that pool owners and subsidies, an approach showcased by the award-winning Basque HAPPENING scheme.

Corporate disclosure rules and investor pressure link sustainable heating directly to asset valuation. As interest rates rise, green loans priced 25-50 basis points below conventional debt make immediate electrification financially rational. Integrated offerings that pair heat pumps with rooftop solar and digital management are therefore scaling fastest inside the Spain heat pump market.

By Installation: New-Build Momentum Gains After 2028 Mandates

Retrofits accounted for 54.43% of 2025 revenue because policy first attacked the legacy building stock. Yet new installations are projected to outpace at 5.56% CAGR as zero-emission requirements for public buildings in 2028 and for all builds in 2030 lock gas out of design specs. Purpose-built electrical infrastructure and underfloor systems shave EUR 2,000-3,000 (USD 2300-3540) from installed cost versus deep retrofits, strengthening relative economics.

Developers of data centers and logistics hubs are pre-ordering air-to-water cascades to de-risk compliance years ahead. Meanwhile, the retrofit wave continues where layered subsidies and high power-to-gas spreads converge. The Spain heat pump market therefore exhibits a crossover point in 2029 when new construction overtakes retrofits in annual unit shipments.

Geography Analysis

Catalonia, Madrid, and the Basque Country together absorbed more than 55% of national installations in 2025, reflecting richer subsidy stacks and dense installer networks. Barcelona’s grants that reach 75% of total cost in multi-family retrofits draw contractors from neighboring provinces, but the talent drain slows rollouts in Andalusia and Castilla-La Mancha. Madrid’s split profile spans geothermal-equipped suburban housing on one side and space-restricted city-center retrofits favoring compact air-to-air units on the other.

Andalusia’s EUR 61.9 million thermal-storage push pairs phase-change materials with heat pumps to counter rising grid congestion as solar PV penetration tops 30%. Valencia showcases marquee ground-source projects like the 4,050 kW City of Arts and Sciences system, yet slower grant uptake limits residential diffusion. Island grids in the Balearics and Canaries face emissions penalties from diesel backup, but tourism operators are pressing ahead regardless, installing over 1 MW of capacity in 2025 to preserve net-zero travel branding.

Northern Atlantic provinces lag due to higher heating loads and fewer installers, though replication of the Basque HAPPENING model could shorten paybacks. Central plateau regions substitute biomass where gas grids are absent, muting electrification urgency. The urban-rural deployment divide is widening as training centers, distribution warehouses, and financial intermediaries cluster around Spain’s ten largest metro areas, reinforcing asymmetric growth patterns within the Spain heat pump market.

Competitive Landscape

Global manufacturers Daikin, Mitsubishi Electric, Viessmann, and Bosch together held roughly half of 2025 shipments, but utilities and energy service companies are redrawing competitive boundaries. Iberdrola’s ATuAire offers zero-upfront turnkey packages that bundle hardware, installation, and long-term clean power, creating a sticky customer relationship traditional OEMs struggle to match. Edison Next’s acquisition of Ecoclima secured scarce hydronic expertise, illustrating how installation capacity now commands premium valuations.

High-temperature industrial systems remain sparsely supplied, with only a handful of OEMs delivering units above 110 °C. Joint ventures such as the 2026 Copeland-Daikin platform promise integrated R290 compressor-inverter kits that could drop mid-capacity system costs by up to EUR 800 (USD 920) by 2028, intensifying price pressure. Distributor consolidation is also accelerating; Grafton Group’s 2026 purchase of Mercaluz builds an Iberian network exceeding EUR 400 million (USD 460 million) annual sales, improving leverage over OEMs and installers.

Digitalization is the next battleground. The Schneider Electric partnership with ATuAire embeds cloud analytics and demand-response APIs into every install, monetizing flexibility and offering building managers granular performance dashboards. These value-added layers differentiate propositions beyond equipment efficiency, signaling that service integration will determine leadership in the Spain heat pump market.

Spain Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corporation

NIBE Industrier AB

Viessmann Werke GmbH & Co. KG

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Grafton Group agreed to acquire Mercaluz for up to EUR 175 million (USD 190.8 million), expanding its Iberian HVAC platform.

- January 2026: Dalrada Technology Spain won a USD 275 thousand nursing-home contract after commissioning four 50 kW units at another facility.

- January 2026: The Ministry for Ecological Transition launched the EUR 50 million (USD 54.5 million) RENORED district-energy grant program with 75% funding for public schemes.

- December 2025: Paloma Rheem purchased a majority stake in Group Atlantic, adding brands Atlantic, Thermor, and Sauter to its European portfolio.

- September 2025: Iberdrola’s ATuAire and Schneider Electric formed a strategic alliance to integrate digital energy management with financed heat-pump packages.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spain heat pump market as revenue earned from new air-source, water-source, and ground-source units that deliver space heating, space cooling, or domestic hot water to residential, commercial, industrial, and institutional buildings.

Scope exclusion: aftermarket services, spare parts, and industrial chillers are outside this remit.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Installers, importers, builders, and municipal efficiency officers in Madrid, Barcelona, Seville, and Valencia shared views on uptake rates, retrofit intensity, and subsidy pass-through, allowing us to align assumptions with market reality.

Desk Research

We drew baseline units and prices from Spanish customs data, Eurostat energy balances, the national energy agency (IDAE), and European Heat Pump Association shipment dashboards. Macroeconomic cues came from Banco de España housing completions, retail electricity-to-gas price files, and degree-day series. Company 10-Ks, investor decks, and news retrieved through D&B Hoovers and Dow Jones Factiva rounded out cost and share insights. The sources listed are illustrative; many additional public records supported validation.

Market-Sizing & Forecasting

A top-down demand pool-dwelling stock, annual completions, usable floor area, and air-to-water penetration were built, then cross-checked with sampled average selling price multiplied by imported units. Bottom-up supplier roll-ups closed commercial gaps. Key variables such as energy-price spreads, subsidy budgets, building-code milestones, and cooling-hour trends feed a multivariate regression that extends to the forecast period. We anchor the base year value and iterate until top-down and bottom-up paths converge within a specified percentage.

Data Validation & Update Cycle

Outputs face variance checks, senior analyst review, and call-backs when anomalies surface. Models refresh yearly, with interim updates whenever policy or currency shifts materially alter the outlook.

Why Mordor's Spain Heat Pump Baseline Earns Reliance

Published estimates often differ because firms vary scope, price curves, and refresh cadence.

Our disciplined equipment-only scope and annual update keep figures current and decision-ready.

Key divergences stem from some studies folding installation labor into revenue or applying uniform double-digit price inflation, contrasts that Mordor analysts temper with observed transaction data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 669.8 mn (2024) | Mordor Intelligence | - |

| USD 668.3 mn (2024) | Regional Consultancy A | Broader cooling appliance scope and higher price uplift |

| USD 1.30 bn (2024) | Global Consultancy B | Includes installation labor and hybrid systems |

The comparison shows that Mordor Intelligence supplies a balanced, transparent baseline grounded in observable trade flows and pragmatic pricing, giving stakeholders a dependable starting point for strategic choices.

Key Questions Answered in the Report

What is the projected Spain heat pump market size by 2031 and how does that compare with 2026?

The Spain heat pump market is expected to reach USD 956.41 million by 2031, up from an estimated USD 744.84 million in 2026, reflecting a 5.13% CAGR over the 2026-2031 period.

Which capacity range is scaling quickest in Spanish industry?

Units above 200 kW are climbing at a 5.44% CAGR as food, chemical, and textile firms electrify process heat up to 160 °C.

Where are the strongest regional incentives located?

Catalonia and Barcelona offer the richest subsidies, covering up to 75% of project cost in some multi-family retrofits.

What technology shift is shaping future product design?

The move to R290 propane refrigerant is reducing global warming potential and promises equipment cost cuts of up to EUR 800 per unit by 2028.

How does hybrid technology fit Spanish decarbonization goals?

Hybrids allow property owners to retain gas boilers for rare peak hours, providing a cost-effective bridge until grid upgrades can handle full electrification.

Why are commercial buyers accelerating purchases?

Access to green loans and heat-as-a-service contracts that remove upfront cost push hotels, hospitals, and offices toward rapid electrification.

Page last updated on: